"It is the duty of the Office to examine and report on the sustainability of the public finances"

Economic and fiscal outlook – November 2025

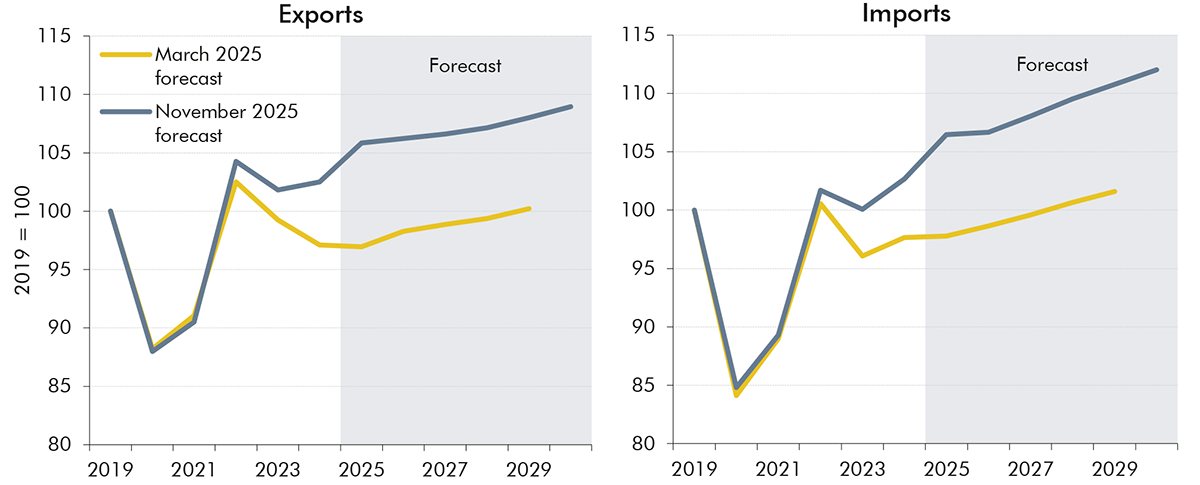

The latest update of our forecasts was published on 26 November 2025 in the November 2025 Economic and fiscal outlook. Read the Executive summary for the key messages of our forecast or the full report on our website.

Chapter 2 sets out our forecasts for the economy over a five-year horizon. We cover our latest forecast changes in light of recent developments and the effect of policies in the Autumn Budget.

In Chapter 3, details the policy measures announced since March 2025, provides an update on selected previous measures, and discusses policy risks and uncertainties.

Chapters 4-6 sets out our forecasts for receipts and public spending over a five-year horizon. We also explain our loans and other financial transactions forecasts. All this, together with new policy decisions, builds the outlook for borrowing and debt.

In Chapter 7, we assess the Government against its fiscal targets and assesses their likelihood of being met on current policy under our central forecast. We consider the uncertainty around our economic and fiscal forecasts and the risks to the Government meeting its targets. We also test the sensitivity of our fiscal forecasts in an alternative economic scenario.

Annex A contains detailed summary tables setting out our economic and fiscal forecasts.

Information or data which has been released alongside the Economic and fiscal outlook or as a result of external requests, since the original publication of the main document.

This Economic and fiscal outlook (EFO) sets out our central forecast and the uncertainties that surround it for the five years to 2030-31, taking account of recent data and government policies announced since our last forecast and up to and including the November 2025 Autumn Budget. The forecasts presented in this document represent our collective view as the three independent members of the OBR’s Budget Responsibility Committee (BRC). We take full responsibility for the judgements that underpin them and for the conclusions we have reached.

As always, we have been greatly supported in our work by the staff of the OBR. We are very grateful for their hard work and expertise. We have also drawn on the work and expertise of officials across government in preparing these forecasts. We are grateful for their engagement and insight.

During the production of this forecast we learned that a respected former colleague, Pavandeep Dhami, sadly passed away. Pav worked at the OBR in its first five years and played a huge part in laying the OBR’s analytical foundations, which we have continued to build upon over the past decade and benefit from today. He will be sadly missed by current and former OBR staff.

The date for this forecast was announced on 3 September, giving two weeks more than the ten weeks’ notice required by the Memorandum of understanding between the Office for Budget Responsibility, HM Treasury, the Department for Work and Pensions and HM Revenue and Customs (MoU).

We published the timetable of the key stages of the forecast on 17 September, once it had been agreed by signatories of the MoU. Given the unusual volume of speculation on the subject prior to the publication of this EFO, the Chair has taken the unusual step of writing to the Chair of the Commons Treasury Committee to set out the facts concerning the evolution of our forecast over the course of the past four months. A copy of this letter is available on our website.

The timetable for the production of this forecast was as follows:

We undertook our regular summer review of the supply side of the economy, which enables us to focus on the key drivers of potential output, a foundation stone of our economy forecast, in slower time and outside of the full forecast round. It also allows us to make judgements that feed into the first round of the forecast process for the Autumn Budget and thereby inform policy development at the earliest opportunity. We informed the Treasury of the outcome of the review on 7 August.

On the fiscal side, we initiated a process of reviewing fiscal forecast models and judgements as part of a fiscal baseline review over the summer, prior to the main forecast process. This process, along with the supply side review, was designed to reduce the volatility of our forecast between rounds to support a smoother policy development process within government. Partly as a result, our pre-measures forecast displayed less variation from round to round than has previously been the case.

Following the conclusion of the supply-side review, fiscal baseline review, and confirmation of the timetable, OBR staff prepared an initial economy forecast, drawing on data released since our previous forecast in March 2025 and incorporating our preliminary judgements on the outlook for the economy. This economy forecast was sent to the Treasury on 17 September.

Using the economic determinants from this forecast (such as the components of nominal income and spending, unemployment, inflation, and interest rates), we commissioned updated forecasts from the relevant government departments for the various tax and spending items that in aggregate determine the position of the public finances. We discussed these in detail with the officials producing them, which allowed us to investigate proposed changes in forecasting methodology and to assess the significance of recent tax and spending outturn data. In many cases the BRC requested changes to methodology and/or the interpretation of recent data. This first fiscal forecast was finalised on 2 October, and we sent a note that described the main elements of it to the Chancellor the following day.

As the process continued, we identified further key judgements that we would need to make for our economy forecast. Where we thought it would be helpful, we commissioned analysis from the relevant teams in the Treasury. We then produced a second pre-measures economy forecast, which incorporated the latest data, and the economic implications of our first fiscal forecast.

This second economy forecast provided the basis for the next round of fiscal forecasts. Discussions with HM Revenue and Customs (HMRC), the Department for Work and Pensions (DWP) and other departments, gave us the opportunity to follow up our requests for further analysis, methodological changes, and alternative judgements from the previous round. We finalised our second fiscal forecast on 17 October and sent a summary of the forecast to the Chancellor on 20 October.

We then produced a third and final pre-measures economy forecast, in which we took on the latest data and incorporated judgements embodied in our fiscal forecast. This final pre-measures economy forecast was based on financial and energy market data averaged over the 10 working days to 10 October. It was sent to the Treasury and other government departments that produce tax and spending forecasts on 23 October.

The agreed timetable required us to close the pre-measures economy and fiscal forecasts earlier than we have previously, to increase the time at the end of the process for the Government to finalise the policy package on the basis of a stable forecast. Given the time between the closure of the pre-measures economy forecast and the publication of our EFO, we decided prior to the start of the forecast process in the summer to take a later window for Bank Rate and gilt yields for the final pre-measures fiscal forecast, which were averaged over the 10 working days to 21 October. This results in very minor discrepancies between the economy and fiscal forecast which we judge to be immaterial, and outweighed by having a more up-to-date set of interest rate assumptions in our fiscal forecast. In practice, the difference between interest rate assumptions used in the economy and fiscal forecasts is very small, with interest rates in the fiscal forecast lower by an average of 0.1 percentage points.

The final pre-measures fiscal forecast, incorporating these later interest rate assumptions, was finalised on 30 October, and sent to the Chancellor the following day on 31 October. No further adjustments were made to our economy or fiscal forecasts after this, other than to take account of the impact of policy measures provided by the Treasury.

In parallel to the production of the forecast, we scrutinised the costing of individual tax and spending measures announced since our March 2025 forecast. As usual, OBR staff and the BRC requested further information and/or changes to almost all the draft costings prepared by HMRC, DWP and other departments. We also undertook a process of engagement and analysis to assess the policy measures included in the Budget that we deemed could have specific effects on our economy forecast. This involved several rounds of engagement with the Treasury and other government departments as both the specification of policies, and our assessment of their impact, were refined.

We made an initial assessment of the economic and fiscal effects of the emerging policy package that was provided by the Treasury on 4 November. We incorporated this package into an initial post-measures forecast, to provide an early view on the effect of policy measures on the economy and public finances, which we sent to the Chancellor on 10 November. This forecast round was produced using our internal ready-reckoner models (rather than being sent to departmental forecasters).

In line with the agreed timetable, on 12 November the Treasury provided the final package of measures that would cause movements in our economy forecast. We sent the resulting final economy forecast to the Treasury on 17 November and a near-final fiscal forecast on 18 November. Final policy decisions, that would only affect the fiscal forecast, were returned by the Treasury on 20 November, a day later than anticipated in the agreed timetable, and our forecast was then finalised and sent to the Treasury on 21 November.

The Treasury made a written request, as provided for in the MoU between us, that we provide the Chancellor and an agreed list of her special advisers and officials with a near-final draft of the EFO on 21 November. This allowed the Treasury to prepare the Chancellor’s statement and accompanying documents. We also provided pre-release access to the full and final EFO on 24 November.

Alongside producing the forecast, we prepared two supplementary briefing papers that have been published at the same time as this EFO: Briefing paper No.9: Forecasting productivity, which summarises the analysis and conclusions of our supply-side review; and Briefing paper No.10: Accounting for the supply-side effects of policy, which provides the conclusions of our review of the criteria for scoring the supply-side effects of policies that was recommended by our recent external review. These papers were shared with the Treasury on 11 November and 20 October respectively.

The agreed forecast timetable was largely adhered to, with the exception of the finalisation of the policy package. Small changes were made to the parameters of three policy measures following the costings certification deadline, meaning that, although we have no concerns about the methodologies used, we have not been able to certify these costings but have used the Government’s estimates of their fiscal impact and will return to them at our next forecast. In addition, one policy measure with direct effects on our economy forecast was altered after it had been finalised. Had we been able to incorporate this, it would have only made a small difference to our final economy forecast.

During the forecasting period, the BRC held dozens of scrutiny and challenge meetings with officials from other departments, in addition to numerous further meetings at staff level and with external stakeholders. We have been provided with all the information and analysis that we requested and have come under no pressure from Ministers, advisers, or officials to change any of our conclusions. The BRC met with the Chancellor on two occasions to discuss the forecast over the course of its production (on 10 October and 30 October). A full log of our substantive contact with Ministers, their offices and special advisers can be found on our website. This includes the list of special advisers and officials who received the near-final draft of the EFO on 21 November.

We would be pleased to receive feedback on any aspect of the content or presentation of our analysis. This can be sent to [email protected].

The Budget Responsibility Committee Richard Hughes, Professor David Miles CBE and Tom Josephs

Chapter 1: Executive summary

Overview

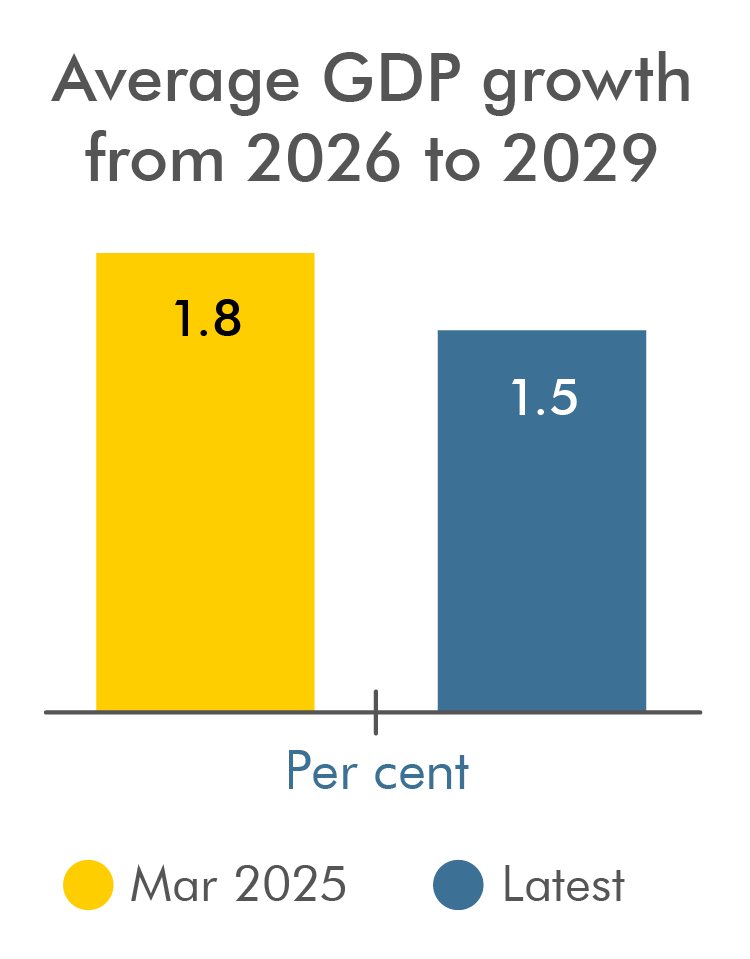

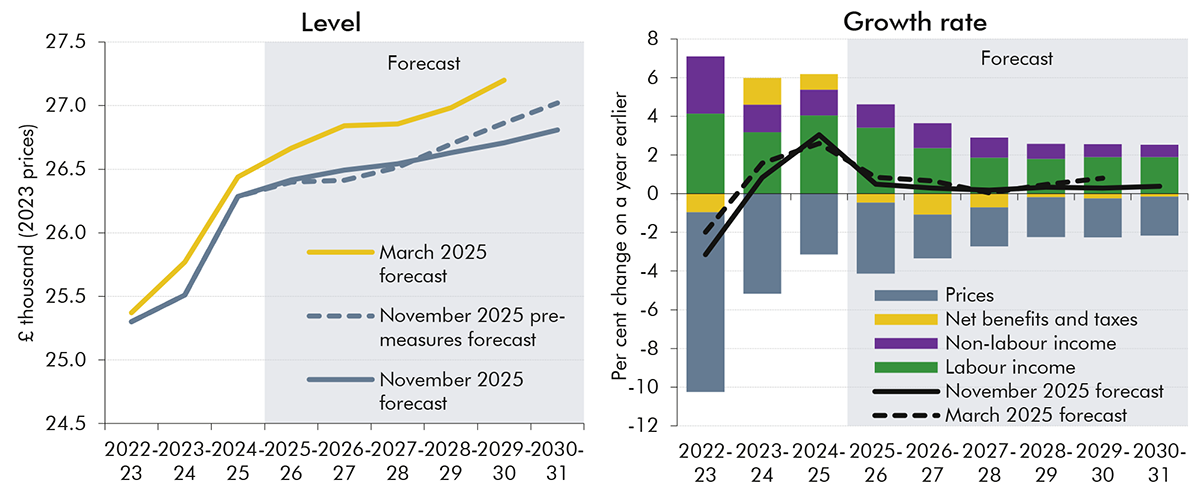

1.1 Real GDP is forecast to grow by 1.5 per cent on average over the forecast, 0.3 percentage points slower than we projected in March, due to lower underlying productivity growth. But cumulative real wage growth and inflation over the next two years are forecast to be around ¾ and ½ a percentage point higher than in March respectively. This means that total growth in nominal GDP over the forecast is only around 1 percentage point lower than in March and is more tax rich, thanks to a larger share accruing to labour income and consumption. This, combined with frozen personal tax thresholds, boosts pre-measures tax receipts by amounts rising to £16 billion by 2029-30 relative to our March forecast. But pre-measures spending is also higher in every year and by £22 billion in 2029-30 due to higher spending by local authorities and on welfare and debt interest. The net result is a modest medium-term deterioration in the pre-measures fiscal outlook, with borrowing £17 billion higher this year but only £6 billion higher in 2029-30 compared to our March forecast.

1.2 Against this backdrop, Budget policies increase spending in every year and by £11 billion in 2029-30, primarily to pay for the summer reversals to welfare cuts and lift the two-child limit in universal credit. The Budget also raises taxes by amounts rising to £26 billion in 2029-30, through freezing personal tax thresholds and a host of smaller measures, and brings the tax take to an all-time high of 38 per cent of GDP in 2030-31. The net impact of Budget spending and tax policies increases borrowing by £5 billion on average over the next three years but then reduces it by £13 billion on average in the following two.

