Recent estimates of UK GDP growth represent an early draft of economic history that will be revised, often substantially, over time. OECD found that initial estimates of UK GDP growth have tended to be revised up over time. This box also highlights revisions to estimates of US and UK productivity growth between July and November 2015, and the substantial productivity shortfall relative to the US and relative to the pre-crisis trend in the UK.

This box is based on BEA productivity and BLS labour productivity data from September 2015 and November 2015 respectively.

As we always stress, recent estimates of UK GDP growth represent an early draft of economic history that will be revised, often substantially, over time. Such revisions are not unique to the UK – a similar process is carried out by statistical offices around the world.

A recent OECD paper looked at the properties of GDP revisions to assess the accuracy and bias in early estimates.a It found that in almost all countries – including the UK – initial estimates have tended to be revised up over time. Compared to other OECD countries, the downward bias in UK early estimates was found to be slightly less than average and not statistically significant. The US stood out as the only country where initial GDP estimates tended to be revised down.

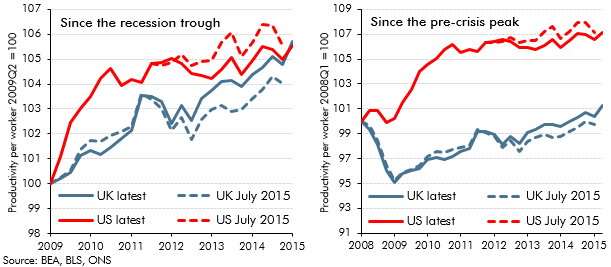

This pattern of revisions has played out in the latest UK and US GDP revisions. As the left-hand panel of Chart A shows, viewed in terms of GDP-per-worker, the vintage of GDP figures available at the time of our July forecast suggested that US productivity growth had been much stronger than the UK’s since the beginning of the recovery in mid-2009. Following upward revisions to UK GDP growth and downward revisions to US GDP growth, productivity growth over that period is now estimated to have been similar on average in both countries. Future revisions may change this again.

More significantly, though, the right-hand panel shows that the latest revisions are small relative to the fall in productivity that the UK experienced in the immediate wake of the recession, which was not mirrored in the US (where employment fell more sharply). Looking at the period since the pre-crisis peak, the recent revisions still leave the UK with a substantial productivity shortfall relative to the US and relative to the pre-crisis trend in the UK. As set out in Chapter 3, prospects for productivity growth represent the most important uncertainty in our economy forecast.

Chart A: Current and previous estimates of US and UK productivity growth

This box was originally published in Economic and fiscal outlook – November 2015