"It is the duty of the Office to examine and report on the sustainability of the public finances"

Fiscal risks and sustainability – July 2025

The latest update of our assessment of the current pressures on the public finances was published in our Fiscal risks and sustainability report. Read the Executive summary for the key points from our analysis or the full report below.

Chapter 2 looks at the implications of demographics, savings, and other trends for the cost of the state pension, adequacy of future retirement incomes, and the structure of the gilt market.

Chapter 3 reviews the public sector balance sheet, looking at risks to the achievement of the Government’s new public sector net financial liabilities (PSNFL) target.

Chapter 4 updates our estimates of the fiscal costs of meeting the Government’s net zero commitments and of climate change-related damage to the UK economy.

Chapter 5 provides an update on the other risks in our fiscal risks register, it summarises the wider risks to the public finances and considers how these risks have evolved since our previous biennial survey in July 2023. Our risks register can be found in ‘Supporting documents’ below.

The Office for Budget Responsibility (OBR) was established in 2010 to examine and report on the sustainability of the public finances. A central feature of our efforts to meet that remit has been finding better ways to capture and communicate economic and fiscal risks. Ever since our first Economic and fiscal outlook (EFO) in 2010, we have emphasised the degree of uncertainty around our central forecasts by using probabilistic ranges (‘fan charts’), alternative scenarios, and sensitivity analysis. Since 2011, our Fiscal sustainability reports (FSRs) presented not only long-term projections of the public finances but also sensitivity analysis to changes in key demographic, macroeconomic, and other assumptions. Between 2017 and 2021, we also produced a biennial Fiscal risks report (FRR), setting out the main risks to the public finances, including macroeconomic and specific fiscal risks.

In the January 2022 update to the Charter for Budget Responsibility, Parliament amended the OBR’s remit to, in effect, give us greater discretion to determine the content of our annual sustainability report, which had previously alternated between the long-term projections in the FSR and the focus on risks in the FRR. Since July 2022, we have published our combined analysis in an annual Fiscal risks and sustainability report (FRS), which incorporates both our biennial long-term projections and updated analysis of major potential fiscal risks. As required under the Charter, the Treasury responded to our most recent September 2024 report in June 2025.[1]

In this FRS we focus on three areas of risk to the long-term fiscal outlook: the sustainability of UK’s system of public and private pensions; the performance of the government’s financial balance sheet and the risks around the new target for public sector net financial liabilities; and the potential economic and fiscal costs of climate-related damage and mitigation. We also update our fiscal risk register.

The analysis and projections in this report represent the collective view of the independent members of the OBR’s Budget Responsibility Committee. We take full responsibility for the judgements that underpin the analysis and projections, and for the conclusions we have reached. We have been supported in this by the full-time staff of the OBR, to whom we are, as usual, enormously grateful.

We have also drawn on the help and expertise of officials across numerous government departments and agencies, including HM Treasury, HM Revenue and Customs, the Bank of England, the Debt Management Office, the Climate Change Committee, the Office for National Statistics, the Department for Work and Pensions, the Government Actuary’s Department and UK Government Investments. We are very grateful for their insight.

In addition, we have benefited from discussions with experts from outside government. In particular, we would like to thank the Association of British Insurers, Green Alliance, the Institute for Fiscal Studies, Lane Clark & Peacock, Nest, the Pensions Policy Institute, the Pensions and Lifetime Savings Association, The Pensions Regulator, the Pension Protection Fund, the Resolution Foundation, Lord Stern of Brentford, Dimitri Zenghelis, Laurence Mutkin (BMO Capital Markets) and Professor Iain Clacher. We would also emphasise that despite the valuable assistance received, all judgements and interpretation underpinning the analysis and conclusions of the FRS are ours alone.

We provided the Treasury with a summary of our main conclusions on 27 June and a final version of this report on 4 July. Given the importance of the report to the Treasury in managing fiscal sustainability and risks, we have engaged with Treasury officials throughout the process.

At no point in the process did we come under any pressure from Ministers, special advisers or officials to alter any of our analysis or conclusions.

We would be pleased to receive feedback on any aspect of the content or presentation of our analysis. This can be sent to [email protected].

The Budget Responsibility Committee Richard Hughes, Professor David Miles CBE, and Tom Josephs

Executive summary

Introduction

1.1 The UK’s public finances have emerged from a series of major global economic shocks in a relatively vulnerable position. At the end of 2024, the UK government’s deficit stood at 5.7 per cent of GDP, around 4 percentage points higher than the advanced-economy average (Chart 1.1). This is the third highest among 28 advanced European economies, and the fifth highest among 36 advanced economies (after France, Slovakia, the US, and Israel). At 94 per cent of GDP, UK government debt is the fourth highest among advanced European economies, and the sixth highest among advanced economies (after Japan, Greece, Italy, France, and the US).[2] And with its 10-year bond yielding 4.5 per cent at the end of June, the UK government faces the third-highest borrowing costs of any advanced economy after New Zealand and Iceland.[3]

1.2 Efforts to put the UK’s public finances on a more sustainable footing have met with only limited and temporary success in recent years. Public sector net borrowing (PSNB) has oscillated around 5 per cent of GDP for the past four financial years. And while getting a measure of public debt falling as a share of GDP has featured in eight out of nine UK fiscal frameworks since 2010, underlying debt has risen by 24 per cent of GDP over the past 15 years and by 60 per cent of GDP over the past 20. The rise in debt since 2010 is partly due to the scale of the two major shocks that the global economy has experienced over this period: the Covid pandemic and the energy crisis. The UK economy has been particularly hard hit by those shocks, and government support to affected firms and households has been relatively generous by international standards. But in the aftermath of the shocks, debt has also continued to rise and borrowing remained elevated because governments have reversed plans to consolidate the public finances. Planned tax rises have been reversed, and, more significantly, planned spending reductions have been abandoned. The more persistent fiscal deficits and ratcheting up of debt that resulted have been accommodated by successive loosening of the fiscal rules.

Chart 1.1: Borrowing across advanced economies, and UK government debt

Note: Underlying debt refers to public sector net debt excluding the Bank of England. Right panel shows OBR forecasts for underlying debt at selected March fiscal events. Source: IMF, OBR

1.3 The result has been a substantial erosion of the UK’s capacity to respond to future shocks and growing pressures on the public finances. Underlying public debt is now at its highest level since the early 1960s and is projected to rise further over the medium term. Arresting this increase has become considerably more challenging as economic growth has slowed and interest rates risen. Despite the tax-to-GDP ratio rising to the highest level in the period since 1950, borrowing is still 3 per cent of GDP above the level that would be needed to durably stabilise debt. And the Government has left itself very small margins against its objectives of restoring the current budget to balance and getting net financial liabilities to fall by the end of the decade. Despite this, public expectations of what government can and should do in response to emerging threats and future emergencies seem to be rising.[4]

1.4 There are signs that the scale of public borrowing in the UK and other large, advanced economies is putting global sovereign debt markets under pressure. Government borrowing costs have risen across the world and long-term gilt yields are now higher in the UK than at any point since the start of the century. Uncertainty about the future path of inflation and fiscal policy in the US, Europe, and Japan has fuelled persistent volatility in sovereign bond yields since the start of the year. And governments in the UK and across advanced economies have shortened the maturity of their new borrowing and are increasingly looking abroad for investors as domestic appetite for their longer-dated debts wanes.[5]

1.5 Against this more challenging domestic and global backdrop, the scale and array of risks to the UK fiscal outlook remains daunting. Since our fiscal risk register was last updated in the July 2023 Fiscal risks and sustainability report (FRS), some risks have been addressed. Most notably, a set reforms to the institutional arrangements for fiscal policymaking have reduced the risks of major fiscal announcements outside the semi-annual forecasting cycle, permanently extended the planning horizon for departmental expenditure, and tightened controls over the creation of contingent liabilities. At the same time, a number of major global risks have crystallised and remain a major source of uncertainty around the medium-term fiscal outlook. In particular, as foreshadowed in our 2022 report, rising geopolitical tensions have given rise to the largest increase in effective global tariff rates in over a century and put the UK and other European countries under pressure to increase defence spending to their highest levels since the end of the Cold War. Over the long term, the demographic pressures of an ageing population and rising costs of healthcare and other age-related expenditures are still, on current policy settings, projected to push borrowing above 20 per cent and debt above 270 per cent of GDP by the early 2070s.

1.6 This 2025 FRS explores three sources of risk in greater depth:

Chapter 2 looks at the UK system of public and private pensions, focusing on the implications of demographics and other trends for the fiscal cost of the state pension, the adequacy of future retirement incomes, and demand for government debt;

Chapter 3 reviews the structure and composition of the public sector balance sheet, and considers the risks to the achievement of the Government’s new public sector net financial liabilities (PSNFL) target;

Chapter 4 updates our estimates of the risks from climate change including the fiscal costs of meeting the Government’s net zero commitments and of climate-related damage to the UK economy; and

Chapter 5 covers the other risks in our fiscal risk register, how they have evolved since our last update in July 2023, and any mitigating actions the Government has taken in the interim.