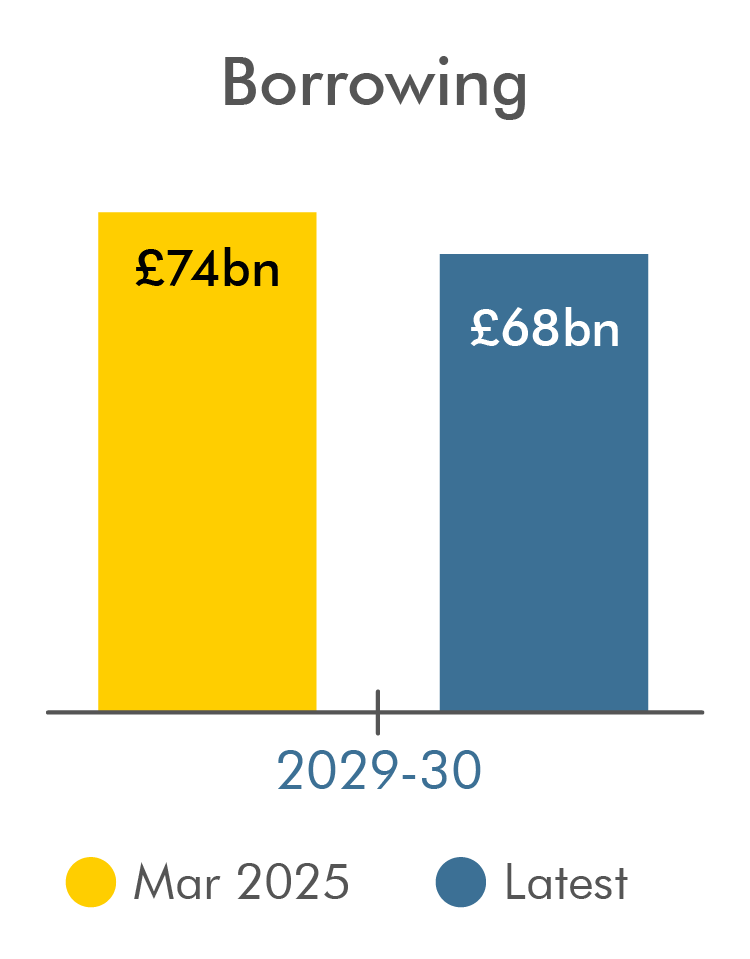

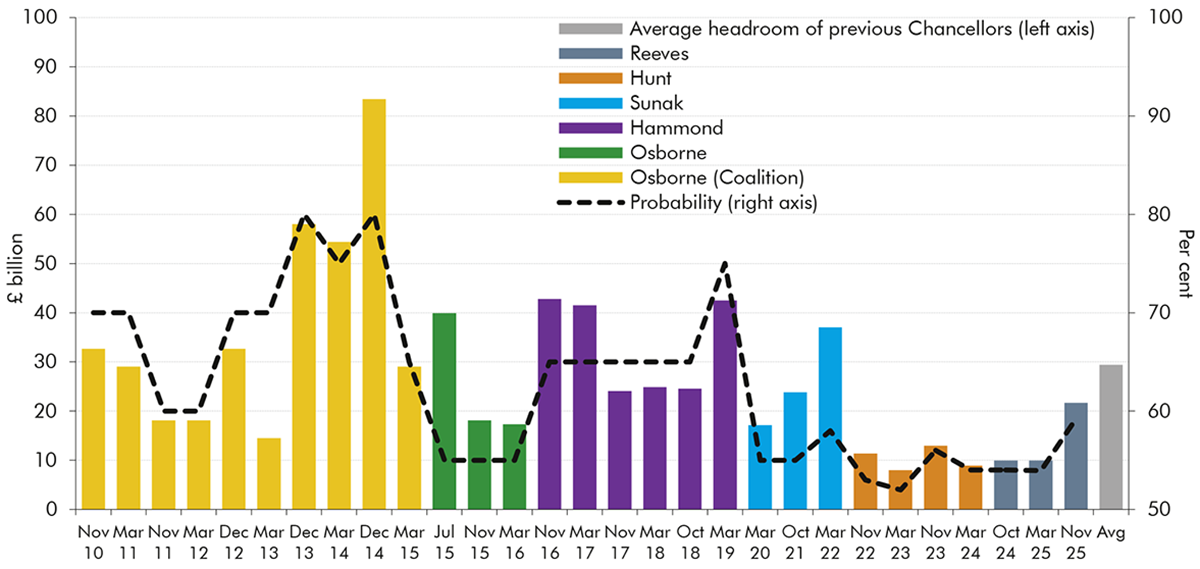

1.3 Taking forecast and policy changes together, borrowing is projected to fall from 4.5 per cent of GDP in 2025-26 to 1.9 per cent of GDP in 2030-31. Debt rises as a share of GDP from 95 per cent of GDP this year and ends the decade at 96 per cent of GDP, which is 2 percentage points higher than projected in March and twice the debt level of the average advanced economy. The current balance target is met in 2029-30 with a margin that fell from £10 billion in the March forecast, to £4 billion in the pre-measures forecast, but is then boosted to £22 billion by Budget policies. This is close to the £21 billion average absolute revision in the fourth year of our pre-measures forecast between fiscal events, and around three-quarters of the £29 billion average margin set aside by previous Chancellors. But it is only around two-fifths of the median £54 billion difference between our forecast for borrowing and final outturn four years hence. It therefore remains a small margin compared to the uncertainties around our economy forecast, including the outlook for productivity, interest rates, equity prices, and earnings growth. It is also small by comparison to the wider risks around our fiscal forecast, which include risks from the uncertain yield from an array of complex tax changes, and pressures on welfare, health, education, asylum, defence, and local authority budgets.

Economic outlook

1.4 We now forecast real GDP growth of 1.5 per cent in 2025, 0.5 percentage points faster than in our March Economic and fiscal outlook (EFO). This is because output growth was revised up in the second half of 2024 and growth was stronger than expected in the first quarter of 2025, at 0.7 per cent. The latter was partly due to the temporary frontloading of property transactions and exports, as households sought to avoid stamp duty threshold changes and businesses tried to get ahead of tariff increases, both of which came in from April. Growth then fell to 0.3 per cent in the second quarter, as these temporary factors unwound, and to 0.1 per cent in the third quarter, when the Jaguar Land Rover shutdown temporarily weighed on growth – both below our March forecast. We expect quarterly growth to pick up only gradually in the near term as geopolitical uncertainty persists and domestic business and consumer confidence remains subdued, including in anticipation of further tax rises.

1.5 We have reduced our central forecast for the underlying rate of productivity growth in the medium term to 1.0 per cent, 0.3 percentage points slower than in our March forecast. The UK’s productivity performance has undershot our forecasts, despite several substantial downgrades since 2010, as a significant rebound from recent negative shocks has not materialised. The further reduction in this forecast is due to a lower forecast for underlying total factor productivity (TFP) growth, which we now forecast at 0.8 per cent rather than 1.1 per cent in the medium term. This decision is not a reflection of any particular government policies. Rather, it is based on our latest assessment of the UK’s productivity performance in historical and international context; what the latest output and labour force data tell us about the impact of shocks and underlying productivity of the economy; and how developments in global trade policy, the sectoral composition of output, the emergence of new technologies like artificial intelligence, and other structural trends are likely to affect the productive potential of the UK economy in the future.[1]

1.6 With estimated medium-term growth in labour supply and capital deepening unchanged at 0.5 and 0.2 per cent respectively, medium-term potential output growth has been revised down by 0.3 percentage points to 1.5 per cent. Real GDP growth is expected to be steady at around 1.5 per cent over the forecast as TFP growth rises from 0.5 per cent this year to its new medium-term trend rate of 0.8 per cent in 2030, offsetting a continued slowdown in labour supply growth. The downward revision to our real GDP growth forecast – which reduces cumulative growth over the forecast by 1.3 percentage points – is offset by upward revisions to historical data and stronger-than-expected growth at the start of 2025, which raise the starting level of GDP by 1.1 per cent relative to March. This means that the level of GDP is only 0.1 per cent lower than March in 2029. We estimate that Budget policies temporarily boost demand by 0.1 per cent next year but have no significant impact on output by 2030.[2]

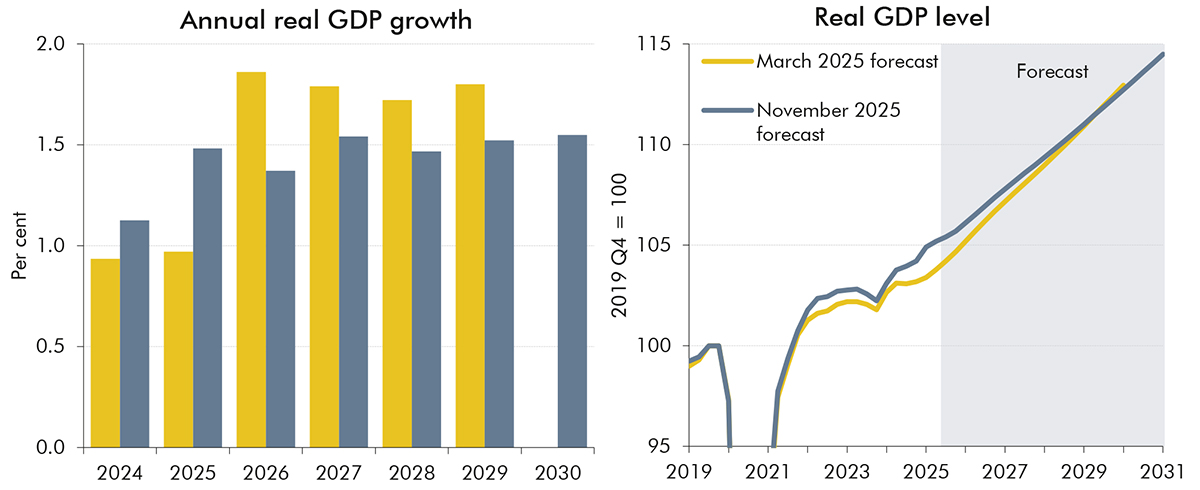

Chart 1.1: Real GDP growth and level

Source: ONS, OBR

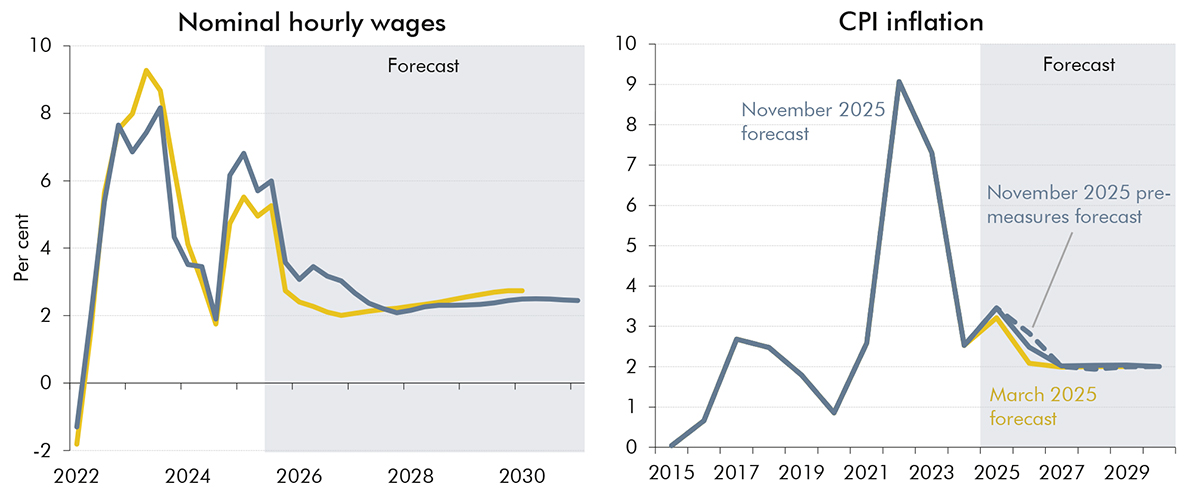

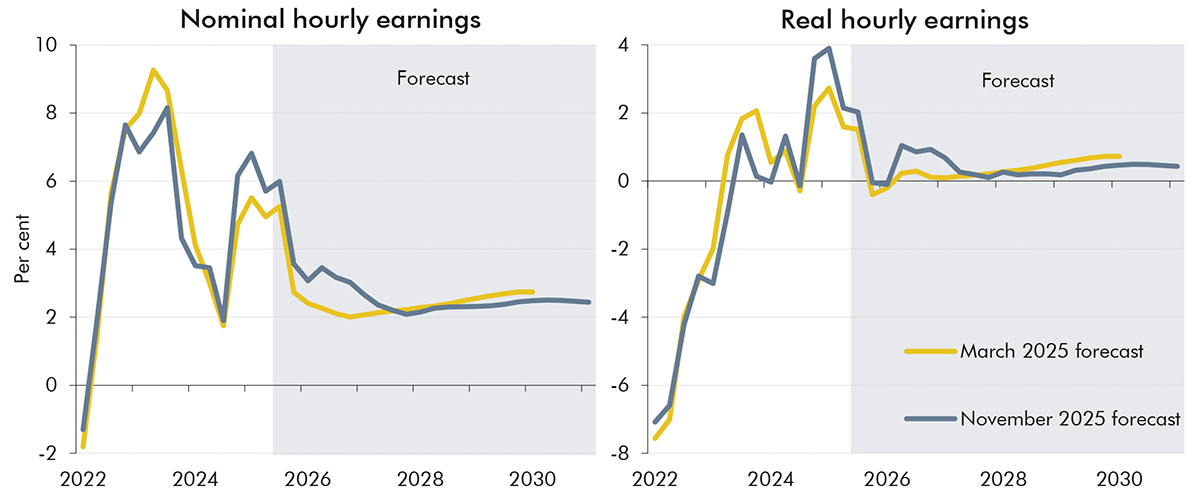

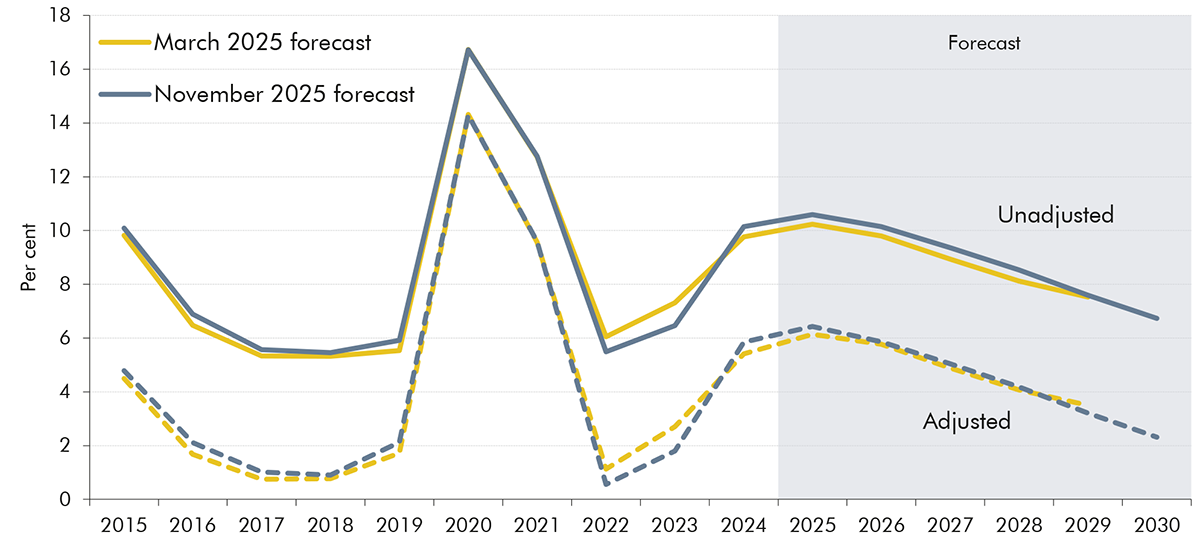

1.7 The downward revision to productivity is not the only material change to our economy forecast since March – we have also revised up our near-term forecast for earnings growth and inflation. Relative to our March forecast, cumulative real wage growth over the next two years is just under ¾ percentage points higher and CPI inflation just over ½ per cent higher as surveys of wage settlement expectations have held up significantly more than we expected, and there is more momentum in domestically generated inflation than we anticipated. This means that, having risen by around 5 per cent in 2024, nominal weekly earnings are estimated to grow at close to the same rate in 2025 before falling to around 3½ per cent in 2026, with growth around 1 percentage point higher than the March forecast in both years. Nominal weekly earnings growth falls back further to an average of around 2¼ per cent a year from 2027 as labour market conditions loosen, inflation drops back, average weekly hours worked fall slightly, and companies rebuild margins and pass on more of the recent rise in employer National Insurance contributions (NICs) to real wages.

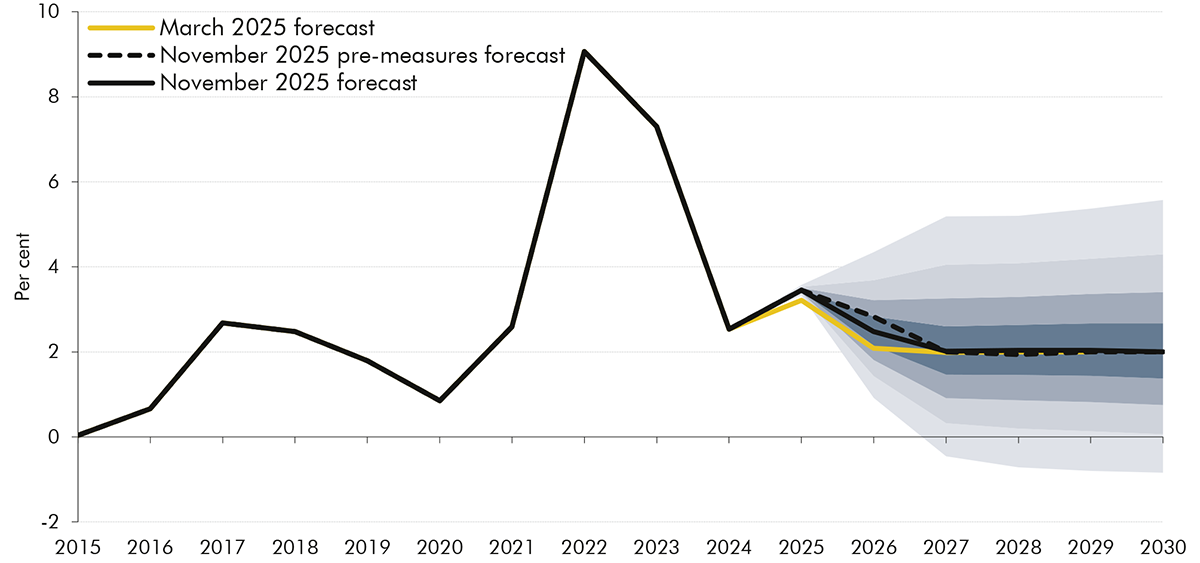

1.8 Greater domestically generated inflation, alongside higher food prices, mean we also expect inflation to stay higher for longer than in March. In this forecast, higher food and services prices push CPI inflation up to 3.5 per cent in 2025 and 2.5 per cent in 2026, respectively 0.2 and 0.4 percentage points higher than the March forecast. These upward pressures on prices are only partly offset by a 0.3 percentage point reduction in inflation in 2026 from Budget policy measures, primarily those that reduce household energy bills. CPI inflation returns to the Bank’s 2 per cent target in 2027, a year later than in our March forecast. The increase in domestically generated inflation also means that cumulative growth in the GDP deflator is 0.5 percentage points higher than in our March forecast.

Chart 1.2: Hourly wage growth and CPI inflation

Source: ONS, OBR

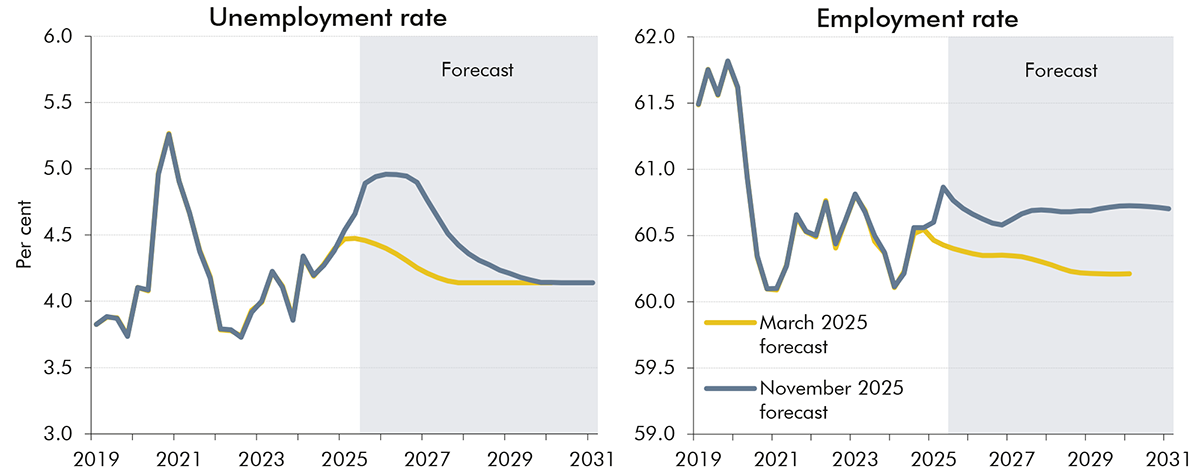

1.9 The unemployment rate has been on a gradual upward trend since a post-pandemic trough of 3.8 per cent in 2022, and we expect it to remain close to its current rate of around 5 per cent until 2027. It then falls back to its estimated equilibrium rate of around 4 per cent over the forecast. The employment rate is expected to be broadly flat at around 61 per cent over the forecast, as a cyclical decline in the unemployment rate is offset by a structural fall in the participation rate from an ageing population and rising sickness-related inactivity. Growth in real household disposable income per person is projected to fall from 3 per cent in 2024-25 to around ¼ per cent a year over the forecast, slightly below our March forecast and well below the last decade’s average growth of 1 per cent a year. Weaker medium-term real wage growth and rising taxes explain the slower growth. Real GDP per person grows by an average of 1.1 per cent a year over the forecast, 0.3 percentage points slower than in March due to weaker productivity growth.

