The land and buildings transaction tax (LBTT) was implemented in Scotland on April 1 2015 while the land transactions tax (LTT) began in April 1 2018. Both taxes replaced the UK Government’s stamp duty land tax but operate in similar ways. In this box we evaluated our March 2023 forecasts for 2023-24, and how they compared to the eventual outturn data. We explained the reasons behind the 10.3 per cent surplus for LBTT and the 9.9 per cent shortfall for LTT.

This box is based on OBR data from March 2025 .

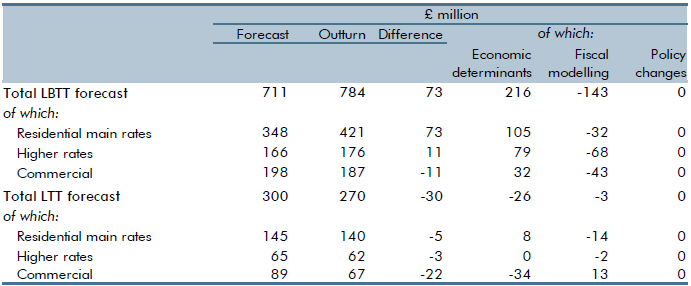

Table A compares the March 2023 forecast for 2023-24 Scottish and Welsh property transaction taxes to the latest outturn data. The overall differences were relatively similar in percentage terms. Outturn exceeded forecasts for Scotland by £73 million (10.3 per cent) but lower for Wales by £30 million (9.9 per cent).

Scottish LBTT

The £73 million difference between outturn and forecast reflects stronger-than-expected receipts across both residential sectors, slightly offset by lower-than-expected receipts in the commercial market:

- Residential main rates receipts exceeded the March 2023 forecast by £73 million (21 per cent). This is more than explained by the value of transactions being higher than forecasted, with some offset from the composition of transactions being less tax-rich than expected.

- Additional dwelling supplement receipts exceeded the March 2023 forecast by £11 million (6.4 per cent). This was also explained by the value of transactions exceeding our forecast, again partly offset by lower-than-expected prices in the upper end of the market, alongside higher-than-expected repayments.

- Commercial receipts were £11 million (5.4 per cent) below forecast. Prices and transactions were stronger than anticipated but this was more than offset by other factors such as more losses to reliefs than anticipated.

Welsh LTT

The £30 million shortfall relative to our March 2023 forecast reflects lower-than-expected receipts across all three markets:

- Residential main rates receipts were £5 million (3.6 per cent) less than forecast. This is mainly because outturn in the final quarter of 2022-23 was not available at the time of the forecast, and was lower than assumed in the forecast.

- Higher rates on additional properties receipts were £3 million (3.9 per cent) lower than forecast. This also relates to differences between the March 2023 forecast and the previous final quarter’s outturn, as explained above.

- Commercial property receipts were £22 million (24.5 per cent) lower than forecast. Prices were lower than expected and fewer sales than expected were nearer the top of the price distribution.

Table B: Devolved property taxes in 2023-24: March 2023 forecast versus outturn

This box was originally published in Economic and fiscal outlook – March 2025