The independent Office for Budget Responsibility was established in 2010 to monitor the public sector’s finances. Twice a year – usually alongside each Budget and Spring or Autumn Statement – we produce detailed forecasts for the coming five years, assessing the likely impact of any policy decisions and expected developments in the economy. Once a year, usually alongside the Budget, we use these forecasts to assess the Government’s performance against the fiscal targets that it has set itself for the management of the public finances.

This guide provides a brief introduction to the UK public finances and to the terms used to describe them in the official statistics. In doing so we are looking at the finances of the public sector as a whole – which encompasses not just central government, but also the devolved administrations, local councils and public corporations. The figures presented in this guide are taken from our March 2026 forecast, which covers the five fiscal years up to 2030-31. Each fiscal year runs from April to March.

The figures presented in this guide are taken from our March 2026 forecast, which covers the five fiscal years up to 2030-31. Each fiscal year runs from April to March.

A pdf version of this guide is also available to download here:

This guide provides a brief introduction to the UK public finances and to the terms used to describe them in the official statistics. We describe the main sources of government income and spending, and explain how these are used to calculate whether the government is running a surplus or a deficit. We also explain how government debt is defined and calculated.

Overview

In each forecast we assess how the public finances are likely to evolve on the basis of existing Government tax and spending policies and our best guess at the likely evolution of the economy. In particular we try to estimate:

- How much money the public sector will raise from taxes and other sources of revenue. In 2025-26, we expect it to raise £1,235 billion, equivalent to around £43,000 per household or 40.4 per cent of national income.

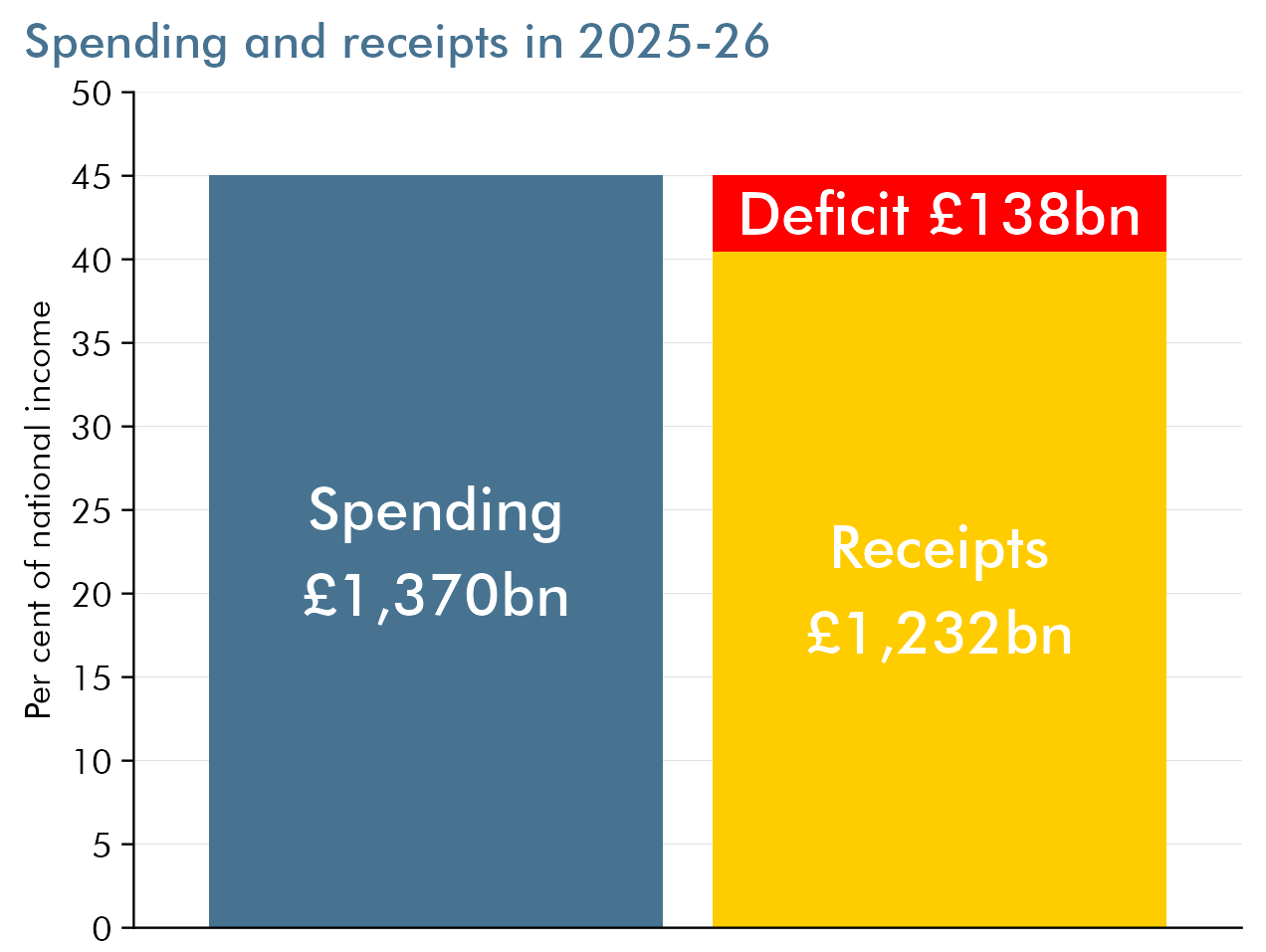

- How much it will spend on things like public services, state pensions and debt interest. In 2025-26, we expect it to spend £1,368 billion, equivalent to around £48,000 per household or 44.8 per cent of national income.Whether it will spend more or less than it raises – in other words whether it will run a budget deficit or surplus. In 2025-26, we expect a deficit of £133 billion. Because the growth in receipts outpaces that of spending, we expect the deficit to fall over the next five years to £59 billion.

