"It is the duty of the Office to examine and report on the sustainability of the public finances"

Economic and fiscal outlook – March 2025

The latest update of our forecasts was published on 26 March 2025 in the March 2025 Economic and fiscal outlook. Read the Executive summary for the key messages of our forecast or the full report on our website.

Chapter 2 sets out our forecasts for the economy over a five-year horizon. We cover our latest forecast changes in light of recent developments and the effect of policies in the Spring Statement.

In Chapter 3, details the policy measures announced since October 2024, provides an update on selected previous measures, and discusses policy risks and uncertainties.

Chapters 4-6 sets out our forecasts for receipts and public spending over a five-year horizon. We also explain our loans and other financial transactions forecasts. All this, together with new policy decisions, builds the outlook for borrowing and debt.

In Chapter 7, we assess the Government against its fiscal targets and evaluate their likelihood of being met on current policy under our central forecast. We consider the uncertainty around our economic and fiscal forecasts and the risks to the Government meeting its targets. We also test the sensitivity of our fiscal forecasts in an alternative economic scenario.

Annex A contains detailed summary tables setting out our economic and fiscal forecasts.

Information or data which has been released alongside the Economic and fiscal outlook or as a result of external requests, since the original publication of the main document.

This Economic and fiscal outlook (EFO) sets out our central forecast and the uncertainties that surround it for the five years to 2029-30, taking account of recent data and government policies announced since our last forecast, up to and including the March 2025 Spring Statement. The forecasts presented in this document represent our collective view as the three independent members of the OBR’s Budget Responsibility Committee (BRC). We take full responsibility for the judgements that underpin them and for the conclusions we have reached.

As always, we have been greatly supported in our work by the staff of the OBR. We are very grateful for their hard work and expertise. We have also drawn on the work and expertise of officials across government in preparing these forecasts. We are grateful for their engagement and insight.

The date for this forecast was announced on 16 December, giving four weeks more than the ten weeks’ notice required by the Memorandum of understanding between the Office for Budget Responsibility, HM Treasury, the Department for Work and Pensions and HM Revenue and Customs (MoU).

We published the timetable of the key stages of the forecast on 22 January, once it had been agreed by signatories of the MoU. Overall the forecast process for this EFO proceeded smoothly. The exception was the process around welfare and employment support policies, which are a subset of the wider package of reforms and policy ambitions announced in the Pathways to Work Green Paper published on 18 March. Details of the policy package were sent to us very late in the process, and late notice of changes and incomplete analysis hampered our ability to reflect these measures in our forecasts:

Policy costings information on the direct fiscal effects of some measures was received late and without sufficient detail. So far as some of the measures are concerned, we have certified the Government’s estimates of their fiscal effects as reasonable and central, but with a high degree of uncertainty attached to them. So far as one measure is concerned, we certified it only on the basis that it was a provisional estimate that would be subject to more comprehensive analysis prior to our next forecast. This is set out in detail in Chapter 3. In addition, relatively small changes were made to the policy parameters of two welfare measures following the costings certification deadline. As a result, we have not been able to certify these costings but have used the Government’s estimates in this forecast and will return to them in our next forecast.

We were unable to incorporate most of the supply-side impacts of these policies in our economy forecast due to insufficient information from the Government on the policy details and analysis of their likely economic effects. We were not, in the limited time available, able to develop our own analysis.We will therefore incorporate an estimate of these impacts in our next forecast.

On this basis, we plan to work with the Treasury and DWP to further scrutinise both the direct and indirect effects of these welfare and employment support policies ahead of our next forecast, alongside the effects of any further measures from the Green Paper that have been sufficiently developed.

The recommendations of our review into the preparation of the March 2024 forecast for departmental expenditure limits (DEL), which were published alongside our previous EFO in October, have continued to be implemented in the production of this forecast.

The timetable for the production of this forecast was as follows:

OBR staff prepared an initial economy forecast, drawing on data released since our previous forecast in October 2024 and incorporating our preliminary judgements on the outlook for the economy. This economy forecast was sent to the Chancellor on 21 January.

Using the economic determinants from this forecast (such as the components of nominal income and spending, unemployment, inflation, and interest rates), we commissioned updated forecasts from the relevant government departments for the various tax and spending items that in aggregate determine the position of the public finances. We discussed these in detail with the officials producing them, which allowed us to investigate proposed changes in forecasting methodology and to assess the significance of recent tax and spending outturn data. In many cases the BRC requested changes to methodology and/or the interpretation of recent data. This first fiscal forecast was finalised on 3 February, and we sent a note that described the main elements of it to the Chancellor the following day.

As the process continued, we identified further key judgements that we would need to make for our economy forecast. Where we thought it would be helpful, we commissioned analysis from the relevant teams in the Treasury. We then produced a second pre-measures economy forecast, which incorporated the latest data, and the economic implications of our first fiscal forecast.

This second economy forecast provided the basis for the next round of fiscal forecasts. Discussions with HMRC, DWP and other departments gave us the opportunity to follow up our requests for further analysis, methodological changes, and alternative judgements from the previous round. We finalised our second fiscal forecast on 18 February and sent a summary of the forecast to the Chancellor the following day.

In parallel, we undertook a process of engagement and analysis to assess the set of policy measures to be announced before or alongside the forecast that we deemed could have specific effects on our economy forecast. This involved several rounds of engagement with the Treasury and other government departments as both the specification of policies, and our assessment of their impact were refined.

We also scrutinised the costing of individual tax and spending measures announced since our October 2024 forecast. As usual, OBR staff and the BRC requested further information and/or changes to almost all the draft costings prepared by HMRC, DWP and other departments.

We then produced a third and final pre-measures economy forecast, in which we took on the latest data and incorporated judgements embodied in our fiscal forecast. This final pre-measures economy forecast was based on energy and financial market data averaged over the 10 working days to 12 February. It was sent to the Treasury on 24 February.

Alongside the development of the final economy forecast we made an initial assessment of the economic and fiscal effects of the emerging policy package. This built on earlier analysis that allowed us to factor in an initial package of measures that was provided by the Treasury on 5 March. We incorporated this package into a preliminary post-measures forecast, in order to provide an early view on the effect of policy measures on the economy and public finances, which we sent to the Chancellor on 10 March. This forecast round was produced using our internal ready-reckoner models (rather than being sent to departmental forecasters).

In line with the agreed timetable, on 12 March the Treasury provided the final package of measures that would cause movements in our economy forecast. We sent the resulting final economy forecast to the Treasury on 17 March and a near-final fiscal forecast on 18 March. Final policy decisions were provided by the Treasury on 19 March and our forecast was then finalised on 21 March and sent to the Treasury on the same day.

The Treasury made a written request, as provided for in the MoU between us, that we provide the Chancellor and an agreed list of her special advisers and officials with a near-final draft of the EFO on 21 March. This allowed the Treasury to prepare the Chancellor’s statement and accompanying documents. We also provided pre-release access to the full and final EFO on 24 March.

During the forecasting period, the BRC held dozens of scrutiny and challenge meetings with officials from other departments, in addition to numerous further meetings at staff level and with external stakeholders. We have been provided with all the information and analysis that we requested and have come under no pressure from Ministers, advisers, or officials to change any of our conclusions. The BRC met with the Chancellor on two occasions to discuss the forecast over the course of its production (on 5 February and 19 February) and one of the Chancellor’s special advisers attended three of the analytical focus groups that we held with Treasury officials. A full log of our substantive contact with Ministers, their offices and special advisers can be found on our website. This includes the list of special advisers and officials who received the near-final draft of the EFO on 21 March.

We would be pleased to receive feedback on any aspect of the content or presentation of our analysis. This can be sent to [email protected].

The Budget Responsibility Committee

Richard Hughes, Professor David Miles CBE and Tom Josephs

Chapter 1: Executive summary

Overview

1.1 The economic and fiscal outlook has become more challenging since the Autumn Budget. Domestic output stagnated in the second half of 2024 and business and consumer confidence have trended lower recently. European energy prices have risen again, and government bond yields are up by around ½ a percentage point. The outlook has also become more uncertain with two geopolitical risks highlighted in our 2022 Fiscal risks and sustainability report beginning to crystallise: upward pressure on defence spending and a tightening of global trade restrictions. And recent UK population, labour force, and output data do not provide a clear signal about domestic economic prospects.

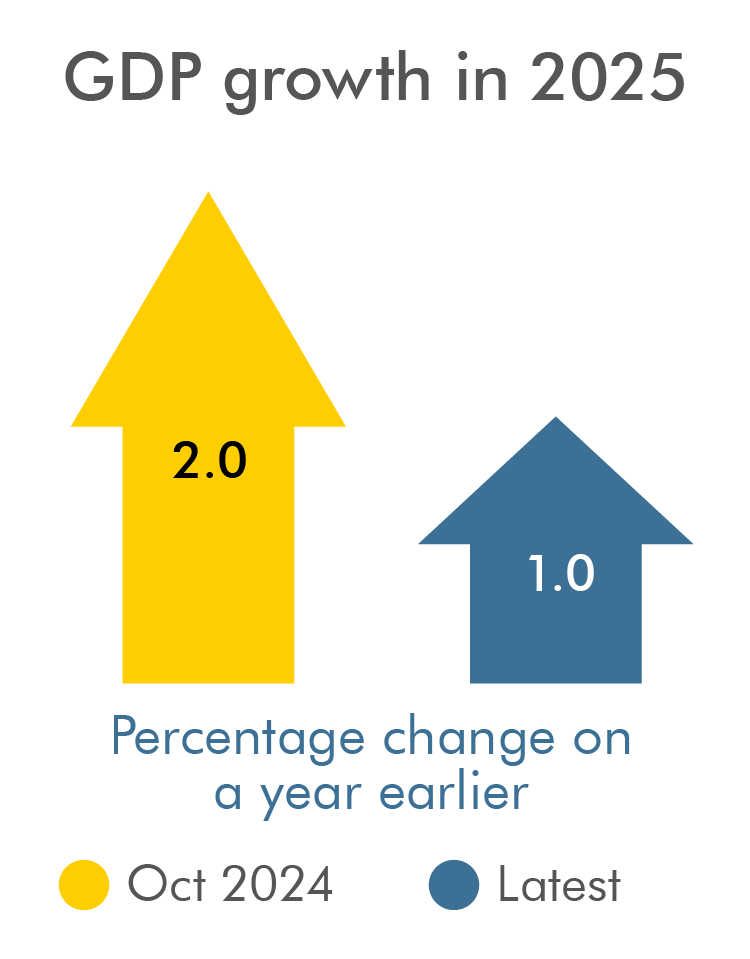

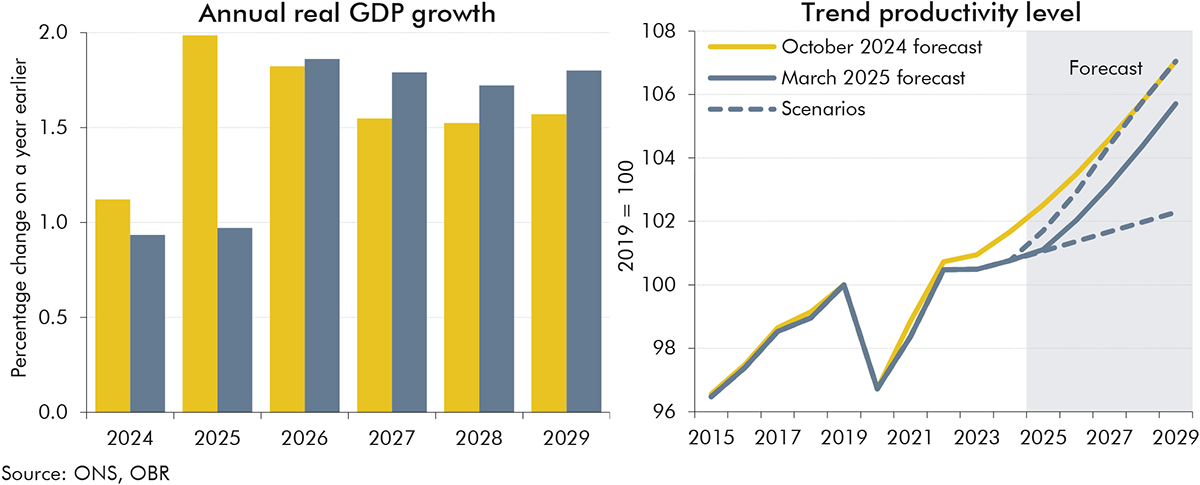

1.2 Against this more challenging and uncertain backdrop, we now expect real GDP growth of 1.0 per cent this year, half the rate in our October forecast, before it recovers to average around 1¾ per cent over the rest of the decade. While the Government’s planning reforms deliver a modest boost to the level of potential output of 0.2 per cent in 2029, its cumulative growth between 2023 and 2029 is still ½ a percentage point lower than we projected in October, and the level of productivity is over 1 per cent lower. Higher energy and food prices and more persistently high wage growth cause inflation to rebound to a quarterly peak of 3.7 per cent in mid-2025, before returning to target over the rest of the forecast.

