Our March 2025 forecast for 2024-25 receipts is £7.5 billion below our October 2024 forecast. This box compared this shortfall to past Autumn to Spring forecast changes, explained the reasons for this shortfall, and described its impacts on the forecast.

This box is based on OBR data from various years .

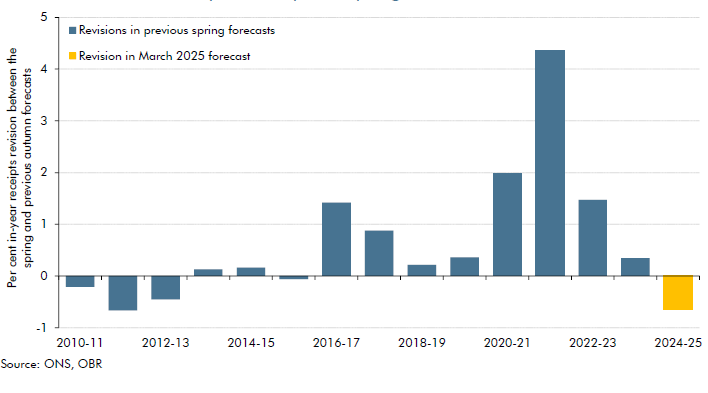

The latest forecast for 2024-25 public sector receipts is £7.5 billion (0.6 per cent) lower than we expected in October, with much of the shortfall in self-assessed income tax, capital gains tax (CGT), and corporation tax. As Chart A shows, in percentage terms this in-year change is the largest downward revision to receipts between an autumn and spring forecast since 2012. There have been larger recent upward revisions of 1.4 per cent in 2016-17, 1.5 per cent in 2022-23, and of much greater magnitude in 2020-21 and 2021-22 during the pandemic.

Chart 4A: Revisions to in-year receipts at Spring forecasts

The shortfall in self-assessed income tax and CGT, and a portion of the shortfall in corporation tax, pertains to 2023-24 liabilities (as these taxes are paid in the year after the liabilities arise). Initial evidence on the composition of the shortfall suggests it has been concentrated in receipts from small company CT, income tax from partnerships and dividend income, and CGT from financial assets. This may be because the high inflation and interest rates in 2023-24 decreased the profitability of small businesses by more than we anticipated. This high inflation was externally driven and so for many small businesses will have increased costs by more than revenues. Further, the tax forecast models may not have adequately captured the effects of higher interest rates on small business expenditure and profits.

A significant portion of the CT shortfall relates to payments on profits in this financial year, with CT from large companies £4.2 billion lower than expected in October. This reflects weaker-than anticipated profits in the second half of 2024-25, due in part to more persistent earnings growth squeezing profits. This can also be seen in outturns for other taxes where stronger-than anticipated nominal earnings mean that PAYE receipts are £1.2 billion higher than expected in

October.

The latest year’s receipts data provide the starting point for the medium-term forecast. Therefore, changes such as these will typically drive a proportional change in the forecast across the medium term by effectively raising or lowering the level of the effective tax rate across the forecast. The exception to this is where there is reasonable evidence to suggest that changes to the current year’s outturn reflect temporary or volatile factors. In this forecast, we made two such adjustments:

- We judged that half of the shortfall in small company corporation tax at this event should not be pushed through to later years. This is because some of the weakness in 2023-24 may be linked to the deferral of writing off losses from previous years against a CT liability until 2023-24, due to the pre-announcement of the CT rate increase.

- CGT liabilities in both 2022-23 and 2023-24 were much weaker than expected after unusually high gains realised in 2020-21 and 2021-22. Because CGT is inherently a more volatile revenue stream, we assume that in the medium term it will return to its pre-pandemic growth trend as share of GDP, and so have tapered off some of the 2023-24 weakness over the forecast period.

After accounting for these two adjustments, £4.5 billion of the overall £7.5 billion shortfall compared to October is assumed to be structural.

We are seeking to improve our approach to forecasting in-year estimates ahead of our next forecast in the autumn. We will audit the existing range of approaches used to produce in-year estimates across the receipts forecasts to identify which produce the most reliable results. We will also seek to use more timely sources of economic data and information from near-term economic forecasts to better inform the estimates. We plan to discuss this further in future Forecast evaluation reports.

This box was originally published in Economic and fiscal outlook – March 2025