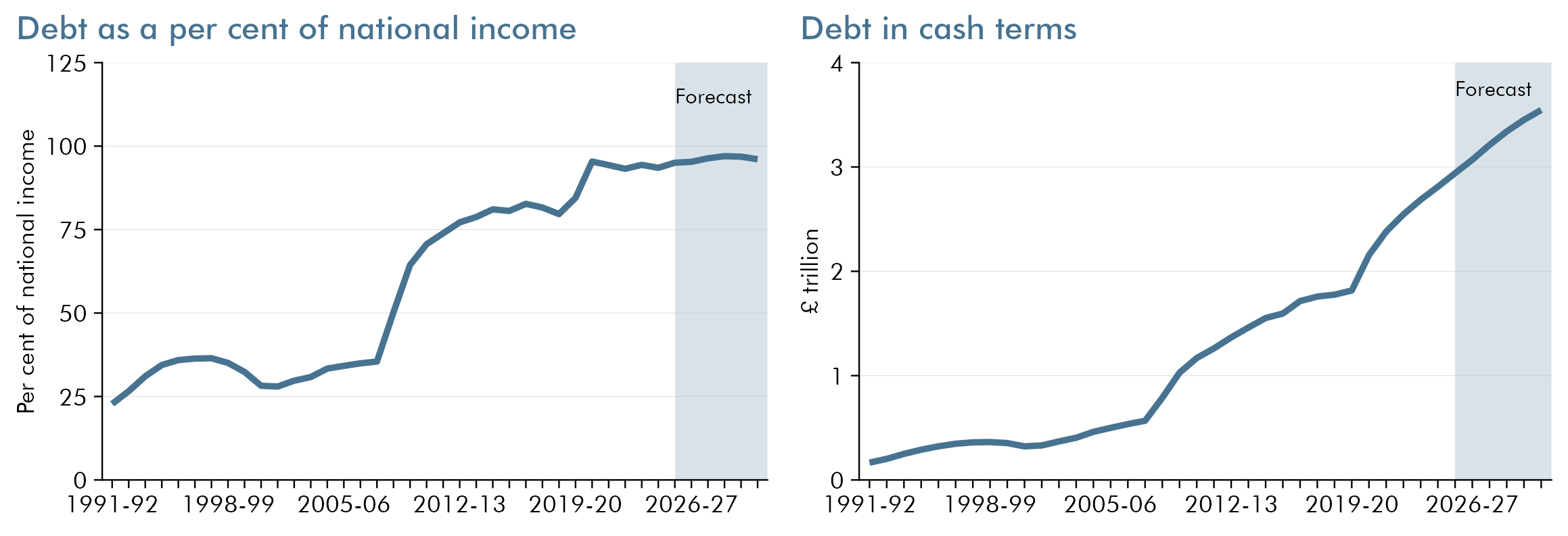

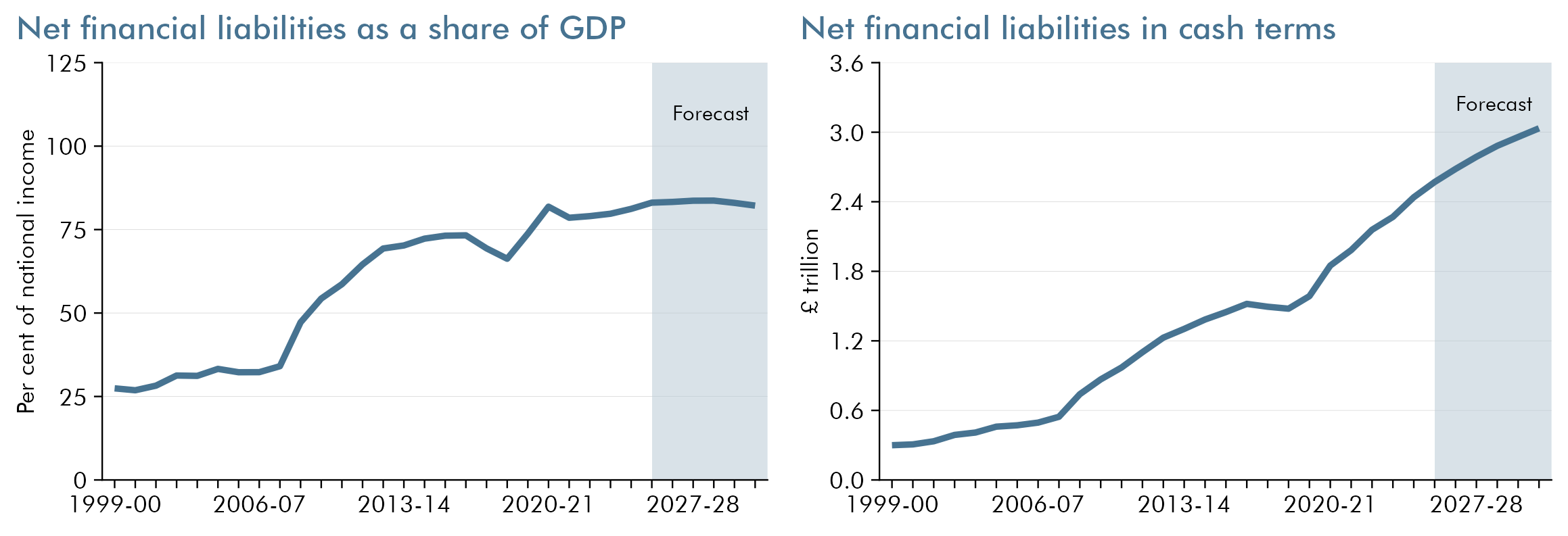

- How much will be added to – or paid off – the national debt in each year. In 2025-26, we expect debt to be equivalent to 94.3 per cent of national income. It is equivalent to around £2.9 trillion or £102,000 per household. We expect the ratio of net debt to national income to peak in 2028-29 before falling gradually to reach 95.1 per cent in 2030-31. In cash terms we expect it to stand at £3.5 trillion by then. Net financial liabilities – a measure that also accounts for financial assets like student loans – are expected to be 82.4 per cent of GDP in 2025-26 and 81.1 per cent in 2030-31.

