In the run-up to our March 2025 Economic and fiscal outlook, global trade policies had been subject to frequent changes and the future direction for trade policy was highly uncertain. In this box, we outlined three illustrative scenarios to show the potential impact of higher US and global tariffs on UK output and inflation, highlighting the primary transmission channels and their probable effects.

This box is based on CEBR, Goldman Sachs, KPMG, LSE, Oxford Economics, Peterson Institute for International Economics, ONS, and OBR data from October 2024 and March 2025 .

The new US administration has announced new tariffs on a range of imports from its trading partners, prompting responses from some countries affected. Both US and other countries’ trade policies have been subject to frequent changes over recent weeks and the future direction for trade policy is highly uncertain. Our central forecast for global output aligns with the IMF’s January World Economic Outlook Update so does not take account of the new tariffs announced by the US and other countries since January. In this box, we outline three illustrative scenarios to show the potential impact of higher US and global tariffs on UK output and inflation, highlighting the primary transmission channels and their probable effects. The fiscal impacts of these scenarios are presented in Chapter 7.

The UK’s trading relationship with the US and rest of the world

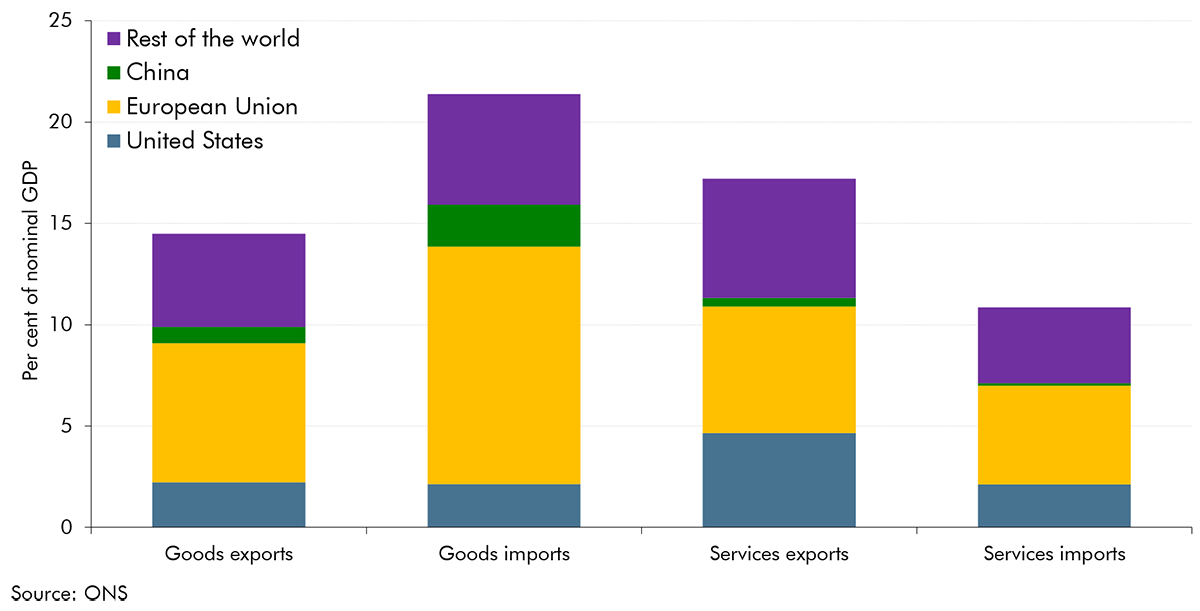

The UK economy is relatively trade-intensive compared with other economies in the G20. UK trade (imports plus exports) as a share of GDP is around 64 per cent, above the G20 average of 55 per cent and far higher than the US at 25 per cent.a

While the US is the UK’s second-largest trading partner (after the EU), the composition of our trade with the US is skewed toward services rather than goods. The US accounted for 15 per cent of the UK’s goods exports and 10 per cent of its goods imports in 2023. In the services sector, the US has a larger role, representing 27 per cent of the UK’s exports and 19 per cent of its imports. The EU as a whole remains by far the UK’s largest trading partner, contributing about 50 per cent of the UK’s trade, roughly two-thirds of which is trade in goods. China, the UK’s third-largest trading partner, accounts for less than 10 per cent of UK trade and is heavily skewed towards goods imports.

The UK’s trade in goods with the US is broadly in balance.b The major broad categories of goods which the UK exports to the US include machinery, transport equipment, and chemicals. Meanwhile UK imports from the US are mainly machinery, transport equipment, and fuel.

Chart 2B: Composition of UK trade in 2023

Mechanisms through which tariffs could affect the economy

Economic theory and empirical evidence suggest that higher tariffs reduce the trade intensity of output and so reduce productivity and real GDP over the long run.c Lower overall trade intensity tends to reduce productivity as, among other channels, it restricts a country’s ability to exploit its comparative advantage and the economies of scale that come from accessing overseas markets.

For a country imposing tariffs, there are a number of channels through which this can affect their economy, including:

- Tariffs increase the cost of importing goods from overseas, which generally lowers the quantity of goods imported. There could be offsetting effects by importing from countries on which tariffs are not applied (trade diversion) and changes in the exchange rate.

- The increases in import costs are generally passed onto households and result in a temporary increase in consumer price inflation, though the effect on the level of consumer prices will be permanent if the tariffs are permanent. This will lower real household incomes and consumption. But the effect on inflation is very uncertain, as movements in exchange rates and trade diversion could apply downward pressure.

- Uncertainty around future trade policy can cause firms to delay or even cancel investment or hiring plans, which can push output temporarily below its potential level and have longer-lasting effects. Temporarily pushing output below its potential level will put downward pressure on consumer price inflation.

