The outlook for trend productivity is one of the most important and uncertain forecast judgements. Successive past forecasts for trend productivity have proven to be too optimistic as productivity growth has continued to disappoint. In this box we explored two alternative scenarios for trend productivity: One where the recent weakness in trend productivity growth persists throughout the forecast period and one where it proves to be entirely cyclical and is offset by higher growth in the near-term.

This box is based on OBR data from March 2025 .

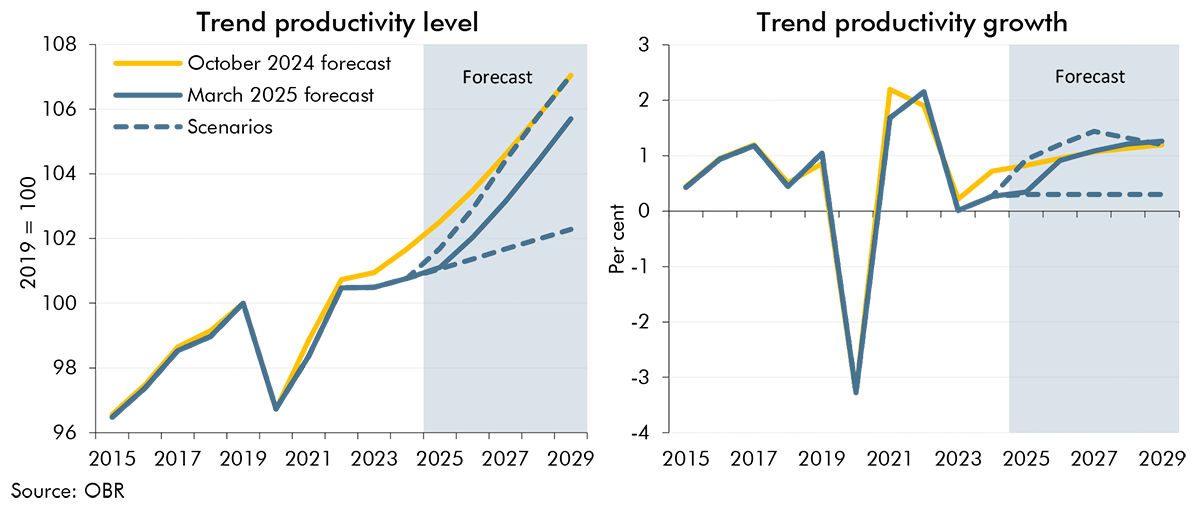

The outlook for trend productivity is one of the most important and uncertain forecast judgements. Successive past forecasts for trend productivity have proven to be too optimistic as productivity growth has continued to disappoint. So, over the past 10 years, we have lowered our medium-term productivity growth assumption from around 2.2 per cent to 1¼ per cent. Given the measurement and volatility issues with recent outturn data, alongside the wider economic risks that could impact future productivity (such as those surrounding global trade), the uncertainty around our productivity assumption remains high.

To illustrate this uncertainty, the following scenarios show how different judgements about the outlook for trend productivity would affect the economic and fiscal forecast (Chart A):

- In an upside scenario, trend productivity growth averages 1.2 per cent a year from 2025 to 2029, 0.3 percentage points higher than in the central forecast. Under this scenario, the level of productivity in 2029 is unchanged from the October forecast and 1.3 per cent higher than in our current central forecast. This would be consistent with the view that the news since October only reflects temporary factors, such as cyclical weakness or measurement issues. Therefore, the level and growth rate of medium-term trend productivity are both unchanged after a period of higher catch-up growth.

- In a downside scenario, trend productivity growth remains at 0.3 per cent a year throughout the forecast. Under this scenario, the level of productivity in 2029 is 3.2 per cent lower than the central forecast. This is consistent with the weakness in trend productivity growth in 2024 continuing over the whole forecast period. The level and the growth rate of trend productivity would both be lower in the medium term.

We discuss the fiscal implications of these scenarios in Chapter 7.

Chart 2A: Trend productivity scenarios

This box was originally published in Economic and fiscal outlook – March 2025