Income

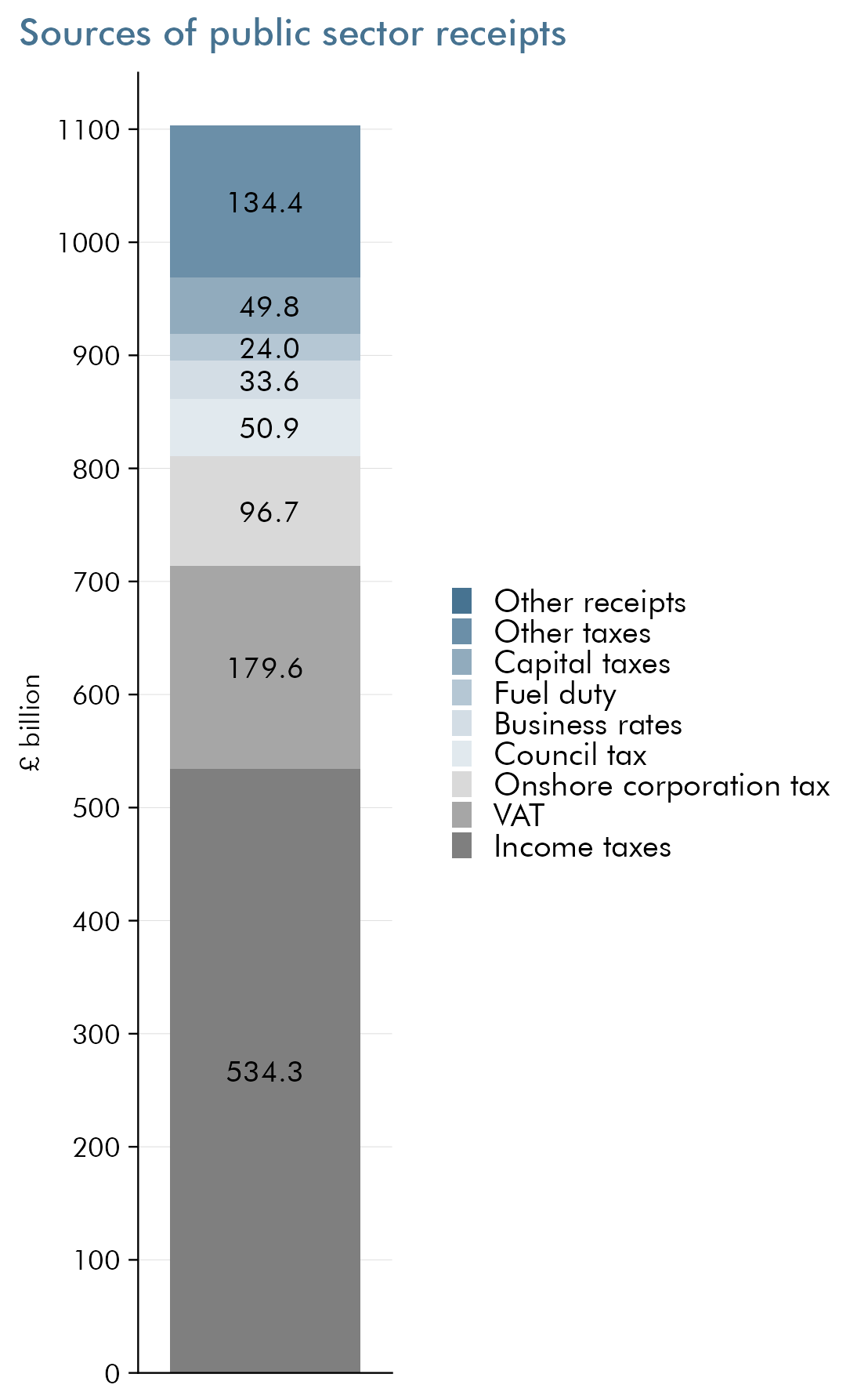

In 2025-26, we expect the public sector’s income to amount to £1,235 billion, equivalent to £43,000 per household or 40.4 per cent of national income. This income is called ‘public sector current receipts’ in the official statistics and comes from many sources. Taxes are the most important at 90 per cent of the total in 2025-26. The taxes that bring in the most money are income tax and National Insurance contributions, which together are expected to raise around £535 billion. Value added tax (VAT) is the next most important, expected to raise £181 billion. Other big taxes include corporation tax, council tax, business rates, capital gains tax and fuel duty. No other tax is expected to raise more than £20 billion in that year.

The public sector also receives other revenues, including interest earned on its assets such as foreign exchange reserves and student loans, while public corporations generate some income. Over the next five years, we expect total receipts to rise by 26 per cent, faster than the growth in the cash size of the economy. The growth in receipts is mainly driven by personal taxes (reflecting earnings growth, frozen tax thresholds to 2030-31 and the increase to employer NICs announced in the October 2024 Budget) and capital taxes (reflecting rising equity and property prices, and policy measures in the October 2024 Budget). But some tax receipts are expected to fall, for example tobacco duty because people are smoking less.

