As life expectancy has increased, successive governments have increased the state pension age, and it next increases between 2026 and 2028 from 66 to 67. In this box, we estimated the impact of this increase on pensioner welfare spending, working-age welfare spending, and tax revenue.

This box is based on DWP, IFS, ONS data from January 2022, March 2023, and March 2025 .

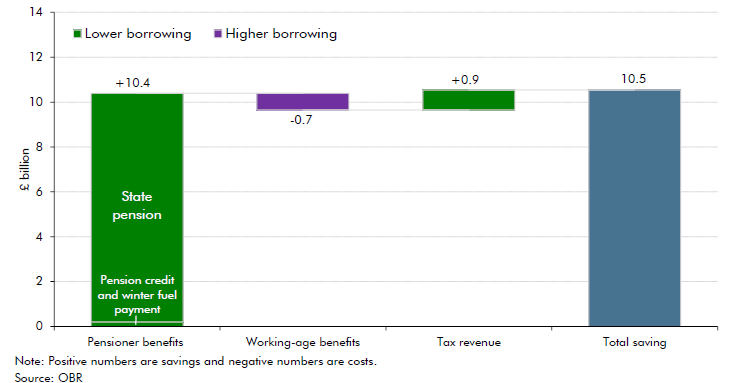

As life expectancy has increased, successive governments have increased the state pension age (SPA). Over the past 15 years, the SPA has risen from 60 to 65 for women between April 2010 and November 2018, and then from 65 to 66 for both men and women between December 2018 and October 2020. Over the period of our latest forecast, the SPA will increase again from 66 to 67 for men and women between April 2026 and March 2028, as announced in the Pensions Act 2014 and confirmed by the Government in March 2023. This has a significant fiscal impact in the current forecast – we estimate its net impact is to reduce borrowing by £10.5 billion in 2029-30.

Chart 6A: Net fiscal saving in 2029-30 from the rise in the state pension age to 67

Increasing the SPA affects the public finances through three main channels. The largest is the direct reduction in the number of people eligible for the state pension in each year, which we estimate saves £10.4 billion in 2029-30 relative to the state pension age remaining at 66. The majority (£10.2 billion) of these savings come from 820,000 fewer 66 year-olds receiving the state pension, with a further saving (£0.2 billion) from 40,000 fewer 66 year-olds receiving pension credit and winter fuel payment. This overall saving equates to 5.7 per cent of total pensioner spending in 2029-30.

These savings are partially offset by a rise in the number of people who remain eligible for working-age benefits as a result. There are currently around 60,000 65 year-olds (excluding mixed age couples)a in receipt of universal credit (UC), equivalent to 7.4 per cent of the 65-year old population. If the share of 66 year-olds in receipt of UC in 2029-30 remains at this level, and assuming average awards for 66 year-olds will be similar to those for 65 year-olds,b this would cost £0.7 billion in 2029-30.c

The rise in the SPA also creates incentives to join or remain in employment. The average employment rate for those in their mid-60s and above is at 11.9 per cent, significantly below the average employment for those aged 16-64 (74.8 per cent) as of 2024.d Previous analysis of the rise of the state pension age from 65 to 66 between 2018 and 2020 suggests that being under the state pension age increased the employment rate of 65 year-olds by 7.4 percentage points and 8.5 percentage points for men and women respectively.e A 2023 DWP evaluation of this rise indicated the increase led to an additional 55,000 65 year-olds in employment (mainly full-time employment) than if the SPA had remained the same, and an average increase in earnings of £52 per week across all 65 year-olds.f If the rise in the SPA to 67 results in a similar rise in employment and earnings, this would boost tax revenues by around £0.9 billion by 2029-30.

Overall, we estimate these channels result in an overall net fiscal saving of £10.5 billion from the SPA rising to 67 relative to it remaining at 66. This is subject to several uncertainties:

- The working-age welfare spending impact could be higher if a significant proportion of those affected by the loss of state pension income claim extra-cost disability benefits.

- The likelihood of entering or remaining in work is likely to be lower at older ages, so the employment response from the rise to 67 may not be as extensive as the rise to 66. However, over the longer run if demographic trends result in more people working at older ages, the benefits from this channel could increase.

- We have assumed that all of the increase in tax revenues is from people entering employment and paying an average tax rate of 34 per cent on their earnings. The actual tax increase would be dependent on the exact earnings and hours distribution.

We will return to the impacts of the rise in the SPA as part of a broader consideration of pensions-related risks in our 2025 Fiscal risks and sustainability report.

This box was originally published in Economic and fiscal outlook – March 2025