- Slower growth in the economies of key trading partners subject to tariffs could have indirect effects on demand for a country’s exports, and therefore on GDP and inflation.

The impact on the UK, and relative importance of these channels, depends on the constellation of tariff policies in place.

Scenarios for the UK economy under different tariff regimes

To explore the potential impact of rising US and global tariffs on the UK economy, we construct three stylised scenarios for trade policy in the US, UK, and rest of the world.d These estimates are drawn from a range of models, empirical estimates, and trade scenarios from other institutions. For all scenarios, we assume that tariff rates rise at the start of the financial year 2025-26 (1 April 2025) and remain permanently elevated. As tariffs provide a one-time shock to the price level, any inflation is likely to be short lived, and we assume that the Bank of England looks through the initial increase in inflation. In addition to the direct impact of higher tariffs, there is an increase in trade policy uncertainty which further dampens economic activity in the first few years of the scenarios.e

In the first scenario, the US increases tariffs levied on goods arriving from China, Canada and Mexico by 20 percentage points, and these countries retaliate equivalently. GDP growth in these countries slows while prices rise. This leads to UK GDP being around 0.2 per cent lower than in our central forecast in 2026-27 as demand for UK exports slows and uncertainty weighs on UK economic activity. However, after the initial disruption, this is broadly offset by trade diversion, where demand for UK goods rises as they are relatively cheaper. Overall, UK GDP is largely unchanged from our central forecast by 2029-30.

In addition to the above, in the second scenario, the US goes further by increasing tariffs on goods arriving from all other countries, including the UK, by 20 percentage points. In this case:

- Initially, higher US tariffs would increase the cost of imported goods to US consumers relative to US-produced goods. This is likely to decrease demand for UK exports and dampen UK economic activity. Using a price elasticity of -0.4 implies that for a 20 percentage point increase in prices of US goods imports (assuming the tariff rise is fully passed through to consumer prices), demand for goods exports to the US would fall by 8 per cent, all else equal.f In the UK, where goods exports to the US make up 2 per cent of GDP, this is equivalent to a little under 0.2 per cent of GDP. Higher US import tariffs would also reduce US demand for foreign currency which could cause a moderate depreciation in sterling, mitigating some of this effect. Overall, UK GDP in this scenario is 0.6 per cent lower than in our central forecast in 2026-27, the peak year of impact as lower demand for UK exports from the US, weaker global GDP growth, and heightened uncertainty dragging on investment weigh on UK GDP.

- In the medium term, reduced trade openness leads to a permanently lower GDP level by around 0.3 per cent. This is only partly offset by the opportunity for trade diversion (for customers in the UK to find alternative sources for goods and for firms to seek markets where tariffs are not significant) and the fading impact of uncertainty.

- We assume that UK inflation peaks at 0.3 percentage points higher than our central forecast in 2025-26. But it is below our central forecast in 2027-28 and 2028-29 as weaker UK GDP growth means spare capacity opens up. It then returns to the 2 per cent target.

The third scenario assumes that, in addition to the above, all US trading partners, including the UK, retaliate against the US by imposing their own equivalent tariffs on US goods. In this case:

- UK inflation rises by 0.6 percentage points above our central forecast in 2025-26 as the price of UK imports of US goods increases. Goods make up around half of the CPI basket with roughly 3 per cent of these imported from the US. Therefore (all other things equal) the 20 per cent increase in US goods import prices could add around 0.3 percentage points to CPI, if it is fully passed through to consumer prices. However, the size and direction of overall the inflation impact is very uncertain, for example due to the

impact of movements in the exchange rate and trade diversion. - We assume tariffs on imports from the US lowers imports (and therefore trade intensity), while the impact of higher inflation on real incomes and slowdown in global growth is likely to mean GDP quickly falls below our central forecast. Alternatives to US goods may be more expensive which could lower living standards further. The peak impact on GDP is around 1 per cent in 2026-27. As GDP growth weakens, there are limited second round effects on inflation, which then falls to 1.8 per cent in 2027-28.

- Even higher global barriers to trade and reduced global productivity in this scenario mean medium-term UK GDP is around ¾ per cent lower than in our central forecast.

Chart 2C: Three trade policy scenarios for UK GDP

Sources of uncertainty around these effects

The effects of these channels are highly uncertain in both magnitude and even direction. The impact of tariffs crucially depends on the ability of importers and consumers to substitute away from goods whose prices increase due to tariffs. For example, in a scenario where the UK imposes tariffs on US imports, the impact on UK output and inflation would be smaller if domestic or non-US substitutes were more readily available.

There will also be frictions as new trading regimes are implemented. In the short term, sudden increases in trade barriers could disrupt supply chains, causing shortages and price volatility, but predicting these effects is challenging due to the complexity of global value chains. Uncertainty about future changes in trade policies may delay investment, hiring decisions, and output, potentially reducing not just activity in the near term but potential output in the medium term.

Our scenarios incorporate estimates consistent with the static effects of increased trade barriers on the medium-term productivity level. But in the long term, dynamic effects on productivity (longer-lasting effects on growth rates) are likely to further weigh on UK and global output. Reduced openness to trade would hinder access to the new technologies and knowledge sharing that support innovation. However, the size of these effects remains uncertain.

Comparison with other estimates

Various external bodies have also estimated the potential impact of higher tariffs on UK GDP under differing tariff regimes, time horizons, and modelling assumptions. Our 2022 Fiscal risks and sustainability report also included estimates of a more severe ‘trade war’ scenario involving reciprocal tariffs levied by all countries on each other. Chart D shows that our estimates for the GDP impact of the three scenarios described above are quite close to the average of other estimates for that level of tariffs.

Chart 2D: External estimates of the effects of higher tariffs on UK GDP

This box was originally published in Economic and fiscal outlook – March 2025