Spending

The public sector raises money in order to spend it, mostly on the day-to-day costs of providing public services, on capital investment and on cash transfer payments that support the incomes of various individuals and families.

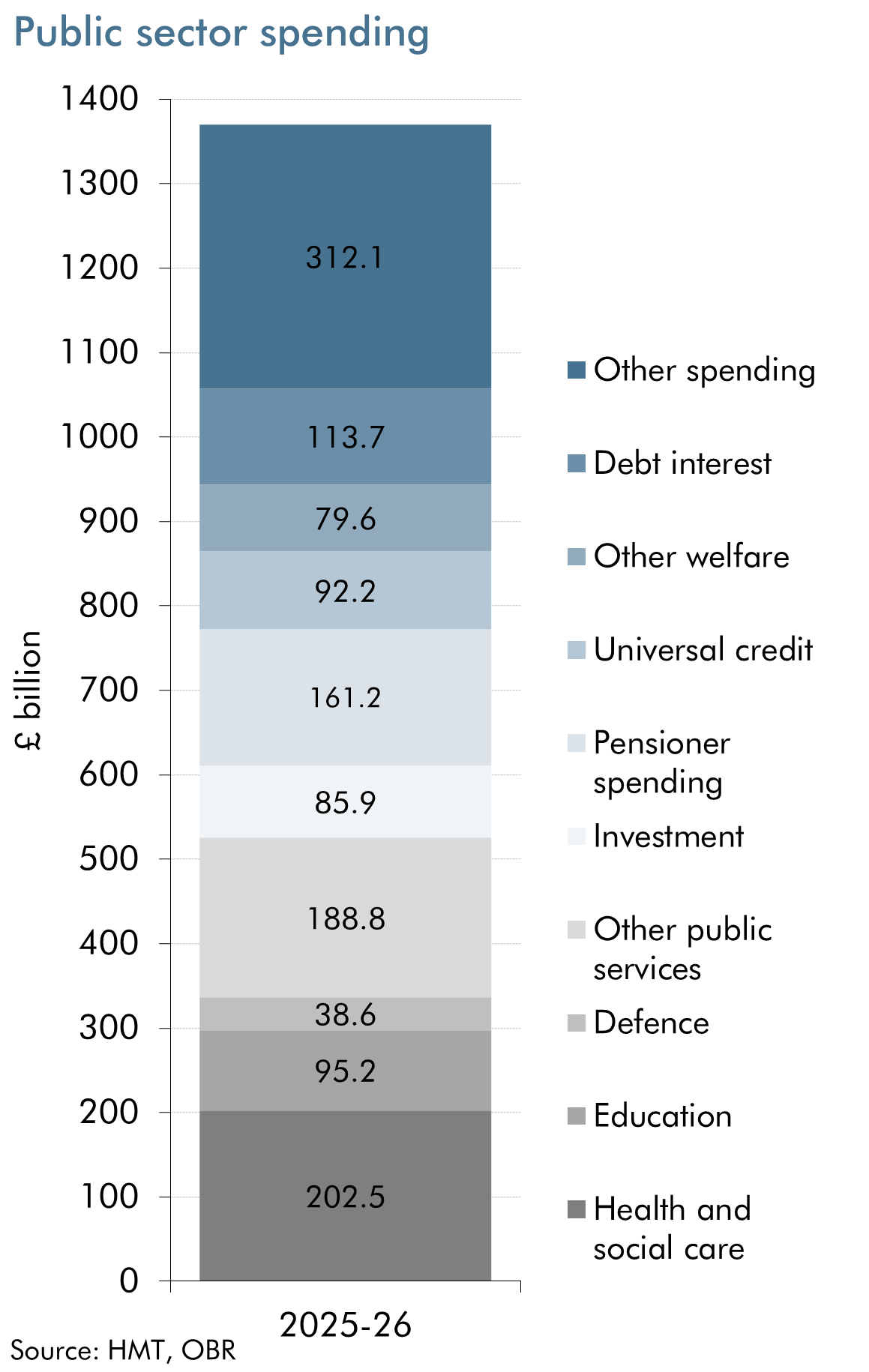

In 2025-26, we expect public spending to amount to £1,368 billion, which is equivalent to around £48,000 per household or 44.8 per cent of national income. This is called ‘total managed expenditure’ and covers many different types of spending. In 2025-26, we expect central government departments to spend £523 billion on the day-to-day ‘current’ running costs of public services, grants and administration. This is 38 per cent of public spending. The biggest items are health (£204 billion), education (£95 billion) and defence (£39 billion). This spending is usually subject to multi-year limits set by the Treasury – known as ‘resource departmental expenditure limits’ or ‘RDEL’.

