In our March 2025 forecast, we estimated that the Government's residential planning reforms will boost housebuilding by 170,000 and GDP by 0.2% by 2029-30. However, there are significant uncertainties around these estimates. In this box, we explored alternative scenarios for housebuilding and their corresponding impact on GDP.

This box is based on MHCLG, Northern Ireland Department for Communities, Scottish Government, StatsWales, and OBR data from July 2024, September 2024, November 2024, December 2024, and March 2025 .

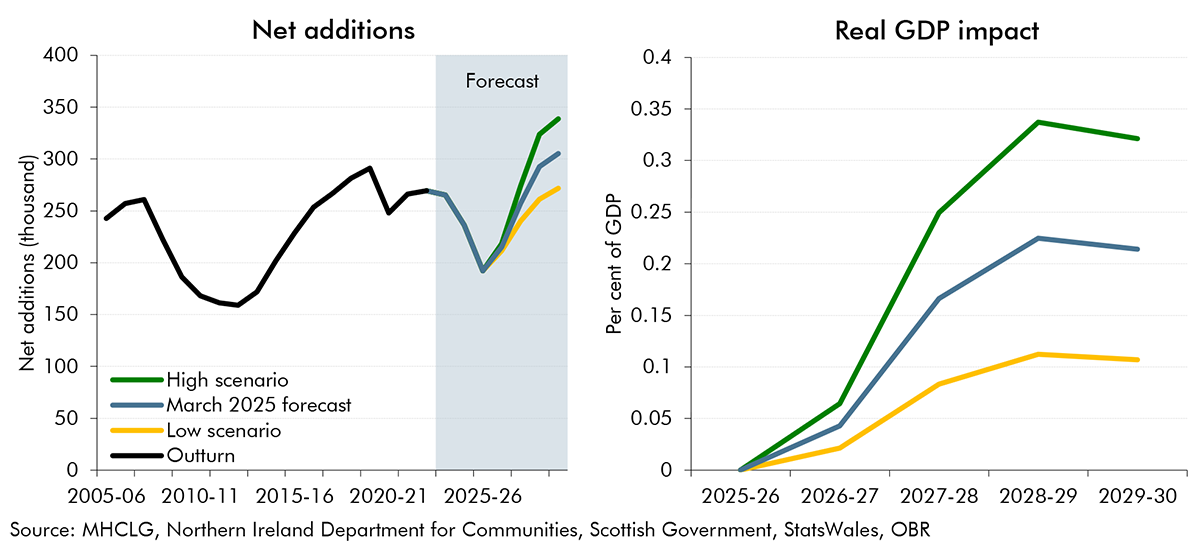

Our central forecast assumes cumulative net additions to the housing stock in the period to 2029-30 are under 1.3 million. Of this, we estimate 170,000 additions are due to the Government’s residential planning reforms and these raise GDP by 0.2 per cent at the forecast horizon. However, there are several significant uncertainties around this estimate. For instance, capacity constraints in the housebuilding sector could prove more binding than assumed if, for example, growing demands on a limited construction workforce hinder housebuilders’ ability to deliver a rapid acceleration in the flow of new houses. Or local opposition to reforms could prevent or delay housebuilding by more than we have assumed, particularly given much of the additional development in the next five years is assumed to take place on current green belt land. Conversely, growing economies of scale and greater adoption of modular construction

methods may enable sustained improvements in the sector’s efficiency and its capacity to build houses.

To illustrate the possible range of outcomes for housebuilding and potential output, we consider two alternative scenarios:

- In the low scenario, cumulative net additions are 1.2 million over the forecast period, a 0.1 million decrease relative to our central forecast. This results in a 0.1 per cent increase to GDP in 2029-30, as a smaller increase in investment leads to less of a pickup in construction sector productivity and, as the stock of houses is smaller, so are the housing services it generates.

- In the high scenario, cumulative net additions are over 1.3 million over the forecast period, a 0.1 million increase relative to our central forecast. The symmetric impacts result in a 0.3 per cent increase in GDP in 2029-30, primarily from the higher investment and associated increase in construction sector productivity, but also from the increased flow of services from a larger housing stock.

Chart 3B: Alternative housebuilding scenarios and their GDP impacts

This box was originally published in Economic and fiscal outlook – March 2025