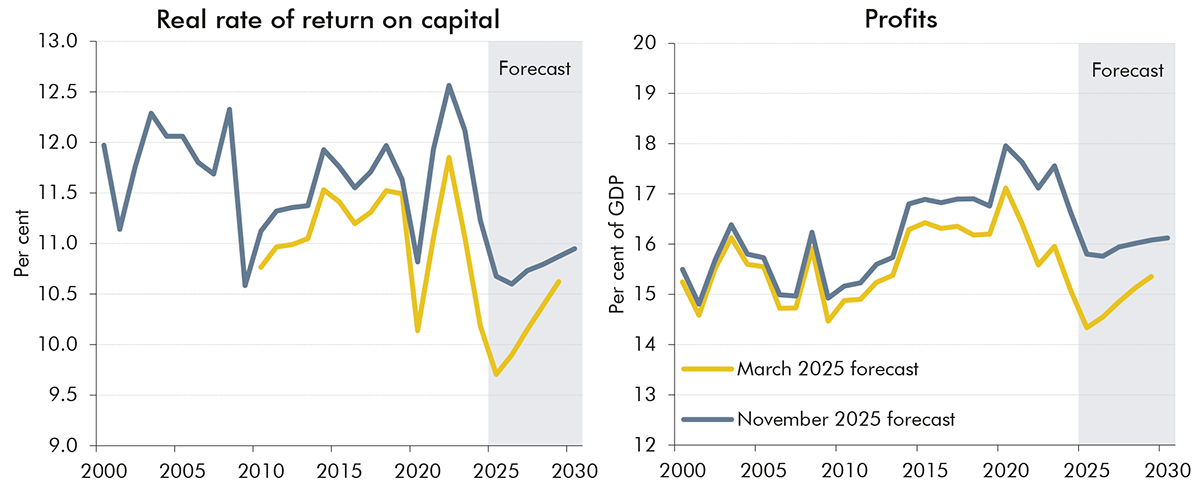

1.10 Business profits are projected to fall in 2025 before picking up across the forecast, but by less than expected in March. We forecast that the real rate of return on capital will fall from around 12½ per cent in 2022 to a low of around 10¾ per cent in 2026 as real wage growth and settlement expectations hold up relative to subdued productivity growth. In the medium term, we forecast that firms are likely to try to rebuild their rate of return by keeping real wage growth below productivity growth, so we expect the rate of return to recover to around 11 per cent. We also project growth in business investment to be weaker over the forecast compared to March due to continued weakness in business sentiment, lower profit growth, and increases in long-term interest rates which have pushed up the cost of capital.

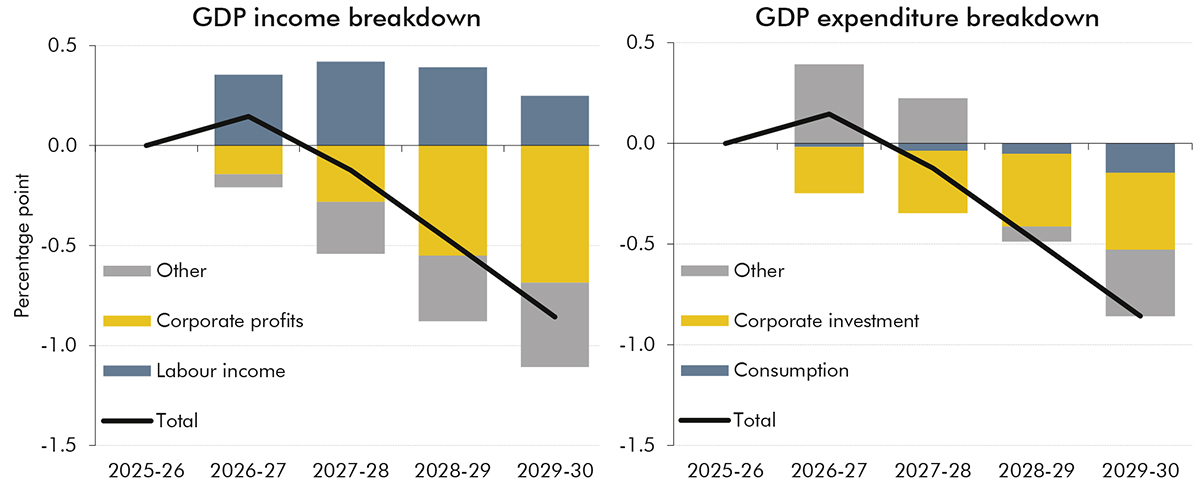

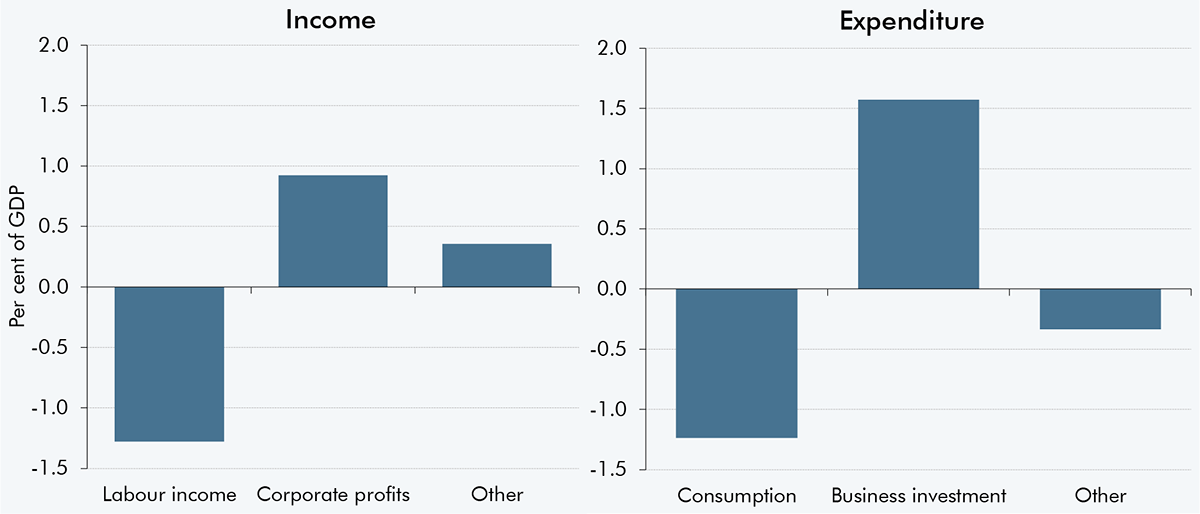

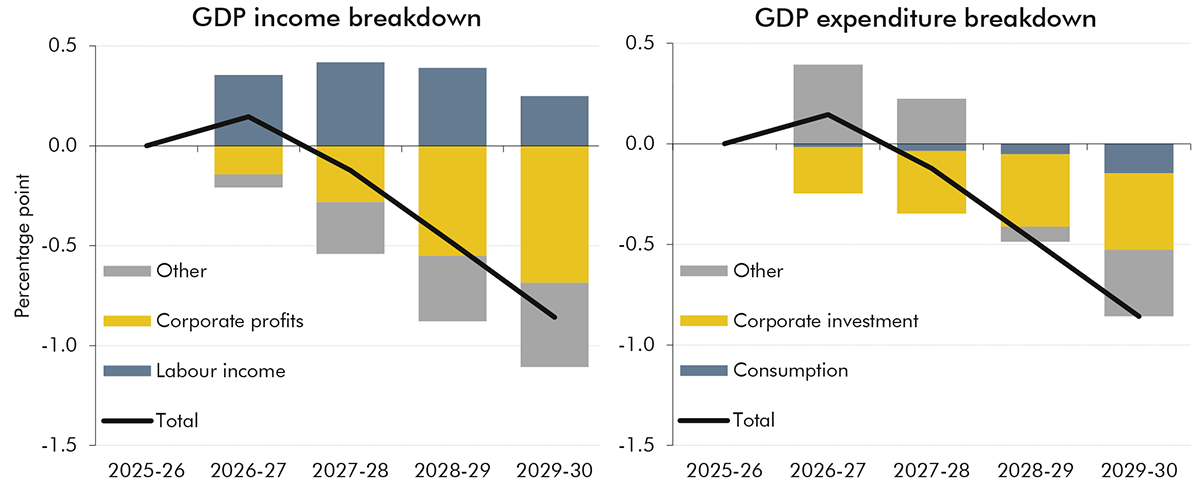

1.11 The overall impact of these changes is that growth in the nominal economy has not been downgraded by as much as productivity, and the composition of nominal GDP growth is more tax rich than in March. Cumulative nominal GDP growth, a key driver of tax revenues, is only 0.9 percentage points lower than in March over the forecast, because the downward revision to real GDP growth is partly offset by the upward revision to inflation. Moreover, cumulative growth in corporate profits has been revised down by significantly more than nominal GDP – by around 6 percentage points – while cumulative growth in labour income has been revised up by 0.9 percentage points. These changes boost tax receipts, as labour income has an effective tax rate of around 40 per cent, whereas corporate profits have an effective tax rate of around 17 per cent. Consistent with these revisions to income, we also now expect a more tax-rich composition of expenditure growth over the forecast. Nominal consumption growth (which has an effective tax rate of 10 per cent) has been revised down by less than nominal GDP, while corporate investment growth (which has a negative short-term effective tax rate, due to investment allowances) has been revised down significantly more than nominal GDP growth.

Chart 1.3: Cumulative growth in nominal GDP: changes since March

Source: ONS, OBR

Fiscal outlook

1.12 The economy changes described above boost overall tax receipts relative to our March forecast by £16 billion in 2029-30, before accounting for Budget policies. In isolation, the reduction in productivity growth could have lowered revenues by around £16 billion in 2029-30. However, the boost to receipts from higher inflation and changes to the composition of nominal GDP growth, set out in the previous paragraph, more than offset this. As a result, income tax and NICs receipts are £11 billion higher than in March by 2029-30, due to higher nominal earnings growth coupled with frozen personal tax thresholds. In addition, VAT receipts are £4 billion higher than March in 2029-30 due to higher pre-measures consumption growth. And corporation tax receipts are little changed relative to our March forecast thanks, in part, to lower investment growth.

1.13 The impact on public sector net borrowing of the higher pre-measures receipts forecast is more than offset by a £22 billion increase in the pre-measures spending forecast by 2029-30, relative to March. Before accounting for policy, higher forecast inflation and earnings and an increase in disability caseloads increase projected spending on welfare by £8 billion by 2029-30. Higher inflation and interest rates increase debt interest spending by £4 billion by 2029-30. The pre-measures forecast also includes a significant increase to local authority spending, which increases borrowing by £8 billion in 2029-30, reflecting substantial recent upward revisions to outturn and rapidly growing spending on special educational needs and disabilities (SEND). Departmental spending has also been revised up by an average of around £6 billion per year across the Spending Review period, before accounting for policy, to reflect risks and pressures, most notably on the NHS, asylum, and the cost of digital ID cards, for which no specific funding has been identified.

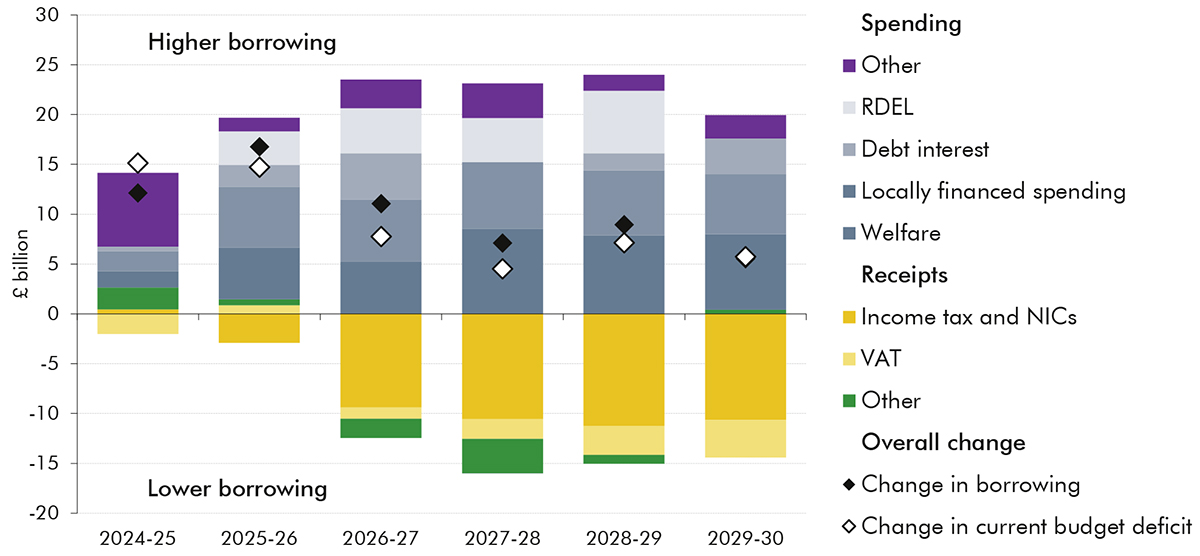

1.14 Before accounting for Budget policies, these forecast changes left borrowing £17 billion higher this year and £6 billion higher in 2029-30. Higher spending pressures, in particular from local authorities and on welfare, drive the substantial deterioration in borrowing this year. This is then partly offset by higher forecast personal tax and VAT receipts from next year onwards due to stronger nominal earnings growth and inflation. The pre-measures deterioration in the current budget matches that of borrowing, leaving a current surplus of around £4 billion in 2029-30, which is £6 billion lower than the £10 billion surplus forecast at the Spring Statement. This change in borrowing since March is small compared to the £21 billion average absolute revision in the fourth year of our pre-measures forecast.

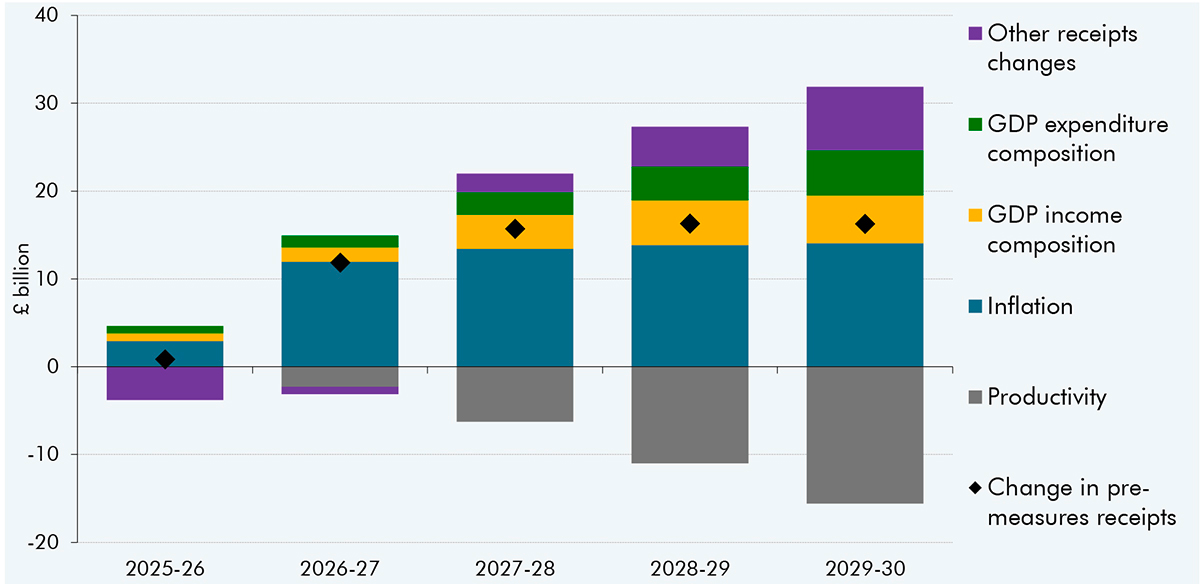

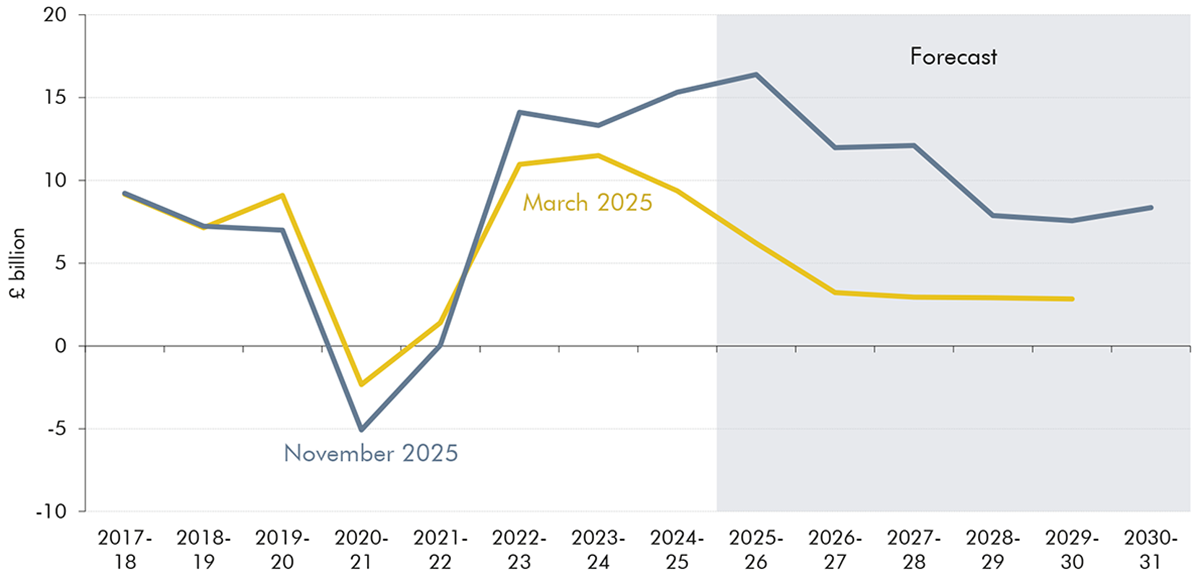

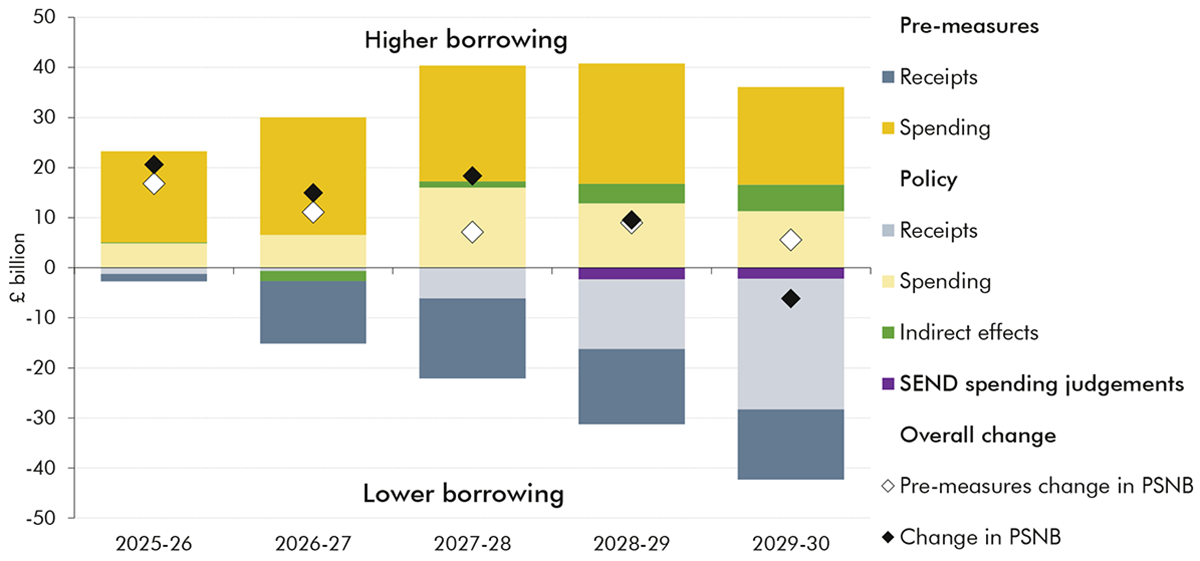

Chart 1.4: Pre-measures change in borrowing since March

Note: This chart excludes the fiscally neutral reclassification of Scottish block grants and Scottish fire and police pensions. It also excludes the effects of changes in our pre-measures forecasts for most environmental levies, VAT refunds, depreciation, council tax, community infrastructure levy and the new extended producer responsibility. Each of these change both receipts and spending by equal amounts and therefore does not change borrowing.