The pensions system (Chapter 2)

1.7 Pensions are an important element of public budgets, household finances, and the financial system. In the UK the state pension is the second-largest item in the government budget after health. Private pension savings are the second-largest asset (after housing) for households. And pension funds and insurance companies with pension liabilities are major holders of government debt, accounting for around a third of gilt holdings in 2023-24.

1.8 The UK pensions system has changed considerably over the past couple of decades. In the state system, recent reforms have introduced a rising state pension age (SPA) linked to life expectancy and a higher flat-rate state pension that is uprated by the triple lock, guaranteeing that it increases each year by the highest of average earnings, CPI inflation, or 2.5 per cent. In the private system, automatic enrolment of employees has increased the number of people saving in occupational pensions while, outside the public sector, the nature of these schemes has shifted from defined benefit (DB) to defined contribution (DC) schemes.[6] These reforms have addressed some concerns around the incomes of current and future pensioners: reliance on means-tested pension credit has fallen from around 23 per cent of individuals of SPA in 2010-11 to around 12 per cent in 2023-24, while automatic enrolment has increased eligible private-sector employees’ pension enrolment from 42 per cent in 2012 to 86 per cent in 2023.

1.9 However, the structure of the pensions system and its likely development over time also give rise to a set of longer-term fiscal pressures and risks that we examine in this report:

a potentially significant increase in the direct fiscal cost of state pension spending over the coming decades due to the triple lock and an ageing population;

the fact that some groups are not saving enough into private pensions to provide them with adequate incomes in retirement, giving rise to both direct and indirect risk to the public finances; and

the decline of DB pensions reducing the demand for gilts and pushing up the Government’s financing costs.

1.10 Spending on the state pension has risen steadily over the past eight decades. It rose from around 2 per cent of GDP in the mid-20th century to around 5 per cent of GDP (£138 billion) today, and is estimated to rise further to 7.7 per cent of GDP by the early 2070s in our central long-term projection. The main drivers of these past and projected trends are:

Demographic changes: The number of adults below SPA per pensioner fell from 3.4 in the early 1970s to 3.2 in the early 1980s. This ratio then flattened out before rising during the 2010s, but is expected to fall again to 2.7 by the early 2070s. This is consistent with projections of life expectancy at birth rising from around 89 to 94 years, and life expectancy at age 65 rising from 21 to 26 years. These demographic changes explain 1.6 percentage points of the projected 2.7 percentage point rise in state pension spending as a share of GDP over the next 50 years. This is sensitive to assumptions around future demographic trends (left panel of Chart 1.2):

in a high life expectancy scenario where life expectancy at 65 instead reaches 29 years by the early 2070s, state pension spending would be 0.7 per cent of GDP higher than in our central projection; and

in a low life expectancy scenario where life expectancy at 65 instead falls slightly to 20 years, spending would be 0.8 per cent of GDP lower at the projection horizon.

Changes to the SPA: The SPA rose to 65 for women over the course of the 2010s and then rose to 66 for both sexes between 2018 and 2020. Three further increases are anticipated over our 50-year projections – to 67 by March 2028, 68 in the late 2030s and 69 in the early 2070s – which are collectively expected to reduce annual state pension spending by around 1 per cent of GDP by the early 2070s, relative to the SPA staying at 66.

The triple lock uprating mechanism: In the central long-term projection, uprating the state pension using the triple lock, rather than earnings uprating, explains a further 1.6 percentage points of the 2.7 per cent of GDP rise in state pension spending by the early 2070s. The impact of the triple lock on pension spending is highly sensitive to assumptions about the future volatility and level of inflation and earnings growth, which is explored in the scenarios described below.

Chart 1.2: Scenarios for state pension spending as a share of GDP

Source: DWP, ONS, OBR

1.11 Due to inflation and earnings volatility over its first two decades in operation, the triple lock has cost around three times more than initial expectations. When it was introduced in 2012, initial estimates assumed that triple lock uprating would result in state pension increases averaging 0.2 percentage points above earnings growth. Based on these assumptions, the move from an earnings-linked to a triple-locked pension would have cost an equivalent of £5.2 billion in 2029-30. In fact, inflation has turned out to be significantly more volatile over this period and earnings growth has been lower, with the non-earnings elements of the lock triggered in eight of the 13 years to date. As a result, and despite the suspension of the triple lock for one year during the pandemic, the triple lock is expected to have cost £15.5 billion annually by 2029-30, around three times higher than initial expectations.

1.12 If this heightened volatility in inflation and earnings were to persist over the next fifty years, this could add an additional 1.5 per cent of GDP (£43 billion in 2024-25 terms) to state pension spending by the early 2070s. By way of illustration (right panel of Chart 1.2):

Our central projection for state pension spending is based on the pattern of earnings and inflation outturns between 1992-93 and the present and sees state pension spending rise from around 5 per cent of GDP in 2024-25 to 7.7 per cent of GDP by the early 2070s.

Were the future behaviour of inflation and earnings to look like the more volatile period from 2010-11 onwards, state pension spending would be 1.5 per cent of GDP (£43 billion in 2024-25 terms) higher by the early 2070s relative to our central projection.

By contrast, were inflation and earnings to look more like the, less volatile, two decades prior to the triple lock’s introduction, spending would be 1.3 per cent of GDP (£38 billion in 2024-25 terms) lower by the early 2070s.

1.13 Despite the increasing generosity of the state pension, recent studies suggest a significant proportion of the population may not be saving enough through private pensions to achieve an ‘adequate’ retirement income. Current pension income in the UK is, in aggregate, broadly evenly split between income from the state pension and income from private pensions. Automatic enrolment has more than doubled the share of eligible employees in the private sector saving into a private pension. Nevertheless, projections in these studies suggest that around 40 per cent of working-age individuals are likely to fall short of the Pensions Commission’s ‘target replacement rate’ for pension income relative to working-age income, while around 10 per cent would fall short of a ‘minimum living standards’ benchmark, even if the triple lock is maintained.[7] These results are based on average projected returns to pension savings, but the shift from DB to DC pensions also means individuals are now exposed to the risk of low or volatile returns. Three groups emerge from this analysis as those for whom the fiscal risks associated with under-saving may be highest:

Due to the increased generosity of the state pension, around 80 per cent of low earners are projected to achieve target replacement rates. However, a third are projected to fall short of the minimum living standards benchmark. This could create direct and indirect fiscal costs and pressures as these individuals may claim means-tested benefits or require state support for social care costs. However, these pressures are likely to be lower than has been the case for past pensioners due to the new flat-rate and triple-lock-uprated state pension and the growing effects of auto-enrolment.

Private renters are more likely than average to have inadequate retirement incomes, with the DWP estimating that almost half will fall short of target replacement rates and a quarter will miss the minimum living standards benchmark. This creates fiscal risks as high ongoing housing costs relative to income drive eligibility for pensioner housing benefit. The likely projected rise in the pensioner renter population, from around 6 per cent today to 17 per cent by the 2040s, would entail around a £2 billion (in today’s terms) increase in housing benefit spending. Indirect pressures on social care costs may also result given housing assets are taken into account in social care means tests.

The self-employed are particularly at risk of inadequate retirement incomes because fewer than one-in-five are enrolled in a private pension scheme (compared with over four-fifths of eligible employees). As a result, around three-fifths of the self-employed are projected to miss both the target replacement rate and the minimum living standards benchmark. This leads to both direct fiscal costs via pensioner benefits, and potentially also wider pressure to support those who have spent a large share of working life in the low-earning and less secure forms of self-employment that have become more prevalent in recent decades.

1.14 The shift from DB to DC pensions also creates a more direct fiscal risk by reducing what has historically been one of the most important sources of demand for UK government debt. Over the past 25 years, pension funds and insurance companies have had relatively stable gilt holdings. In that time, the total stock of gilts has risen from 28 per cent of GDP to 84 per cent of GDP, meaning the share of gilts held by pension funds and insurance companies has fallen steadily from around two-thirds in 1998-99 to around one-third in 2023-24 (Chart 1.3). As the share of gilts held by the pensions sector has declined, overseas investors and the Bank of England (through its Asset Purchase Facility), have become the largest and second-largest holders of gilts at 31 and 29 per cent respectively.

Chart 1.3: Gilt holdings by sector

Note: Right panel uses gilt holdings data in the final quarter of the financial year as consistent quarterly data are not available pre-1997. Source: ONS

1.15 The overall ageing of the UK population is likely to mean greater demand for all assets, including gilts, in future. Analysis using our new UK Overlapping Generations model suggests that the stock of assets could rise by around 25 per cent of GDP between 2023 and 2074 to reach around 400 per cent of GDP. This is driven by a shift in the population age structure towards older cohorts at a more asset-rich stage of their lives. And this stronger overall demand for assets could, all things equal, put a small amount of downward pressure on returns on UK assets. But what is true for the demand for assets in general is not necessarily true for the demand for UK gilts, which our modelling of the UK pensions sector suggests will go in the other direction.