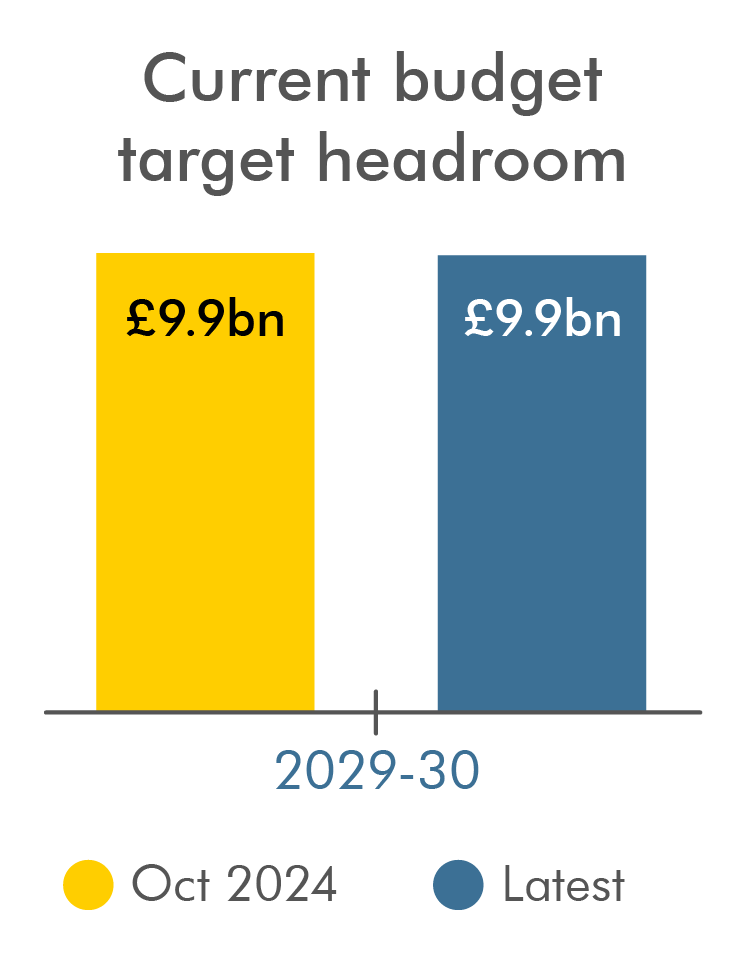

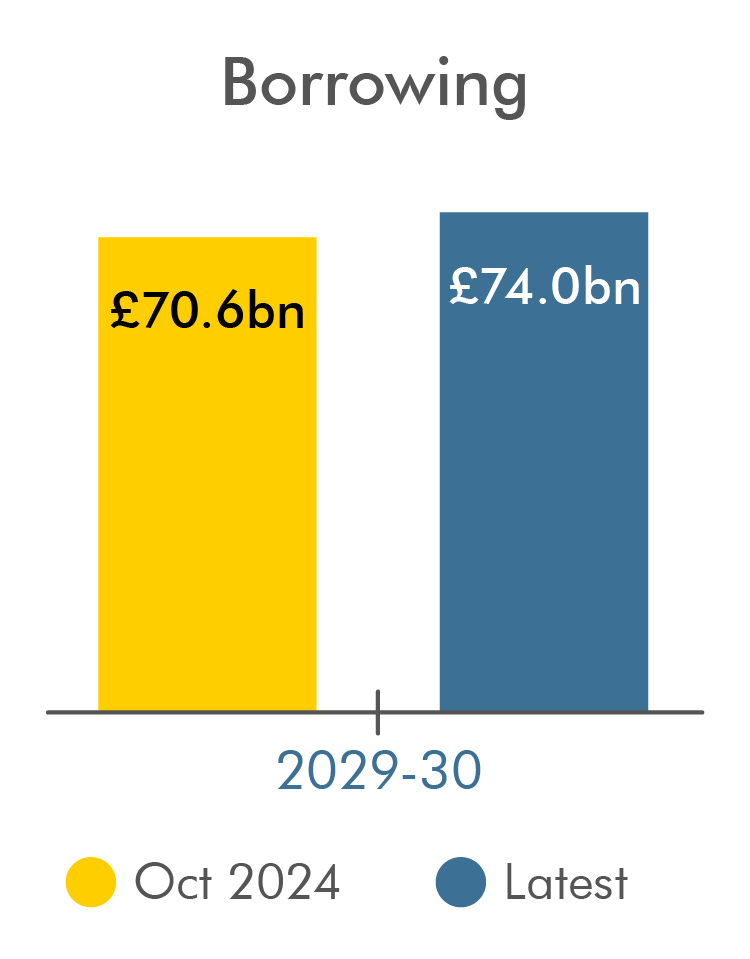

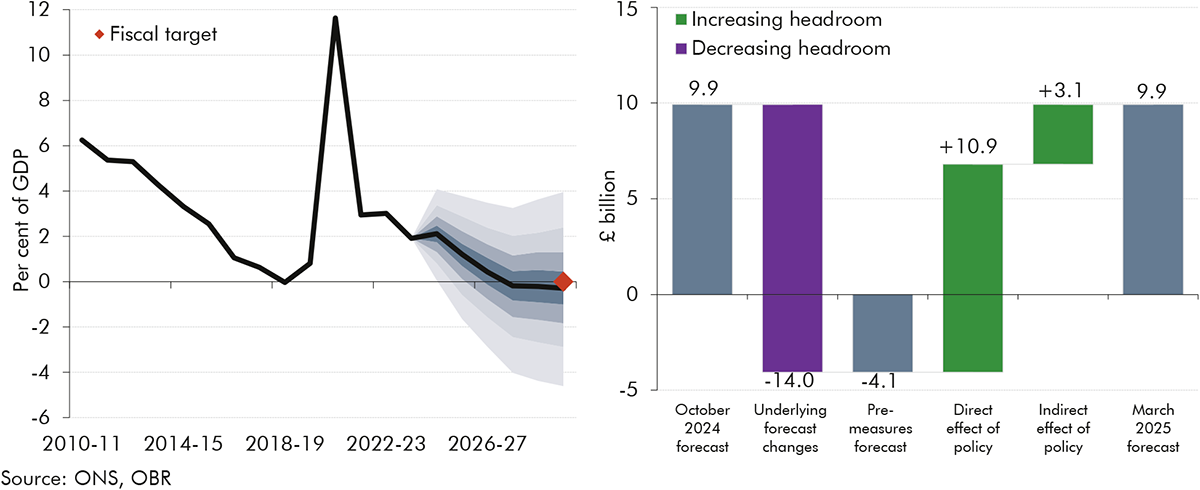

1.3 The underlying fiscal outlook has also deteriorated since October. Higher debt interest payments and weaker-than-expected receipts take the current balance from a surplus of £9.9 billion to a deficit of £4.1 billion in 2029-30, before accounting for new policies. Government policies, notably the direct savings from welfare reforms and the reduction in day-to-day departmental spending, and the indirect boost to receipts from planning reforms, raise £14.0 billion in 2029-30, offsetting the underlying deterioration. This means that the fiscal rules for a current balance and for net financial liabilities to be falling in 2029-30 are both met by similar small margins to October of £9.9 billion and £15.1 billion respectively. But borrowing is projected to be £3.5 billion higher and debt 0.6 per cent of GDP higher at the end of the decade than in our October forecast.

1.4 Significant uncertainty surrounds domestic and global economic developments. If the projected recovery in UK productivity growth fails to materialise, and it continues to track its recent trend, then output would be 3.2 per cent lower and the current budget would be 1.4 per cent of GDP in deficit by the end of the decade. A 0.6 percentage point increase in Bank Rate and gilt yield expectations across the forecast would eliminate current balance headroom. And if global trade disputes escalate to include 20 percentage point rises in tariffs between the USA and the rest of the world, this could reduce UK GDP by a peak of 1 per cent and reduce the current surplus in the target year to almost zero.

Economic outlook

1.5Since the October forecast, developments in outturn data and indicators of business, consumer and market sentiment have, on balance, been negative for the economic outlook. The ONS has revised up the historical size of the UK workforce by 1.5 per cent (½ a million) in 2024. It also revised up the level of real GDP by 0.8 per cent in mid-2024. But real GDP growth largely stagnated over the second half of 2024 rather than continuing to grow, as we expected in the October forecast, meaning the level of output was broadly in line with our previous expectations by the end of 2024. The net effect of these developments was that the measured level of productivity (output per hour worked) at the end of 2024 was 1.3 per cent lower than in the October forecast. In recent months, indicators of both business and consumer confidence have also trended lower. And European gas prices have risen while government bond yields have increased across many advanced economies.

1.6In our central forecast, real GDP is now projected to grow by 1.0 per cent in 2025, half the 2.0 per cent assumed in October. Around one-third of the lower growth this year reflects what appears to be structural weakness. This is concentrated in productivity, and its trend level is 1.3 per cent lower at the forecast horizon than expected in October. The remaining two-thirds is due to what appear to be cyclical, temporary, factors including higher interest rate expectations, increases in gas prices, and elevated uncertainty. GDP growth is expected to accelerate to 1.9 per cent in 2026 as monetary policy eases, gas prices fall back, and slack in the economy is taken up. Growth then averages 1¾ per cent over the rest of the decade. Government policies temporarily boost demand by 0.1 per cent in the middle of the forecast and permanently raise supply by 0.2 per cent at the forecast horizon. Overall, the permanent hit to productivity is partly offset by stronger workforce growth, leaving cumulative growth in potential output between 2023 and 2029 ½ a percentage point lower than forecast in October. There remains considerable uncertainty about how to interpret recent developments in UK labour force, GDP, and productivity data, and in US and global trade policy. We therefore explore the economic and fiscal implications of alternative scenarios for both domestic productivity growth and global tariff policies.

Chart 1.1: Real GDP growth and trend productivity level

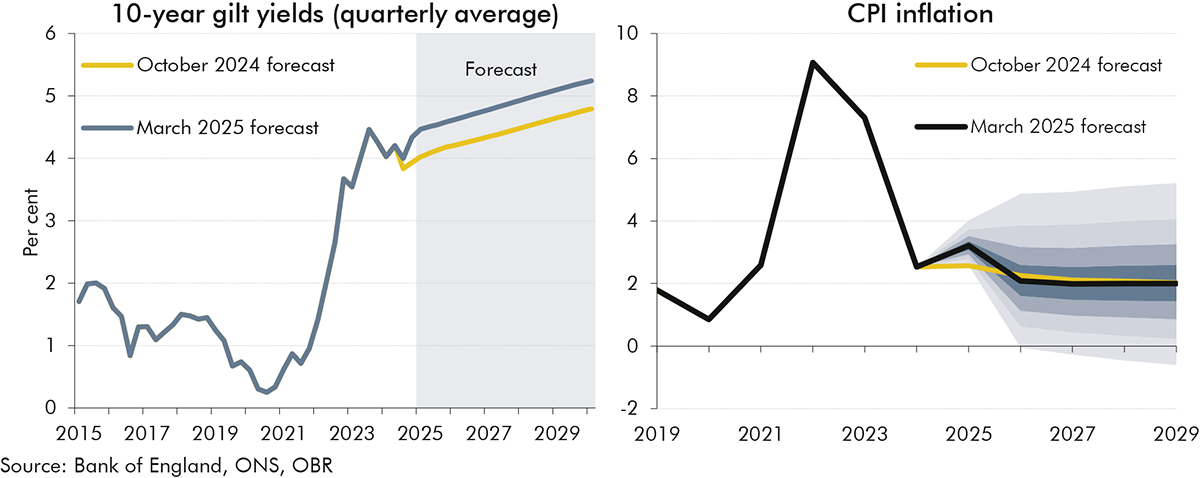

1.7Interest rate expectations have risen since our October forecast. Bank Rate is expected to fall from its current level of 4.5 per cent to 3.8 per cent from mid-2026 onwards. Expectations are, on average, around a ¼ percentage point higher than in the October forecast. UK 10-year gilt yields have also risen by around ½ a percentage point since early October with similar moves in many other advanced economies. Interest rate expectations have remained highly volatile over this period, with 10-year gilt yields varying by a full percentage point between 3.9 and 4.9 per cent.

1.8Annual CPI inflation is forecast to rise from 2.5 per cent in 2024 to 3.2 per cent in 2025, 0.6 percentage points higher than forecast in October. Wholesale gas prices are expected to peak at around 130 pence a therm in 2025, which is around 30 per cent higher than forecast in October. Oil prices are forecast to average 74 dollars a barrel in 2025, 4 per cent higher than in October. The resulting increases in the Ofgem price cap, coupled with higher food prices and the increase in regulated water bills, are expected to push monthly inflation up to a peak of 3.8 per cent in July 2025. From 2026 onwards, CPI inflation falls rapidly back to around the 2.0 per cent target as energy prices drop, food price inflation falls, and wage growth eases back from currently elevated rates.

Chart 1.2: Gilt yields and CPI inflation

1.9We expect the unemployment rate to peak at 4.5 per cent (1.6 million people) in 2025 as spare capacity opens up, before falling to its estimated structural rate of 4.1 per cent in 2028. This is 0.4 percentage points (160,000 people) higher in 2025 than assumed in our October forecast, due to a larger negative output gap (greater excess supply) in the near term. Having fallen by over a percentage point since 2019, the employment rate is forecast to decline slightly further from 60.5 per cent in the second half of 2024 to 60.2 per cent in 2029. This is because population ageing outweighs the effects of the forthcoming rise in the state pension age, and a reduction in inactivity due to caring (from a falling birth rate and expanded childcare provision). But this level is 0.3 percentage points higher than forecast in October, due to ONS revisions and recent data suggesting the current trend participation rate is higher than we previously thought. While our fiscal forecast takes account of the direct fiscal costs of some of the welfare policies in the Government’s Pathways to Work Green Paper and their indirect effects on aggregate demand, we have not incorporated most of their supply-side impacts on the labour market. This was due to insufficient information from the Government on the policies announced and analysis of their likely economic effects. We will incorporate our estimate of these impacts in our next forecast.