Source: ONS, OBR

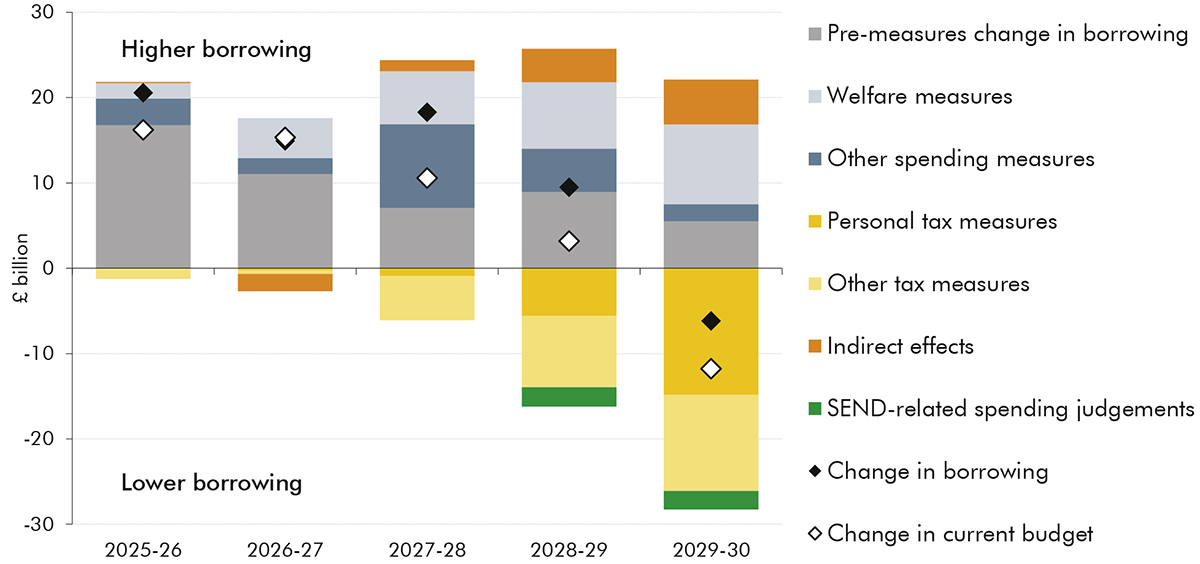

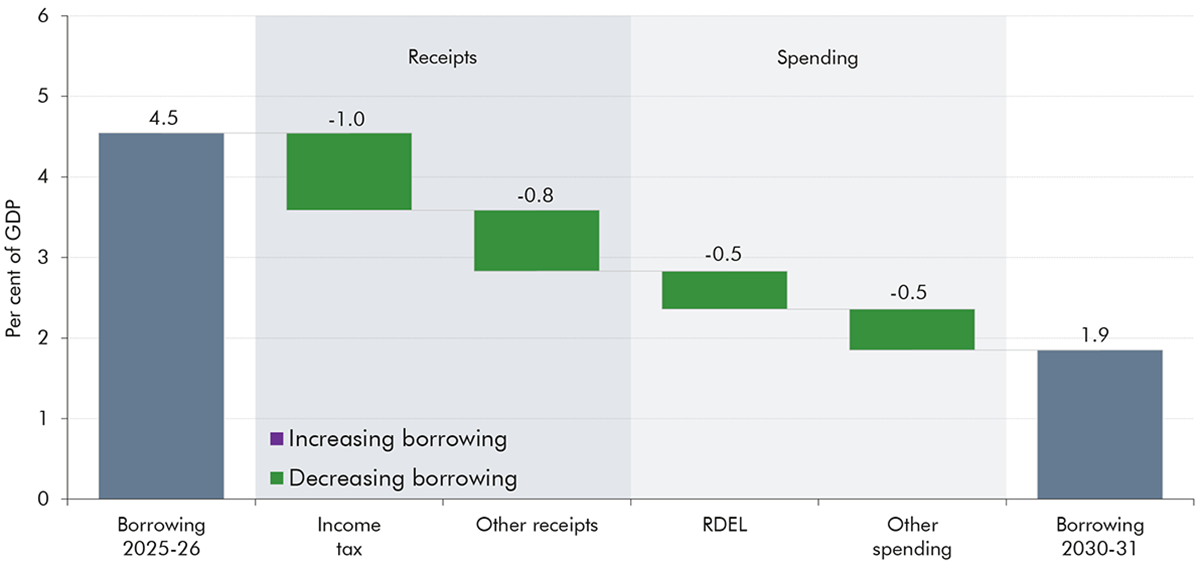

1.15 In the face of this comparatively modest medium-term deterioration in the pre-measures fiscal outlook, the direct effects of Budget policies increase borrowing by £6 billion next year but reduce it by £15 billion in 2029-30. Policy measures reduce the current deficit by more than borrowing due to the estimated impact of policy on local government and other capital spending.

1.16 Spending policies in this Budget increase borrowing in every year, by £7 billion next year and by £11 billion in 2029-30. They comprise:

Welfare measures, with a combined cost of £9 billion in 2029-30. These include the reversals to previously announced cuts to winter fuel payments and health-related benefits (costing £7 billion in 2029-30), and the removal of the two-child limit within universal credit (costing £3 billion by 2029-30) which increases benefits for 560,000 families by an average of £5,310.

Other spending measures, which increase borrowing by £2 billion in 2026-27 and £10 billion in 2027-28, but only £2 billion in 2029-30. These include temporarily part-funding the renewables obligation, which costs £3 billion next year and an average of £2 billion in 2027-28 and 2028-29, before the subsidy is removed in 2029-30; as well as changes to departmental spending which increase spending in the near term and leave it broadly unchanged over the forecast period as a whole.

1.17 Tax increases raise £0.7 billion next year and £26 billion in 2029-30, more than offsetting the increase in spending by the final years of the forecast. They comprise:

A set of personal tax rises with a combined yield of £15 billion in 2029-30. These include: freezing tax thresholds from 2028-29 onwards, which raises £8.0 billion in 2029-30 and contributes to around 780,000 more basic-rate, 920,000 more higher-rate, and 4,000 more additional-rate taxpayers by 2029-30 than in the March forecast; charging National Insurance on salary-sacrificed pension contributions, which raises £4.7 billion; and increasing tax rates on dividends, property and savings income by 2 percentage points, raising £2.1 billion.

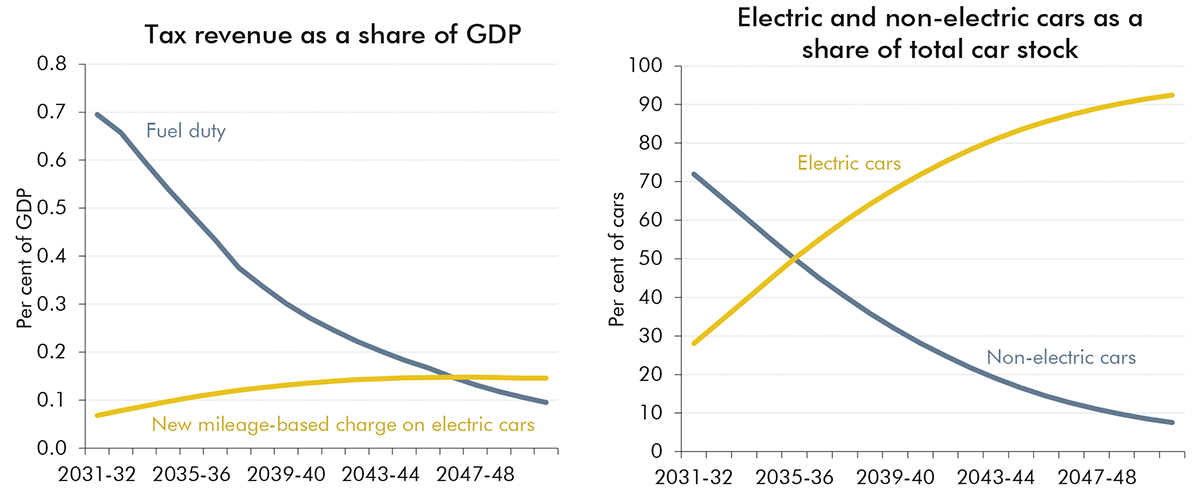

Other tax changes raise £11 billion by 2029-30. These include a new mileage-based charge on electric and plug-in hybrid cars from April 2028 at around half the fuel duty rate paid by drivers of petrol cars (raising £1.4 billion); a reduction to writing down allowances in corporation tax (£1.5 billion); reforms to gambling taxation (£1.1 billion); changes to capital gains tax reliefs on employee ownership trusts (£0.9 billion); and tax administration, compliance and debt collection measures (£2.3 billion). These tax rises are partially offset by a further freeze to fuel duty rates until September 2026, which costs £2.4 billion next year and £0.9 billion in the medium term.

1.18 The indirect effects of Budget policy measures on the economy are estimated to lower borrowing by £2 billion in 2026-27 largely thanks to impact of lower inflation on debt interest spending. From 2027-28 onwards, the indirect effects of policy add to borrowing by amounts rising to £5 billion in 2029-30. This is mainly due to higher debt interest spending from additional borrowing in the early years of the forecast, and from lower receipts, as the personal tax rises reduce consumption and lower inflation reduces nominal earnings. In addition, we have judged that the Government’s decision to assume the full cost of SEND within central government will lead to higher departmental spending in 2028-29 and lower local authority spending in subsequent years.