1.16 The shift from DB to DC pensions is likely to result in significantly lower pensions sector holdings of gilts as a share of GDP. At the end of 2024, private sector DB schemes held 52 per cent of their total assets in the form of gilts, especially long-term and index-linked gilts which closely match their liabilities. Yet 86 per cent of scheme members in this sector are in schemes closed to new joiners. By contrast, DC schemes hold a more diverse portfolio of UK and global equities and bonds, with only 7 per cent of their total assets in UK gilts. Based on modelling of DB and DC schemes’ membership, contributions, asset holdings, decumulation, and insurance buy-outs, in our central projection over the next 50 years:

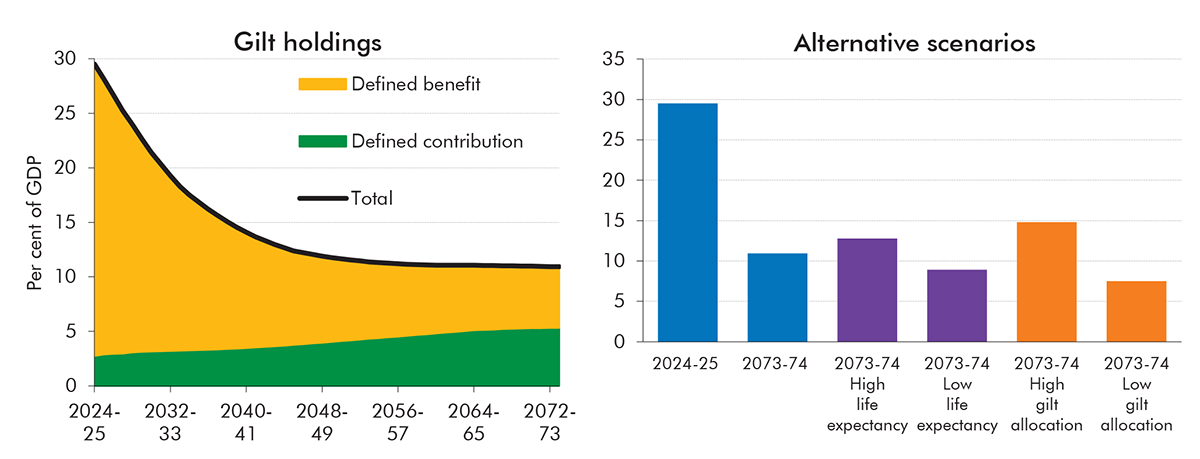

Total pension scheme holdings of gilts as a share of GDP are projected to fall by 18.6 percentage points from 29.5 per cent of GDP in 2024-25 to 10.9 per cent of GDP in the early 2070s (left panel of Chart 1.4), within which:

DB pension holdings are projected to fall from 26.7 per cent of GDP today to 5.6 per cent of GDP in the early 2070s, by which point schemes which are today closed to new members will have almost entirely wound down their assets. The bulk of remaining DB gilt holdings at this point are in open schemes, including funded public sector schemes; and

DC pension holdings are projected to rise from 2.8 per cent of GDP today to 5.3 per cent of GDP by the early 2070s, by which point DC accounts for the vast majority of private sector pension provision, but entails lower contribution rates in working age and a lower allocation of assets to gilts.

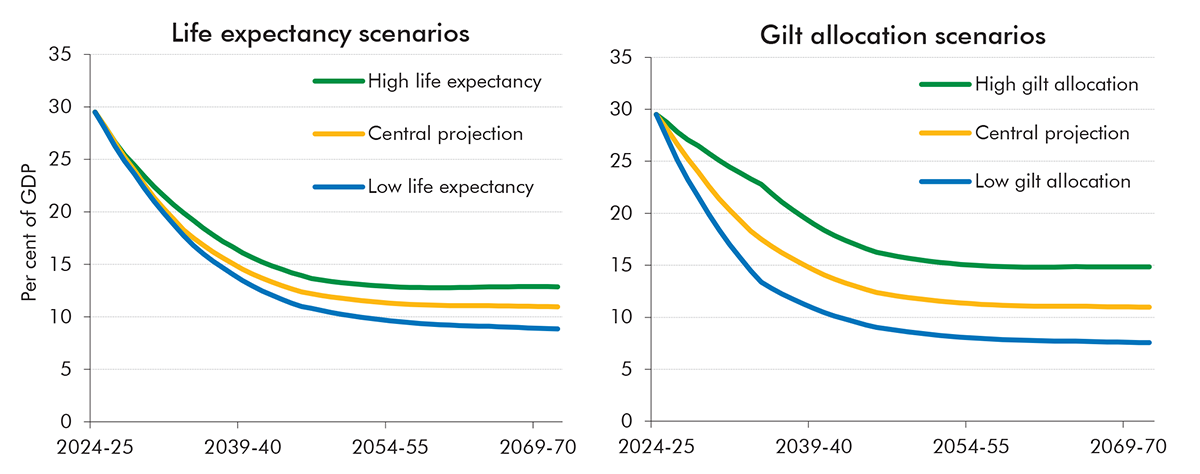

Given the inherent uncertainties around these projections, we also explored a set of alternative scenarios in which average life expectancy at 65 is around four years higher or lower, and average gilt allocations by pension schemes are 25 per cent higher or lower by 2073-74 (right panel of Chart 1.4). In all alternative scenarios, gilt holdings by the pensions sector are projected to at least halve as a share of GDP by the early 2070s.

Chart 1.4: Projected pensions sector gilt holdings, and alternative scenarios

Source: OBR

1.17 This decline in the pensions sector’s gilt holdings could push up interest rates on government debt by around 0.8 percentage points, assuming the stock of debt remains close to 100 per cent of GDP. Higher interest rates would be needed to entice more price-elastic buyers than pension funds, such as overseas investors, into the UK gilt market. With debt at 100 per cent of GDP, this could eventually increase debt interest spending by £22 billion (in today’s terms). The impact on interest rates and debt interest costs could be lower if the market has already anticipated and therefore priced in these trends, especially at longer maturities where demand has already fallen the most. The Government has already in recent years sought to reduce issuance of the longest-maturity debt in response to this declining demand. This reduces its exposure to long-term rates but increases its refinancing risk and makes total interest costs more sensitive to short-term shifts in market sentiment.

Public sector balance sheet (Chapter 3)

1.18 In October 2024, the newly elected Government adopted a new fiscal rule targeting public sector net financial liabilities (PSNFL). This represented a break with the stock targets that have featured in all-but-one previous UK fiscal frameworks since 1997, which focused on the narrower balance sheet aggregate of public sector net debt (PSND). While PSND captures all debt liabilities of the public sector, it only nets off its holdings of liquid financial assets (principally foreign exchange reserves and cash deposits) (Figure 1.1). Relative to PSND, PSNFL captures a greater range of financial liabilities, notably those of funded public sector pension schemes, and illiquid financial assets, notably loans and equity investments. It is still narrower in coverage than the most comprehensive measure of the public sector balance sheet, public sector net worth (PSNW) which captures all liabilities, including those of unfunded public sector pension schemes, and all assets including non-financial assets, such as land, buildings, military equipment, infrastructure, and intangible assets.