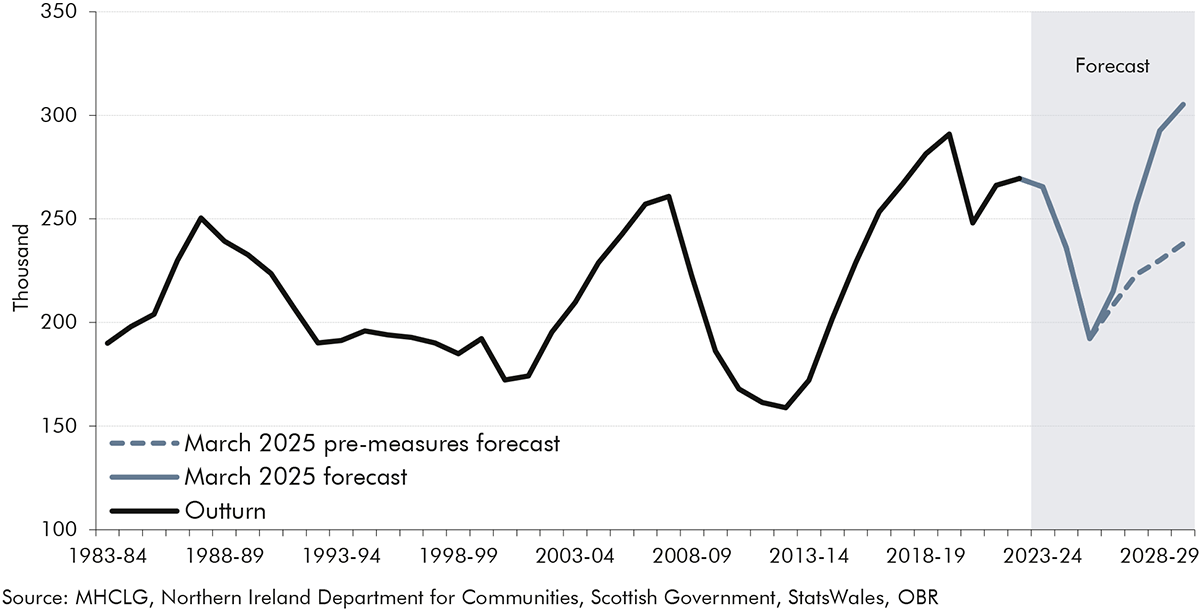

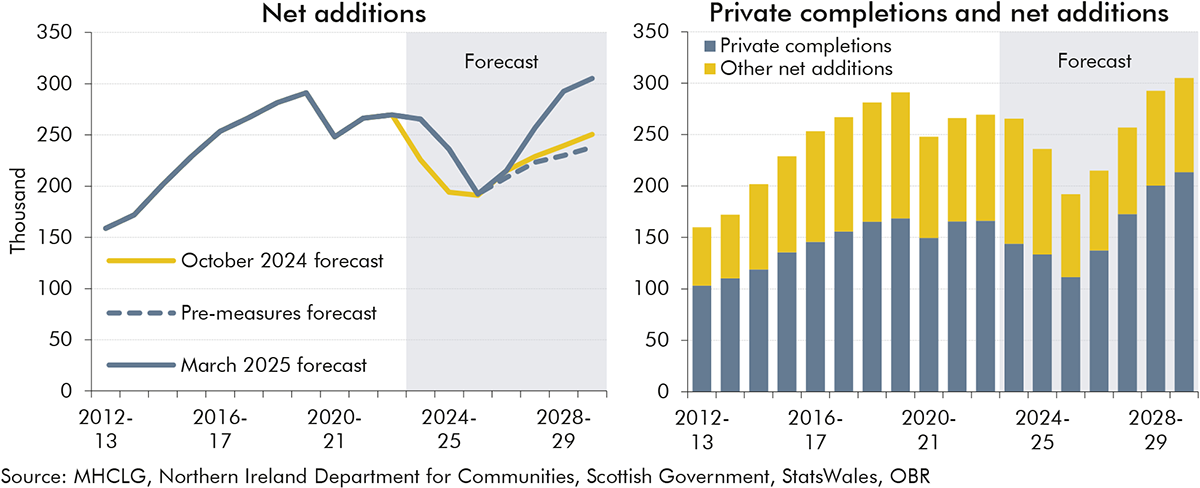

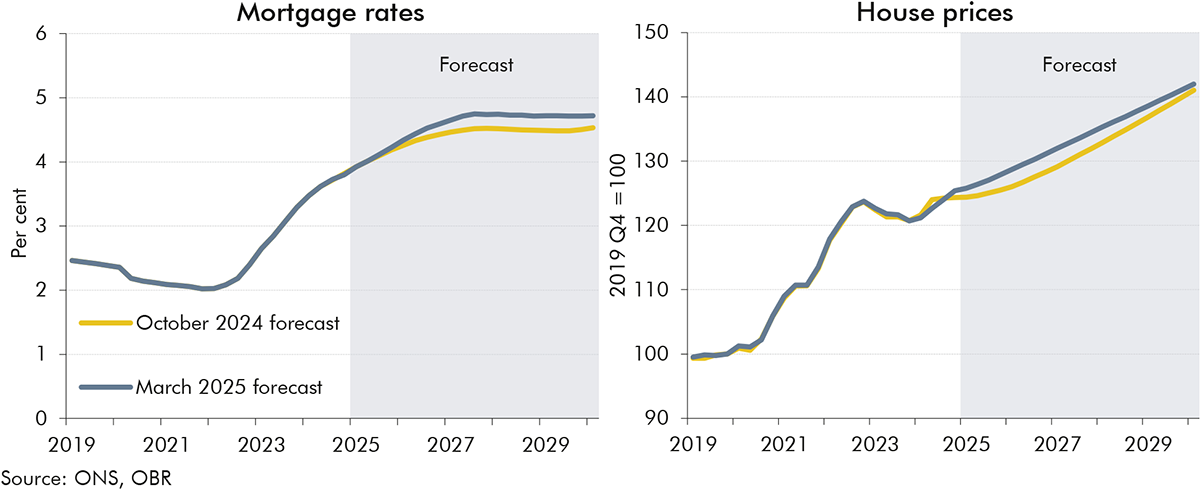

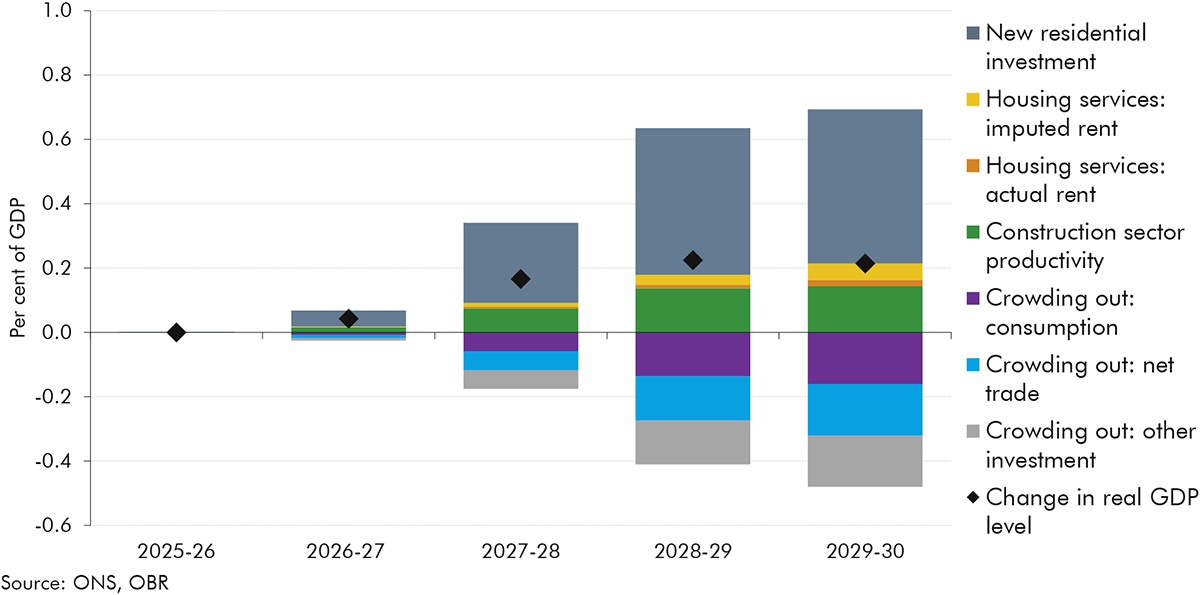

1.10From a 12-year low in 2025-26, net additions to the UK housing stock are forecast to reach 305,000 a year by the end of the decade. From 2025-26 to 2029-30, we project around 1.3 million cumulative net additions to the housing stock. Of this, we estimate an additional 170,000 are due to the Government’s reforms to the National Planning Policy Framework, increasing the total housing stock by around 0.5 per cent in 2029-30. By the fifth year of the forecast, we expect these reforms could add 0.2 per cent to the level of potential output thanks to a boost in the productivity of residential construction and the increased flow of housing services from the higher stock of houses. Over a longer horizon we would expect these effects to build to 0.4 per cent by 2034-35, and we would anticipate a further additional benefit from greater labour mobility and agglomeration effects, adding just under 0.1 per cent to potential GDP by 2034-35.

Chart 1.3: Net additions to the UK housing stock

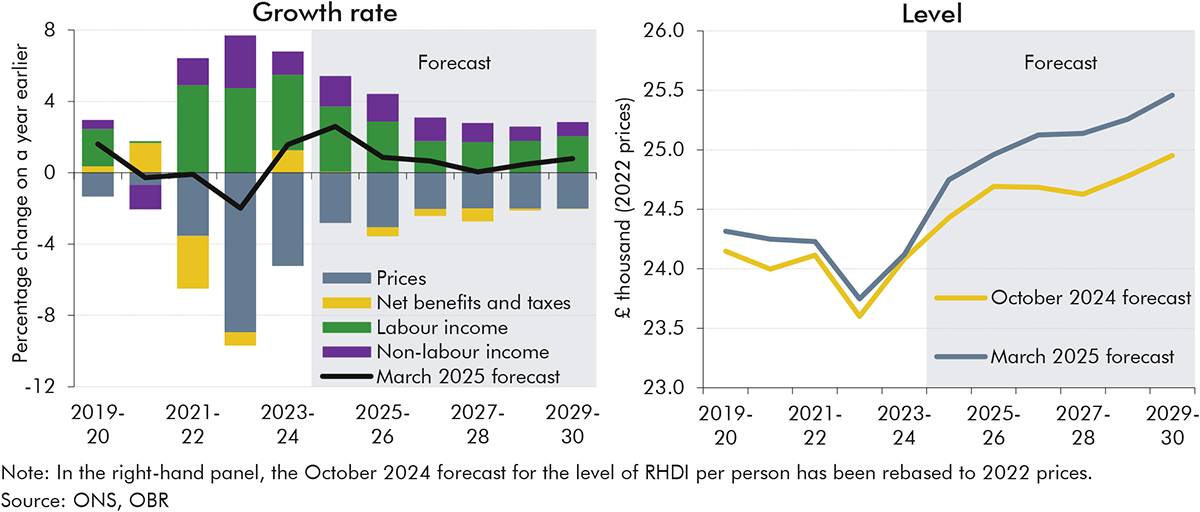

1.11After falls of 0.9 per cent in 2023 and 0.1 per cent in 2024, real GDP per person is expected to recover slightly with growth of 0.3 per cent in 2025, before averaging 1.4 per cent over the rest of the forecast. Nominal earnings growth is forecast to ease from 4.7 per cent in 2024 to 4.3 per cent in 2025, 0.7 percentage points stronger than our October forecast. Nominal earnings growth then averages just over 2 per cent a year from 2026 as the labour market loosens, and firms rebuild margins and have more scope to pass on higher costs from the rise in employer National Insurance contributions (NICs) to employees. Real earnings grow by 1.4 per cent in 2025, stagnate in 2026 and 2027, before growth recovers a little to reach 0.5 per cent in 2029. Real household disposable income (RHDI) per person is expected to grow by an average of around ½ a per cent a year from 2025-26 to 2029-30. Compared to our October forecast, stronger wage growth means RHDI per person growth is slightly higher on average.

1.12Average growth in nominal GDP from 2025-26 onwards is broadly unchanged relative to October. But we expect stronger growth in labour incomes, which have a high effective tax rate, thanks to wage settlement expectations continuing to hold up relative to weak productivity growth and falling inflation. Growth in nominal consumption and corporate profits, two of the other important tax bases, is weaker over the forecast than in October.

Fiscal outlook

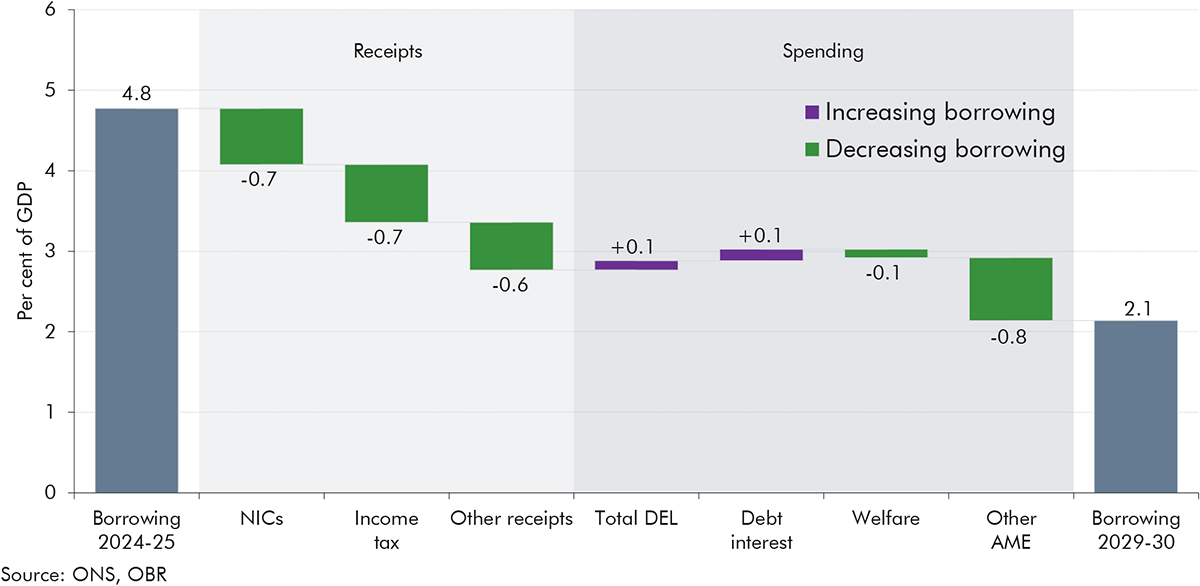

1.13Before the impact of new policies, borrowing is projected to be £13.1 billion higher in 2029-30 than in the October forecast. The most significant drivers of this are higher forecast Bank Rate, gilt yields, and RPI inflation, which together raise debt interest costs by amounts rising to £10.1 billion in 2029-30 relative to October. Other spending areas are also higher in the near term, by £5.2 billion in 2025-26, mainly reflecting higher capital spending by local authorities and public corporations, but these increases taper off in the medium term. Receipts in 2024-25 are expected to be £7.6 billion below the October forecast mainly due to weaker-than-expected self-assessment and onshore corporation tax payments. But higher forecast growth in nominal earnings boosts income tax and NICs over the remainder of the forecast, offsetting much of this in-year shortfall. As a result, total pre-measures receipts are down only £0.6 billion in 2029-30 compared with October. By 2029-30, forecast changes to debt interest and tax drive a slightly larger deterioration in the current balance (revenues minus day-to-day spending) than in borrowing, from a surplus of £9.9 billion in October to a deficit of £4.1 billion, before policy changes.

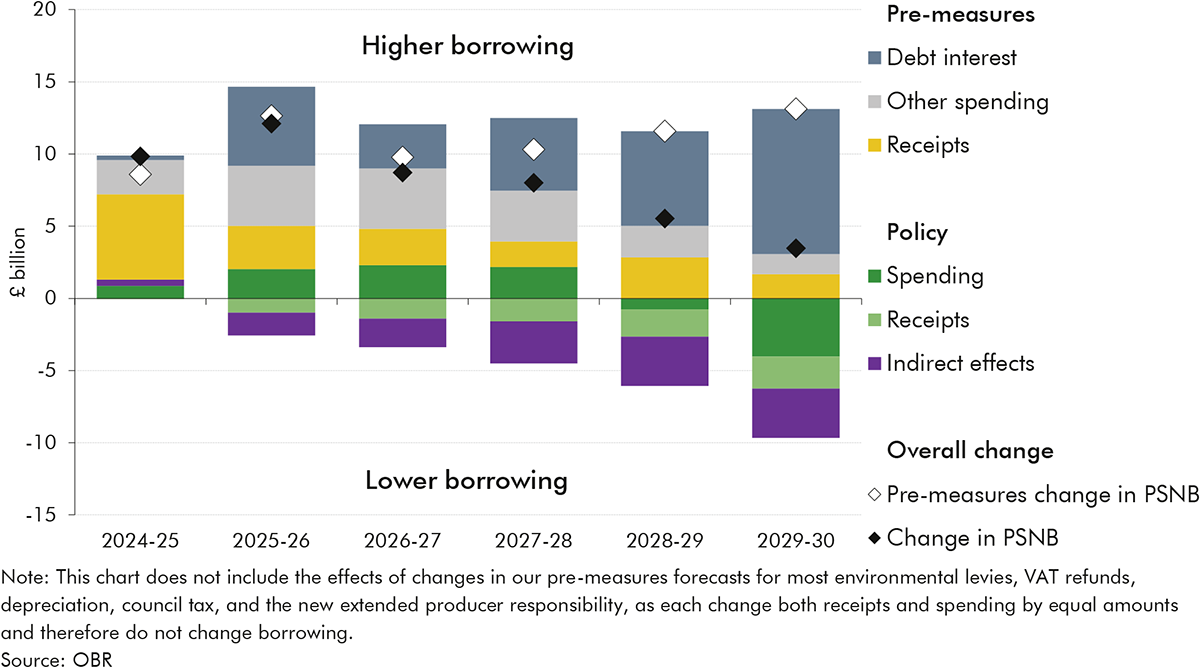

1.14Against this weaker pre-measures fiscal outlook, the Government has announced a set of policies which reduce borrowing by £9.7 billion and improve the current balance by £14.0 billion in 2029-30. These comprise:

Welfare reforms, announced in the Pathways to Work Green Paper, which are estimated to reduce spending by £4.8 billion in 2029-30. The savings come principally from tightening the gateway for personal independence payment (PIP), which is estimated to reduce PIP awards for around 800,000 claimants, and from reducing the generosity of health-related universal credit (UC) for 3 million families. These reductions are partially offset by an increase in the standard allowance for all of the over 6½ million families on UC, and the decision to reverse the 2023 reforms that tightened the work capability assessment (WCA).

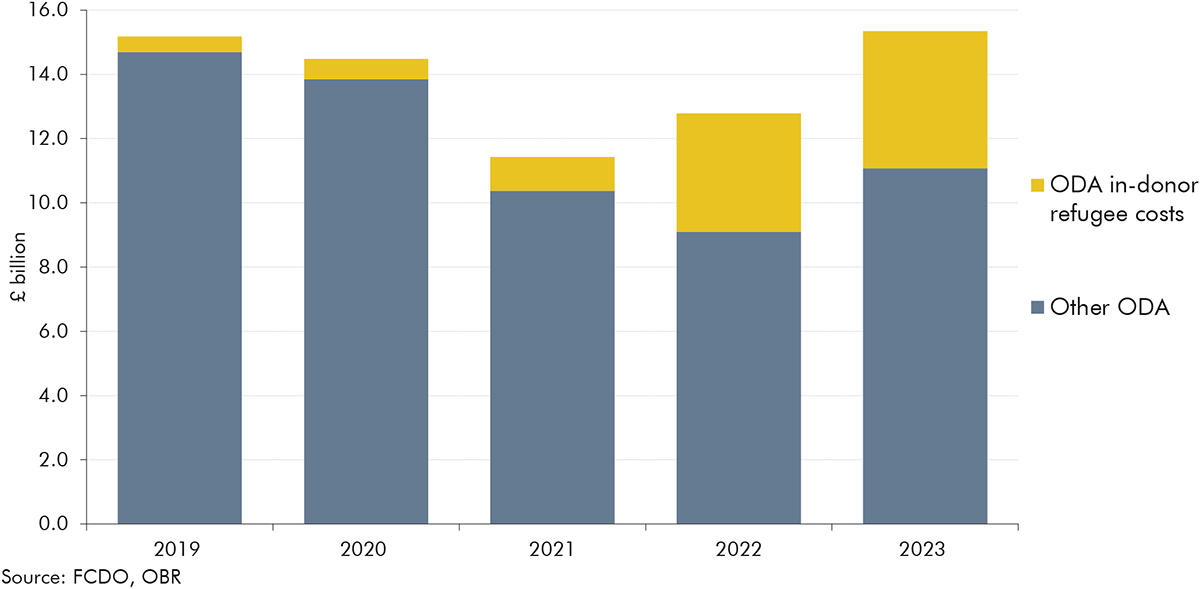

A change in the composition of departmental spending leaves it slightly higher overall by 2029-30. Capital spending is increased across the forecast, reaching £4.4 billion in 2029-30. Current spending is increased in the near term, by £1.7 billion at the peak in 2026-27, to fund new policy commitments including allocation to a ‘transformation fund’. But it is then cut in the final two years of the forecast and by £3.6 billion in 2029-30, despite £1.4 billion of commitments to a DWP employment support package and tax and welfare compliance. The current-to-capital shift in the composition of spending mainly reflects a capital-heavy increase in defence spending to meet the Government’s commitment to spend 2.5 per cent of GDP in 2027-28, which is funded by more current-heavy reductions to Official Development Assistance (ODA).

A small package of tax changes, which raise £2.2 billion in 2029-30. This includes £1.0 billion from tax compliance and debt recovery measures, and £0.7 billion from higher visa and passport fees and increases in council tax, which are offset by higher spending.

The indirect effects of policies lower borrowing by a further £3.4 billion in 2029-30, mainly due to higher receipts as a result of the estimated impact of the Government’s planning reforms on GDP and property transactions.