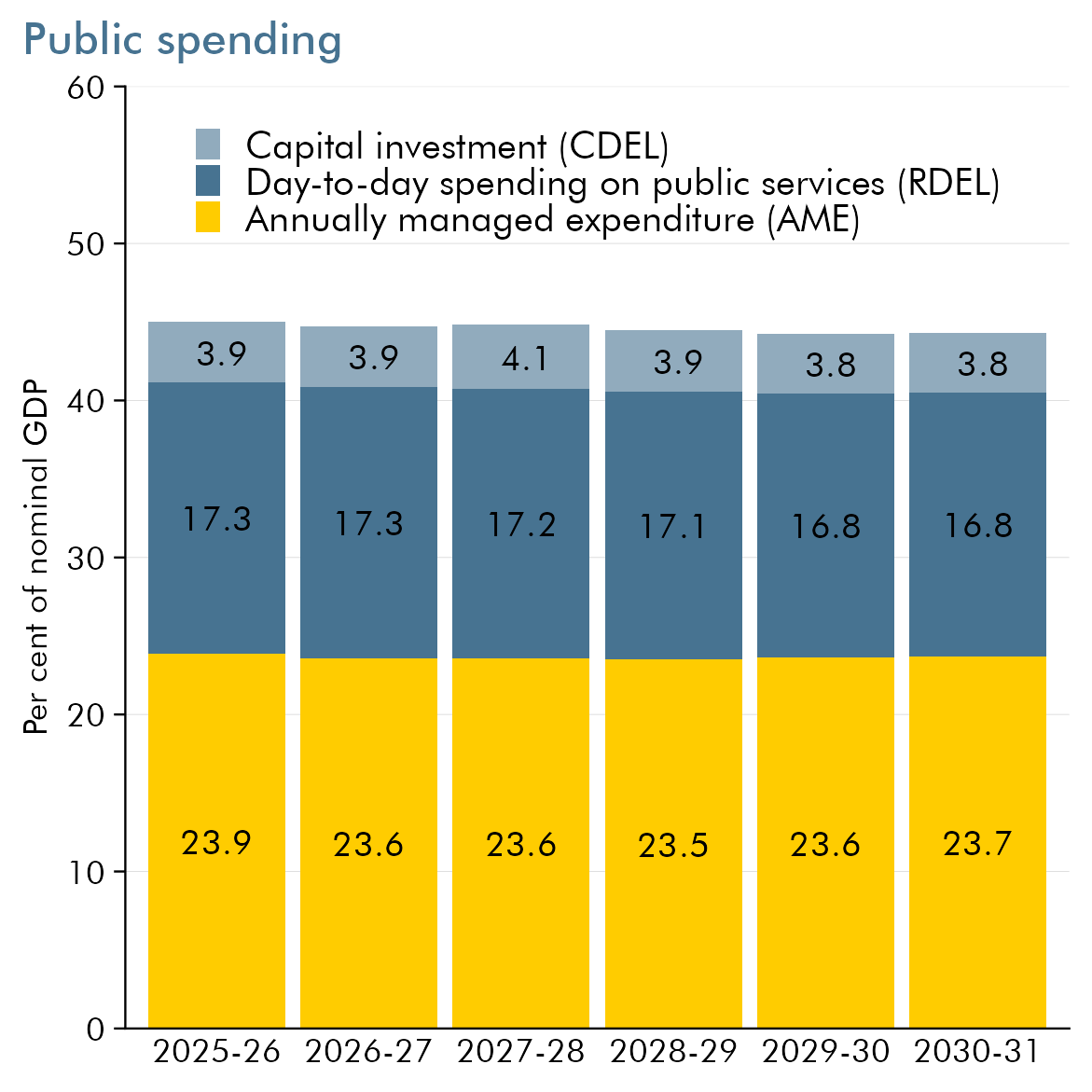

We also expect the public sector to spend £157 billion – 11 per cent of the total – on capital investment such as roads and buildings and on loans to businesses and individuals. Around 75 per cent of this will be spent by government departments, usually subject to multi-year Treasury limits – ‘capital departmental expenditure limits’ or ‘CDEL’. Some of the remainder will be carried out by local authorities (mostly on roads, schools and housing) and public corporations like Transport for London, and 5 per cent of capital investment is on student loans.

The Government set out detailed department-by-department plans for RDEL and CDEL in its 2025 Spending Review. This set RDEL plans for all departments for 2025-26 to 2028-29 and set CDEL plans for all departments for 2025-26 to 2029-30.

The biggest component of ‘annually managed expenditure’ or ‘AME’ is cash transfers through the welfare system, expected to cost £333 billion in 2025-26.

Net interest payments on the national debt are expected to cost £110 billion in 2025-26. This includes the interest government pays to private sector holders of the bonds it issues – known as ‘gilts’ – and also the interest paid by the Bank of England on the money created during the ‘quantitative easing’ of monetary policy since the late 2000s financial crisis and recession. Net debt interest (interest paid minus interest received) is expected to be 9 per cent of non-interest receipts across the forecast period.

Over the next five years, we expect public spending to rise by 18 per cent in cash terms, 1 percentage point slower than the economy, as a result of: a decline in RDEL as a share of GDP; a decline in other spending areas, mainly time-limited spending items that are set to come to an end over the next couple of years, such as the Infected Blood and Post Office compensation schemes; and a rising surplus in unfunded public service pension schemes. These declines more than offset a forecast rise in welfare spending and debt interest.

