The Government announced that it intends to take on Royal Mail’s historic pension deficit with effect from April 2012. This box explored how the transfer of the relevant assets and liabilities will impact the public sector finances.

The Government is currently legislating to take on Royal Mail’s historic pension deficit with effect from April 2012. It intends to take over the pension liabilities accrued up to March 2012 and a share of the pension fund’s assets, leaving behind a fully funded pension scheme. The Treasury estimates the value of the assets being transferred at around £28 billion, with the present value of the liabilities transferring at around £37.5 billion. The liabilities will crystallise over time in the form of payments to pensioners.

The ONS decide on the treatment in the National Accounts of public sector transactions. The advice we have received from the Treasury is that the initial transfer of assets will be treated as a capital grant from the private to the public sector. The liabilities will be treated as a contingent liability which will not affect the National Accounts but will feature in the Whole of Government Accounts.

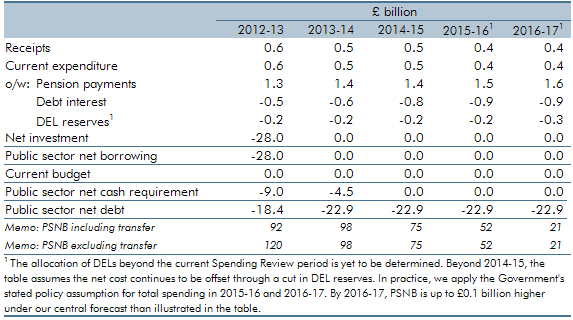

The Government has announced its intention to cancel the gilt holdings during 2012-13 and sell the majority of the non-gilt assets within the first two years, although less liquid assets such as property and private equity will take longer to realise. We therefore assume that all non-gilt liquid assets are sold in 2012-13 and 2013-14, but make no assumption for the less liquid assets. Although it remains dependent on the final amount and breakdown of the assets and liabilities transferred, the Treasury’s latest estimates, included in our forecast, are that:

- PSNB will be reduced in 2012-13 by the total value of the assets transferred, which is around £28 billion;

- the central government net cash requirement (CGNCR) and PSND will immediately be reduced by around £4.5 billion, reflecting the cash portion of the assets transferred. They will fall by a further £9 billion over 2012-13 and 2013-14 as the non-gilt liquid assets are sold. The transfer of gilts held by the fund will reduce PSND by over £9 billion in 2012-13, equal to the uplifted nominal value of the debt. (The market value of the debt is estimated to be over £11 billion, but the uplifted nominal value, which is the amount that affects PSND, is closer to £9 billion). The subsequent cancellation of gilts will have no further impact on the fiscal aggregates. In total, as a result of these elements, PSND will be reduced by £23 billion from 2013-14 onwards;

- pension payments will raise public sector expenditure and PSNB over time, by between £1.3 and £1.6 billion in each year of the forecast period; and

- income from the assets retained will raise receipts by around £0.5 billion per year, while debt interest costs will fall by up to £1 billion each year.

The overall impact of these flows would be to raise PSNB by up to £0.3 billion per year in the medium term, but the Government has chosen to offset the forecast net cost over the current Spending Review period through a reduction in DEL reserves, leaving no overall impact on PSNB over these years. Table A sets out the various effects of the transfer on the public finances including this offset. The current budget and the cyclically-adjusted current budget are unaffected.

The immediate impact on the public finances would appear to be significantly beneficial. However, the value of the liabilities exceeds the current present value of the assets resulting in a real cost to the Government over the lifetime of the pension scheme.

Table A: Impact on the public sector finances of the Royal Mail transfer