Figure 1.1: Comparison of public sector balance sheet aggregates

Source: OBR

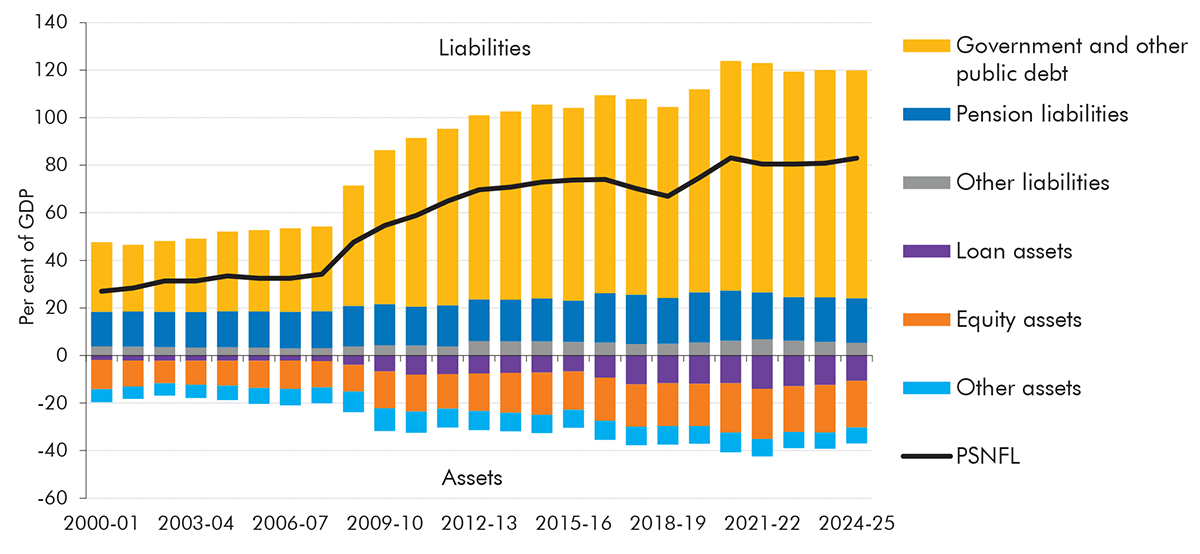

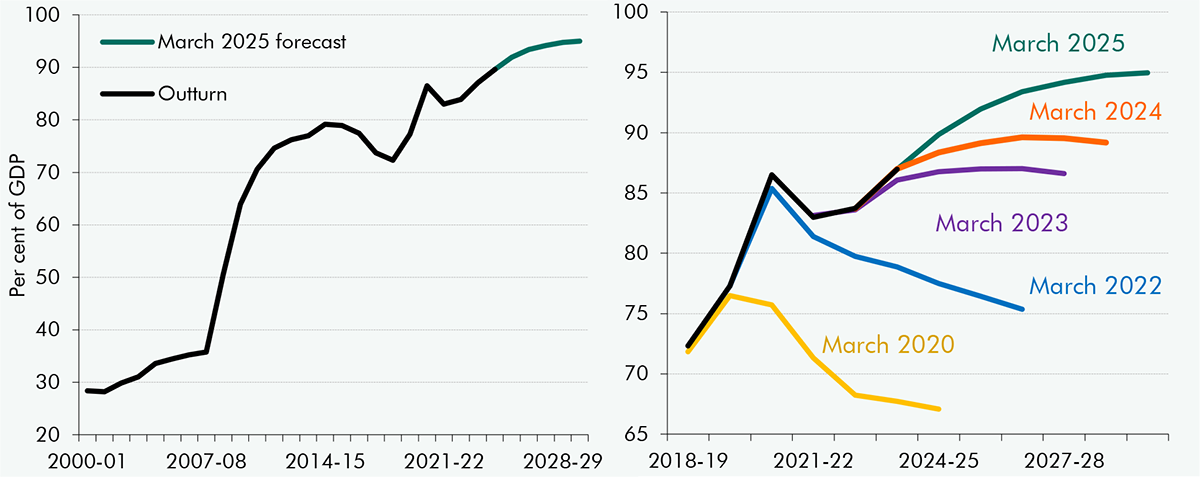

1.19 Over the past two decades, the size and complexity of the government’s financial balance sheet has expanded considerably. Since 2004-05, PSNFL has more than doubled from 33 per cent of GDP to 83 per cent of GDP last year (Chart 1.5). Within this:

Financial liabilities have more than doubled as a share of GDP from 57 per cent in 2005-06 to 132 per cent at the end of 2024-25. Much of this comes from an increase in government bond (gilt) issuance to finance the large and persistent deficits over much of this period. Since 2008, a significant proportion of these liabilities have been in the form of Bank of England reserves issued to finance the purchase of gilts under quantitative easing, and to issue loans under the Term Funding Scheme (TFS) and its predecessors. Both these schemes are now unwinding, though these reserves still stood at £713 billion at the close of 2024-25. The final significant financial liabilities are the pension promises of funded public sector pension schemes, mainly the Local Government Pension Scheme, which have increased steadily over this period from 15 to 19 per cent GDP.

Financial assets have nearly doubled as a share of GDP from 26 per cent in 2005-06 to 50 per cent at the end of 2024-25. The single-largest element today is the 20 per cent of GDP in equities now held mainly by funded public sector pension schemes. The second-largest asset on the financial balance sheet is loans which amounted to 11 per cent of GDP in 2024-25. Student loans worth £139 billion account for about half of that total, with another £91 billion in loans from the TFS and various forms of policy lending by bodies such as the British Business Bank (BBB) and the National Wealth Fund (NWF) accounting for the remainder.

Chart 1.5: Assets and liabilities within PSNFL

Source: OBR

1.20 Historically, year-to-year changes in the value PSNFL have been driven by public sector net borrowing (PSNB), but, since the financial crisis, movements in a wider range of financial assets and liabilities have also been important (Chart 1.6):

In all but two of the past 20 years, PSNB has accounted for the vast bulk of the year-to-year change in PSNFL. Government has financed this borrowing mostly by the net issuance of gilts (yellow). In periods where the Bank of England has bought gilts from the market for the purposes of its quantitative easing programme, this has led to a reduction of gilts in the private sector, financed by the net issuance of reserves (green).

Especially in times of economic and financial stress, the public sector has also made active use of loans (purple) and equity investments (orange) as a tool of public policy. The Government acquired shares in RBS and Lloyds as part of its interventions at the height of the financial crisis. In the wake of the Brexit referendum and then the Covid pandemic, the Bank used the creation of additional reserves to fund the issuing of loans under the TFS and its small and medium enterprise successor (TFSME). Government has also acquired a large stock of student loans since the 2012-13 reforms to higher education financing.

Pension liabilities (dark blue) have, in some years, accounted for significant changes in the level of PSNFL. In particular in 2016-17 when the discount rate applied to future payments was reduced, sharply increasing the present value of pension liabilities.

Other assets and liabilities (grey), which includes assets such as deposits and taxes owed but not yet paid, and liabilities such as monies owed by the government but not yet settled, have had modest impacts on PSNFL over this period.

Chart 1.6: Year-on-year changes in PSNFL by assets and liabilities

Source: ONS

1.21 The risks to the medium-term outlook for PSNFL can be decomposed into three components:

Transactions, which are the difference between (a) spending on consumption and non-financial assets, or the purchase or sale of financial assets at amounts that differ from their market value, which will increase PSNFL; and (b) receipts from taxes and other sources which will decrease PSNFL. The sum of all transactions over a given period is equal to PSNB, which is the flow equivalent of PSNFL.

Valuation changes to the stocks of assets or liabilities already held on the balance sheet. This will happen for all assets recorded at their market value, such as listed equities, or for assets held in foreign currencies. Valuation changes also can arise from impairments, such as write-downs in the value of non-performing loans.

Classification changes, when the ONS moves the recording of institutions or other bodies in and out of the public sector. This can cause the level of PSNFL to change with no corresponding transaction or valuation change recorded, if the financial balance of the reclassified body is different from that of the rest of the public sector.

1.22 In the 2025 Spending Review, the Government increased its planned use of financial transactions over the next four years by £9.6 billion. This means a total of £26.4 billion has now been allocated for financial transactions within the departmental expenditure limits (DEL) envelope. Ensuring that our forecasts for PSNFL reflect the worth of the financial assets created or acquired through these transactions requires us to value them appropriately. Recording loans at their nominal value may be appropriate for high-quality loans. For example, loans held by the NWF are expected to make credit losses of under 4 per cent. But for other loans, losses are expected to be much higher. For example, losses on Start up loans issued by the BBB are expected to be between 30 and 40 per cent. The ONS is currently reviewing the recording of loans on the balance sheet and there is a risk that at least some get significantly revalued.

1.23 Unexpected changes to the recorded value of financial assets and liabilities already on the public sector balance sheet can also pose a risk to the outlook for PSNFL. These changes can occur either due to real world events or reassessments by the ONS. In this report we look at the sensitivity of PSNFL to downside shocks from:

a revaluation due to a 1 percentage point change in discount rates used to value funded public sector pension liabilities. This might be due to changes in economic conditions that prompt a change to the long-run expectations that drive discount rates, or due to other conceptual changes by the ONS;

a 10 per cent fall in the market value of the equity assets of funded public pension schemes and general government equity holdings; and

a 30 per cent decrease in the value of central government loan assets excluding student loans. These are loans primarily held by public financial institutions including the BBB and NWF. Such a revaluation might be driven by deteriorating economic conditions or from revisiting over-optimistic initial modelling assumptions.

1.24 The shocks would raise the level of PSNFL by between 1.0 and 2.6 per cent of GDP in the year of the shock (Chart 1.7). In these sensitivities the shock occurs in 2025-26, four years before the year targeted by the fiscal rules (2029-30). As the impact of the shock on the trajectory of PSNFL is greatest in the first year of the forecast and muted thereafter, the current fiscal rule, which targets PSNFL falling in the final year of the forecast, would not be broken in any scenario. But the downward trajectory of PSNFL in the target year is changed in all scenarios, being somewhat shallower in the loan valuation scenario but slightly steeper in the other two scenarios.

Chart 1.7: Public sector net financial liabilities: sensitivity to shocks

Source: OBR

1.25 A final set of risks to the outlook for PSNFL come from the potential reclassification of ‘near public sector’ bodies which are currently classified to the private sector but provide essential services or serve an important public policy purpose. We look at the scale of the reclassification risk from three such bodies, all of which pose a risk to PSNFL because they have significant net financial liabilities (which are captured in PSNFL) backed by significant non-financial assets (which are not captured in PSNFL). These are:

Water companies which had £91 billion in debt and other financial liabilities, £12 billion in financial assets, and £94 billion in non-financial assets (mainly the water network) in 2023-24. Based on these figures, were the water companies to come onto the public sector balance sheet, PSNFL could increase by around £78 billion (2.8 per cent of GDP).