Chart 1.5: Public sector net borrowing: changes since March

Source: OBR

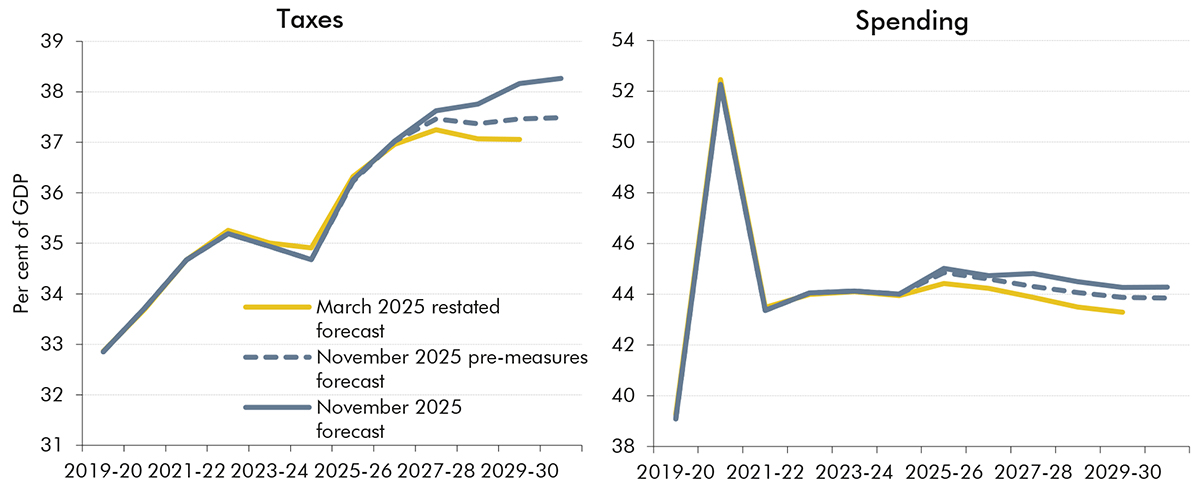

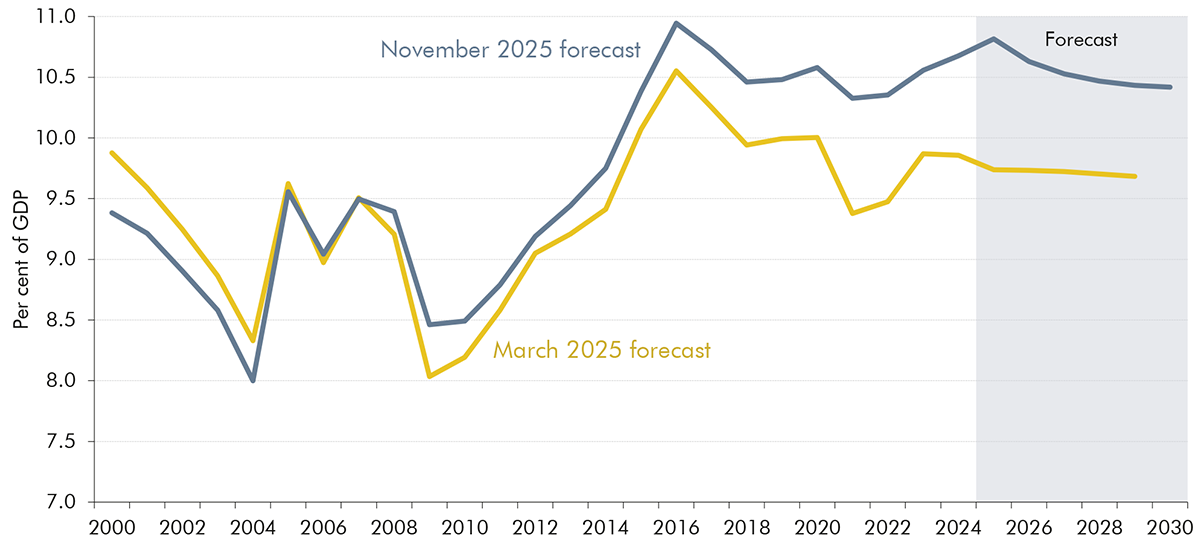

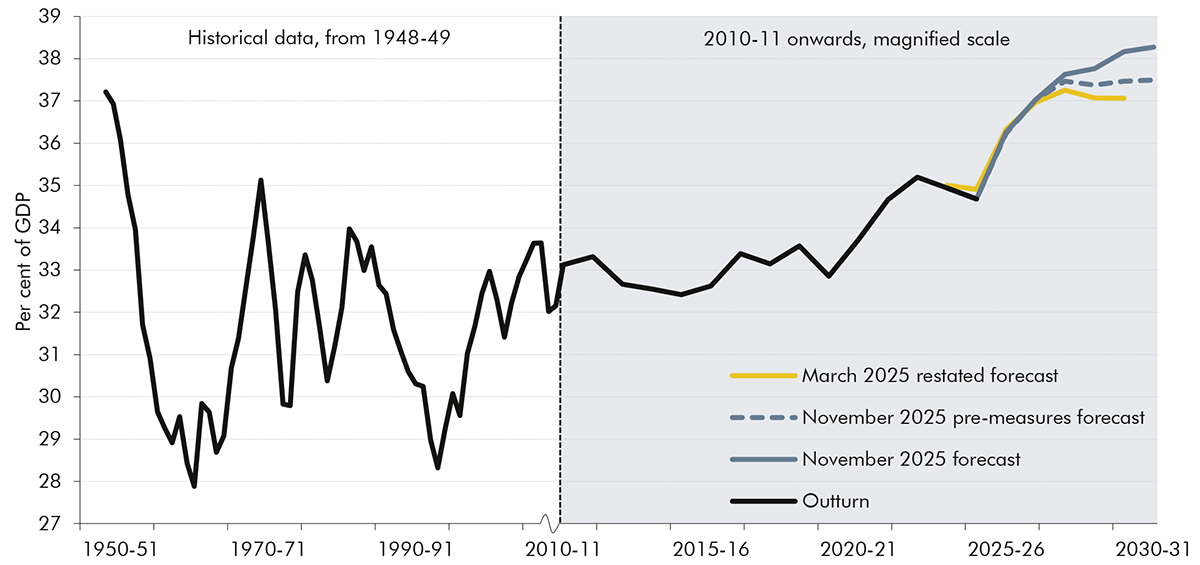

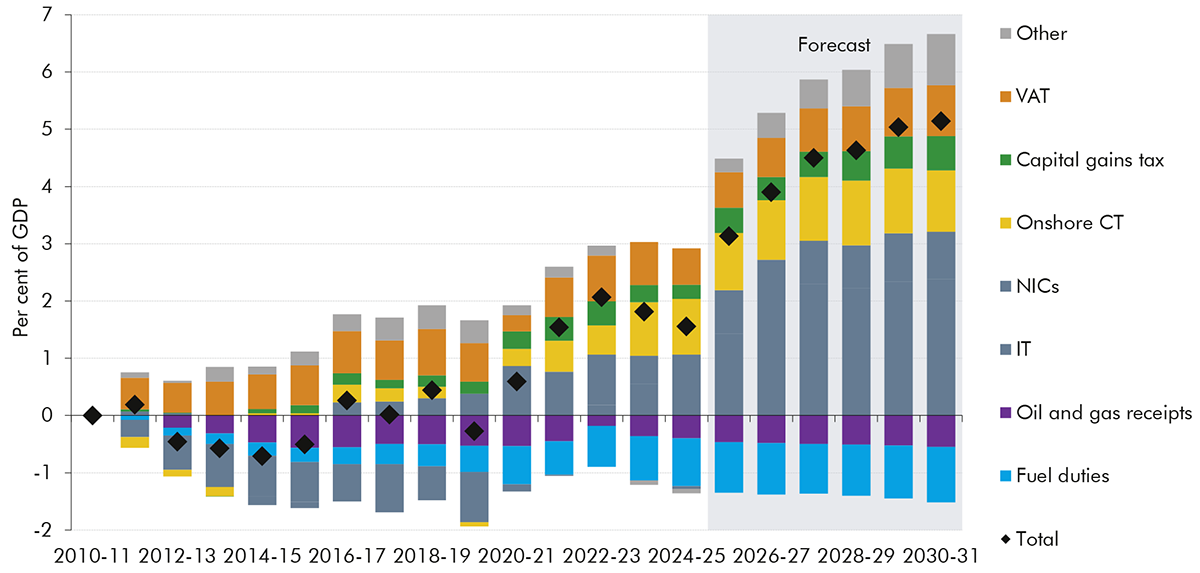

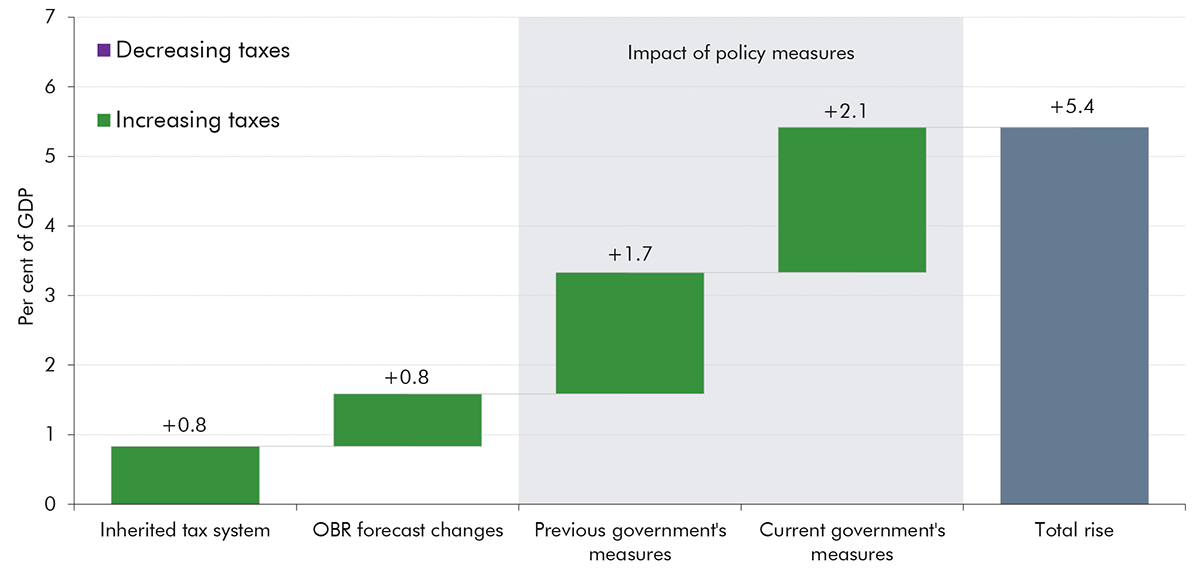

1.19 Incorporating both pre-measures changes and the impacts of policy, National Accounts taxes as a share of GDP are forecast to increase from 35 per cent in 2024-25 to an all-time high of just over 38 per cent from 2029-30 onward. This would be 5 percentage points above their pre-pandemic level. Around two-thirds of this increase in the tax take since 2019-20 comes from rising personal taxes – primarily due to previously announced threshold freezes and employer NICs increases, and the personal tax rise package in this Budget. The forecast for the tax take in 2029-30 is 1 per cent of GDP higher than in our March forecast, with two-fifths of this increase coming from our pre-measures forecast revisions and three-fifths from the tax measures in this Budget.

1.20 Spending as a share of GDP is forecast to rise from 44 per cent in 2024-25 to 45 per cent in 2025-26 and then fall back to 44 per cent of GDP by 2030-31. This would also be 5 percentage points above its pre-pandemic level. The projected fall in spending over the forecast period mainly comes from slower growth in departmental resource spending, which falls by 0.5 per cent of GDP; reductions in spending on a number of time-limited items, such as the Infected Blood and Post Office compensation schemes; and a rising surplus on unfunded public service pension schemes. These declines more than offset a forecast rise in welfare spending (of 0.3 percentage points) and debt interest (of 0.1 percentage points).

Chart 1.6: National Accounts taxes and spending as a share of GDP

Note: Throughout this chapter and this EFO, unless otherwise stated, March 2025 forecast numbers as a per cent of GDP have been rebased to remove the impact of 2025 Blue Book levels revisions.

Source: ONS, OBR

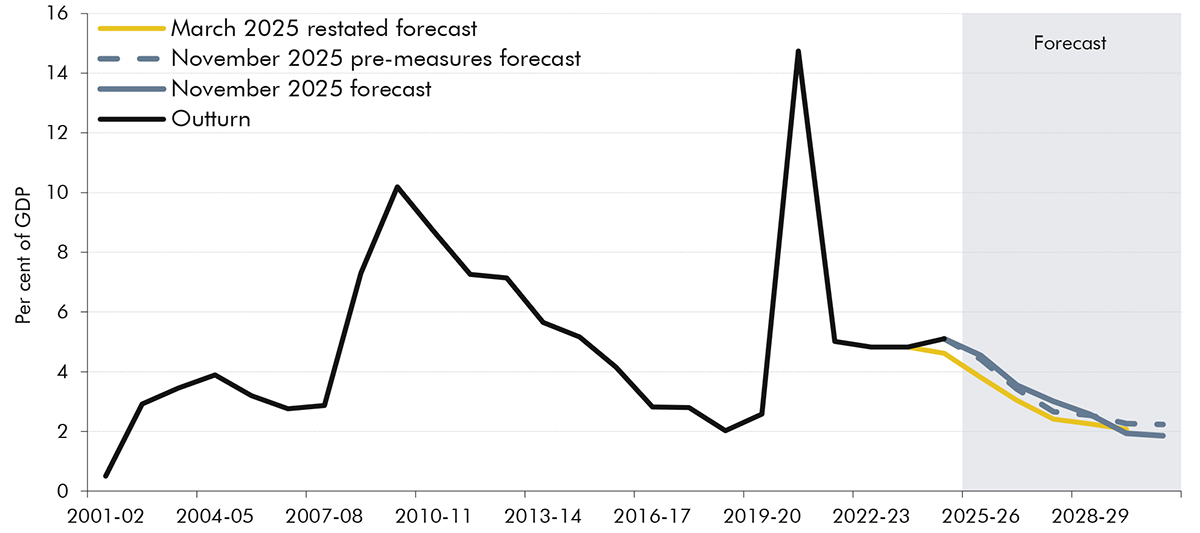

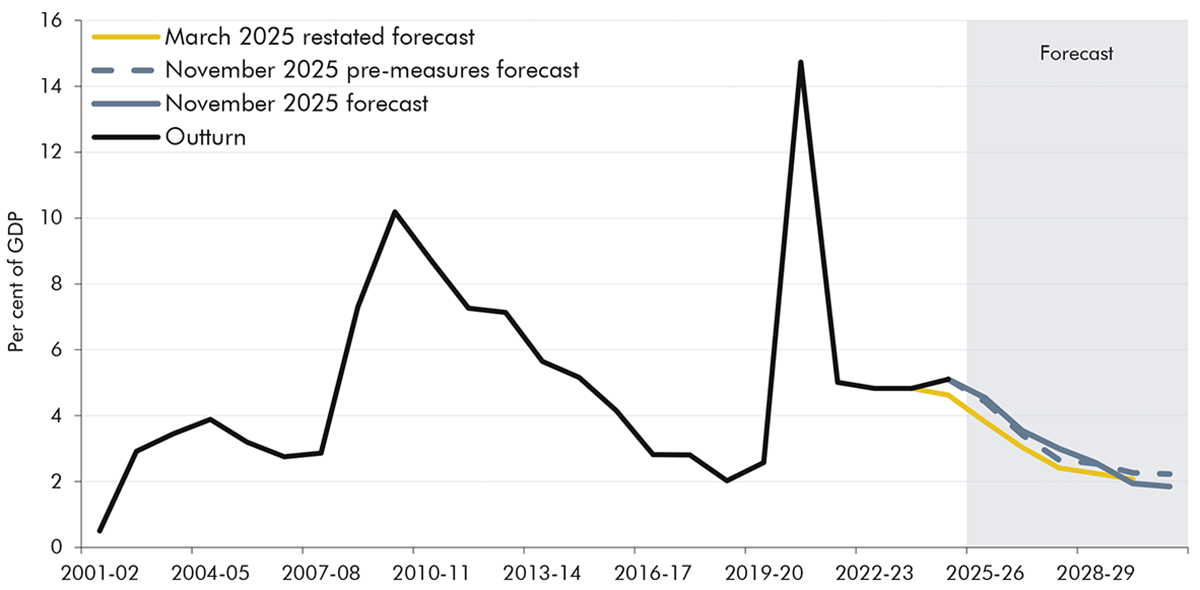

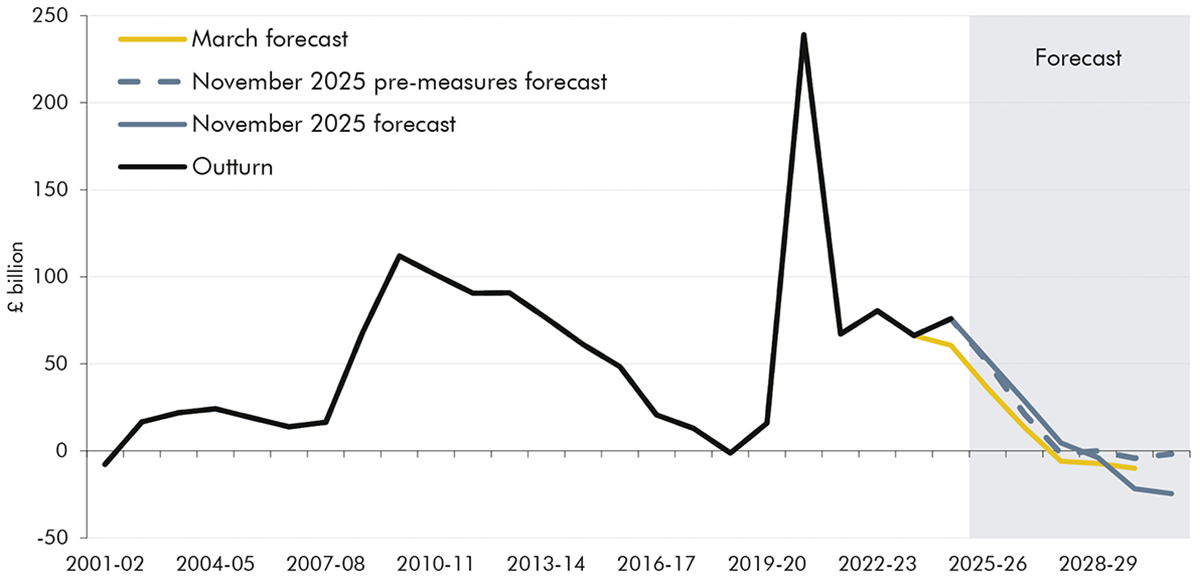

1.21 Borrowing as a share of GDP is projected to fall from 5.1 per cent last year, to 4.5 per cent this year, and then decline to 1.9 per cent of GDP in 2030-31. Compared to March, it is estimated to be higher by £12 billion (0.4 per cent of GDP) in 2024-25 and £21 billion (0.7 per cent of GDP) higher in 2025-26, but still lower by £6 billion (0.2 per cent of GDP) in 2029-30. In-year forecast revisions and policy changes mean that borrowing this year is forecast to be around 5 per cent of GDP for the fifth year since the pandemic. And the profile of the planned medium-term reduction in borrowing has largely been shifted back a year relative to March with more of the weight of consolidation coming in 2028-29 and 2029-30. Around three-quarters of the planned reduction in borrowing over the next five years now comes from tax increases, compared with two-thirds in Autumn Budget 2024.

Chart 1.7: Public sector net borrowing

Note: Throughout this chapter and this EFO, unless otherwise stated, March 2025 forecast numbers as a per cent of GDP have been rebased to remove the impact of 2025 Blue Book levels revisions.

Source: ONS, OBR

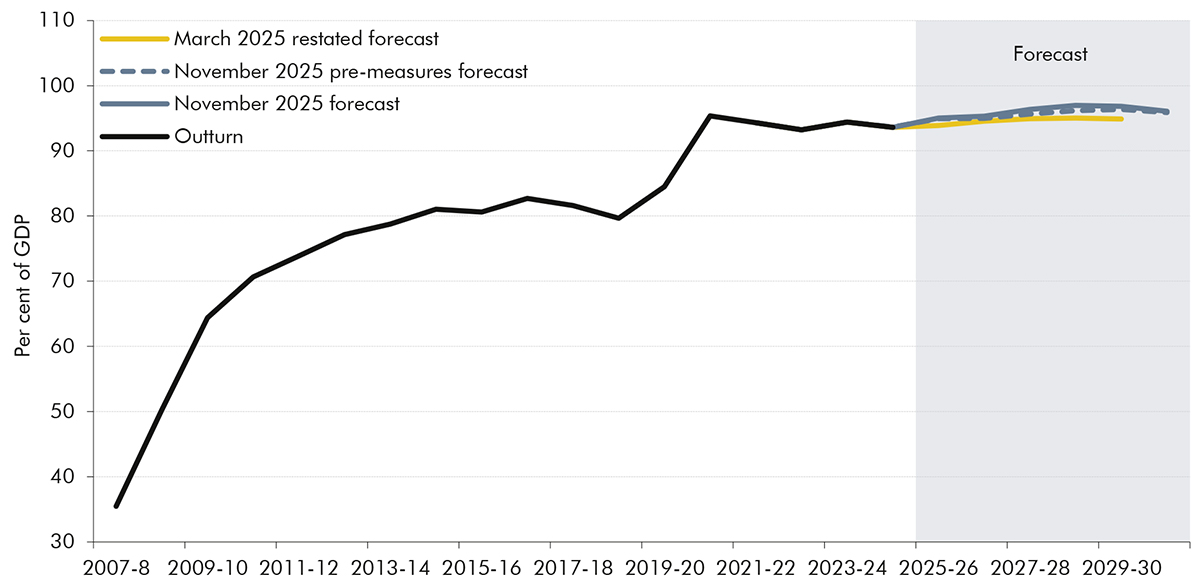

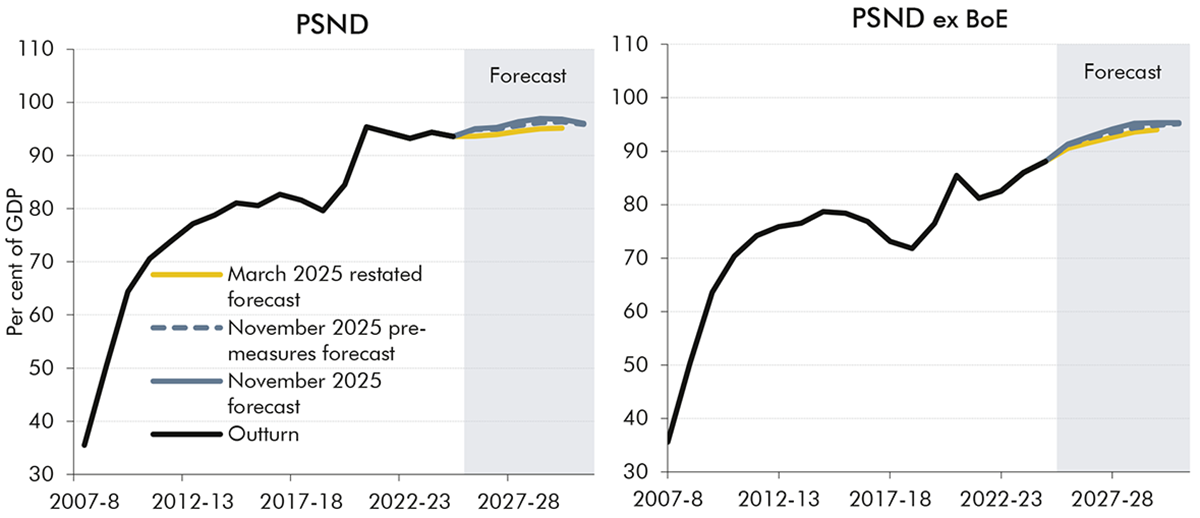

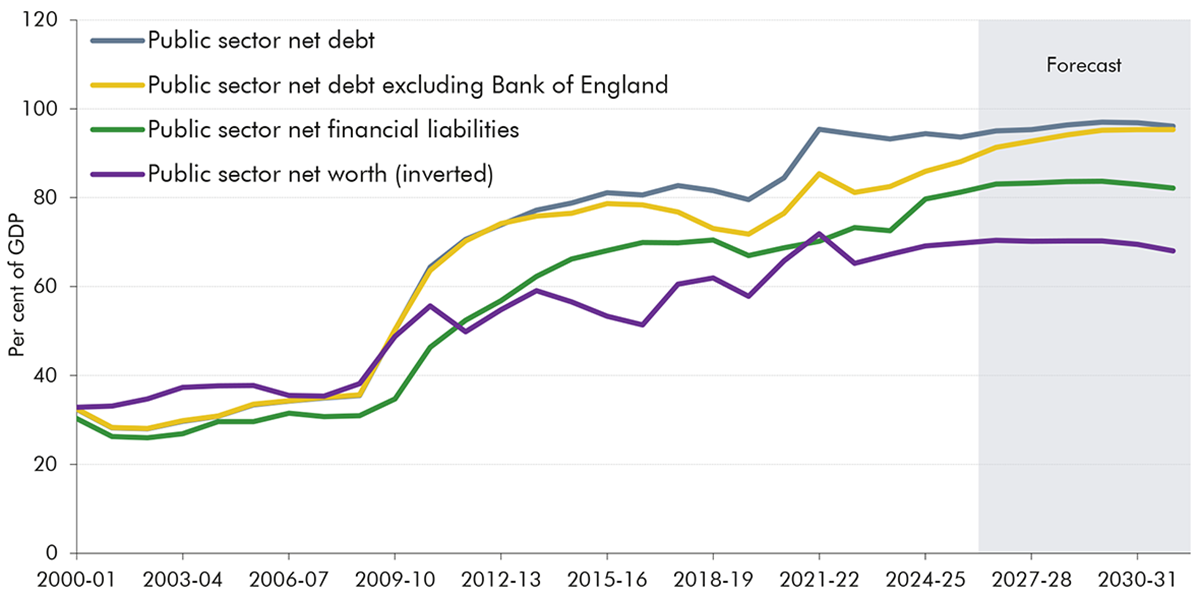

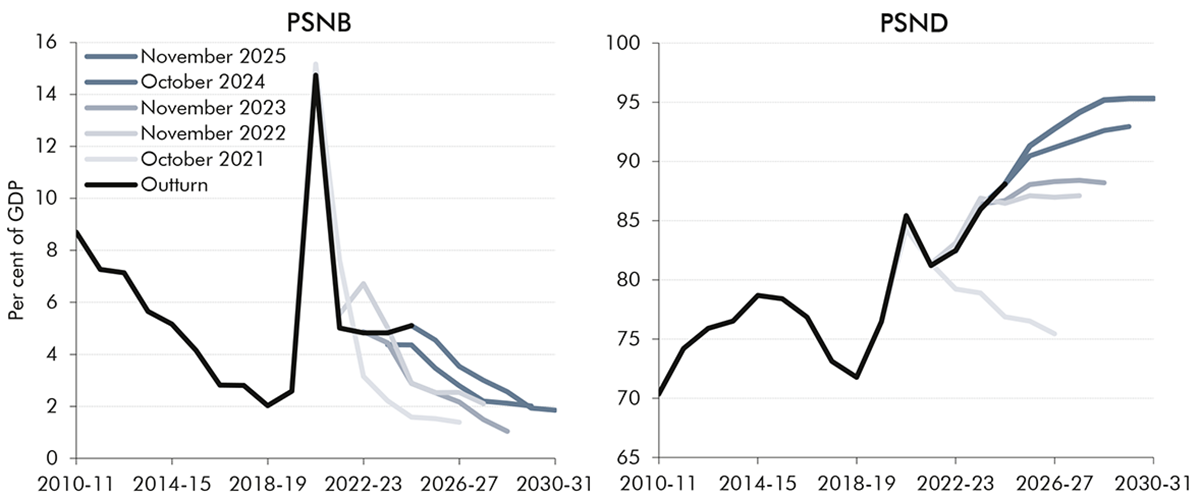

1.22 Public sector net debt (PSND) is forecast to rise from 95.0 per cent of GDP this year to a peak of 97.0 per cent of GDP in 2028-29. It declines slightly to 96.1 per cent of GDP in 2030-31 mainly due to a one-off Bank of England repayment. Compared to the restated March forecast, PSND is 1.5 per cent of GDP higher on average over the forecast, mainly due to higher borrowing in the near term. Underlying debt, excluding the Bank of England, follows a similar trend to forecasts over the past few years, with higher near-term borrowing meaning debt is initially forecast to rise and it then stabilises later but at a higher level than previously forecast.