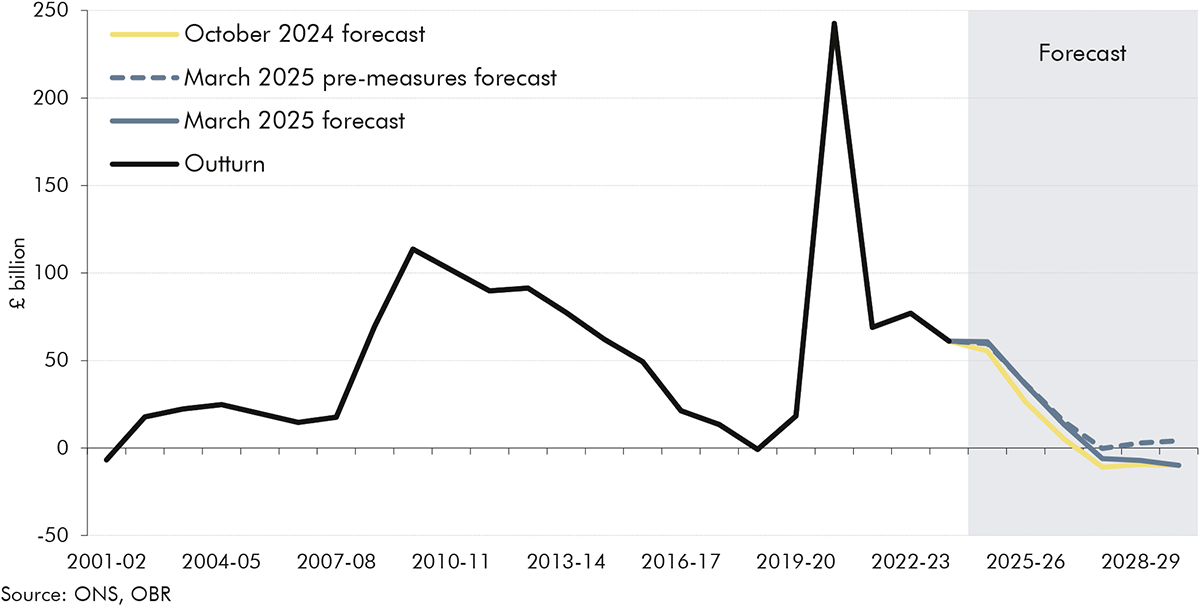

Chart 1.4: Public sector net borrowing: changes since October

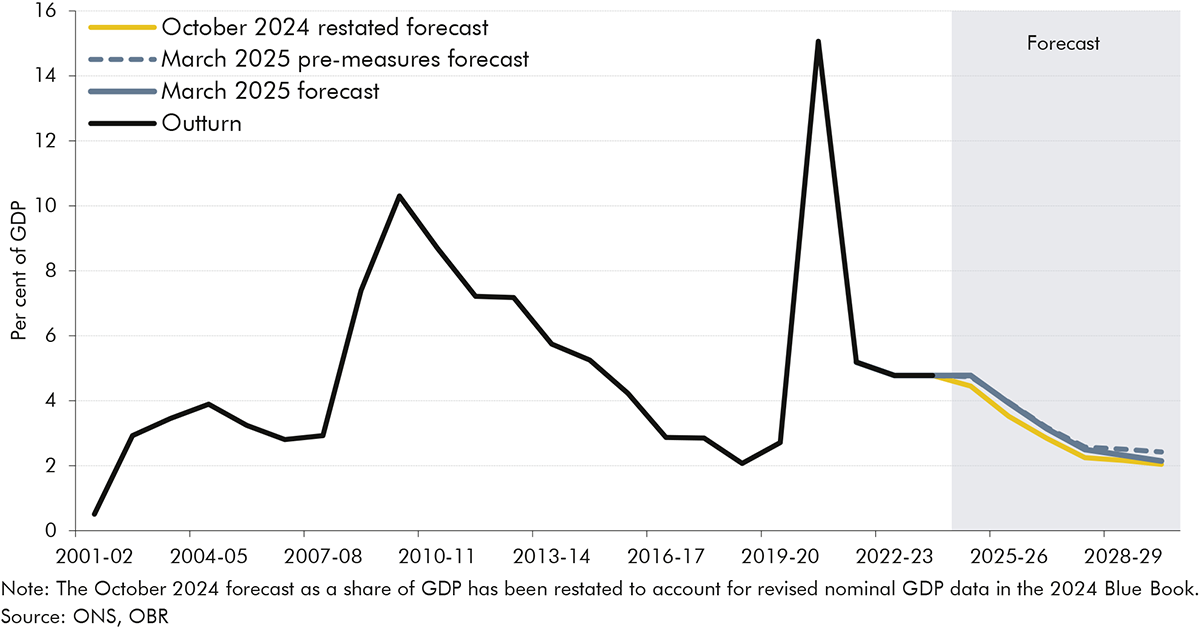

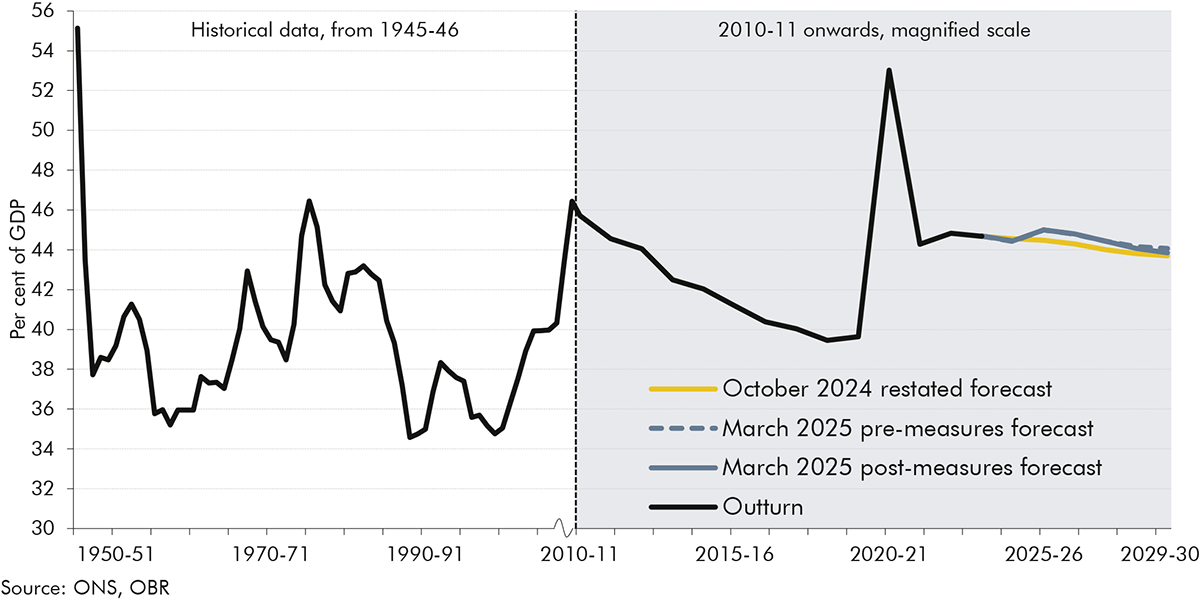

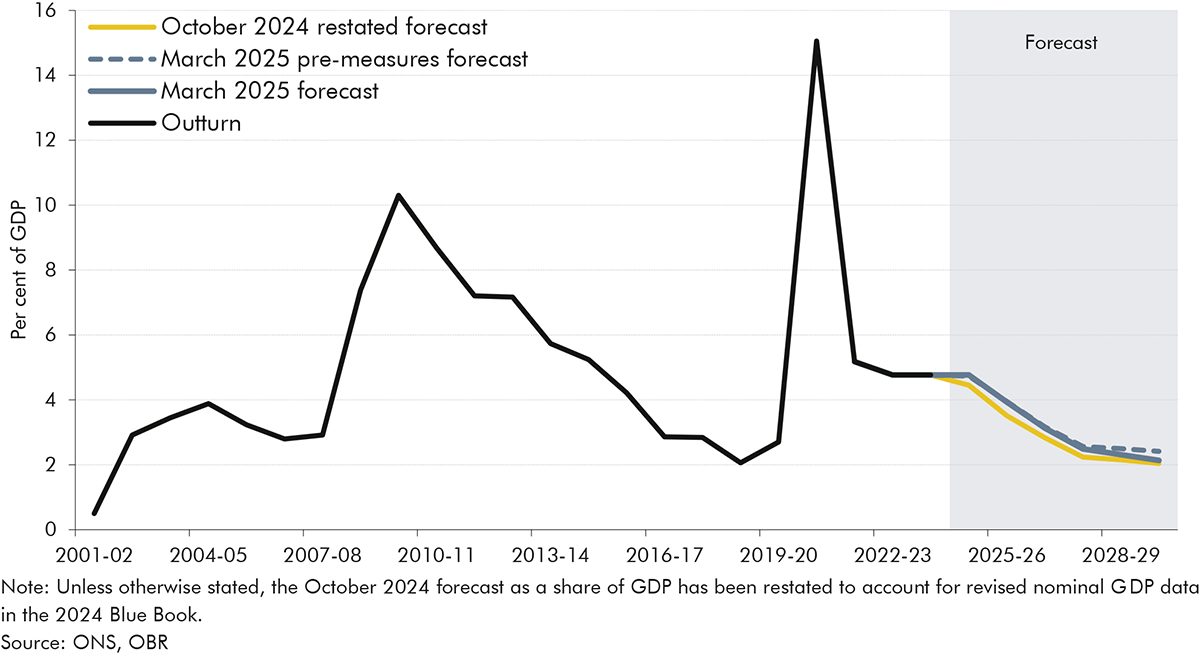

1.15Taking account of both forecast and policy changes, public sector net borrowing (PSNB) is forecast to fall from £137.3 billion (4.8 per cent of GDP) this year to £74.0 billion (2.1 per cent of GDP) in 2029-30. Compared to the October forecast, it is higher by £12.1 billion (0.4 per cent of GDP) in 2025-26 falling to £3.5 billion (0.1 per cent of GDP) in 2029-30. A rising tax take contributes three-quarters to the fall in borrowing as a share of GDP over the next five years, with a reduction in spending as a share of GDP contributing the remaining quarter.

Chart 1.5: Public sector net borrowing

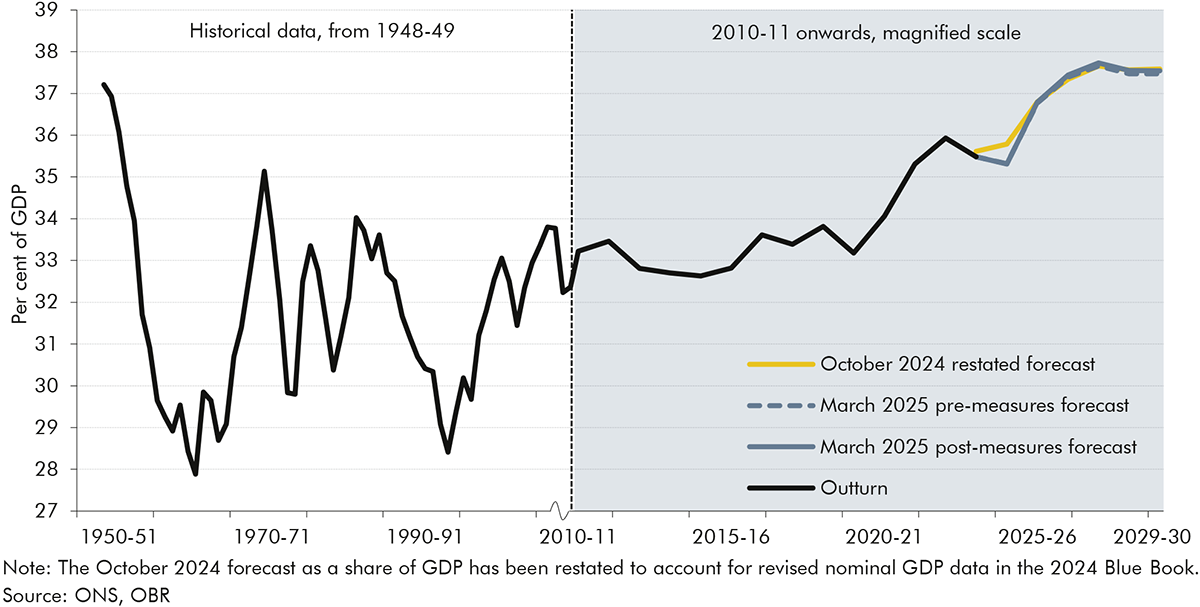

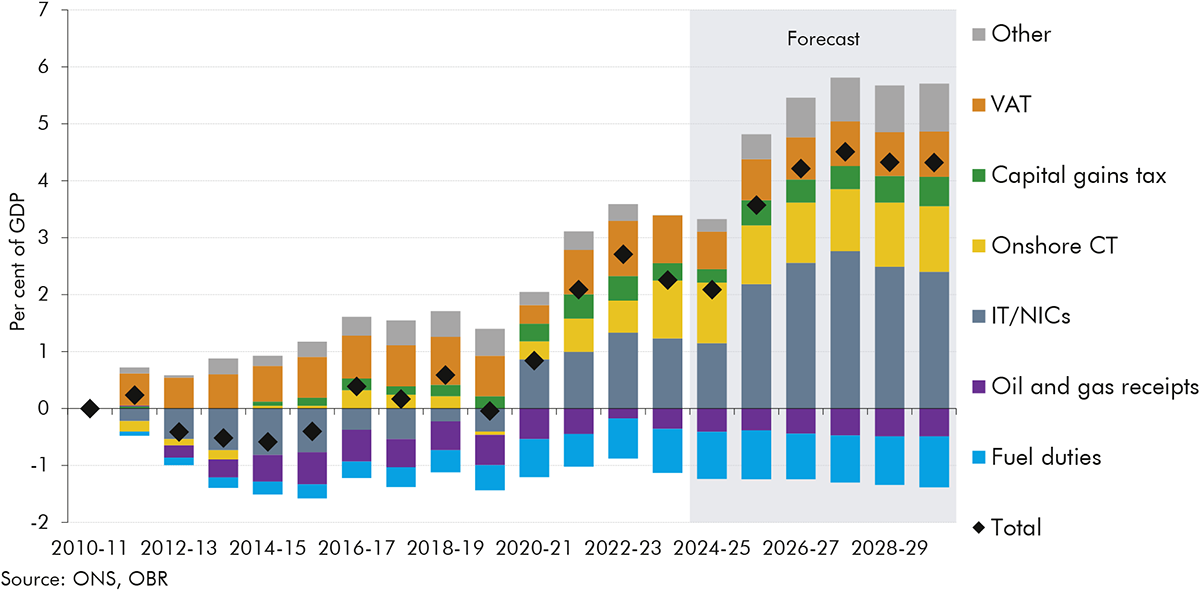

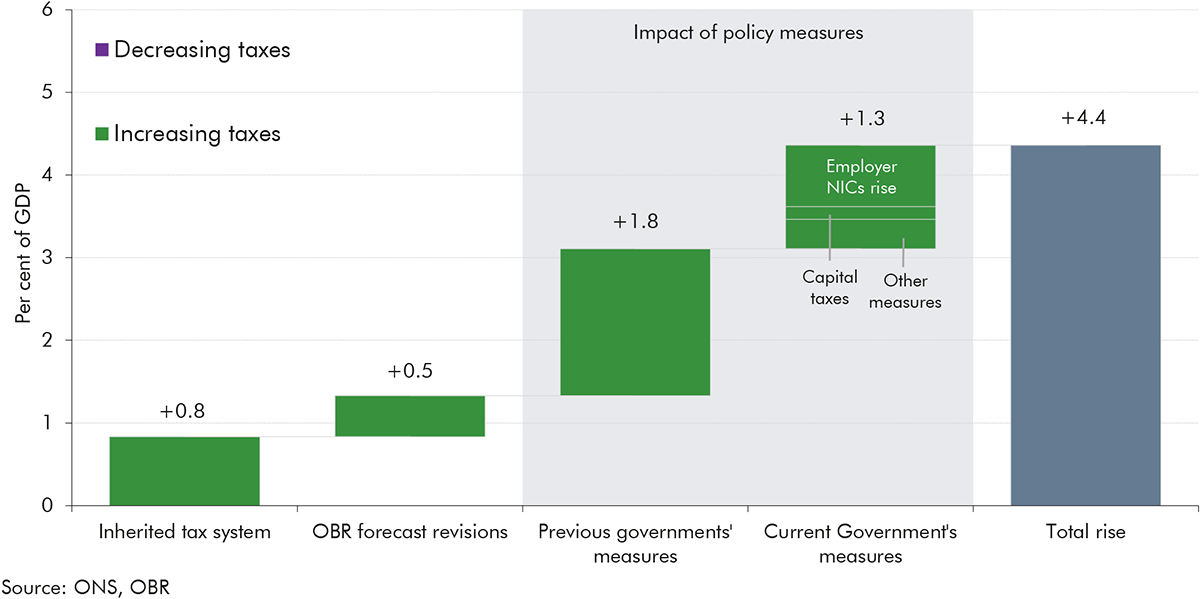

1.16Tax as a share of GDP is forecast to rise from 35.3 per cent this year to a historic high of 37.7 per cent in 2027-28 and remain at a high level for the rest of the forecast. The sharp forecast increase in 2025-26 is largely due to the Autumn 2024 Budget increase in employer NICs, which takes effect in April 2025, and an expected recovery in capital tax receipts. The further forecast rise in the tax take to 2027-28 is mainly due to growth in nominal earnings combined with frozen tax thresholds, further rises in capital taxes, and a boost to receipts from the Temporary Repatriation Facility (TRF) announced at the Autumn Budget as part of the reforms to the non-domicile regime. The tax take is then forecast to level off as personal thresholds are unfrozen, the TRF window closes, and the take-up of electric vehicles reduces fuel duty receipts.