Housing associations which had £111 billion in debt and other financial liabilities, £12 billion in financial assets, and £223 billion in non-financial assets (mostly houses) in 2023-24. Based on these figures, were housing associations to come into the public sector, PSNFL could increase by around £99 billion (3.5 per cent of GDP).

Higher education institutions which had £37 billion in debt and other financial liabilities, £45 billion in financial assets (mostly a few large endowments), and £66 billion in non-financial assets (mostly land and buildings) in 2023-24. Based on these figures, were the whole sector to come into the public sector it could reduce PSNFL by around £8 billion (0.3 per cent of GDP). However, absorbing the most vulnerable 39 higher education institutions, which have large liabilities and relatively small financial endowments, could increase PSNFL by around £ 1 billion (less than 0.1 per cent of GDP).

1.26 There are further risks to the public balance sheet from contingent liabilities, which are liabilities that are not included on the balance sheet but may crystallise at some point in the future. UK Government Investments (UKGI) estimates that a relatively small fraction (£16 billion of the £250 billion total) might be expected to expire in the next five years and so represent a risk to PSNFL, if the resulting costs are manged outside of DEL allocations. In the longer run, there are more significant risks from contingent liabilities related to nuclear decommissioning, which UKGI projects will crystallise costs of £115 billion largely over 30 years from now.

1.27 There are also considerations around the return on the assets held on the balance sheet. It is currently not possible to gauge the relative riskiness of the Government’s financial assets, though UKGI aims to report on the quality of the balance sheet in its Financial Investment Report, starting from this autumn. A simple calculation based on the effective interest rate on assets and liabilities recorded in PSNFL suggests the interest return on assets is considerably lower (2.9 per cent in 2024-25) than the Government’s cost of financing (3.2 per cent) and therefore presumably considerably lower than a risk-adjusted rate would be.

Climate change (Chapter 4)

1.28 Climate change poses significant risks to economic and fiscal outcomes in the UK. Over the past five years the average global temperature was 1.3-1.4 °C above pre-industrial levels (left panel of Chart 1.8). This is the highest level since global records began, and temperatures are on course to exceed, by 2029, the Paris Agreement goal to limit the rise to 1.5°C above pre-industrial levels. The costs of a hotter and more volatile climate are also rising, with the latest estimated 10-year average economic and insured losses from extreme weather up by 29 and 38 per cent, respectively, on the previous rolling 10-year average (right panel of Chart 1.8).

Chart 1.8: Global climate change indicators and climate-related damages

Note: Temperature anomaly refers to global-average temperature in each year relative to the average temperature for the pre-industrial period. Source: Left panel: Copernicus, Met Office Hadley Centre, NOAA; right panel: Swiss Re

1.29 Climate change creates risks to the public finances through three main channels:

mitigation: the fiscal costs incurred to transition from a fossil fuel-based to a net zero emissions economy;

damage: the costs to government from the damage to the economy and public finances caused by a hotter climate with more extreme weather; and

adaption: the costs to government of measures taken to reduce the impact on, and increase the resilience of, the economy to higher temperatures and increasingly volatile and extreme weather.

1.30This FRS updates and integrates previous OBR analysis of the fiscal risks from climate mitigation, produced in 2021, and from climate damage, produced in 2024. In the period since each of these analyses was produced, there have since been significant developments in the evidence base on climate change and to climate change policy. These include: a further increase in global average temperatures in recent years; more comprehensive and up-to-date estimates of climate-related damage costs; updated estimates of the economy-wide costs of transitioning to net zero in the Climate Change Committee’s (CCC’s) Seventh Carbon Budget advice; and greater clarity about the UK Government’s plans for meeting its share of those costs in the 2025 Spending Review. Therefore, in this report, we:

update our previous estimates of the potential fiscal costs of climate damage;

update our previous estimates of the potential fiscal costs of climate mitigation;

combine these two estimates to obtain a more comprehensive picture of the overall net fiscal cost of climate change;

compare these estimates against the Government’s climate-related spending plans; and

explore a range of alternative scenarios for both damage and mitigation costs.

1.31Our latest estimate is that the fiscal costs from climate-related damage could add 2.0 per cent of GDP to primary borrowing by the early 2070s, 0.7 percentage points higher than our previous estimate. This is based on a scenario where global temperatures rise to just below 3°C above pre-industrial levels.[8] The increase in estimated costs under this scenario compared to our previous estimate is due to using a more comprehensive and up-to-date analysis of the economic damage from a changing climate. This is now estimated to reduce the level of GDP by 8 per cent by the early 2070s, 3 percentage points more than in the 2024 FRS projection (Chart 1.9). The bulk of the fiscal costs from this increased damage are due to lower productivity and employment and therefore lower tax receipts. The accumulated impacted of higher primary borrowing and the additional debt interest costs could add 56 per cent of GDP to debt by the early 2070s, 23 percentage points higher than our previous estimate.

Chart 1.9: Impact on GDP and government borrowing of climate change damage

Source: NGFS, OBR

1.32Our latest central estimate of the fiscal cost of climate change mitigation through to 2050-51 is £803 billion (21 per cent of GDP), or £30 billion a year on average, of which two-thirds can be attributed to lost receipts (Chart 1.10). Expenditure accounts for the bulk of the fiscal cost in the next decade, particularly public investment in residential buildings, removals and surface transport. Receipts losses – mainly from lost fuel duty receipts – rise steadily over the projection period. The impact of the net zero transition on the public finances is a function of:

The share of the whole-economy investment costs borne by the state. In our central scenario, we assume that government bears around 36 per cent of the CCC’s latest estimate of the whole-economy costs, which would amount to around £9.9 billion (0.3 per cent of GDP) per year between 2025 and 2050. The net zero investment spending for the next four years announced by the Government in the 2025 Spending Review is broadly in line with this assumption.

The extent to which government replaces the revenue losses from declining consumption of hydrocarbons. In our central scenario, these revenue losses amount to £20.5 billion (0.5 per cent of GDP) per year on average between 2024-25 and 2050-51. Of this, three-quarters comes from declining fuel taxes as petrol-driven cars are replaced by electric vehicles.

1.33There is considerable uncertainty around the economic and fiscal costs associated with climate change mitigation. The fiscal cost of the net zero transition could be lower if governments chose to replace the lost revenues from fuel duty, for example through an alternative motoring tax, or if they chose to fund a lower share of the economy-wide investment path, for example through relying more on regulation to deliver the transition. It could be higher if governments choose to fund a higher share of the investment costs and rely less on regulation or taxation to achieve the transition.

Chart 1.10: Annual fiscal costs of the net zero transition

Source: CCC, HMRC, OBR

1.34Our latest central estimate of the costs to government of the net zero transition, of 21 per cent of GDP, is 9 per cent of GDP lower than the previous estimates in the 2021 Fiscal risks report. This reduction is mainly driven by the CCC’s latest estimates of the whole-economy investment cost of reaching net zero. This reduction in climate mitigation costs stands in contrast to the rising costs of climate damage since our previous assessment, which unlike transition costs are driven by the degree to which the major global emitters reduce their emissions over the coming decades, rather than what happens in the UK.

1.35Taken together, in the 3°C central scenario the combined fiscal impacts of climate damage and mitigation could add 74 per cent of GDP to government debt by the early 2070s, relative to our latest long-term projection. Of this rise, mitigation costs contribute around a tenth of the total, while the indirect and direct costs from climate damage contribute around three-fifths, including via the effects of lower growth in the nominal GDP denominator. The remaining costs come from the interest costs of servicing the additional debt issued to finance the higher primary borrowing. The baseline long-term projection from our 2024 FRS included losses from fuel duty, at 16 per cent of GDP by the early 2070s, which take the fiscal impact of climate change to 108 per cent of GDP at that point when added to the purely additional costs explained above.

1.36Given the significant uncertainty around the path of global temperatures, the cost of climate-related damage to the economy, and the share of net zero transition costs that might be borne by government, we explore a range of alternative scenarios for the fiscal impact of climate change. The results of these, relative to our 2024 FRS baseline, are shown in Chart 1.11:

A below 2°C scenario which incorporates the fiscal impacts of below 2°C damage and central public investment costs. Compared to our central scenario, this adds 26 per cent of GDP less to debt by the early 2070s.

A high fiscal share scenario which incorporates the fiscal impacts of below 3°C damage and assumes the government accepts a higher share of economy-wide investment costs of getting to net zero. Compared to our central scenario, this adds 3 per cent of GDP more to debt by the early 2070s.

A low fiscal cost scenario which incorporates the fiscal impacts of below 3°C damage and assumes the government accepts a lower share of economy-wide investment costs and finds a replacement for the lost revenue from motoring taxes. Compared to our central scenario, this adds 40 per cent of GDP less to debt by the early 2070s. However, this scenario outcome is reliant on industry and households paying more of the wider economy costs of the net zero transition.

Lower and higher GDP damage scenarios which incorporate the fiscal impacts of a lesser or greater GDP hit from the below 3°C rise in temperature. Compared to our central scenario, these add 29 per cent less and 63 per cent more to debt, respectively, by the early 2070s.