Deficits and surpluses

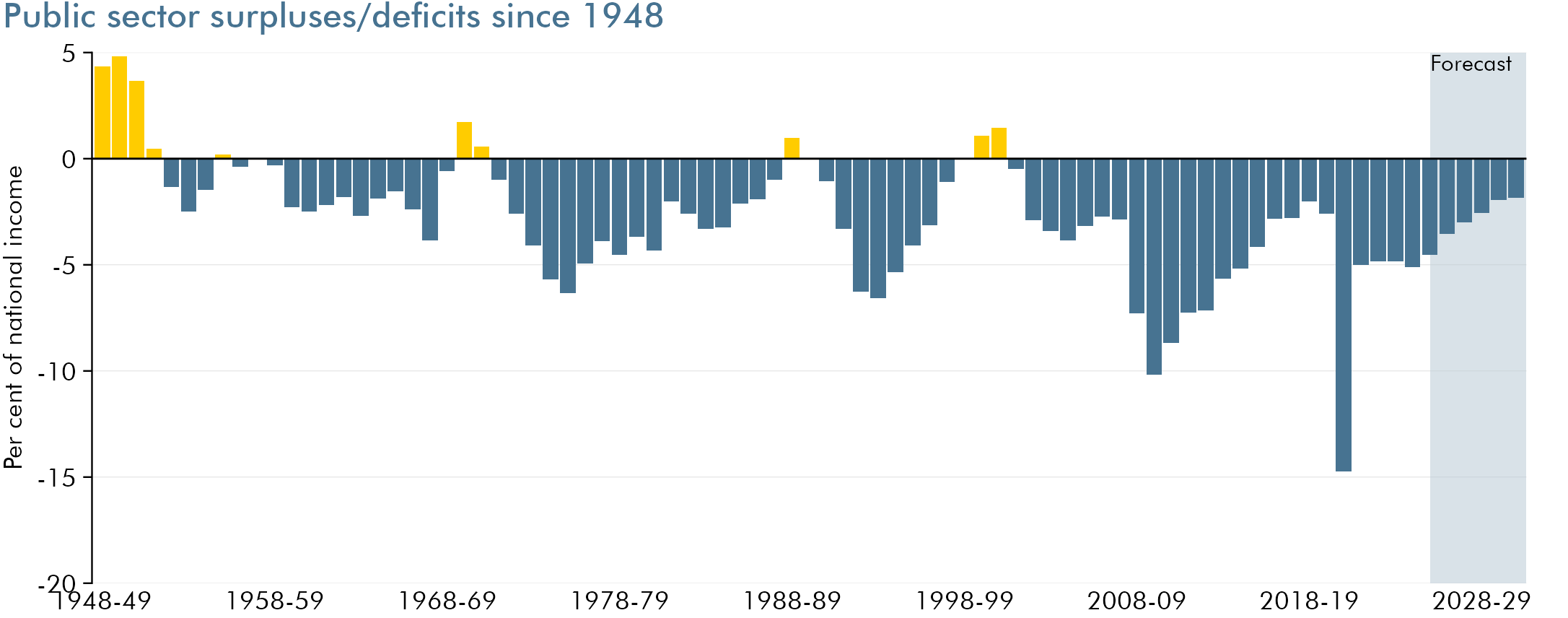

When total spending in a year is higher than total receipts, the Government needs to borrow to cover the difference. This gap is known as the budget deficit or ‘public sector net borrowing’. When receipts are higher than spending, the government runs a surplus.

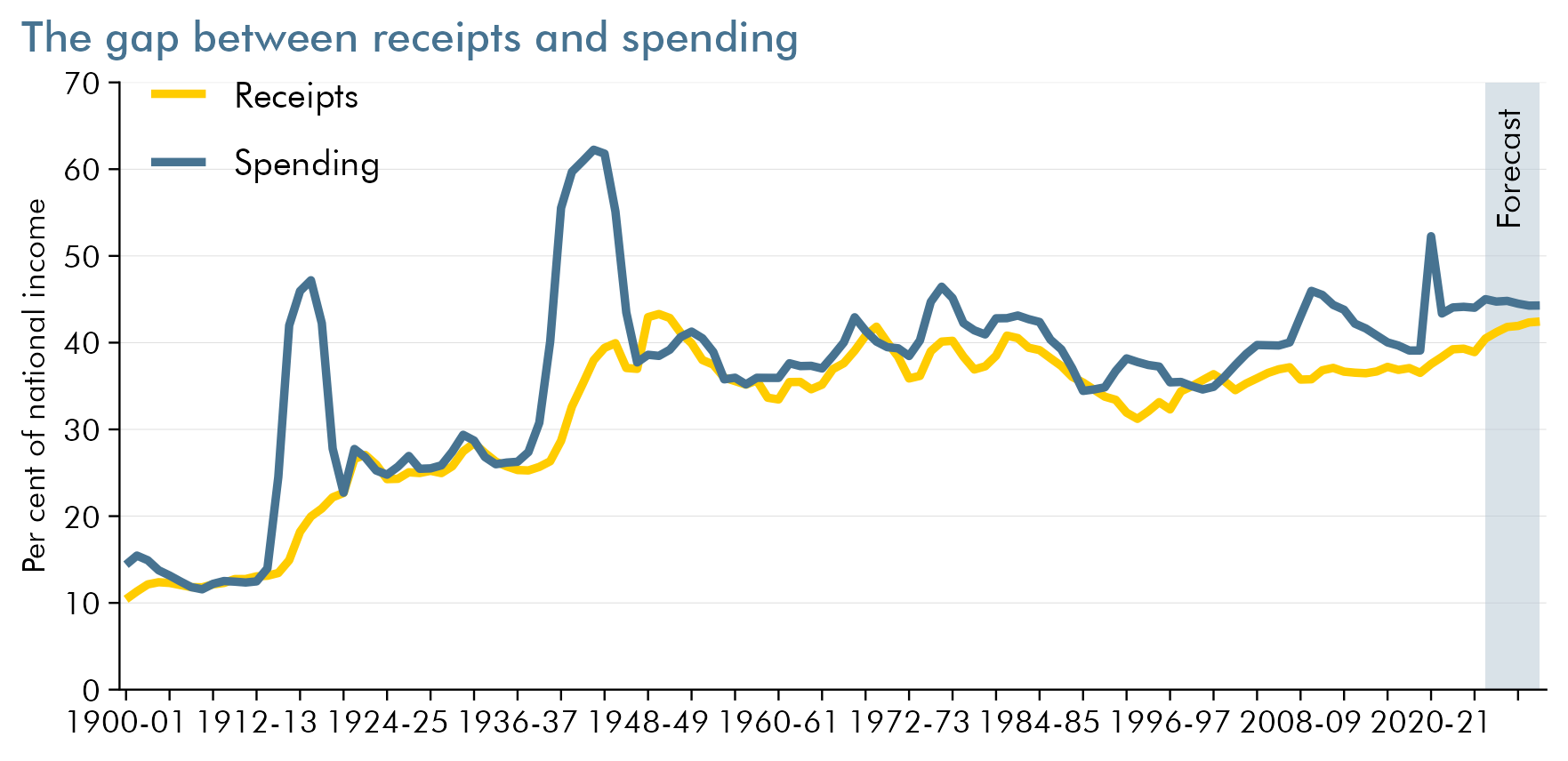

In 2025-26, we expect a deficit of £133 billion or 4.3 per cent of national income. This is a sharp fall from the 2020-21 peak of £311 billion, which was the highest since the second world war. Over the five-year forecast, we expect the growth in receipts to outpace that of spending and the deficit to fall. We expect the deficit to be £59 billion in 2030-31 when receipts are expected to be 42.7 per cent of national income and spending 44.3 per cent.