Chart 1.6: National Accounts taxes as a share of GDP

1.17Public spending is forecast to rise to 45.0 per cent of GDP next year, before declining over the remainder of the decade to 43.9 per cent of GDP in 2029-30. Within total spending:

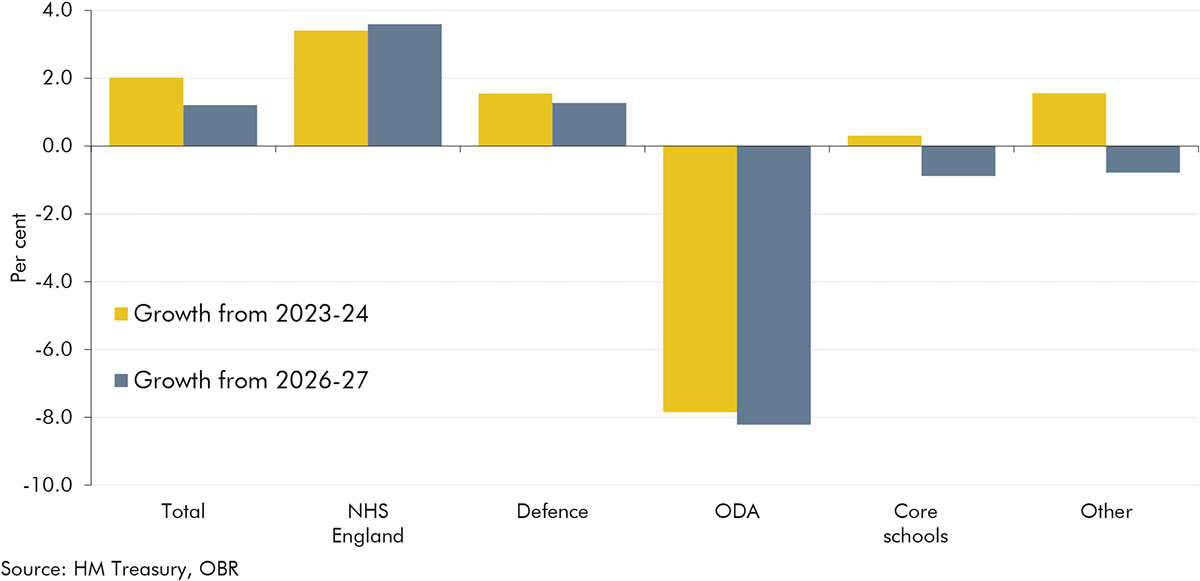

Departmental expenditure limits(DELs) rise over the next three years, from 18.9 per cent of GDP in 2023-24 to a peak of 19.9 per cent of GDP in 2026-27, and then fall back to 19.4 per cent of GDP in 2029-30. Real growth in resource DEL is 4.0 per cent in 2025-26 and then averages 1.2 per cent from 2026-27 onwards, 0.1 percentage points lower than in October. Real growth in capital DEL averages 2.2 per cent over the forecast, and is 1.0 percentage point higher from 2026-27 onwards than in October due to the increase in defence spending.

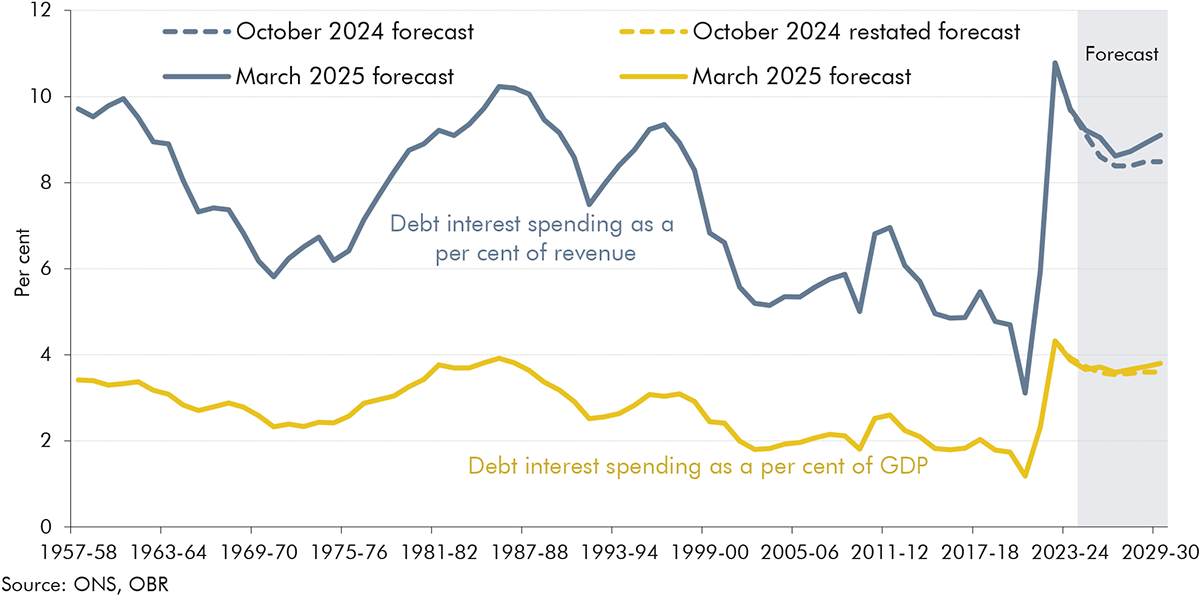

Annually managed expenditure (AME) falls from 25.8 per cent of GDP in 2023-24 to 24.5 per cent of GDP in 2029-30. In the medium term, the decline is driven by welfare spending, which as a result of the latest policy reforms now falls slightly as a share of GDP, and smaller elements of AME including unfunded pensions and student loans. Having risen by around 2 per cent of GDP since 2019-20, debt interest spending is now expected to be broadly flat across the forecast as a share of GDP, rising very slightly in the final years.

Chart 1.7: Public spending as a share of GDP

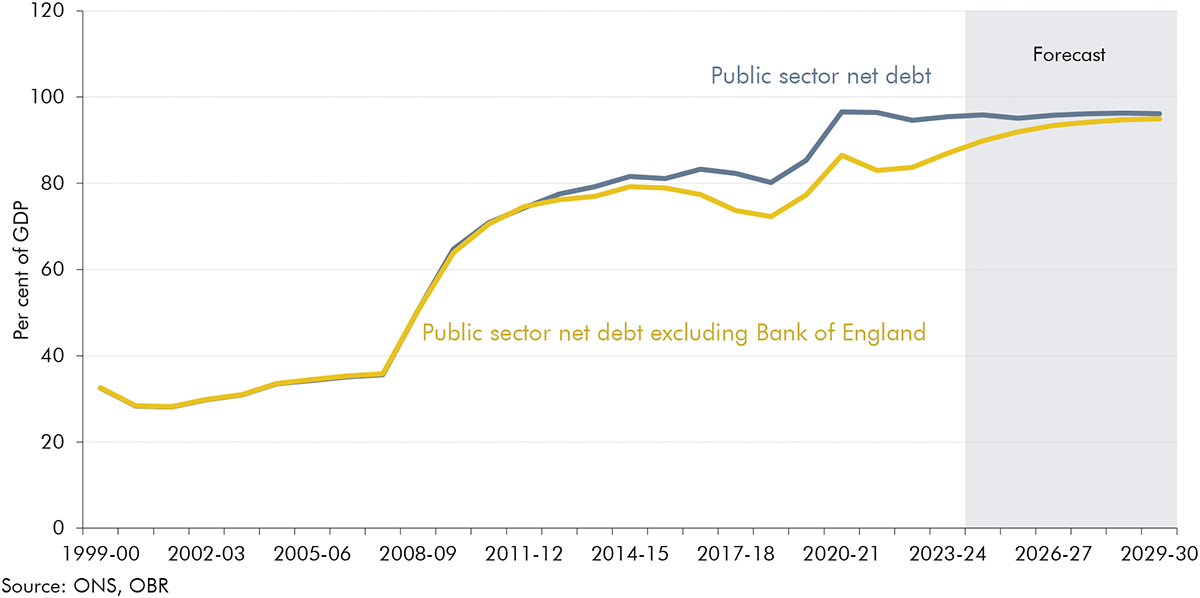

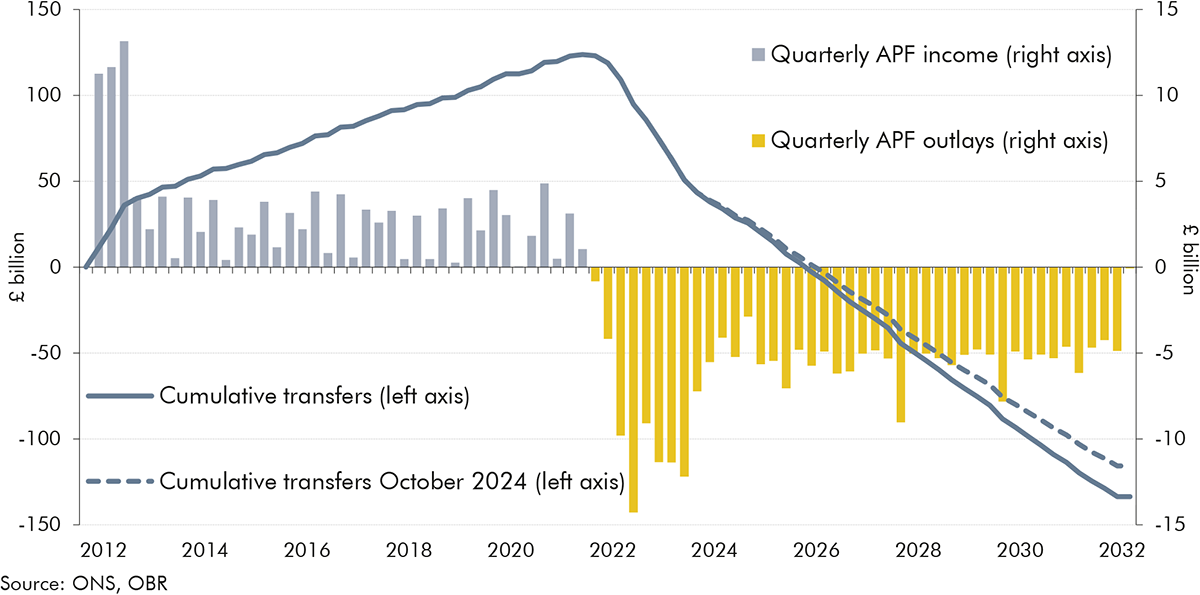

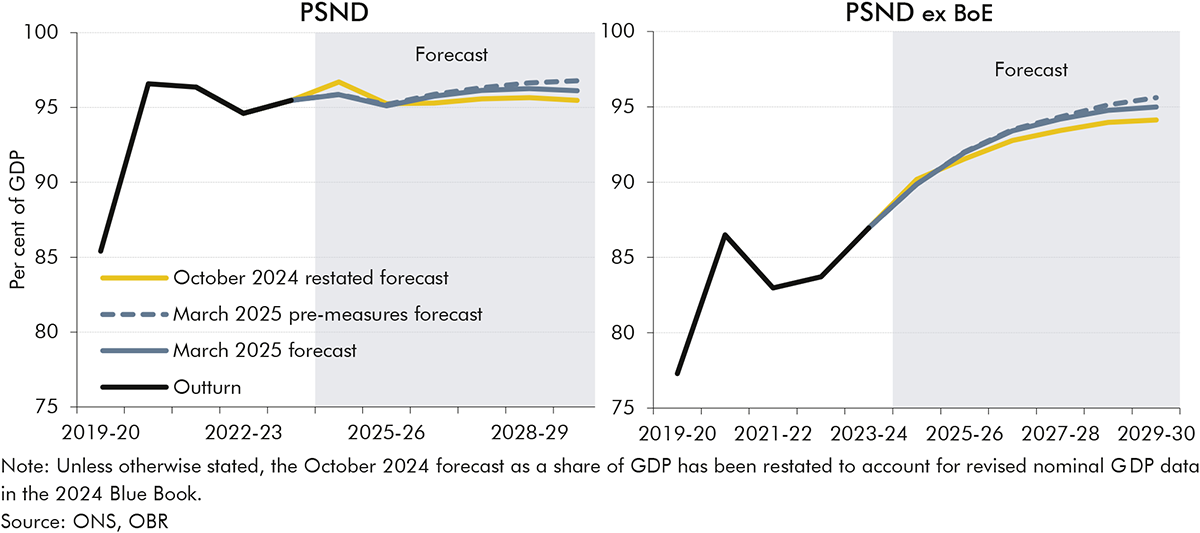

1.18Public sector net debt (PSND) is largely flat over the forecast at 95.9 per cent of GDP this year and 96.1 per cent of GDP in 2029-30. Compared to the October forecast, PSND is 0.8 percentage points lower this year due to ONS revisions, but 0.6 percentage points higher on average from 2026-27 onward mainly due to higher forecast borrowing. Net debt excluding the Bank of England rises in every year of the forecast as a share of GDP. It converges with PSND toward the end of the decade as the Term Funding Scheme and asset purchase facility unwind.

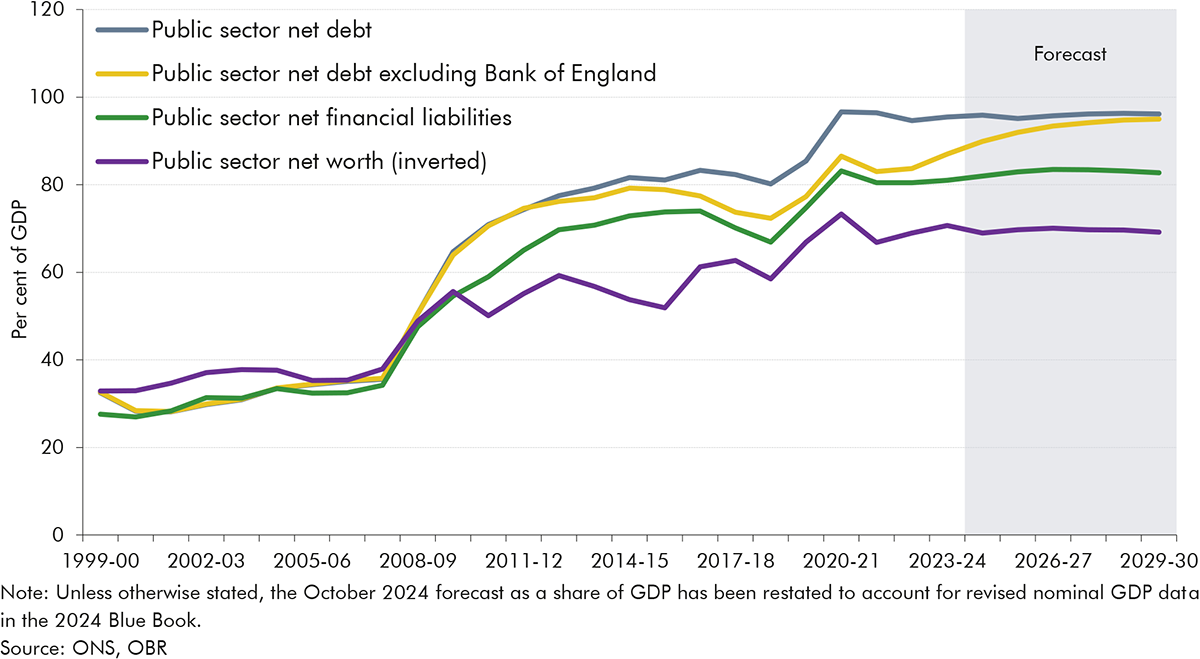

Chart 1.8: Measures of public sector debt

Performance against the Government’s fiscal targets

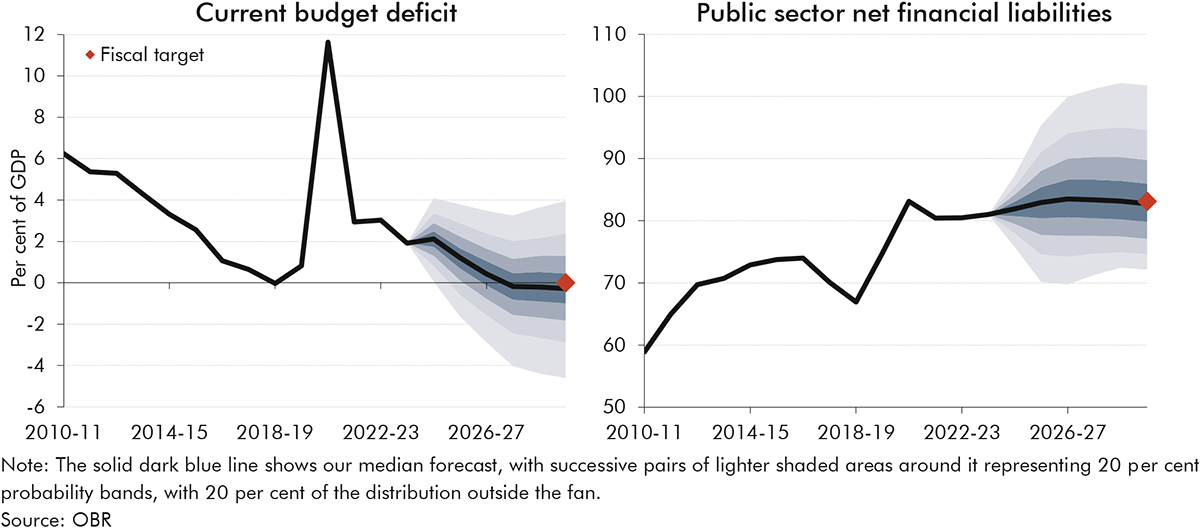

1.19The Government’s fiscal mandate for the current budget to be in balance in 2029-30 is met with headroom of £9.9 billion (0.3 per cent of GDP) in the central forecast. Underlying forecast changes reduced headroom against the current budget by £14.0 billion, so the fiscal mandate would have been missed by £4.1 billion in the pre-measures forecast. Government policies improved the current budget by £14.0 billion so that the mandate is met with identical headroom to October. As set out in the next section, there is significant risk around the central forecast for the current budget. Based on stochastic simulations, the probability of meeting the fiscal mandate is 54 per cent.