Chart 1.11: Climate change scenarios: PSND differences from baseline in 2073-74

Source: OBR

1.37In addition to these quantified scenarios, there are significant uncertainties about the path of climate change and its economic and fiscal consequences that cannot, for the moment, be readily quantified. One important missing piece of our analysis of the overall climate cost puzzle for the UK is the economy-wide and fiscal cost of adapting to climate change, and its knock-on effects for the degree of climate-related damage. Other factors that could significantly increase or reduce the projected economic and fiscal costs of climate change include:

On the upside: an accelerated global transition where the world significantly invests and speeds up decarbonisation; greater-than-expected economic resilience to a changing climate; and technological advances which could make net zero generation technology cheaper.

On the downside: tipping points where climatic events cause large and irreversible changes to global climate; untested new technologies which may not deliver carbon reductions as fast as currently assumed; and a more significant reduction in UK growth due to economic spillovers from the impact of more extreme climate damage elsewhere in the world.

Risk register (Chapter 5)

1.38A more comprehensive survey of developments in the array of risks recorded in our fiscal risk register confirms that risks to the fiscal outlook remain elevated since our last update in the 2023 FRS. Of the 50 risks on the register, 12 have increased, three have been added, and 11 have crystallised but remain active risks. Only nine have decreased and one has been resolved.[9]

1.39There has been a significant crystallisation of all three of the geopolitical risks to the public finances, explored in our 2022 FRS, in the form of both rising trade tensions, upward pressures on defence spending, and growing cyber threats:

While the trade negotiations between the US and its other major trading partners are ongoing, scenarios included in our March 2025 Economic and fiscal outlook estimated that a 20 percentage point increase US tariffs on all goods imports that was not reciprocated by other countries would see the UK current budget deficit rise by around £10 billion (0.3 per cent of GDP) a year on average. The imposition of additional reciprocal tariffs by other countries would have a similar impact. If fully implemented, the US administration’s ‘Liberation Day’ tariffs would represent the US imposing an estimated 16.1 per cent weighted average tariff on goods imports.[10] This is a 14.6 percentage point increase relative to 2022, a similar magnitude to the former scenario.

On defence, in its 2025 Spending Review, the Government announced an increase in defence spending from 2.4 per cent of GDP in 2024-25 to 2.6 per cent in 2027-28, funded via a cut in overseas aid. Meeting the new NATO target of spending 3.5 per cent of GDP on core defence by 2035 would require spending to rise by a further £38.6 billion.

Cyber-attacks have continued to intensify, as evidenced by the recent attacks on the Legal Aid Agency, HMRC, and Marks & Spencer. We estimate that a cyberattack on critical national infrastructure has the potential to temporarily increase borrowing by 1.1 per cent of GDP.

1.40Domestic economic, demographic, social, and financial trends also continue to generate pressures and risks to the public finances. Significant increases in health-related welfare caseloads have seen onflows for incapacity and working-age disability benefits double since the pandemic. Our forecast assumes that health-related onflows will fall halfway back to pre-pandemic levels by the end of the decade. Were current onflow levels instead sustained across the forecast period, welfare spending would be roughly £12 billion higher than forecast in 2029-30. Interest rates remain highly volatile with the 10-year gilt rate ranging from 3.5 to 4.9 per cent between January 2024 and January 2025. With net debt around 100 per cent of GDP, a 1 per cent increase in gilt yields would increase debt interest spending by around 1 per cent of GDP (£30 billion in 2024-25 terms) in the long run. The tax-to-GDP ratio is forecast to reach a historic high of 37.7 in 2027-28, with uncertainty around both the impact this will have on the economy and around the yield from key policy measures which deliver this increase.

1.41Some changes to fiscal policymaking frameworks have reduced fiscal risks, but unfunded policy announcements present new risks. The introduction of the fiscal lock and extension to the planning horizon for departmental spending have reduced fiscal risks relating to the announcement of significant fiscal policy measures that are not reflected in medium-term forecasts and budgets. But policy announcements such as the recent announcements on increasing defence spending by 2035, reversing planned cuts in winter fuel payments, and scaling back planned welfare reforms, present new downside risks to the fiscal position.

1.42Given recent shocks to economy and public finances – and particularly in the light of the magnitude of the risks described in the report – any appreciation of the fiscal outlook cannot be based solely on a central forecast of tax, spending, borrowing, and debt but needs to take account of the inevitability of unexpected, and often negative, shocks.

Chapter 2: The pensions system

Introduction

2.1 In all advanced economies, pensions are an important element of public budgets, household finances, and the financial system. In the UK, expenditure on the state pension, at £138 billion (around 5 per cent of GDP) in 2024-25, is the second-largest item in the government budget after health. Private pension savings, estimated at £3.2 trillion (114 per cent of GDP) in 2024, are the second-largest asset on household balance sheets after housing. And private pension funds held around a third of all gilts in 2023-24.[11]

2.2 The size and structure of the UK pension system gives rise to three distinct fiscal risks:

The design of the state pension triple lock means the public finances are asymmetrically exposed to shocks to inflation and earnings growth, both of which have been unusually volatile in recent years. This feature of the triple lock, combined with the overall ageing of the population, means that in our latest long-term fiscal projections, state pension spending was, after health, the second-largest source of upward pressure on non-interest spending. It accounted for around a quarter of the 10.8 percentage point projected increase in the primary deficit over the next 50 years.[12]

The 2012 policy of automatic enrolment into defined contribution pension schemes has significantly increased participation in private pensions among private sector employees.[13] However, there are still gaps in coverage and many individuals risk not saving enough to provide an adequate retirement income, which could create fiscal pressures on future governments.

Structural changes in the private pension market, particularly the decline of defined benefit schemes in the private sector in favour of defined contribution schemes, are affecting the demand for, and therefore the cost of, government debt over both the medium and long term.

2.3 This chapter explores in greater depth the potential fiscal risks stemming from the public and private pensions systems. It:

surveys the UK pension system in both international and historical context;

examines the fiscal risks associated with state pensions;

explores recent trends in the level and composition of private pension savings, and potential fiscal risks posed by low pension saving among future retirees; and

considers the implications of the structural shift away from defined benefit to defined contribution pensions for the demand for gilts.

The UK pensions system in context

UK pensions in international context

2.4 Aggregate pension payments in the UK are currently split roughly evenly between the state pension and pensions from a wide range of private schemes. Broadly speaking, the UK system for current and future retirees comprises:

a largely flat-rate (non-earnings-related) state pension linked to past contributions, alongside some means-tested pensioner benefits;

a large, tax-incentivised private pensions system comprising a mix of defined benefit and defined contribution occupational and personal schemes.

2.5 Comparing pensions internationally is complex given the diversity of approaches to retirement income provision.[14] However, OECD analysis suggests total UK public pensions spending is at the low end of advanced economies, and the UK relies more on private pension income than most other advanced economies (Chart 2.1). This balance means that, in principle, UK public spending is less directly exposed to demographic pressures than other countries. On the other hand, this means there are indirect risks to public spending if private pensions do not provide adequate retirement incomes in future.

Chart 2.1: Public and private pension benefit spending in OECD countries, 2019

Note: Private pension spending reflects the income received by pensioners, not the contributions made in working life. Numbers for Ireland are expressed as a percentage of gross national product. Source: OECD

The UK pensions system

2.6 Both the public and private elements of the UK pensions system have undergone considerable change over the past 20 years, spurred by the 2002-06 Pensions Commission. Its recommendations included: a rising state pension age (SPA) linked to life expectancy; a flat-rate state pension linked to earnings; and the automatic enrolment of employees into funded pensions saving with a right to opt-out, with a modest compulsory matched employer contribution.[15] To a very large extent, these recommendations were implemented in the years that followed, albeit with a ‘triple-locked’ rather than simply earnings-linked state pension. ‘Pension freedoms’, subsequently introduced in 2015, gave people the right to withdraw defined contribution and personal pensions from the age of 55 without having to purchase an annuity.

2.7 As a result, today’s state pension is paid at a flat rate (unless deferred) to all qualifying individuals above the state pension age. This ‘new state pension’, awarded to those reaching SPA from April 2016 onwards, reaches £230.25 per week in 2025-26 for individuals who have the at least 35 qualifying years of National Insurance contributions. It entails higher awards for lower earners than the predecessor basic state pension, while removing separate earnings-related elements. It is supplemented by pension credit and other means-tested support for low-income pensioners. Since 2012, the ‘triple lock’ has stipulated that the basic and new state pensions should be uprated annually by the highest of earnings growth, CPI inflation, or 2.5 per cent.

2.8 Private pensions now have two main forms:

Defined benefit (DB) schemes pay a guaranteed income in retirement linked to past years of service and earnings, funded by employee and employer contributions and returns on accumulated assets. DB schemes are, outside the public sector, now largely closed to new contributions – only 7 per cent of private sector employees were contributing to one in 2021, compared to 82 per cent of public sector employees.[16] In terms of membership, the size of the DB sector has therefore declined, and this is likely to continue over time.