Chart 1.8: Public sector net debt

Note: Throughout this chapter and this EFO, unless otherwise stated, March 2025 forecast numbers as a per cent of GDP have been rebased to remove the impact of 2025 Blue Book levels revisions.

Source: ONS, OBR

Performance against the Government’s fiscal targets

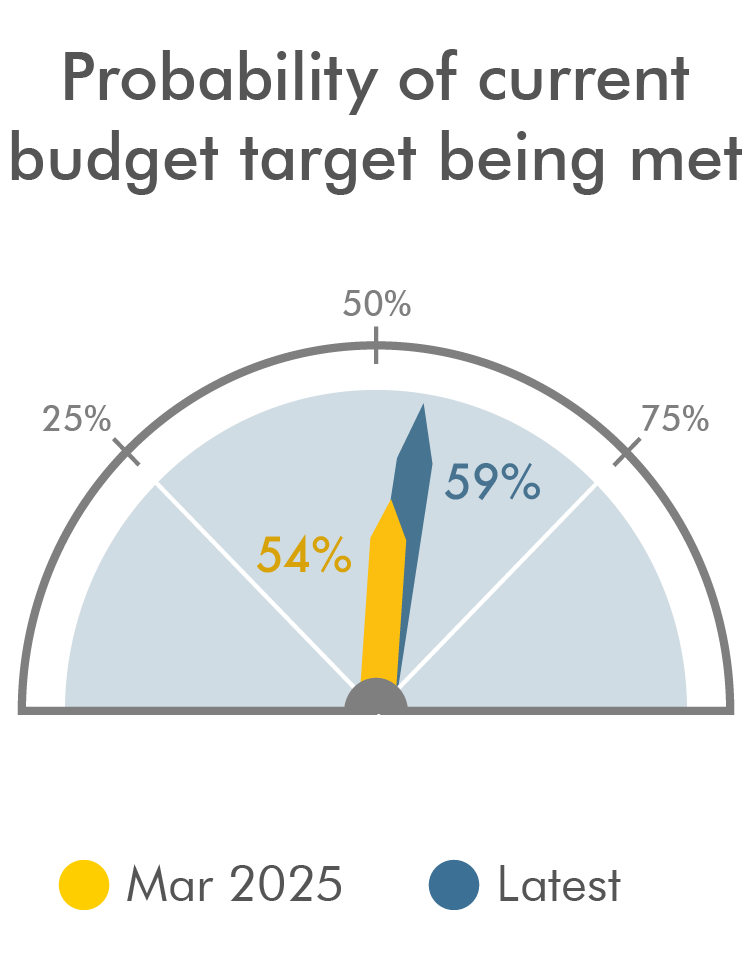

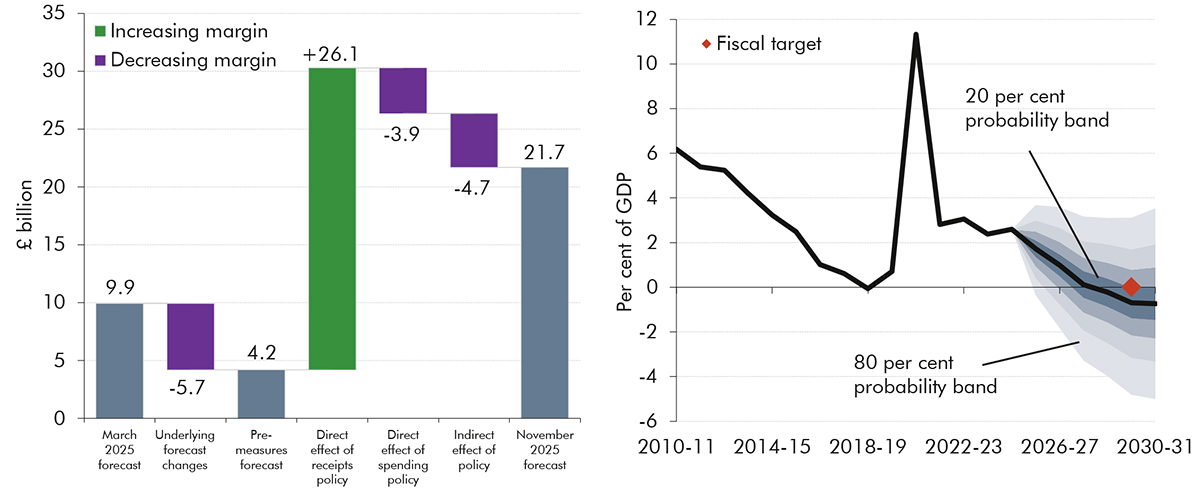

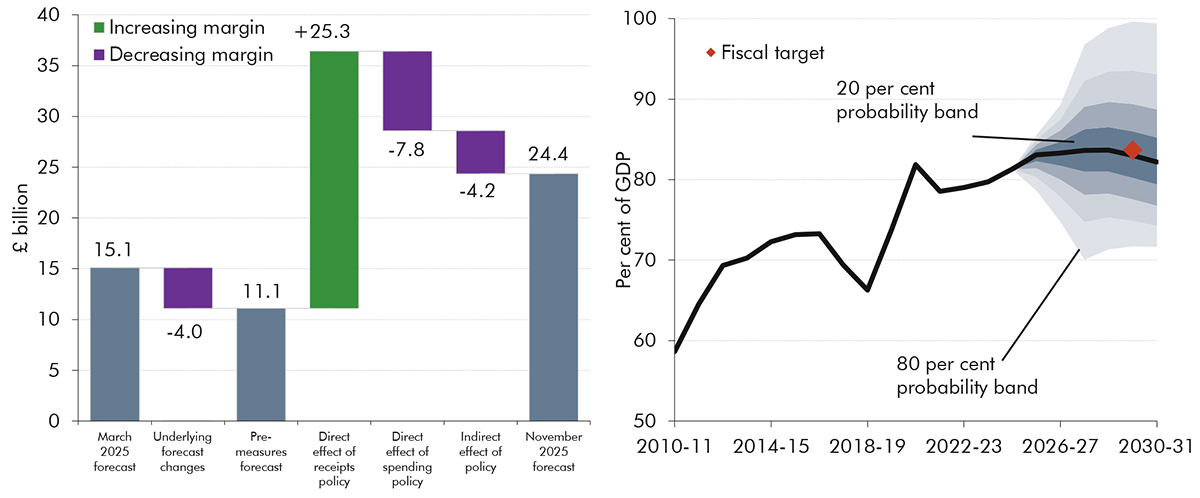

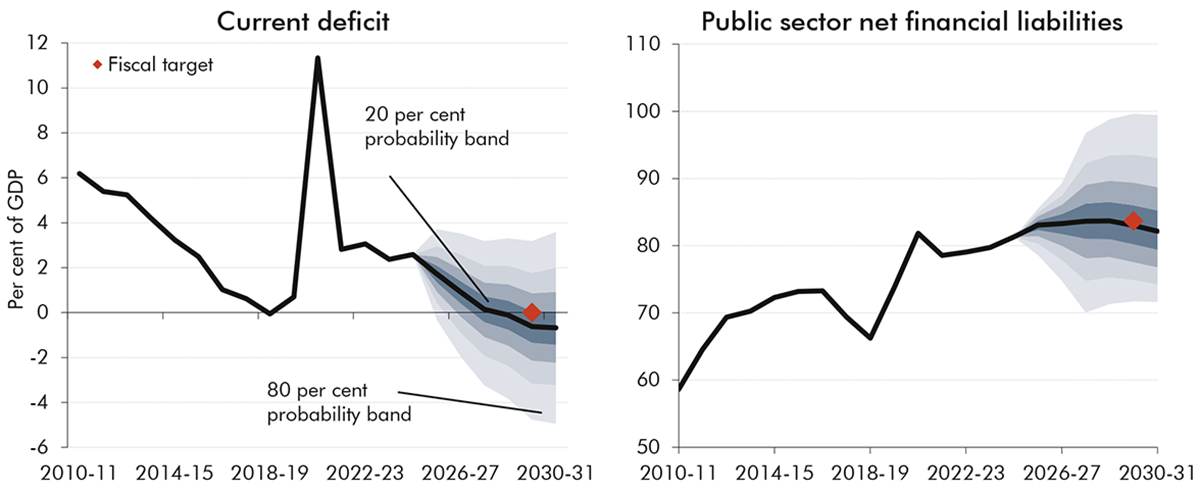

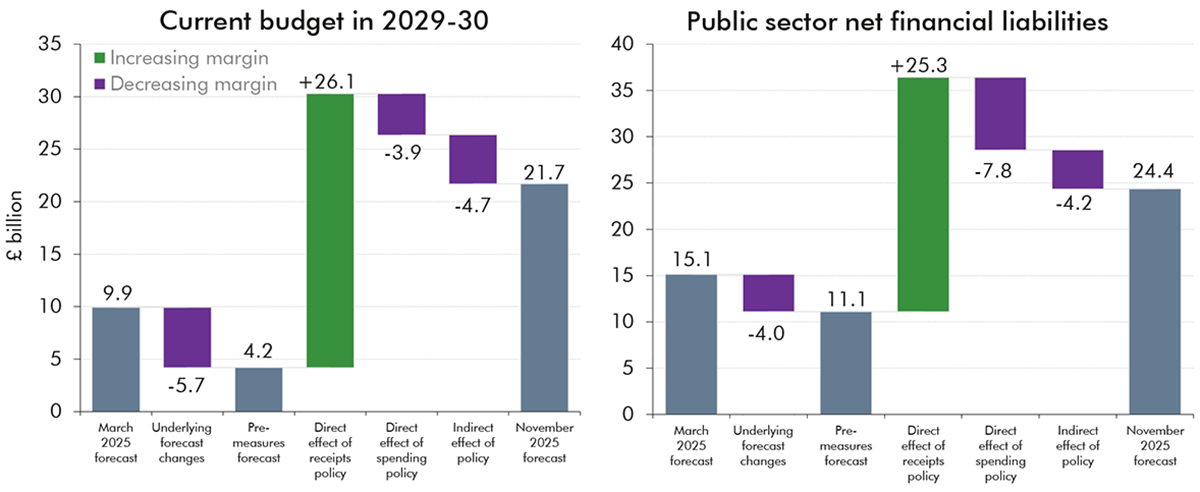

1.23 In our central forecast, the Government’s fiscal mandate for the current budget to be in balance in 2029-30 is met by a margin of £22 billion (0.6 per cent of GDP), which is £12 billion (0.3 per cent of GDP) more than in March. Underlying forecast changes reduced headroom against the current budget by £6 billion – so the fiscal mandate would have been met by around £4 billion in the pre-measures forecast. Budget policies then improved the current budget by around £18 billion so that the mandate is met with a bit more than double the £10 billion margin in the previous two forecasts.

1.24 The probability of meeting the fiscal mandate is 59 per cent, up from 54 per cent in March. This reflects the larger projected current surplus in the target year and also the target year moving a year forward in the forecast period compared to March. The margin against the fiscal mandate is roughly equal to the £21 billion average absolute pre-measures forecast revision to borrowing in four years’ time. It is three-quarters of the £29 billion average margin maintained by previous Chancellors. But it is only two-fifths of the £54 billion median difference between our four-year forecast for borrowing and actual outturn. The large difference between forecast and outturn several years ahead in large part reflects the scale of unforeseen shocks that have hit the economy over the past couple of decades and the scale of the fiscal policy response to them.

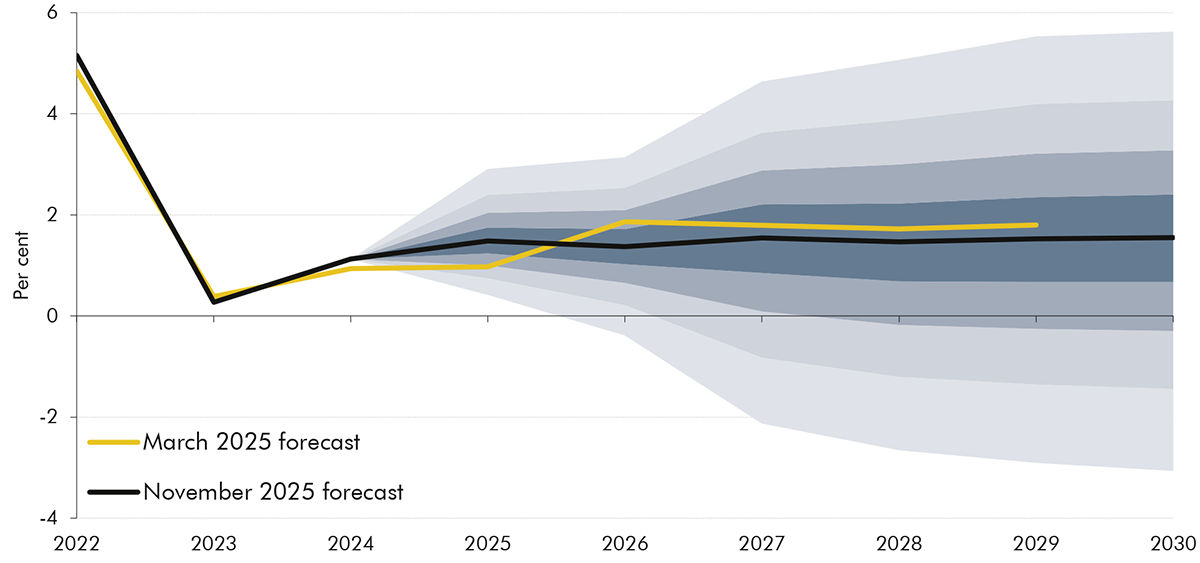

Chart 1.9: Current budget margin and current deficit fan chart

Source: ONS, OBR

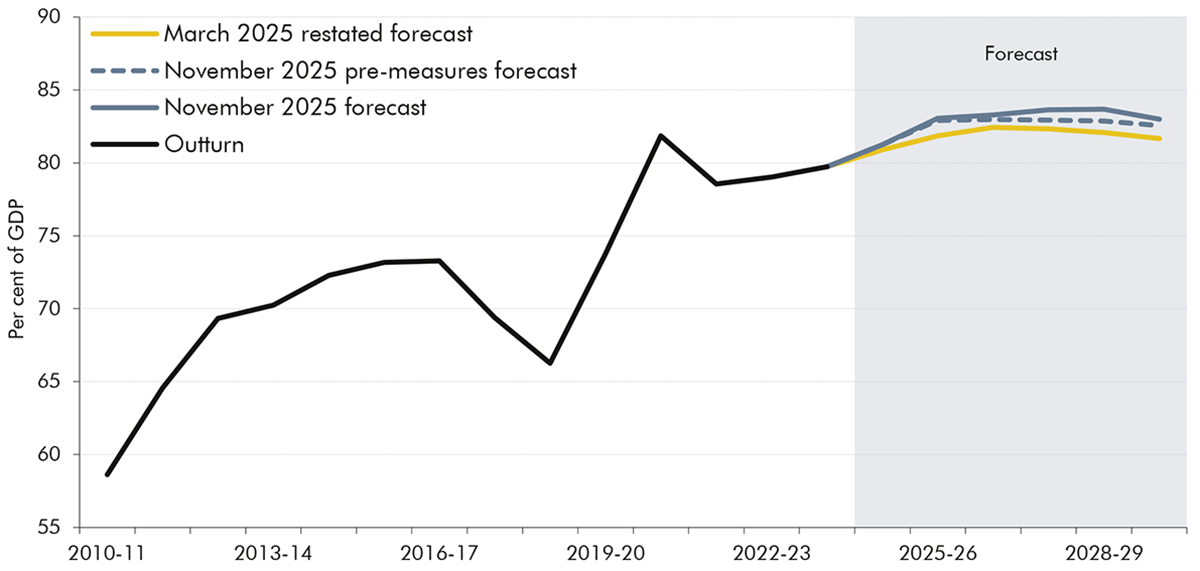

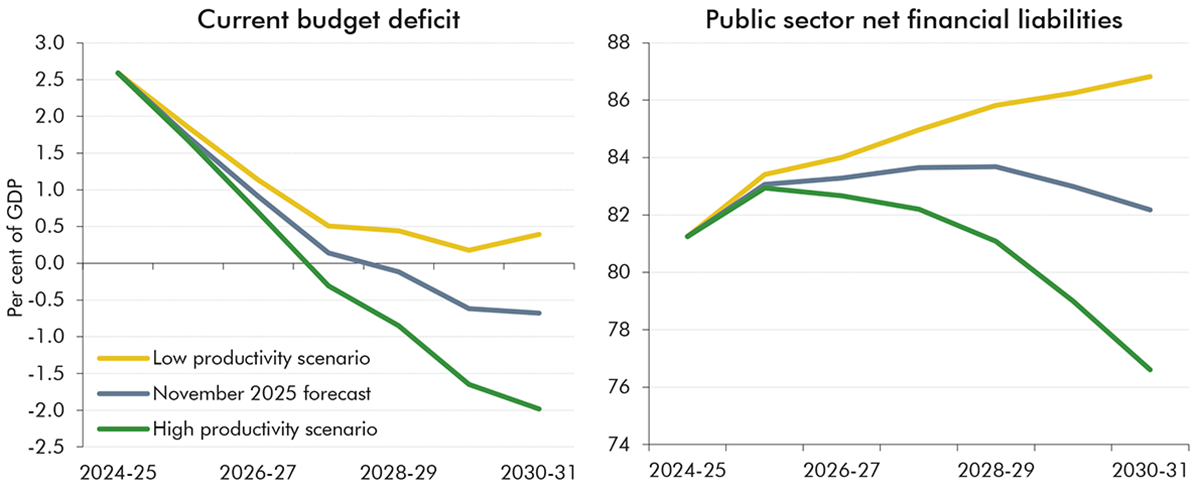

1.25 The supplementary target for public sector net financial liabilities (PSNFL) to be falling in 2029-30 is also met in the central forecast, by a margin of £24 billion (0.7 per cent of GDP). This is £9 billion (0.3 per cent of GDP) more than in March. PSNFL is forecast to rise from 83.1 per cent of GDP this year to a peak of 83.7 per cent in 2028-29 and falls thereafter to 82.2 per cent in 2030-31. Based on historical forecast errors, the probability of meeting the supplementary target is 52 per cent, up from 51 per cent in March.