Chart 1.9: Current budget deficit fan chart and changes in headroom

1.20The supplementary target for public sector net financial liabilities (PSNFL) to be falling in the final year of the forecast is also met in the central forecast, with headroom of £15.1 billion (0.4 per cent of GDP). On our central forecast, PSNFL rises from 81.9 per cent of GDP this year to a peak of 83.5 per cent in 2026-27, and falls thereafter to 82.7 per cent in 2029-30. Forecast changes reduced headroom by £10.8 billion, with measures restoring nearly all of it such that the target is met by a £0.6 billion smaller margin relative to October. Based on historical forecast errors, the probability of meeting the supplementary target is 51 per cent.

Chart 1.10: Net financial liabilities fan chart and changes in headroom

Risks and uncertainties

1.21Headroom of £9.9 billion against the fiscal mandate is only one-third of the average of £31.3 billion that Chancellors have set aside against their fiscal rules since 2010. It is also a very small margin compared to the risks and uncertainty inherent in any fiscal forecast. The average absolute final-year revision to pre-measures borrowing over the past ten forecasts has been £19.4 billion. And risks to the forecast are heightened at present given the significant uncertainty surrounding domestic and global economic developments.

1.22Key risks to our economy forecast include:

The outlook for productivity growth, one of the most important forecast judgements, is uncertain both in terms of its level and growth rate. Trend productivity growth averages 1.0 per cent a year in our central forecast. If the recent weakness in trend productivity growth persists and growth averages just 0.3 per cent a year, the current budget would be in deficit by 1.4 per cent of GDP in 2029-30. If the recent weakness proves to be entirely cyclical and so trend growth in output per hour averages 1.2 per cent a year, the current budget would be in surplus by 0.9 per cent of GDP in 2029-30.

High and volatile market expectations for Bank Rate and gilt yields continue to shape the fiscal outlook. Higher debt interest costs just since October were enough to eliminate the current surplus in the pre-measures forecast. Were Bank Rate and yields on gilts issued across the forecast to both be 0.6 percentage points higher, less than the 1 percentage point volatility in 10-year gilt yields since early October, it would be enough to eliminate the headroom against the fiscal mandate.

Risks around the global outlook have intensified since October. This is particularly true for trade policy, and in Box 2.2 we explore the implications of three tariff scenarios. In the most severe of these scenarios, with a reciprocal 20 percentage point increase in tariffs between the US and the rest of the world, UK real GDP is 1 per cent lower than in our central forecast in the peak year of impact. This would almost entirely eliminate the headroom against the fiscal mandate, as additional tariff revenue is more than offset by lower receipts from income, corporation, and consumption taxes.

1.23Significant risks to the fiscal forecast over the medium term include:

The tax-to-GDP ratio is forecast to increase to a post-war high of 37.7 per cent of GDP in 2027-28. Part of this increase is driven by the policies announced at the previous Budget, including the increases in employer NICs and capital taxes, with the estimated yield from several of these policies remaining highly uncertain. The forecast also assumes that seldom-implemented fuel duty indexation and the reversal of the 5p cut from 2026-27 raises £4.6 billion in 2029-30. There are also significant risks around key economic forecast assumptions which drive tax revenues, such as earnings and employment growth, and from the assumption that the implied tax gap, a measure of tax compliance, falls to a historic low due to recent compliance policy measures.

Departmental spending plans for the three years beyond 2025-26 will be set at the Spending Review this summer. The forecast for these years implies significant pressures on ‘unprotected’ departments, whose day-to-day budgets may need to be cut by 0.8 per cent a year in real terms from 2026-27 to accommodate assumed commitments in other areas. The Government has addressed a previously identified fiscal risk by raising defence spending from to 2.3 to 2.5 per cent of GDP by 2027-28, funded by a reduction in ODA from 0.5 to 0.3 per cent of GNI. But it also has ambitions to further increase defence spending to 3 per cent of GDP in the next Parliament, which would cost an additional £17.3 billion in 2029-30. Planned savings in ODA, particularly with respect to cuts in asylum spending, may drive spending pressures elsewhere.

The Pathways to Work Green Paper measures included in our forecast constitute the largest package of welfare savings since July 2015. The full impacts of these policies are very uncertain given the complexity of how trends in health, demography and the economy interact with the benefits system (as our 2024 Welfare trends report explored). Welfare reforms incorporated into previous OBR forecasts have in many cases saved much less than initially expected, such as the transition from disability living allowance to PIP, or taken far longer to implement than expected, as was the case for the roll-out of UC. And the July 2015 package of benefits freezes and reductions to tax credits and UC was subsequently reshaped or reversed over successive fiscal statements. We will undertake a full assessment of the potential impact of the Green Paper polices on the labour market ahead of our next forecast.

1.24The long-term fiscal outlook remains very challenging, with pressures from an ageing population, climate change, and rising geopolitical tensions putting the public finances on an increasingly unsustainable path. The baseline projection in our 2024 Fiscal risks and sustainability report would require fiscal tightening of 1.5 per cent of GDP per decade over the next 50 years to return debt to pre-pandemic levels. Leaving policy settings unchanged in the long term would see debt rise to over 270 per cent of GDP by the mid-2070s.

Chapter 2: Economic outlook

Introduction

2.1 This chapter describes our latest economy forecast, summarised in Table 2.1, including:

the conditioning assumptions, including interest rates, commodity and equity prices, the global economy, exchange rate, and fiscal policy (from paragraph 2.5);

the forecast for potential output and its components (from paragraph 2.14);

the output gap and real GDP (from paragraph 2.30);

inflation (from paragraph 2.36);

the labour market including employment, unemployment, and earnings (from paragraph 2.40);

the composition of economic activity, including households, businesses, government, and trade and the current account (from paragraph 2.46);

housing, including the impact of planning reforms (from paragraph 2.57);

nominal GDP (from paragraph 2.63); and

how our forecast compares to recent external forecasts (from paragraph 2.64).

Table 2.1: Key economy forecast assumptions and judgements

Key metric (per cent unless otherwise stated)

October 2024

March 2025

Change

Gilt yields

10-year gilt yields average from 2025 to 2029

4.4

4.8

↑

Bank Rate

Average from 2025 to 2029

3.7

3.9

↑

Gas prices

Average in 2025 (pence a therm)

97.3

128.8

↑

Inflation

Quarterly peak CPI inflation in 2025

2.7

3.7

↑

Real GDP

Growth in 2025

2.0

1.0

↓

Potential output

Cumulative growth from 2023 to 2029

10.2

9.7

↓

Labour supply

Cumulative growth from 2023 to 2029

3.9

4.3

↑

Trend productivity

Cumulative growth from 2023 to 2029

6.0

5.2

↓

Output gap

Output gap in 2025

0.1

-0.6

↓

Real GDP per person

Level in 2029 (Index, 2019=100)

105.4

105.4

–

Nominal earnings

Average annual growth from 2025 to 2029

2.5

2.7

↑

Nominal GDP

Level in 2029 (£ billion)

3,367

3,433

↑

Key: ↑ Higher, ↓ Lower, – Unchanged

Developments since the October forecast

2.2 Since finalising our October 2024 forecast, several key data releases have changed our view of the recent performance of the UK economy. This includes the Quarterly National Accounts released on 30 September consistent with Blue Book 2024, which contained revisions to GDP outturns between 2020 and the second quarter of 2024 (but was released too late to be included in our October forecast). Other releases include subsequent ONS population, labour force, and GDP estimates covering the remainder of 2024. The key changes in these releases were:

The size of the UK adult population has been revised up by ½ million (0.9 per cent) in 2024 following the reweighting of the ONS Labour Force Survey (LFS).[1] This reflects stronger population growth since mid-2022 driven by higher net migration than previously estimated. The size of the UK labour force was also revised up by around ½ million (1.5 per cent) in 2024. Average hours remained broadly in line with our October forecast for the year as a whole, despite significant volatility throughout the year. As a result, at the end of 2024, labour supply (measured as total hours worked) was 1.4 per cent higher than in the October forecast.

Real GDP growth from 2022 to mid-2024 was also revised up by the ONS, so that by the second quarter of 2024 the level of real GDP was 0.8 per cent higher than we thought in October.[2] But GDP growth slowed dramatically over the second half of 2024 to just 0.1 per cent combined across both quarters, 0.7 percentage points lower than expected in October. This means that the level of real GDP in the final quarter of 2024 was only 0.1 per cent higher than the October forecast.

A larger-than-expected labour force and a GDP level broadly in line with previous expectations mean that the level of productivity (measured output per hour worked) at the end of 2024 was 1.3 per cent lower than in the October forecast. In growth-rate terms, productivity fell 0.4 per cent in 2023 and a further 1.0 per cent in 2024.

Real GDP per capita at the end of 2024 was also 0.7 per cent below the October forecast and 1.1 per cent lower than its level at the end of 2019.

2.3 In addition to these developments in UK economic outturn data, the global economic outlook has also become more challenging and more volatile than in October. Market expectations for the future path of interest rates and energy prices have both increased. Bank Rate and 10-year gilt yields are 0.2 and 0.4 percentage points higher on average across the forecast period, respectively. Gas prices in 2025 are forecast to be around 30 per cent higher than in our October forecast. And following the election of a new US administration in November, US trade policies and those of its major trading partners remain in flux.

2.4 The higher starting point for the size of the workforce, weaker outturn data for productivity, the recent slowdown in GDP growth, and higher market expectations for energy prices and interest rates explain a large part of the changes in this forecast relative to October. But significant uncertainty continues to surround recent economic developments in the UK. This is partly due to issues with data measurement and volatility, demonstrated by the latest quarterly data showing a partial reversal of the earlier decline in productivity. And the global economic policy environment has been changing from day to day in the run-up to this forecast. Alongside the central forecast we therefore explore the economic and fiscal implications of alternative scenarios for UK productivity (Box 2.1 and Chapter 7), interest rates (Chapter 7), and global trade policy (Box 2.2 and Chapter 7).

Conditioning assumptions

Monetary policy, gilt yields, and equity prices

2.5 Based on market pricing, Bank Rate (taken over the 10 working days to 12 February) is expected to fall from its current level of 4.5 per cent to 3.8 per cent from mid-2026 onwards (Chart 2.1). The Bank of England cut Bank Rate by 0.25 percentage points in February, and market participants expect further cuts totalling 0.6 percentage points this year. However, the expected path of Bank Rate is both slightly higher and flatter than in October. It is 0.2 and 0.3 percentage points above the October forecast, respectively, in 2026 and 2029. Market participants’ expectations for Bank Rate have remained volatile since finalising our October pre-measures forecast. Expectations for 2029 have ranged by a full percentage point, from 3.1 to 4.1 per cent.

Chart 2.1: Bank Rate

2.6 Market pricing for 10-year gilt yields, taken over the same window, rise from 4.3 per cent at the end of 2024 to 5.2 per cent in 2029 (Chart 2.2, left panel). On average across the forecast, this is 0.4 percentage points higher our October forecast. Since early October, UK 10-year spot gilt yields have increased by around ½ percentage point. This increase was broadly in line with the increase in bond yields across many other advanced economies (Chart 2.2, right panel). 10-year gilt yields have also remained volatile, varying by a full percentage point between 3.9 and 4.9 per cent over the same period. We explore the sensitivity of the fiscal outlook to alternative paths for interest rates in Chapter 7.

Chart 2.2: 10-year bond yields

2.7 Equity prices, as measured by the FTSE All-shares index,increased by 6 per cent in 2024 and are 0.7 per cent higher than our October forecast on average across the forecast period. Equity prices are assumed to grow in line with nominal GDP. They are an important driver of both the capital taxes forecast and the value of equity assets within public sector net financial liabilities (PSNFL).

Commodity prices

2.8 Market-based expectations for gas and electricity prices, over the same window as described above, have risen significantly since the October forecast, particularly in the near term. Wholesale gas prices are expected to peak at an average of just under 130 pence a therm in 2025, which is around 30 per cent higher than forecast in October. Prices remain elevated in 2026 before falling to just under 90 pence a therm from mid-2027 onwards, though the average is still 15 per cent higher than our October forecast. Electricity prices are also higher than in October, up more than 20 per cent on average over 2025 and 2026 and over 5 per cent in the medium term. Oil prices are forecast to average 74 dollars a barrel in 2025, up 4 per cent from October, then gradually fall back to 71 dollars in 2029, down 1 per cent from October. The outlook for commodity prices is also uncertain. Gas price expectations for 2025 have ranged from a low of just under 90 to a high of around 135 pence a therm since the October forecast.

Chart 2.3: Gas and oil prices

World economy and the exchange rate

2.9 Our forecast for the world economy is based on the IMF’s 17 January World Economic Outlook Update (WEO). This did not incorporate recent developments in US and global trade policy but did include the, relatively modest, impact of a temporary increase in trade policy uncertainty in the run-up to January. We now expect global GDP growth of 3.3 per cent in 2025 and 2026, unchanged this year and up 0.1 percentage points next year relative to our October forecast. The slightly stronger global growth outlook is driven by stronger growth in the US, which is only partly offset by weaker growth in Europe and other advanced economies.

2.10 Even before taking account of tariffs announced since the start of the year, the January WEO expected global trade growth to slow from 3.4 per cent in 2024 to 3.3 per cent on average between 2025 and 2027. This is 0.1 percentage points lower than our October forecast as trade policy uncertainty temporarily weighs on growth. Cumulative growth in UK export markets between 2024 and 2029 is around 2 percentage points lower than anticipated in October, in line with weaker eurozone and US import growth. Given the considerable uncertainty over the global trade outlook, in Box 2.2 we explore alternative scenarios for the impact of different US and global trade policies on the UK economy.

2.11 The trade-weighted sterling effective exchange rate is 1 per cent lower across the forecast period than in our October projection.[3] Compared to our October outlook, the pound is around 5 per cent weaker against the dollar and ¾ per cent stronger against the euro over the forecast.

Fiscal policy

2.12 From a deficit of 1.9 per cent of GDP in 2024-25, the primary balance (public sector non-interest revenue minus non-interest expenditure) is projected to improve by 3.0 per cent of GDP over the forecast to a primary surplus of 1.0 per cent of GDP in 2029-30. This is primarily due to a rising tax take in 2025-26 and 2026-27, mainly due to frozen tax thresholds and the rise in employer National Insurance contributions (NICs). Public spending also falls slightly as a share of GDP over the forecast period. So, the boost to demand from past fiscal policy announcements wanes over the forecast, as the primary deficit becomes a surplus.[4] This consolidation stabilises debt, although at an elevated level, helping to ensure that borrowing costs and inflation are lower than they otherwise might be.

2.13 The path of overall borrowing is similar to that in our October forecast. This reflects a pre-measures deterioration due to a 0.1 per cent of GDP lower primary balance in 2029-30, and 0.2 per cent of GDP higher net interest payments. This is offset by the effect of government decisions, including tighter fiscal policy and the indirect effects of planning reform, which raise the primary balance by 0.2 per cent of GDP by our forecast horizon. We discuss the magnitude and composition of this fiscal tightening in Chapter 3, with the ‘indirect effects’ of government decisions on our economy forecast discussed in Box 3.1 in Chapter 3.