A rising share of private pension saving is instead in defined contribution (DC) schemes, where employees and their employer make tax-free contributions into a fund that grows with market returns.[17] Pension freedoms mean that at any age from 55 (set to rise to 57), individuals can either draw down flexibly from this fund or convert it into an annuity which pays out a fixed yearly income until death, or do both (draw down flexibly and then convert into an annuity). In 2021, 66 per cent of all private sector employees were participating in a DC scheme or personal pension, up from 22 per cent in 2012. This rapid increase reflects the roll-out of automatic enrolment, which has seen over 11 million employees begin saving since 2012.[18]

2.9 Of the £3.2 trillion of assets in pension schemes in 2024, around 55 per cent are in DB schemes, with just over two-thirds of these in private sector DB schemes and the remainder in public sector funded DB schemes. This proportion will fall steadily over the coming decades as private sector DB continues to decline and automatic enrolment into DC schemes continues to build.

2.10 The majority of public sector workers are in an unfunded pension scheme, with payments to pensioners covered by the contributions from current employees topped up as needed by the Exchequer. These schemes had liabilities estimated at £1.4 trillion as of the end of 2024-25, although these are not counted within the public sector net financial liabilities (PSNFL), the balance sheet metric that features in the Government’s fiscal rules. Box 3.1 in Chapter 3 provides further detail and an assessment of the fiscal risks and pressures associated with these schemes. Other public sector DB schemes, notably the Local Government Pension Scheme (LGPS), are funded and therefore do appear on the financial balance sheet of the public sector. As set out in Chapter 3, these are recorded in PSNFL with a total of around £550 billion in assets and liabilities in 2024-25.

The state pension and fiscal sustainability

2.11 This section explores fiscal risks and pressures related to the state pension. It outlines the key drivers of changes in state pension spending over the recent past, and then explores scenarios for state pension spending over the coming 50 years based on variations in demography and policy settings.

The increasing cost of the state pension

2.12 Spending on state pensions as a share of GDP has risen steadily over the past eight decades (Chart 2.2). The around 5 per cent of GDP (£138 billion) spent on state pensions in 2024-25 is, as a share of the economy, around 35 per cent higher than 50 years ago, and 15 per cent higher than in 2010-11. As well as other long-term drivers discussed below, the latter reflects the introduction of the higher flat-rate state pension (uprated by the triple lock) during the 2010s. This helped reduce reliance on means-tested pension credit, whose claimants fell from 2.7 million (23 per cent of individuals of state pension age) in 2010-11 to 1.4 million (12 per cent of individuals) in 2023-24.[19]

2.13 Based on the assumptions set out below, in the long-term projections in our 2024 Fiscal risks and sustainability report (FRS) state pension costs are set to rise further to 7.7 per cent of GDP by the early 2070s, around 50 per cent higher than today. In addition, spending on other benefits targeted at pensioners is projected to increase from 1.0 to 1.3 per cent of GDP between 2024-25 and 2073-74. This is mostly attributable to a 0.2 percentage point projected increase in spending on disability benefits.

2.14 This projected rise in spending on the state pension is the second-largest increase in non-interest spending after health in our long-term projections. It is therefore a major contributing factor to the conclusion in each of the long-term projections we have produced over the past 15 years that, if current policy settings were to be maintained over the long run, debt would be on an unsustainable path.

Chart 2.2: Pensioner spending as a share of GDP

Note: Outturn data is taken from DWP’s 2025 Benefit expenditure and caseload tables, the forecast from our March 2025 Economic and fiscal outlook, and the projection is based on applying the same growth rates as in our 2024 FRS. Nominal GDP is consistent with the projection in our 2024 FRS. DWP outturns use a different accounting basis to our forecast, which can result in small differences in estimates of state pension spending, but the difference is negligible by 2029-30. The forecast and projection include three increases to the state pension age between 2026 and 2028 to 67, 2037 to 2039 to 68, and 2072 to 2074 to 69. ‘Other pensioner benefits’ relate to pension credit, attendance allowance, disability living allowance, housing benefit and income support. Source: DWP, OBR

2.15 The main drivers of the trajectory of state pension spending seen over the past 80 years and projected for the next 50 years are:

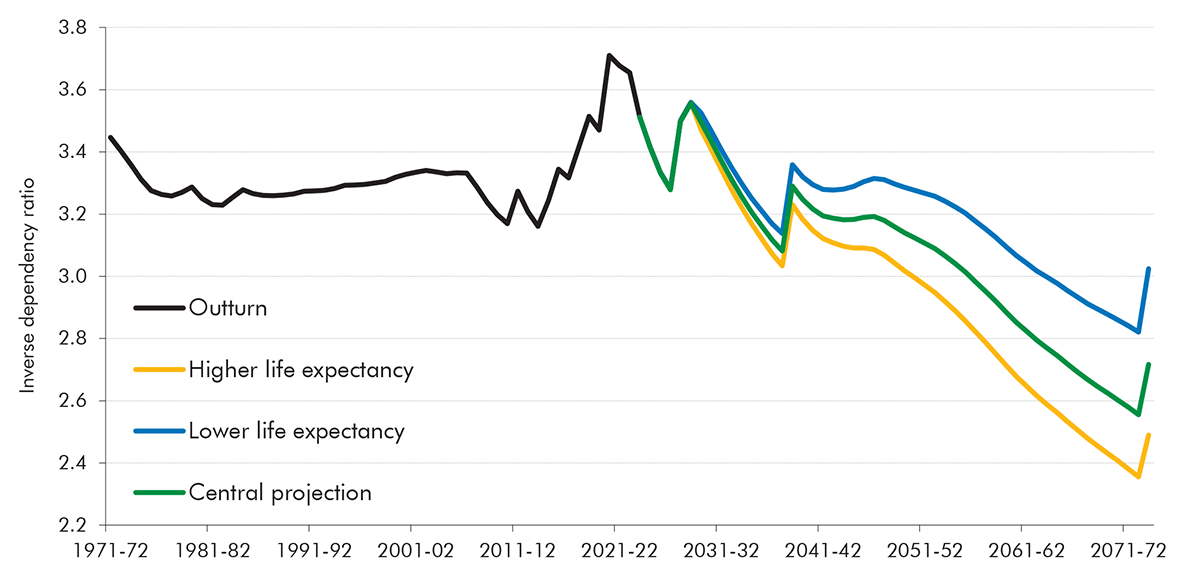

Demography, due to generational dynamics and rising life expectancy, particularly changes in the ratio of working-age population relative to pensioner population. This ratio fell from the mid-20th century to the early 1980s as the large pre-war generations moved into retirement and life expectancy increased, with the number of working-age people per pensioner falling from 3.4 in 1971-72 to 3.2 in 1981-82 (Chart 2.3). This ratio then flattened out until the mid-2000s as rising life expectancies were counterbalanced by the large baby boomer generation being in prime age, before increasing during the 2010s due to the rising female SPA and the effects of working-age immigration. The ratio of working-age people to pensioners is expected to begin falling again in the future, from 3.4 today to 2.7 by the early-2070s, as life expectancy continues rising and the baby boomers move through retirement. These dynamics correspond closely with the state pension spending patterns seen in Chart 2.2. Demographic changes over the projection period explain 1.6 percentage points of the rise in state pension spending as a share of GDP over the next 50 years. Chart 2.3 also presents alternative projections for the working-age-to-pensioner ratio on the basis of higher and lower life expectancy assumptions. These are described in the next section and used in our scenarios for state pension spending and gilt holdings.

Changes to the state pension age, which rose for women from 60 to 65 across the 2010s, and then increased for both men and women from 65 to 66 between 2018 and 2020. This temporarily stabilised state pension spending as a share of GDP in the 2010s. We similarly expect the legislated rise in the SPA to 67 by March 2028 to drive a dip in state pension spending as a share of GDP for a couple of years in the late 2020s (Chart 2.2). Over the projection, in line with stated government policy, we assume a further rise in the SPA to 68 between 2037 and 2039, and to 69 between 2072 and 2074. As discussed below, we estimate that these three SPA increases collectively reduce state pension spending in the early 2070s by around 1 per cent of GDP.

The mechanism for uprating the annual value of state pension entitlements. An earnings link was removed in the late 1970s, and the state pension was usually uprated in line with prices from then until the early 2010s, contributing to the flatter trajectory of spending as a share of GDP over this period shown in Chart 2.2. Since 2012 the triple lock uprating mechanism has been in place. Its effects in the years since then do not stand out on Chart 2.2 mainly due to the offsetting impact of the changes to the SPA in this period. Nevertheless, the cost of the triple lock over this period has been substantially higher than originally expected due to the combined volatility of earnings and inflation, as we explore in more detail below. In our central projection we assume that triple lock uprating is an average of 0.53 percentage points above earnings growth, in line with inflation and earnings outturns since 1992-93. This explains 1.6 percentage points of the 3.1 percentage point rise in state pension spending as a share of GDP over the next 50 years. The risks around this assumption are discussed in more detail below.