Chart 1.10: Net financial liabilities margin and fan chart

Source: ONS, OBR

Risks and uncertainties

1.26 These margins are larger than at recent events but remain small in the context of the significant risks and uncertainties around the central forecast. While the pre-measures change to overall borrowing in this forecast compared to March was relatively small, this was the net effect of significant offsetting changes within our economy forecasts and between tax and spending, which may not recur in future forecasts. And previous forecasts have seen significant changes to the fiscal outlook from the impact of major economic shocks and the crystallisation of specific risks to spending or receipts.

1.27 Key risks to our economy forecast, explored in Chapter 7, include:

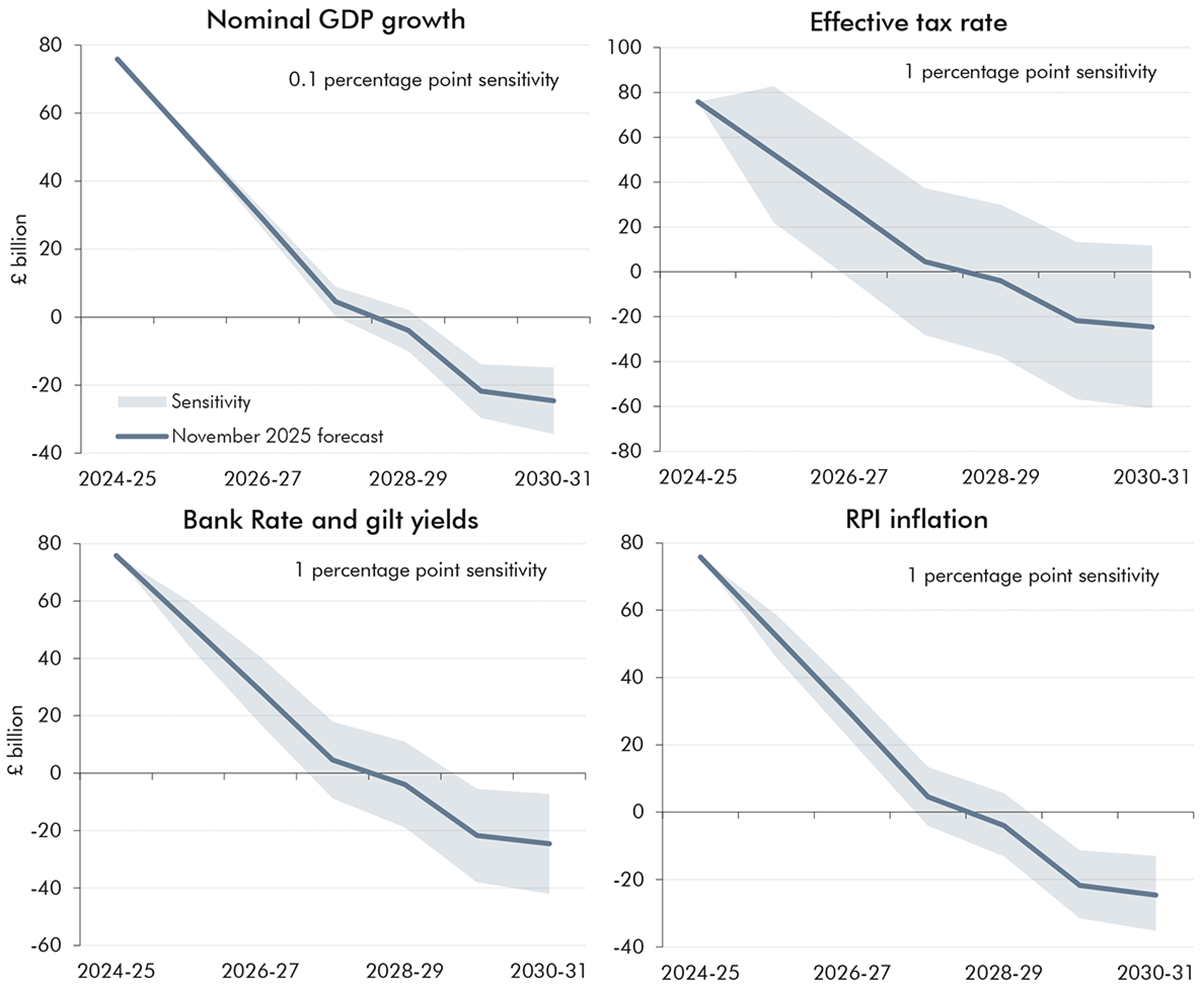

Productivity growth remains one of the most important, but uncertain, judgements in our economy and fiscal forecasts. We have revised down our assessment of medium-term productivity growth from 1.3 per cent to 1 per cent. If productivity growth were to be 0.5 per cent in each year of the forecast, similar to growth over the past 15 years and around half our revised medium-term trend, the current budget would be in deficit by £6 billion in 2029-30 compared to a surplus of £22 billion in our central forecast. If productivity were to grow more quickly than in our central forecast with growth reaching 1.5 per cent in the medium term, based in part on a more optimistic scenario for the impact of AI, the current budget would be in a surplus of £59 billion in 2029-30.

Bank Rate and gilt yields have varied by around 0.6 percentage points since March. Our sensitivity analysis suggests that a 1 percentage point increase in Bank Rate and gilt yields would reduce the current surplus by £16 billion in 2029-30, reducing the margin against the fiscal mandate. A 1 percentage point decrease in interest rates would increase the margin by a similar amount.

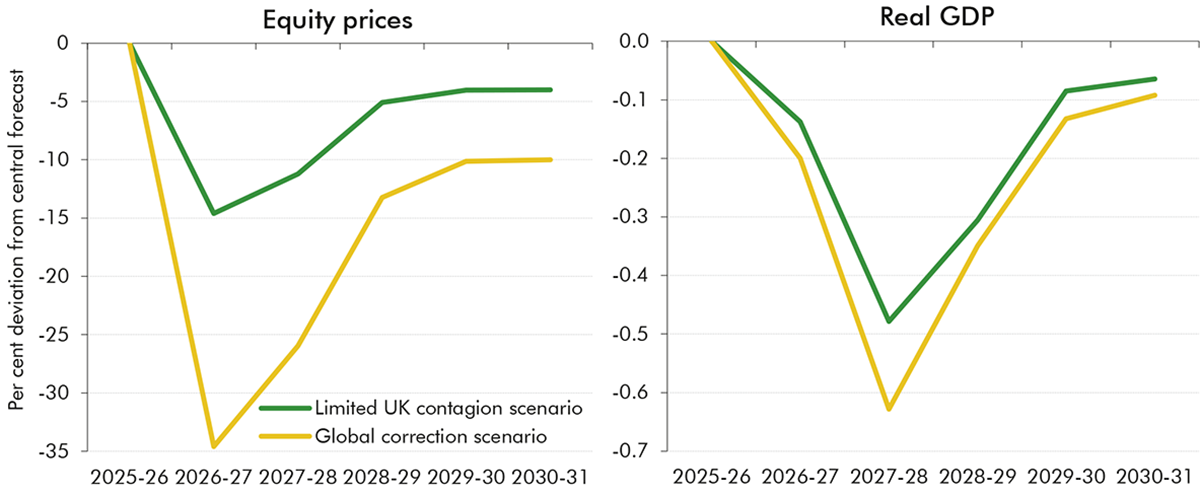

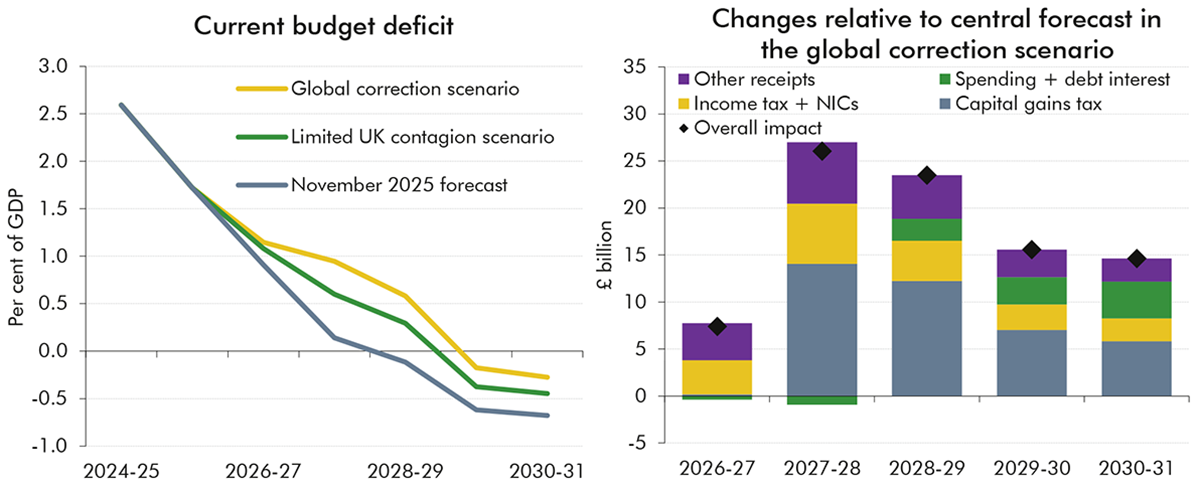

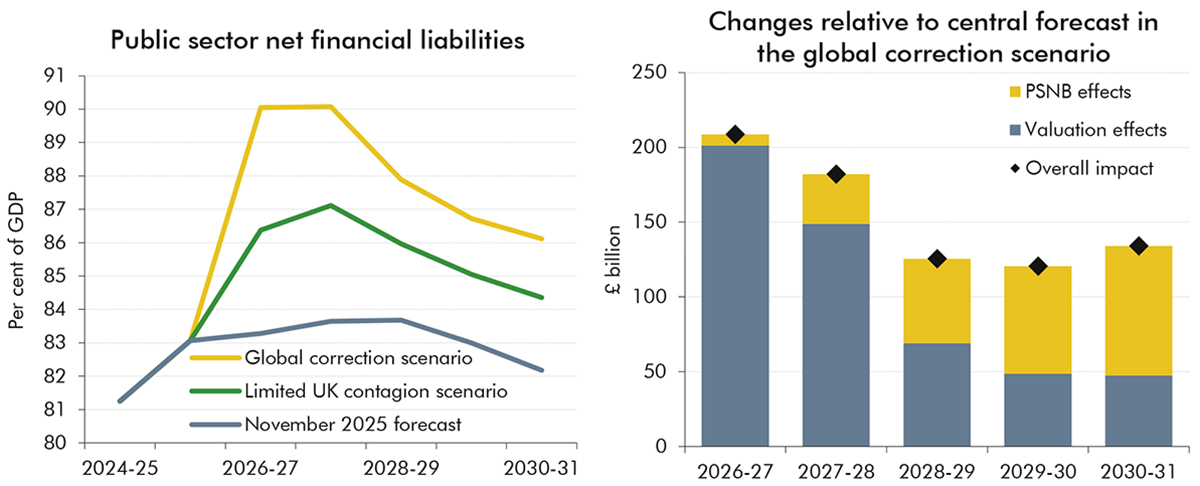

UK equity prices are, on average, 4 per cent higher than in our March forecast. The price-to-earnings ratio for US equities is close to the levels seen during the dotcom bubble and post-pandemic rally in 2021. In our ‘global correction’ scenario, UK and world equity prices fall 35 per cent in 2026-27, and remain lower than in our central forecast over the medium term. This reduces UK GDP by 0.6 per cent at its peak and 0.1 per cent over the medium term. The decline in real GDP leads to a £16 billion (0.4 per cent of GDP) deterioration in the current budget and £121 billion (3.7 per cent of GDP) increase in PSNFL by 2029-30. In the ‘limited UK contagion’ scenario, UK equity prices fall by 15 per cent in 2026-27 and the peak fall in UK GDP is 0.5 per cent. This results in a £9 billion (0.2 per cent of GDP) and £61 billion (2.1 per cent) increase in the current budget deficit and PSNFL in 2029-30 respectively.

1.28 Key risks to the medium-term fiscal forecast include:

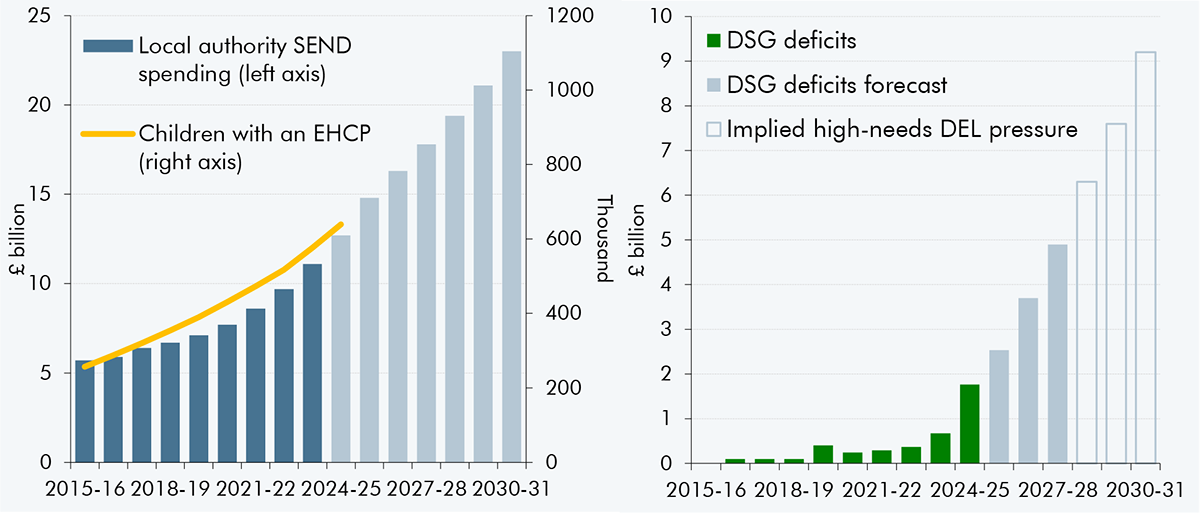

Local authority borrowing has increased by around £7 billion a year in this forecast compared to March, reflecting recent upward revisions to outturn and financial pressures including from the costs of SEND. The ‘statutory override’, which allows local authorities to disregard deficits caused by financing SEND provision when meeting their requirement to balance budgets, is due to end in 2027-28. At this point the stock of these deficits is estimated to reach a total of £14 billion, and as a result many local authorities would likely be unable to meet their balanced budget requirement. The Government has not set out how this fiscal risk would be addressed.

With inflation now forecast to be higher than when Spending Review envelopes were set in March 2025, overall real departmental spending growth would have been 0.1 percentage points lower on a pre-measures basis. In addition, the Government has stated that the full cost of SEND provision will be absorbed within departmental budgets in 2028-29, but no savings have been identified to offset the estimated £6 billion pressure this will create. Other spending risks include: the impact on the NHS budget of further strikes and negotiations over NHS pharmaceutical spending; the assumption that the Home Office will reduce small boat arrivals and end the use of hotels for asylum seekers by mid-2028, and deliver savings on the asylum budget of £1.1 billion; the unfunded cost of digital ID cards at a provisional annual cost of £0.6 billion over the Spending Review period; and the commitment for defence spending to reach 3.5 per cent of GDP by 2035, which would cost an additional £32 billion in today’s money.

There also remains significant uncertainty around the future costs of welfare spending due to the growth of disability and health caseloads, which have increased very sharply since the pandemic. We assume in the forecast that these caseloads will continue to rise but at a slower pace than recently. If growth instead continued at the rate seen since the pandemic, this would increase spending in 2029-30 by a further £11 billion.

The tax-to-GDP ratio is forecast to increase to an all-time high of 38.3 per cent of GDP in 2030-31. A higher level of the tax take increases the risk that incentives within the tax system distort or constrain economic activity by more than expected. The yield from the personal tax threshold freezes, extended in this Budget, is very sensitive to future inflation and nominal earnings growth. If nominal earnings growth was 1.8 percentage points lower than forecast, this would reduce personal tax revenues by 2029-30 by £19 billion.

1.29 At this Budget the Government has taken action to mitigate some fiscal risks that we have highlighted previously. The probability of the fiscal mandate being met is now 59 per cent, its highest level since before the pandemic, and with a margin of £22 billion, double that in March. The introduction of the new mileage-based charge on electric cars will offset around one-quarter of the 0.6 per cent of GDP in revenue set to be lost from fuel duty by 2050 due to the transition to electric vehicles. The target year for the fiscal mandate is now the fourth year of the forecast (2029-30), rather than the fifth year, which reduces the scope for fiscal consolidation to be further postponed. And the target year will move to the third year of the forecast from next year. The Government has also set out a further set of reforms to manage balance sheet risks.