Potential output

2.14 In our central forecast, potential output growth falls from 1.5 per cent in 2024 to 1.2 per cent in 2025 and then picks up gradually to 1.8 per cent in 2029 (Chart 2.4). Most of the potential output growth in 2024 and 2025 comes from growth in the adult population. A slowdown in net migration from recent, exceptionally high, levels drags down growth in aggregate potential output in 2025. The rise in growth in later years is due mainly to a projected recovery in total factor productivity (TFP) growth, which more than offsets a further drop in the growth of the labour supply. We describe each component of potential output from paragraph 2.19 and the implications for output per person are discussed in paragraph 2.35.

Chart 2.4: Potential output growth

2.15 Compared to our October forecast, the level of potential output in 2029 (the final year of our forecast) is 0.3 per cent higher (Chart 2.5). This is the net result of a significant upward revision to trend total hours worked (1.5 per cent) and downward revision to the level of trend productivity (1.3 per cent). It is also the net result of upward revisions to historical data and downward revisions to a combination of recent data and our forecast.

2.16 The level of potential output in 2023 was 0.7 per cent higher than we assumed in the October forecast. This is based on upward revisions to historical data for real GDP and our judgement that spare capacity over this period is unchanged. This upward revision to the starting level of potential output was driven by a much higher level of labour supply (adding 1.2 percentage points), partially offset by a lower starting level of trend productivity (deducting 0.5 percentage points).

2.17Pre-measures potential output growth between 2023 and 2029 has been revised down by a cumulative 0.5 percentage points over the six years, or an annual average of 0.1 percentage points:

Potential output growth in 2024 and 2025 is a combined 0.5 percentage points lower. We think that part of the recent weakness in productivity growth is structural and will continue in the first half of 2025.

Before accounting for policy measures, potential output growth averages 1.6 per cent in the four years from 2026 to 2029, broadly in line with our October forecast. The decision to leave our assumption for medium-term potential output growth broadly unchanged reflects our current judgement that recent weakness in productivity growth reflects a combination of data volatility, measurement issues, and temporary factors (such as the drag from higher energy prices and lingering effects of Covid). These tell us little about how fast the economy’s supply capacity will grow in the medium term. While growth in productivity is little changed, the level is consistently lower over the forecast, as described in detail below.

2.18Policy measures incorporated in this forecast are estimated to raise potential output by 0.2 per cent in 2029, mainly driven by the effect of residential planning reforms (see Chapter 3 for more details).

Chart 2.5: Level of potential output: changes since October

Labour supply

2.19 Labour supply (measured by trend total hours worked) is projected to be 1.5 per cent higher than in October at the end of the forecast period.[5] This entirely reflects a higher starting point due to a larger population. Annual labour supply growth over the forecast period is unchanged from October. It falls from 1.2 per cent in 2024 to 0.5 per cent in 2029 as net migration falls, while participation and average hours worked slightly decrease due to an ageing population. Aside from a small negative impact on labour supply from reversing reforms to the work capability assessment (WCA) announced in 2023, we have not incorporated supply-side effects of policies in the Government’s Pathways to Work Green Paper in this forecast, due to insufficient information (see Box 3.2 in Chapter 3 for more details).

Adult population

2.20 The size of the adult population in the ONS LFS has been revised up by 0.5 million (0.9 per cent) to 55.7 million in 2024, mainly driven by higher historical net migration. There have been further revisions to migration which are not yet incorporated in the LFS data. Net migration is now estimated to have peaked at 906,000 in the year to mid-2023, 166,000 higher than the previous estimate. There are also some upward revisions to the years to mid-2021 and mid-2022, averaging 30,000 a year.[6] We use the ‘migration category variant’ of the latest ONS population projections in this forecast.[7]

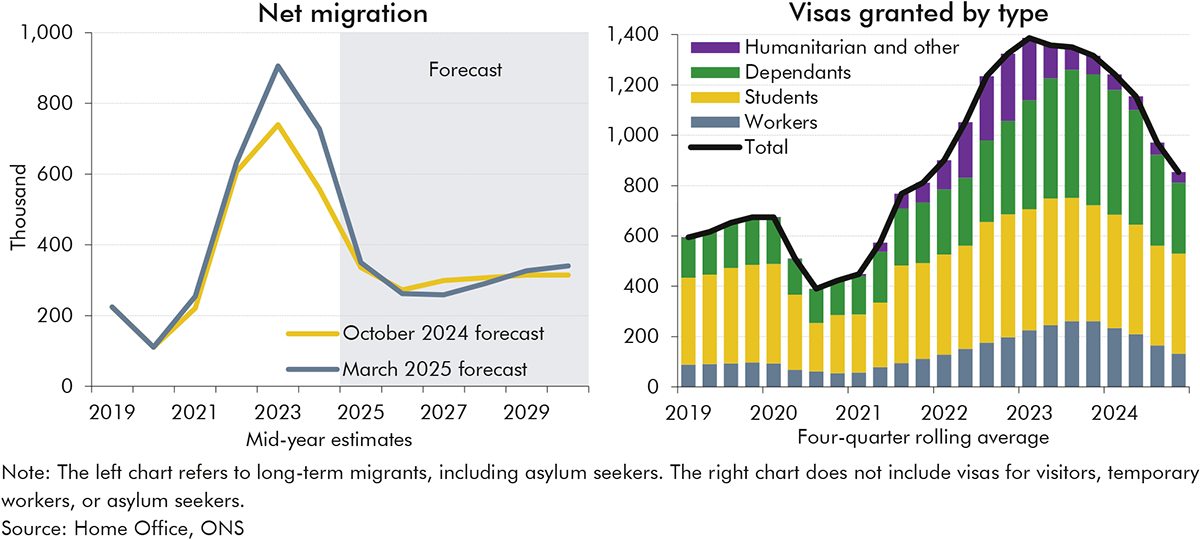

2.21 In this variant, net migration falls sharply from 728,000 in the year to mid-2024 to a trough of 258,000 in the year to mid-2027, before reaching 340,000 at the forecast horizon (Chart 2.6, left panel). This sharp fall in net migration over the forecast is consistent with the tightening of visa policies, mainly regarding dependants of students and care workers, and higher levels of emigration following recent high levels of immigration (especially among students). The effect of tighter visa policies is already evident in the latest visa data which show a sharp reduction across most visa types up to December 2024 (Chart 2.6, right panel). The medium-term level of net migration is slightly higher than in our October forecast (by 25,000). This is in line with evidence suggesting a higher share of immigrants are staying in the UK under the new migration system.

Chart 2.6: Net migration forecast and visas granted

2.22 Based on these latest ONS population projections, we now assume the adult population grows by 2.1 million people over the next five years to reach 57.8 million in 2029. Annual adult population growth averages 0.8 per cent over the forecast period, in line with the October forecast. In 2029, the adult population is ½ million higher than in the October forecast, almost entirely reflecting the higher starting level. Despite the LFS now using a more up-to-date population base, it is still not capturing the latest upward revisions to migration data. This means that there are likely to be some further upward revisions to the adult population in the next LFS reweighting, expected in 2026.

Trend labour force participation

2.23 The trend labour force participation rate is forecast to fall slightly from 63.0 per cent in 2024 to 62.8 per cent in 2029. Across the forecast period, this is 0.3 percentage points higher on average than the October forecast, largely reflecting a higher starting point and a broadly unchanged forecast profile.[8] This forecast incorporates a set of age-specific participation rates using the new ONS population projections. The decline in the participation rate over the next five years is driven primarily by the steady ageing of the population as the share of over-60s rises from 25 per cent in 2022 to 27 per cent in 2029. There is also a contribution from inactivity due to long-term sickness, consistent with the forecast for a further rise in incapacity benefits caseloads (see Chapter 5 for more details).

2.24 This decline is partly offset by three other factors. First, the increase in the state pension age from 66 to 67 in 2028 which boosts participation among this group (see Box 6.1). Second, a further decline in inactivity due to caring for young children as a consequence of falling birth rates and policy measures to increase childcare provision. Third, a boost from new migrants, as this group are more likely to be of working age than the domestic population, which more than compensates for their slightly lower participation rate for a given age.

Average hours worked

2.25 Trend average hours worked fall slightly over the forecast, from 32.0 hours in 2025 to 31.8 hours in 2029. This reflects the drag from the ageing population as older people work shorter hours on average. The LFS measure of average hours worked has been very volatile over the past year, which may be related to ongoing issues with the survey, making it difficult to identify trends in hourly productivity. While there is a lot of uncertainty around the estimates, on balance, we judge that the starting position of trend average hours is marginally higher than our October forecast. The cumulative fall in average hours worked over the forecast (and negative contribution to potential output growth) is similar to the October forecast, at around ½ per cent.

Trend productivity

2.26 Both the level and growth rate of measured productivity have been lower than we expected in October. That is because, between 2021 and the second quarter of 2024, the ONS revised up the total population and total hours worked by more than they revised up GDP, mechanically lowering the level of productivity. And in the second half of 2024, GDP growth was weaker than expected, while total hours worked were higher than forecast in October. As a result, measured output per hour fell by 0.4 per cent in 2023 and by 1.0 per cent in 2024, ending the year 1.3 per cent lower in level terms than in our October forecast.

2.27 We judge the weaker-than-expected productivity growth in 2023 and 2024 partly reflects cyclical factors. Survey indicators and inflation data suggest some spare capacity has opened up within firms, though not enough to fully explain the weakness in measured output per hour. We therefore estimate that trend (or underlying) productivity continued to grow in 2023 and 2024, but weakly and at a slower pace than assumed in the October forecast. However, as much of the downward revision to measured productivity growth was due to the ONS more accurately reflecting recent population growth, we think some of the recent weakness is structural. Therefore, the estimated level of trend productivity is lower than in our October forecast by 0.5 per cent in 2023 and by 0.9 per cent in 2024.

2.28 In our central forecast, we expect that the level of trend productivity will remain permanently below our October forecast, but growth will return to a similar medium-term rate (Chart 2.7). Trend productivity growth in 2025 is expected to be 0.3 per cent, compared to 0.8 per cent in October, largely reflecting base effects from the weakness in the second half of 2024. Trend productivity growth from 2026 onwards is little changed from the October forecast. It returns to 1¼ per cent by 2029, broadly the average of the higher growth in the decade before and lower growth in the decade after the global financial crisis. The level of trend productivity is therefore 1.3 per cent below our previous forecast in 2029. This forecast is comprised of:

Capital deepening (proxied by the change in the capital stock per hour worked), which contributes 0.2 percentage points to average annual trend productivity growth from 2025 to 2029, broadly unchanged from October. This reflects the fact that forecast growth in investment and hours worked has not changed significantly since October.

Total factor productivity (the economy’s efficiency at combining capital and labour to produce output), which contributes 0.8 percentage points to average annual productivity growth over the forecast. This is 0.1 percentage point less than in October, mostly reflecting lower growth in 2025 due to base effects from the weakness in the second half of 2024. TFP growth reaches around 1.0 per cent in 2029.

2.29 We expect that the impact of policies incorporated in this forecast will increase the level of trend productivity by 0.2 per cent in 2029. This increase is driven by the residential planning reforms, which we expect to increase construction sector productivity and housing services due to the higher housing stock.

Chart 2.7: Annual trend productivity level and growth

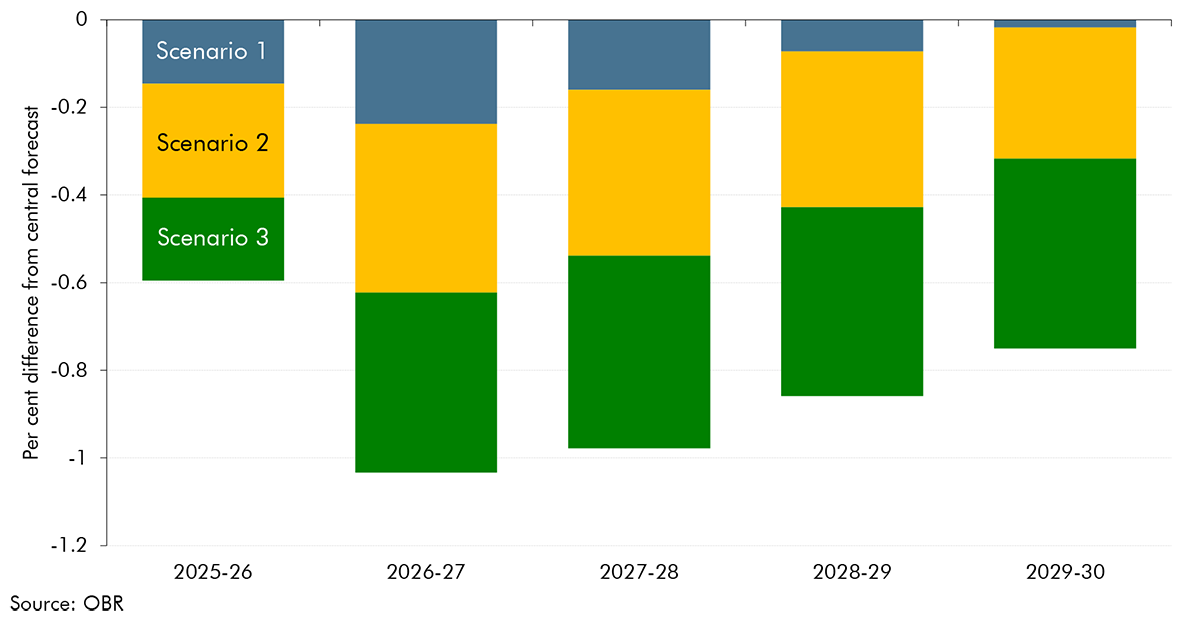

Box 2.1: Alternative scenarios for trend productivity

The outlook for trend productivity is one of the most important and uncertain forecast judgements. Successive past forecasts for trend productivity have proven to be too optimistic as productivity growth has continued to disappoint. So, over the past 10 years, we have lowered our medium-term productivity growth assumption from around 2.2 per cent to 1¼ per cent. Given the measurement and volatility issues with recent outturn data, alongside the wider economic risks that could impact future productivity (such as those surrounding global trade), the uncertainty around our productivity assumption remains high.

To illustrate this uncertainty, the following scenarios show how different judgements about the outlook for trend productivity would affect the economic and fiscal forecast (Chart A):

In an upside scenario, trend productivity growth averages 1.2 per cent a year from 2025 to 2029, 0.3 percentage points higher than in the central forecast. Under this scenario, the level of productivity in 2029 is unchanged from the October forecast and 1.3 per cent higher than in our current central forecast. This would be consistent with the view that the news since October only reflects temporary factors, such as cyclical weakness or measurement issues. Therefore, the level and growth rate of medium-term trend productivity are both unchanged after a period of higher catch-up growth.

In a downside scenario, trend productivity growth remains at 0.3 per cent a year throughout the forecast. Under this scenario, the level of productivity in 2029 is 3.2 per cent lower than the central forecast. This is consistent with the weakness in trend productivity growth in 2024 continuing over the whole forecast period. The level and the growth rate of trend productivity would both be lower in the medium term.

We discuss the fiscal implications of these scenarios in Chapter 7.

Chart A: Trend productivity scenarios

The output gap and real GDP

Output gap

2.30 The latest indicators suggest that there is currently a small amount of spare capacity (excess supply) in the economy, and slightly more than we forecast in October. Our estimate of the output gap (real GDP relative to our estimate of potential output) in the fourth quarter of 2024 is -0.5 per cent. This is 0.2 percentage points lower (more spare capacity) than in October. The negative output gap reflects subdued economic growth in recent quarters, capacity utilisation indicators falling slightly below their normal levels, and a loosening labour market. Given we cannot directly observe the output gap, there is always significant uncertainty around these estimates.

2.31 We expect that the output gap will trough in 2025 at -0.6 per cent before narrowing and closing by early 2027 as output returns to our estimate of potential (Chart 2.8). Over 2025 and 2026 we now expect excess supply, rather than excess demand as in October, with the output gap 0.6 percentage points lower on average over this period. This reflects the lower starting point, higher market expectations for interest rates, lower business and consumer confidence, and increased uncertainty, including around global trade policy. Government policy measures announced since October are expected to lift the output gap by around 0.1 percentage points through the middle of the forecast period, primarily reflecting the impact of planning reforms (see Chapter 3).

Chart 2.8: Output gap

Real GDP

2.32 Real GDP grew by 0.9 per cent in 2024, 0.2 percentage points lower than anticipated in October. We now expect similar growth of 1.0 per cent in 2025, half the 2.0 per cent growth assumed in our October forecast (Chart 2.9, right panel). Around one-third of this difference in 2025 reflects the lower growth in potential output due to structural weakness in productivity, as discussed above. The remaining two-thirds reflects cyclical weakness due to higher interest rate and energy price expectations, rises in uncertainty, and a fall in confidence. The latter is shown by measures of consumer and business confidence having generally trended lower in recent months. The S&P Global/CIPS UK composite PMI also points to only a modest expansion in activity in the first couple of months of 2025 as it remains below the historical average.