Chart 2.3: Demographic projection and scenarios

Note: Inverse dependency ratio defined as the number of adults below state pension age divided by the number of individuals at state pension age and above. State pension age changes are implemented in whole years rather than gradually in this chart. The higher and lower life expectancy scenarios are based on the change in the high life expectancy variant for those aged 70 and over in the ONS’s 2018 population projections, from which we derive either positive or negative changes to apply to the 2021-based population projections underpinning our most recent long-term projections. More detail on the mortality assumptions underpinning this variant can be found at: ONS, National population projections, mortality assumptions: 2018-based, October 2019. Source: ONS, OBR

How much more has the triple lock cost than originally estimated?

2.16 The triple lock was announced in the June 2010 Budget for implementation from April 2012 onwards.[20] At the time, the OBR’s estimate of the cost of the triple lock by the end of the 2010 forecast period in 2014-15 was £0.5 billion a year, relative to a baseline assumption of earnings uprating. This was based on forecasts for inflation and earnings growth which assumed that over this period the triple lock would only be triggered in 2012-13 and 2013-14, by 0.6 and 0.4 percentage points, respectively, compared to earnings uprating. We also assumed that, over the long run, triple lock uprating would be an average of 0.2 percentage points per year higher than earnings growth.[21]

2.17 In practice the triple lock has cost around three times more than initial expectations. This is primarily because the period since 2012 has seen more volatile inflation and lower earnings growth than the two decades prior to the triple lock’s introduction. The left panel of Chart 2.4 shows that the non-earnings elements of the lock have been triggered in eight of 13 years to date, and they are expected to be triggered in three of the five years of our latest medium-term forecast. As a result, we estimate that uprating by the triple lock rather than earnings will have added £15.5 billion (0.5 per cent of GDP) to state pension spending annually by 2029-30. This is around three times higher than the £5.2 billion we estimate the triple lock would have cost by that point under initial assumptions (right panel of Chart 2.4).[22] Relative to CPI uprating, we expect that the triple lock will have added £22.9 billion to annual state pension spending by 2029-30.

Chart 2.4: State pension uprating and spending

Note: The triple lock has been in effect for uprating of the basic (and later, new) state pension from 2012-13 onwards, with the exception of 2022-23 when a ‘double lock’ was applied, which is accounted for in the modelling in the right panel. The right panel presents the evolution of basic and new state pension spending, to which the triple lock has applied since 2012-13, with the uprating assumptions underpinning the original triple lock costings and, beyond that, the initial long-run expectation that the triple lock would outpace earnings growth by 0.2 percentage points a year on average. Source: DWP, ONS, OBR

Scenarios for state pension spending over the long term

2.18 In the central projection, spending on the state pension is projected to rise from around 5 per cent of GDP in 2024-25 to 7.7 per cent of GDP in 2073-74, as shown in Chart 2.2 above. The following sections explore how this trajectory is shaped by the key factors set out above – demographics, rises in the state pension age, and the path of triple lock indexation – and the implications of alternative scenarios for life expectancy and triple lock uprating.

Demographics

2.19 In the 2021-based ONS population projections underpinning our 2024 FRS projection, the pensioner population is expected to grow more than twice as fast as the working-age population up to 2073-74. This is consistent with shifts in the population age structure, alongside life expectancy at birth rising from around 89 to 94 years, and life expectancy at age 65 rising from 21 to 26 years.[23]

2.20 The future level of spending on the state pension is highly sensitive to trends in life expectancy. As seen in Chart 2.5, under the two alternative demographic scenarios from Chart 2.3 above:[24]

in a high life expectancy scenario where life expectancy at 65 instead reaches 29 years by the 2070s and there are 1.9 million more pensioners than in the central projection, state pension spending would be 0.7 per cent of GDP higher in the early 2070s than in our central projection; and

in a low life expectancy scenario where life expectancy at 65 instead falls slightly to 20 years and there are 1.9 million fewer pensioners than in the central projection, spending would be 0.8 per cent of GDP lower at the projection horizon.

Chart 2.5: State pension spending under different demographic scenarios

Source: DWP, ONS, OBR

State pension age

2.21 Future spending on the state pension is also sensitive to assumptions about future rises in the state pension age. The central long-term projection set out above is conditioned on the assumptions that the SPA rises from 66 to 67 between 2026 and 2028, to 68 between 2037 and 2039, and to 69 between 2072 and 2074.[25] The 2018 Fiscal sustainability report estimates that each single-year increase in the SPA reduces state pension spending by around 0.3 per cent of GDP, meaning the three increases in our current long-term projection collectively reduce state pension spending in the early 2070s by around 1 per cent of GDP. This is broadly consistent with the medium-term estimate, set out in Box 6.1 of the March 2025 Economic and fiscal outlook (EFO), that the rise to 67 in the late 2020s will reduce state pension spending by around £10 billion by the end of the decade.

Triple lock uprating

2.22 As discussed above, future levels of pension spending are also highly sensitive to the future path of inflation and earnings. Our latest long-term projection is based on an updated assumption that triple lock uprating averages 0.53 percentage points above earnings growth in the long run, on the basis of observed earnings growth and inflation outturns in the period since 1992-93. However, recent trends in inflation and earnings have proven much more volatile than was experienced at the time the triple lock was legislated for.

2.23 Chart 2.6 explores the implications of alternative assumptions for the impact of the triple lock on long-run state pension spending. It shows that:

our central projection sees state pension spending rising to 7.7 per cent of GDP by 2073-74, 1.6 per cent of GDP higher than if the state pension were uprated with earnings, which was the policy in place prior to the triple lock’s introduction;

were the future behaviour of inflation and earnings to look more like the more volatile period from 2010-11 onwards, triple lock uprating would average 0.93 percentage points above earnings growth, and state pension spending as a share of GDP would reach 9.1 per cent by the early 2070s, 1.5 percentage points higher than in our central projection; and

were the future behaviour of inflation and earnings to look more like the less volatile period from the early 1990s through to 2009-10, triple lock uprating would average 0.11 percentage points above earnings growth, and state pension spending as a share of GDP would reach 6.3 per cent by the early 2070s, 1.3 percentage points lower than in our central projection.

Chart 2.6: State pension spending under different triple lock scenarios

Note: Spending on the basic and new state pension only, to which the triple lock applies. Source: DWP, ONS, OBR

2.24 In conclusion, while changes to the state pension have played a substantial role in reducing reliance on means-tested pensioner benefits in recent years and improving retirement income adequacy in future (discussed in detail below), they have also contributed to state pension spending becoming a large and growing fiscal risk. Over the next 50 years, the ageing population and the continuation of the triple lock would both put significant, and roughly equal at around 1.6 per cent of GDP, upward pressure on state pension spending. And further risks stem from the uncertainty around these pressures. A plausible range for life expectancy improvements would increase or decrease state pension spending in the early 2070s by around 0.7 per cent of GDP. The risk in relation to the triple lock appears even larger. Alternative trajectories for the triple lock, based on earnings and inflation outcomes over different periods within the past three decades, could increase or decrease spending by around 1.4 per cent of GDP in the early 2070s. These risks are only partially offset by planned and anticipated increases to the state pension age, which collectively reduce spending by around 1 per cent of GDP.

Private pensions and savings adequacy

2.25 As discussed above, pension income in the UK is, at the aggregate level, currently broadly evenly split between state support and income from private pensions. The relative importance of private pensions means that the UK public finances are less directly exposed to demographic pressures than in some other countries. However, the reliance on private pensions could also potentially create indirect fiscal pressures on future governments. If future incomes from private pension savings were insufficient to provide some groups with what is considered to be an adequate standard of living in retirement, this could create pressure on future governments to provide additional state support. Fiscal risks associated with under-saving for retirement could crystallise through the following channels:

Direct fiscal costs: from an increase in the cost of the supplements to pensioner income provided by the welfare system. Under the current system, this could result from increased claims for means-tested support such as pensioner housing benefit and pension credit.

Indirect fiscal costs: from the state having to cover more of the cost of areas such as social care, which is currently funded both privately and by the state. Social care demand is projected to rise sharply in the coming decades,[26] and those with little or no savings for retirement will likely have their costs met by the state. In 2023-24 the average cost of a local authority funded care home place in England for someone over the age of 65 was around £47,500 a year.[27]

Wider pressure to support retirement incomes for under-savers may emerge, such as that which gave rise to pension credit and the winter fuel payment in the late 1990s and early 2000s, when pension incomes had fallen behind those still of working age.

2.26 This section considers these risks further by assessing evidence on the adequacy of private pension saving in the UK in recent studies by the Department for Work and Pensions (DWP) and the Institute for Fiscal Studies (IFS).

Projections of the adequacy of private pension savings

2.27 The introduction of automatic enrolment into DC pension schemes in 2012 has dramatically increased pension participation among eligible private sector employees, from 42 per cent in 2012 to 86 per cent in 2023 (Chart 2.7). Participation among public sector employees has remained high across the period, averaging over 90 per cent since 2003.

Chart 2.7: Pension enrolment by eligible employees and the self-employed

Note: Public sector and private sector employees based on Annual Survey of Hours and Earnings data in April of each year, showing the share of employees eligible for automatic enrolment enrolled in a pension. Self-employed based on Family Resources Survey data based on all ages in financial years. Source: DWP