Swings into deficit have become steadily more pronounced over the post-war period. And budget surpluses have been achieved in only 10 years since 1948 and only three years since 1971-72.

Movements in the budget deficit are in part the result of the ups and downs of the economy. When the economy is strong, the deficit will be lower as taxes receipts increase and welfare spending costs are reduced. The opposite is true when the economy is weak.

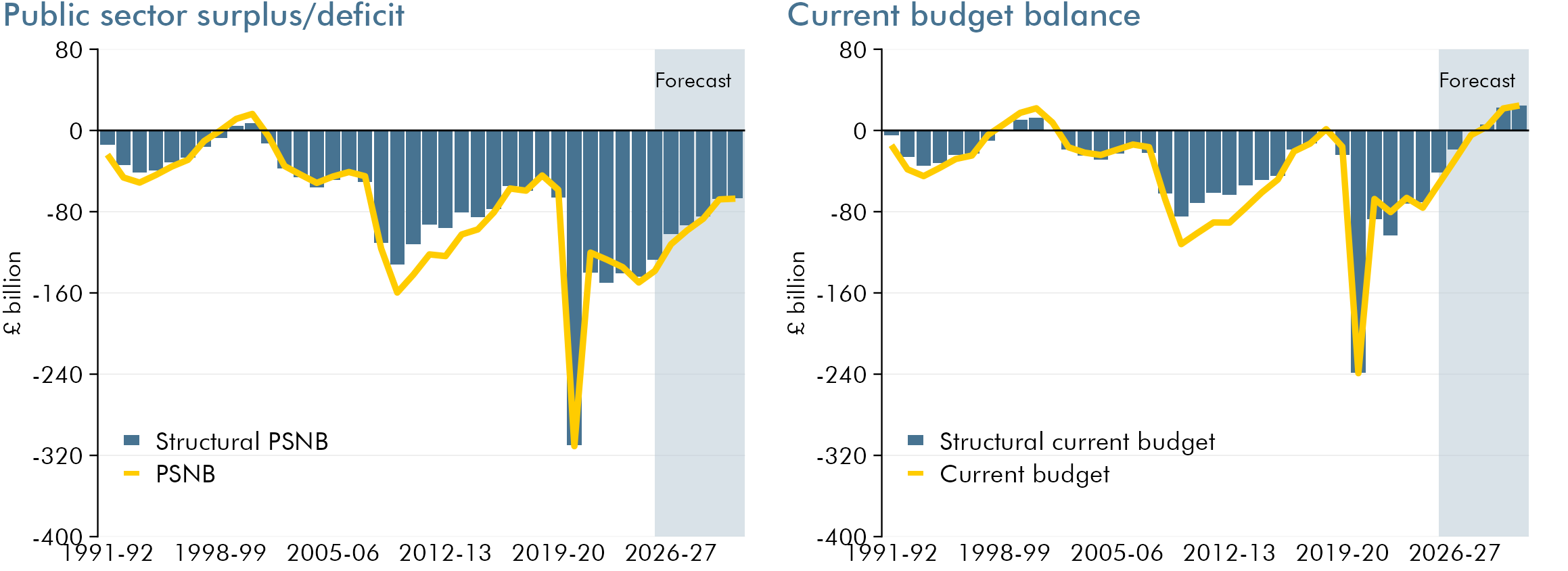

The ‘structural’ budget deficit is an estimate of how large the deficit would be if the economy was operating at a normal, sustainable level of employment and activity. We never know precisely what this ‘normal’ level would be, so these estimates are always uncertain. Using our usual approach, we currently estimate that the economy is initially operating below its sustainable level in the central forecast, we then assume that the ‘output gap’ narrows gradually from 2026 as recent easing in monetary policy feeds through to activity and closes in the middle of 2029. When there is spare capacity in the economy, the structural deficit is smaller than the overall deficit, with a ‘cyclical’ part of the deficit that would disappear automatically as the economy returns to a normal level of activity by the forecast horizon.

The headline deficit is the difference between total receipts and total spending, but people are also interested in the ‘current deficit’ (or surplus), and this is now the focus of the Government’s main fiscal target. The current deficit counts all receipts and all current spending, but excludes spending on net investment. As long as net investment is positive, the current deficit will be smaller than the overall deficit. We expect the current deficit to be £49 billion in 2025-26, and that there will be a current surplus of £30 billion by 2030-31. The target for the current budget to be in balance by 2029-30 was last formally assessed at the November 2025 forecast, where it was met by a margin of £22 billion.

Debt

So far we have been looking at the flows of spending and receipts that take place each year and the deficits and surpluses they result in. But because governments run deficits much more often than they run surpluses, they have built up a significant stock of outstanding debt over time. Occasional crises, such as wars or pandemics, which increase expenditure or reduce receipts often add significantly to public debt.

Normally, if the public sector runs a deficit in a particular year, debt will rise in cash terms. But it can still fall as a share of national income if the cash size of the economy is growing sufficiently strongly. (That said, some government activity adds to its debt without adding to the deficit in any given year, most significantly providing loans to students and businesses where the loans are financial assets for the government, provided they are expected to be repaid in future.)