2.33 Our central forecast has GDP growth accelerating to 1.9 per cent in 2026 then averaging 1.8 per cent a year over the rest of the forecast, broadly in line with our potential output forecast. The projected acceleration in 2026 reflects monetary policy loosening, falls in energy prices, and a gradual easing of uncertainty resulting in spare capacity in the economy being used up. While the forecast for GDP growth is much weaker in the near term, in line with recent data developments, our forecast for medium-term GDP growth is slightly higher than in October. This is due to the more negative starting output gap providing more scope for above-trend GDP growth and the impact of planning reforms. From 2023 to 2029, cumulative real GDP growth is around ½ percentage point lower than the October forecast.

Chart 2.9: Real GDP growth

2.34 The risks around our forecast for real GDP growth are substantial, with considerable uncertainty regarding both the domestic and international outlook. As always, productivity growth is one of the most important and uncertain forecast judgements, and Chapter 7 sets out the fiscal implications of the alternative productivity scenarios described in Box 2.1. Since October, market expectations for interest rates have been volatile across advanced economies, underscoring the continued uncertainty around the monetary and fiscal policy outlook. Developments in global trade policies represent another significant forecast risk. We explore the effect of potential changes in global trade policy on real GDP in Box 2.2. Purely based on historical forecast errors, there is roughly a three-in-ten chance that real GDP will fall in 2025, and roughly a similar chance that growth will exceed 2 per cent this year (Chart 2.9, left panel).

GDP per person

2.35 After falling by 0.9 per cent in 2023 and by another 0.1 per cent in 2024, real GDP per person is expected to grow by 0.3 per cent in 2025. Growth then rises to an average of 1.4 per cent a year over the rest of the forecast, driven by the recovery in productivity growth. Real GDP per person recovers to its early 2022 pre-energy crisis level by the start of 2026 (Chart 2.10). This is around a year later than we forecast in October, reflecting weaker near-term productivity growth. By the end of the forecast, we expect real GDP per person to be broadly in line with our forecast from October.[9]

Chart 2.10: Real GDP per person

Inflation

2.36 CPI inflation is forecast to rise from 2.5 per cent in 2024 to 3.2 per cent in 2025, but then fall rapidly to around the 2.0 per cent target from mid-2026 onwards. Monthly CPI inflation is expected to peak at around 3.8 per cent in July 2025. This is driven by increases in the Ofgem price cap due to higher energy prices, higher food prices due to an increase in domestic costs, and the increase in regulated water bills from April 2025. From 2026 onwards, CPI inflation is forecast to fall rapidly as increases in household energy bills fall out of the annual comparison and more spare capacity in the economy opens up.

2.37 Compared to October, CPI inflation is forecast to be 0.6 percentage points higher in 2025, then marginally lower from 2026 to 2028. This would leave the CPI price level 0.2 per cent higher at the end of the forecast period in 2029. Chart 2.11 illustrates that, based on historical forecast errors, there is roughly a one-in-five chance of CPI inflation being below 2.6 per cent or above 4.0 per cent in 2025.

Chart 2.11: CPI inflation

2.38 RPI inflation is forecast to average 4.1 per cent in 2025, before falling rapidly to 3.2 per cent in 2026 and to 2.9 per cent on average thereafter. Our forecast for RPI inflation in 2025 has been revised up 0.6 percentage points relative to the October forecast, in line with the upward revision to CPI. However, in 2026 and 2027 we forecast a slightly larger gap between RPI and CPI inflation than in October, because of stronger growth in house prices and mortgage interest payments which affect RPI but not CPI.

2.39 The GDP deflator – which measures the price of all domestically produced goods and services – is forecast to grow largely in line with CPI inflation throughout the forecast. We expect the GDP deflator to grow by 3.2 per cent in 2025, before slowing down to 1.7 per cent in 2026. The latter is slightly lower than our forecast for CPI inflation of 2.1 per cent as higher energy prices temporarily lower the UK terms of trade, given the UK is a net importer of energy. From 2027 onwards, GDP deflator growth averages around 2 per cent a year, in line with CPI inflation. Compared to our October forecast, cumulative growth in the GDP deflator between 2024-25 and 2029-30 is forecast to be marginally lower as there is more spare capacity in the domestic economy in the first two years of our forecast.

Labour market

2.40 Recent data suggest that the labour market continues to loosen, with vacancies falling and the unemployment rate rising, although wage growth remains strong. The loosening likely reflects weak economic growth and subdued business confidence weighing down on labour demand. The increase in employer NICs is also likely to be contributing to falling recruitment and rising redundancies. In this forecast, we have not incorporated any impact of the Government’s Plan to Make Work Pay as there is not yet sufficient detail or clarity about the final policy parameters. Aside from WCA reforms, we were also unable to incorporate supply-side effects of the policies in the Government’s Pathways to Work Green Paper due to, as yet, insufficient information on their effects (see Box 3.2 in Chapter 3). We plan to include the effects of both in our next forecast.

2.41 Issues with the LFS remain, which currently make labour market forecasts particularly uncertain. Following the recent reweighting, the LFS now uses a more up-to-date population base (see paragraph 2.20). But it is still not capturing the latest upward revisions in migration outturn data, which are expected to further increase the LFS population base in the next reweighting. Additionally, sampling issues and resulting biases remain in the LFS, which mean that participation and employment rates are likely to still be underestimated.

Employment and unemployment

2.42 The employment rate is forecast to decline slightly from 60.5 in the second half of 2024 to 60.2 per cent in 2029 as population ageing weighs on participation (Chart 2.12, left panel). The starting point is 0.6 percentage points higher than previously forecast and up from 60.2 in the first half of 2024. This is likely in part due to issues with the LFS as other employment measures, such as the RTI and workforce jobs, suggest employment growth slowed in 2024. Population growth means that cumulative employment growth over the forecast is around 1.2 million, broadly the same as in October. However, due to historical LFS revisions, the level of employment is estimated to be around ½ million higher in the outturn than in October, and this gap is retained throughout the forecast.

2.43 We expect the unemployment rate to peak at 4.5 per cent (1.6 million people) in 2025 as spare capacity opens up, before falling to its estimated structural rate of 4.1 per cent in 2028 (Chart 2.12, right panel). The unemployment rate has been trending up since the post-pandemic trough of 3.8 per cent in 2022, albeit with some volatility likely due to issues with the LFS. The general trend is in line with wider indicators of a cooling labour market as labour demand weakens. Compared to the October forecast, the unemployment rate is 0.4 percentage points (around 160,000 people) higher in 2025, in line with a more negative output gap, while our estimated structural rate is unchanged.

Chart 2.12: Employment and unemployment rates

Average earnings

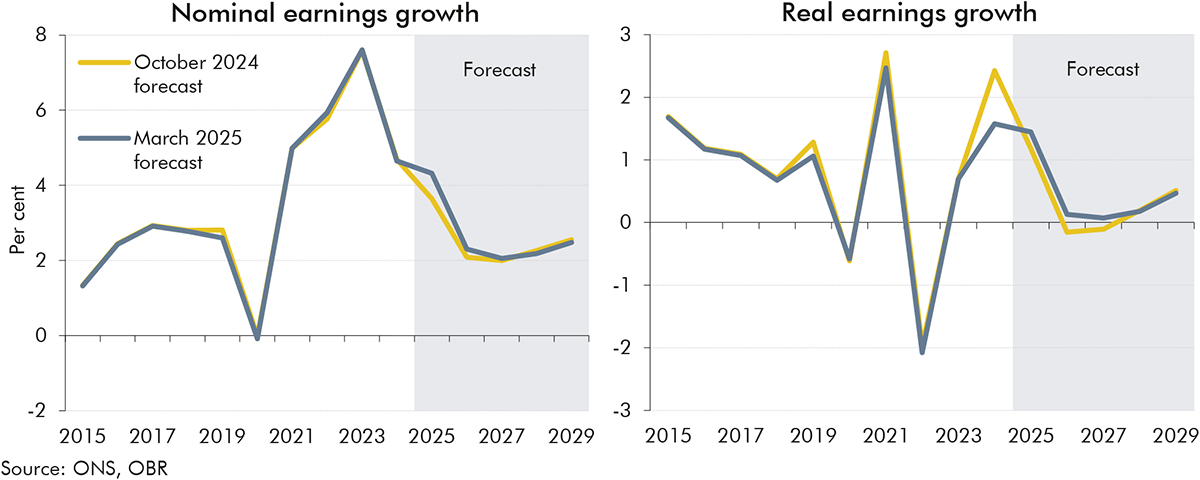

2.44 We forecast nominal earnings growth to ease from 4.7 per cent in 2024 to 4.3 per cent in 2025 (Chart 2.13, left panel). Nominal earnings growth remained strong in the second half of 2024 and annual growth was 5.5 per cent in the fourth quarter.[10] The recent strength has been driven by a combination of the timing of backdated public sector pay settlements and resilient private sector growth. The near-term outlook remains relatively strong, with the forecast for the last quarter of 2025 broadly in line with surveys of pay settlement growth expectations of around 3 to 4 per cent. Across 2025, average nominal wage growth is 0.7 percentage points higher than the October forecast. However, the ongoing loosening in labour market conditions, the recent hit to business sentiment, compressed company margins, and the rise in employer NICs should eventually weigh on the outlook for wage growth. From 2026 onwards, nominal earnings growth slows further, averaging between 2 and 2½ per cent.

2.45 In our central forecast, real earnings grow by 1.4 per cent in 2025 before stagnating in 2026 and 2027 (Chart 2.13, right panel). Real wage growth is below productivity growth in the middle years of the forecast as firms rebuild profit margins, which have recently been compressed. We expect firms to have more scope to pass on higher costs from increased employer NICs to workers as the labour market continues to loosen. Real wage growth then begins recovering towards productivity growth in the medium term. Compared to our October forecast, real earnings growth is 0.3 percentage points higher in 2025, as wage settlement expectations have held up relative to weak productivity growth and falling inflation. Growth is broadly unchanged from October over the rest of the forecast.

Chart 2.13: Nominal and real earnings growth

Composition of economic activity

2.46 Over the last few years, a series of significant shocks has contributed to falls in labour market participation, weak productivity growth, and high consumer price inflation, with much of the latter imported from abroad. However, real household disposable incomes have held up surprisingly well. This was initially a result of substantial government support and, more recently, due to a higher share of income going to labour as company profit margins have been squeezed. Eventually, we assume that these shocks will be passed onto households and recent experience suggests this will occur through real wage adjustment rather than through higher unemployment. Therefore, over the forecast, we expect firms to rebuild profit margins and the labour share of income to fall back slightly.

Households

Household disposable income

2.47 We expect real household disposable income (RHDI) per person to grow at an average of around ½ per cent a year in the five years from 2025-26 to 2029-30 (Chart 2.14, left panel).[11] But growth is projected to vary significantly around this average, first slowing sharply from 2½ per cent in 2024-25 to almost no growth in 2027-28. This is driven by four factors: (i) lower real wage growth as firms rebuild profit margins; (ii) non-labour income growth returning to medium-term trends; (iii) an increase in household taxes as firms pass employer NICs onto wages and income tax thresholds remain frozen; and (iv) slower benefits growth due to a rising state pension age and welfare measures announced since October. After the sharp slowdown, RHDI per person growth picks up to average ⅔ per cent a year in 2028-29 and 2029-30 as the freeze on income tax thresholds ends and real wage growth increases. Compared to the October profile, stronger real wage growth means RHDI per person grows slightly more quickly across the forecast. Aggregate RHDI growth averages 1 per cent a year across the forecast, while population growth averages just under ½ per cent a year.

2.48 Policy measures lower RHDI per person slightly – around ¼ per cent by 2029-30. The main driver is lower benefit income due to the Government’s welfare reforms. Planning reforms boost incomes, offsetting some of the hit, as higher productivity raises wages and a larger housing stock means more compensation for housing services. Yet three quarters of the extra income from housing services comes as ‘imputed rent’ – what homeowners would receive if they rented out their home. This makes the boost less tangible for households.

Chart 2.14: Real household disposable income per person

Household saving

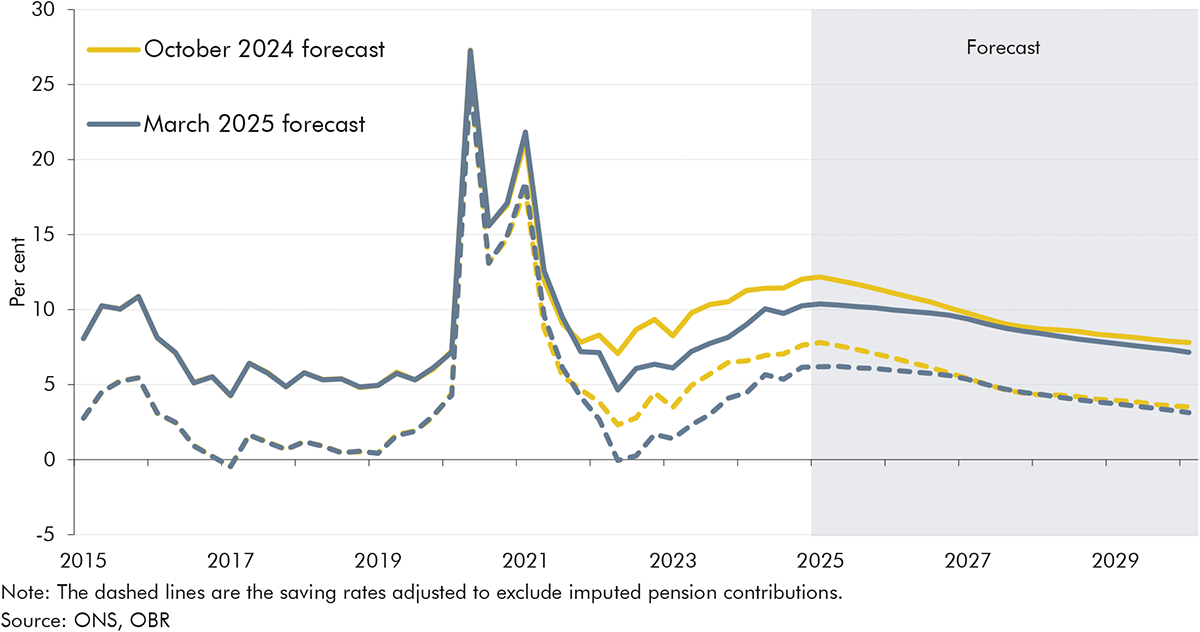

2.49 The household saving rate (adjusted to exclude imputed pension contributions) rose from 2¾ per cent in 2023 to an estimated 6¼ per cent at the end of 2024. We expect the saving rate to hold around this level in 2025 before falling steadily over the rest of the forecast, going below 3¼ per cent by the start of 2030 (Chart 2.15). Household saving has risen in recent years as resilient real wages and rising net interest income have supported RHDI, while higher interest rates and greater uncertainty have incentivised saving. We expect these factors to unwind over the forecast, prompting households to lower their saving rate back towards historical averages. This allows households to maintain a steady share of consumption in GDP, despite a falling labour share in income. Policy measures boost the saving rate slightly, as households look to fund higher residential investment driven by the planning reforms. But the difference is less than ¼ percentage point by the start of 2030. Compared to our October forecast, downward revisions to outturn mean we expect a lower saving rate across most of the forecast.

Chart 2.15: Saving rate

Household consumption

2.50 Real private consumption is expected to grow by 1.5 per cent a year on average over the forecast. This is broadly in line with the October forecast as higher growth in household income is offset by slightly shallower fall in the household saving rate. Consumption growth was weak in 2024 and near-term indicators, including consumer sentiment surveys and intelligence from the Bank of England’s Agents network, suggests consumer demand remains subdued. However, we expect consumption growth to increase from 1.2 per cent in 2025 to 1.8 per cent in the final year of the forecast, supported by the falling saving rate. Policy measures are expected to weigh slightly on consumer spending in the latter half of the forecast as a reduction in welfare benefits lowers household incomes, and the saving rate is slightly higher to help fund the increase in residential investment. There are risks in both directions around our consumption forecast, reflecting uncertainty around future real wages and household saving.

Profits and business investment

2.51 Profits as a share of GDP are forecast to fall to 14.3 per cent in 2025, a level last seen in 2010 after the global financial crisis, before recovering to 15.4 per cent in 2029 (Chart 2.16, left panel). The profit share dropped from 16.2 per cent in 2019 to 15.1 per cent in 2024 as margins were eroded by firms granting workers above-productivity increases in real wages. The net rate of return on business sector capital has also been on a steady downward trend, from 12 per cent in 2015 to 9 per cent in the first half of 2024. We expect the profit share of GDP to fall further in 2025 as wage settlement expectations have continued to outpace productivity growth and inflation and as the employer NICs rise initially hits profits. The profit share then gradually increases over the rest of the forecast as we assume firms rebuild their margins and pass on more of the costs from the employer NICs rise to higher consumer prices and lower nominal wages.