The most widely watched measure of debt in the UK is ‘public sector net debt’, which subtracts the relatively small amount of assets that the Government could readily turn into cash if required (for example, foreign exchange reserves) from the gross total. We expect public sector net debt to fall gradually from its peak of 96.3 per cent of national income in 2028-29 to 95.1 per cent of national income in 2030-31, which is equivalent to around £3.5 trillion, or £120,000 per household.

One of the Government’s legislated fiscal targets is to make sure that net financial liabilities – a wider measure that includes financial assets like student loans and equity stakes the Government holds in investments – is falling relative to national income by 2029-30. This target was last formally assessed at the November 2025 forecast where it was met by a margin of £24 billion.

International comparisons

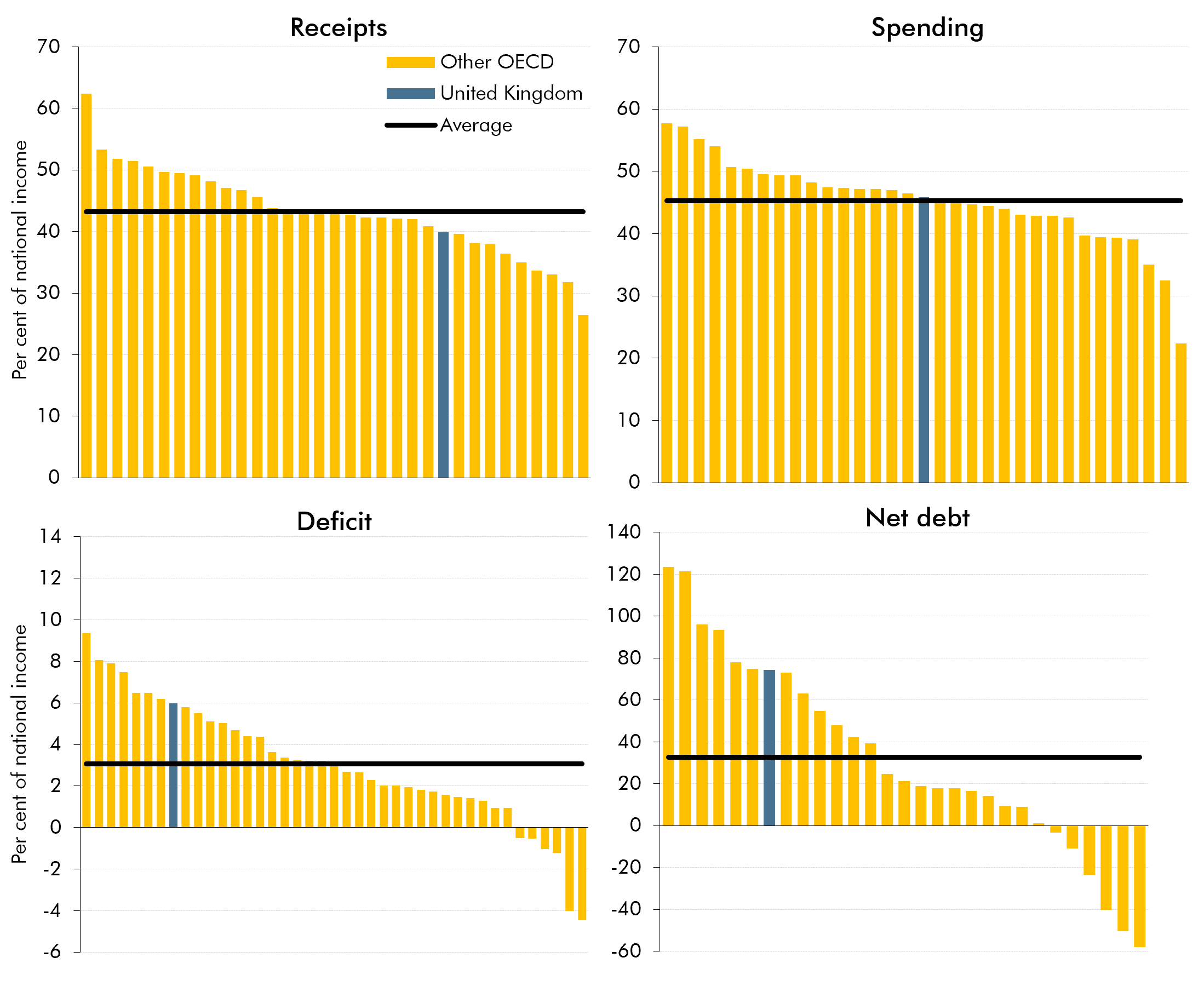

How do the public finances in the UK compare to those in other countries? To answer this question we can look at the data for 42 industrial countries produced by the Organisation for Economic Cooperation and Development (OECD). Unfortunately, the OECD data are not directly comparable with that we have presented so far: for example, the OECD does not cover public corporations, while it defines spending and revenue somewhat differently. The impact of the pandemic, war in Ukraine and subsequent energy price spikes has varied hugely between countries and has led to most countries shifting significantly from their usual fiscal position. The impact on the UK’s public finances in particular was comparatively large.

These caveats aside, in 2025:

- The UK government raised slightly more revenue relative to national income than the US, Japan and Australia, but less than Germany and Scandinavian countries like Denmark and Norway.

- Public spending as a share of national income in the UK is slightly above the average of other industrial countries – the UK spends more than the US and Japan, but much less than Italy or France.

- Spending just above the international average, and raising less in revenue, leaves the UK running a budget deficit that’s above the industrial world average.

- Net debt in the UK is also higher than the average of other industrial countries.