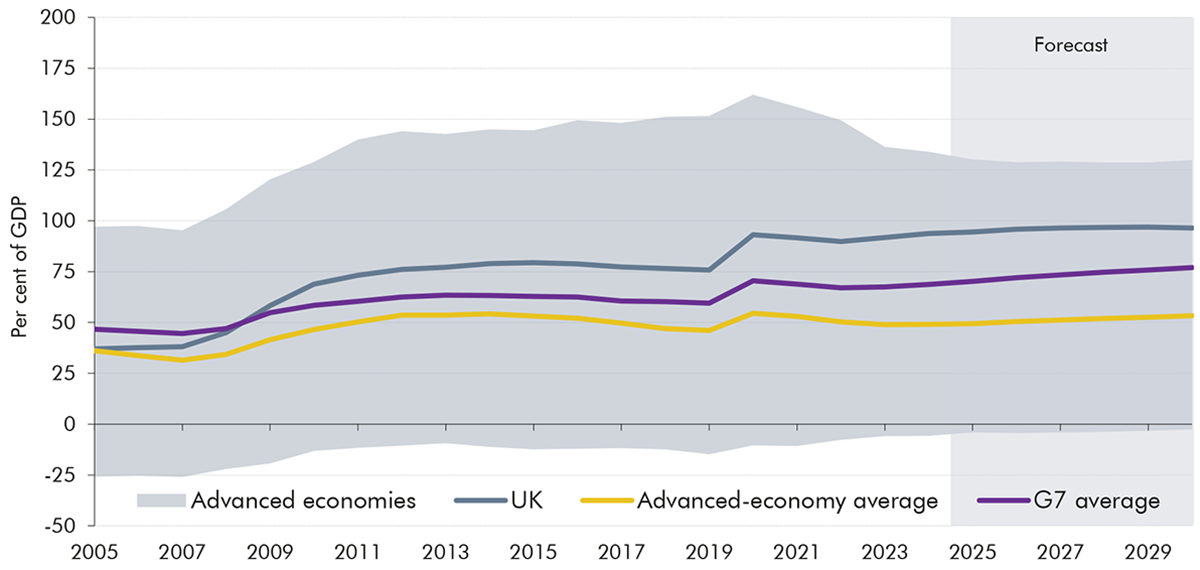

1.30 While this Budget addresses some fiscal risks and increases the margin held against the Government’s fiscal targets, it still leaves the UK public finances relatively vulnerable to future shocks. Even if the Government were to meet its fiscal rules and reduce overall borrowing to below the roughly 2½ per cent of GDP it invests by the end of the decade, this would only reduce the UK’s deficit to the level that the average advanced economy had already achieved several years ago. And it would only just be enough to leave the UK’s debt, which has nearly tripled since the start of the century, stabilising at 96 per cent of GDP by the end of the decade. That would leave the UK with a debt-to-GDP ratio that is around twice the advanced-economy average and the sixth-highest among advanced economies. And the UK would still be devoting more of national income to paying the interest on that debt than at almost any time in its post-war history.

Chapter 2: Economic outlook

2.1 This chapter describes our latest economy forecast, summarised in Table 2.1, including:

the labour market including employment, unemployment, and earnings (from paragraph 2.37);

the composition of economic activity, including households, businesses, government, trade and the current account, and the housing market (from paragraph 2.44);

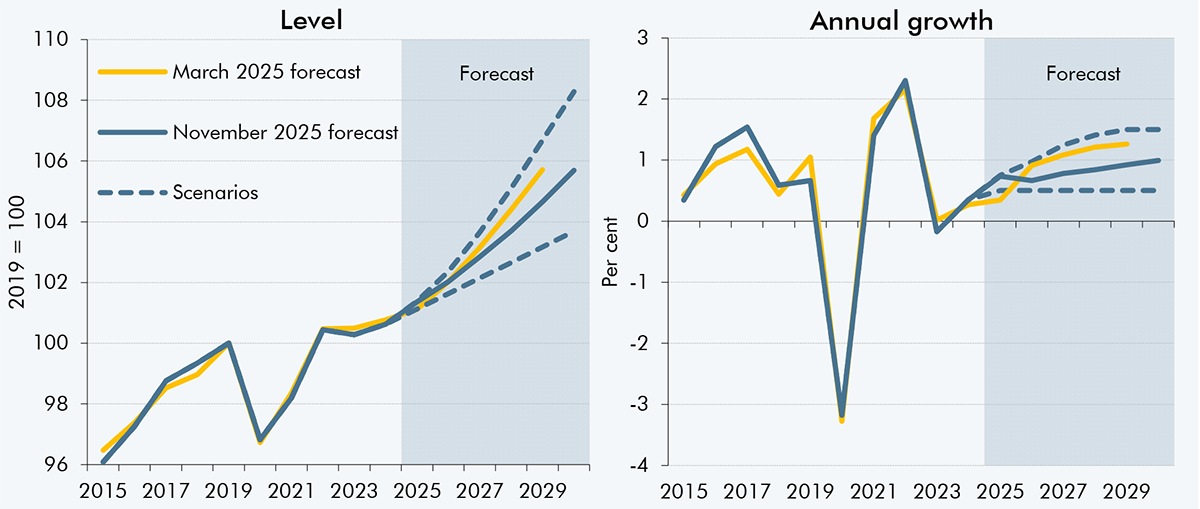

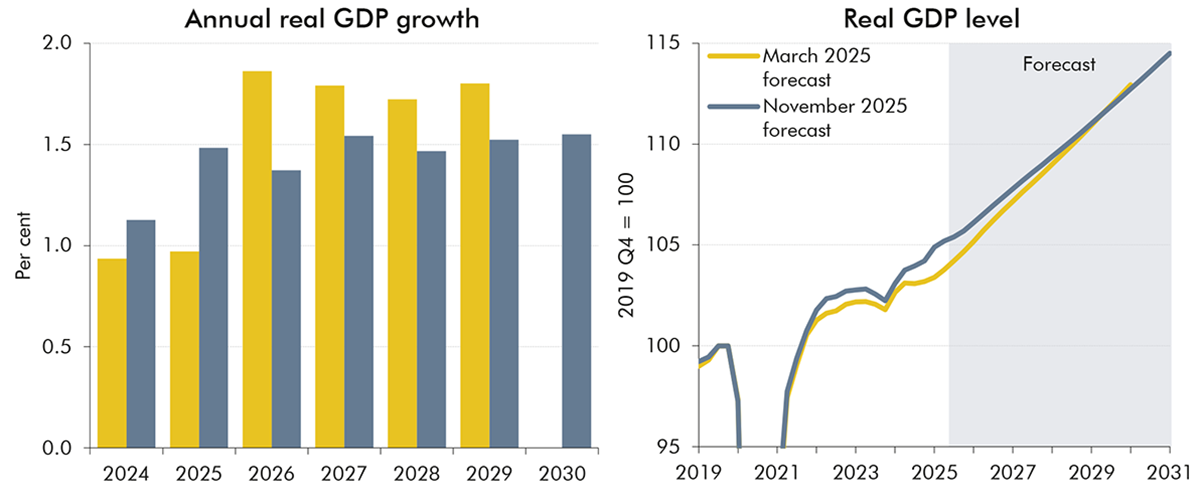

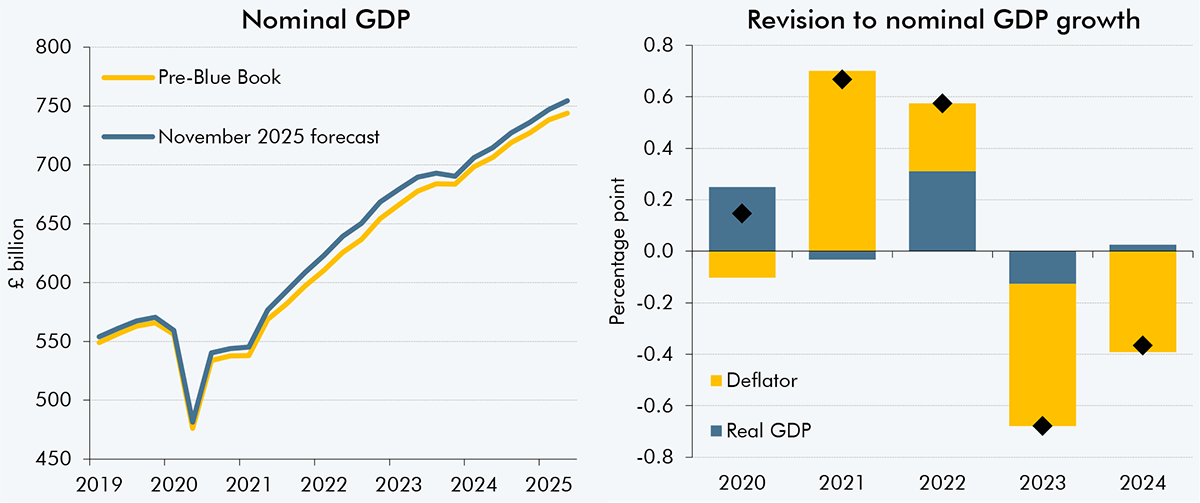

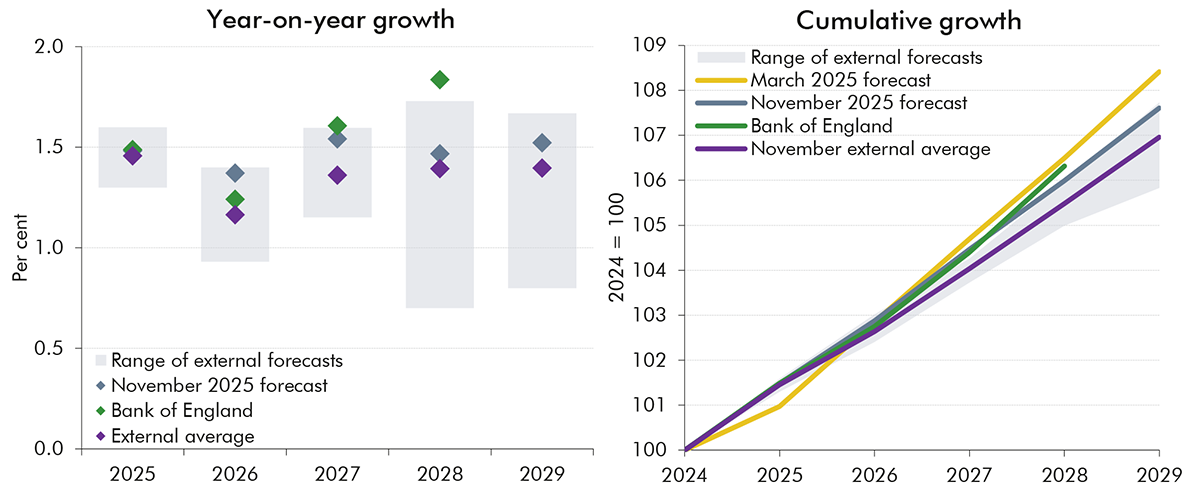

2.2 Relative to our March forecast, the economic outlook is characterised by somewhat weaker medium-term real GDP growth, higher near-term inflation, and a more fiscally favourable composition of nominal GDP growth. We have revised down our central forecast for underlying medium-term productivity growth by 0.3 percentage points to 1.0 per cent after taking stock of its historical evolution and potential drivers over the forecast (see Box 2.1). With our estimate of potential labour supply growth broadly unchanged from March, real GDP growth now averages 1.5 per cent between 2026 and 2029, down from 1.8 per cent in March. At the same time, the ONS has revised up the level of GDP in 2024 by 0.6 per cent, and we have raised our central estimate for real GDP growth in 2025 from 1.0 to 1.5 per cent. The net effect of the higher starting point for, but lower growth in, real GDP over the next five years is to leave its level largely unchanged in 2029 relative to our March central projection. [3]

2.3 In terms of the nominal economy, lower real GDP growth is partly offset by higher inflation and we expect the composition of nominal growth over the forecast to be more tax rich than March. This is mainly because we have revised up our forecast for real wage growth and CPI inflation in 2026 by 2/3 per cent and 0.4 per cent respectively. This reflects the fact that surveys of wage settlement expectations have held up significantly more than we expected and there are signs of more momentum in domestically generated inflation than we anticipated in March. Policy measures in this Budget reduce CPI inflation by 0.3 percentage points in 2026. Cumulative growth in nominal GDP from 2025-26 to 2029-30 is 0.9 percentage points lower than in March, but its composition is more skewed toward labour income and away from corporate profits. Because labour income has a higher effective tax rate and personal tax thresholds are frozen, meaning fiscal drag brings more people into higher tax bands, this more than offsets the negative impact of lower nominal GDP growth on nominal tax receipts. However, significantly higher pre-measures spending, due to higher inflation and other pressures, means there is still a modest deterioration in borrowing over the medium term relative to March, before taking account of government policies.

Table 2.1: Summary of the economy forecast

Key metric (per cent unless otherwise stated)

March 2025

November 2025

Change

Conditioning assumptions

Bank Rate

Average from 2025 to 2029

3.9

3.8

↓

Gilt yields

10-year gilt yields average from 2025 to 2029

4.8

5.1

↑

Global growth

Average growth from 2025 to 2029

3.2

3.1

↓

Key judgements

Potential output

Final year growth(1)

1.8

1.5

↓

Trend productivity

Final year growth(1)

1.3

1.0

↓

Labour supply

Final year growth(1)

0.5

0.5

—

Output gap

Average in 2025 and 2026

-0.4

-0.5

↓

Real GDP

Average growth from 2025 to 2029

1.6

1.5

↓

Inflation

Average CPI inflation between 2025 and 2026

2.6

3.0

↑

Nominal earnings

Average growth from 2025 to 2029

2.7

3.0

↑

Nominal GDP

Cumulative growth from 2025-26 to 2029-30

15.7

14.8

↓

Labour income

Cumulative growth from 2025-26 to 2029-30

12.3

13.1

↑

Corporate profits

Cumulative growth from 2025-26 to 2029-30

23.7

17.2

↓

1) Final year is 2029 in the March forecast and 2030 in the November forecast.

Key: ↑ Higher, ↓ Lower, — Unchanged

Source: Bank of England, ONS, OBR

Conditioning assumptions

Interest rates

2.4 Our economy forecast is conditioned on market expectations for interest rates in the 10 working days to 10 October. Over this period:

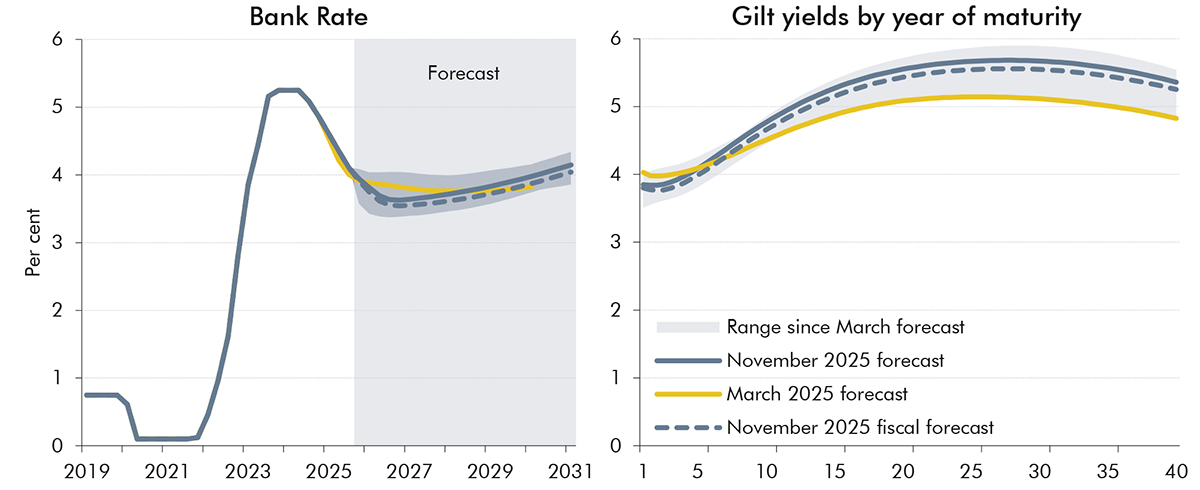

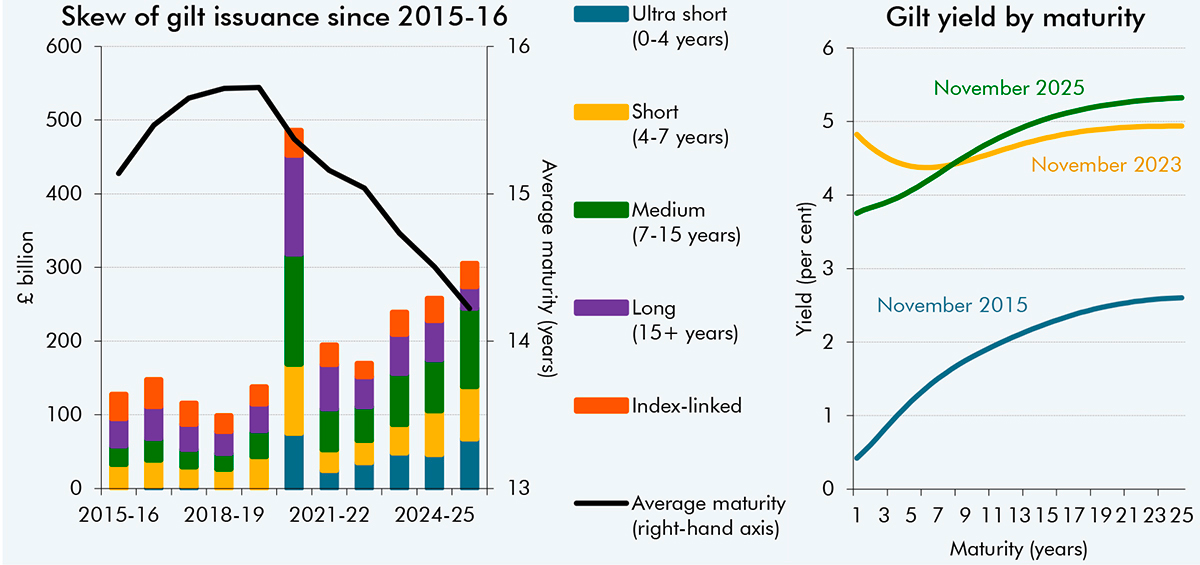

Market participants expected Bank Rate to fall from its current level of 4 per cent to a low of 3.6 per cent at end-2026. The expected rate then rises gradually, returning to 4 per cent by end-2030. Compared to our March forecast, Bank Rate is 0.2 percentage points lower in 2026 and 0.1 percentage points higher in 2029 (Chart 2.1, left panel). Since March, Bank Rate expectations for 2026 have ranged from 3.4 to 4.0 per cent.

The 10-year gilt yield was 4.8 per cent and the 20-year gilt yield was 5.6 per cent. Compared to March, near-term yields are slightly lower but long-term yields are higher, with 10-year yields up 0.3 percentage points and 20-year yields up 0.5 percentage points (Chart 2.1, right panel).Market participants expected the 10-year gilt yield to rise to 5.8 per cent by 2030. This would be the highest level since 2000, but still lower than the longer-term average yield since 1980 of 6.0 per cent. Interest rates on government bonds have remained volatile since March, particularly at longer maturities, with 20-year yields ranging from 5.1 to 5.7 per cent.

2.5 As explained in the Foreword, given the time between closing the pre-measures economy forecast and publishing the Economic and fiscal outlook (EFO), we have taken a later reading of market expectations for interest rates to use in our pre-measures fiscal forecast. These are based on the 10 working days to 21 October. This ensures that our fiscal forecast uses more up-to-date market expectations. Differences compared to the numbers used in our economy forecast were relatively small, with both Bank Rate expectations and gilt yields on average 0.1 percentage points lower (dashed lines in Chart 2.1). Interest rates have fluctuated since we closed our pre-measures forecast, but as of 21 November they were broadly where they were in the 10 days to 21 October.

Chart 2.1: Bank Rate and gilt yields

Note: Our economy forecast uses the 10 working days to 10 October and our fiscal forecast uses the 10 working days to 21 October.

Source: Bank of England, OBR

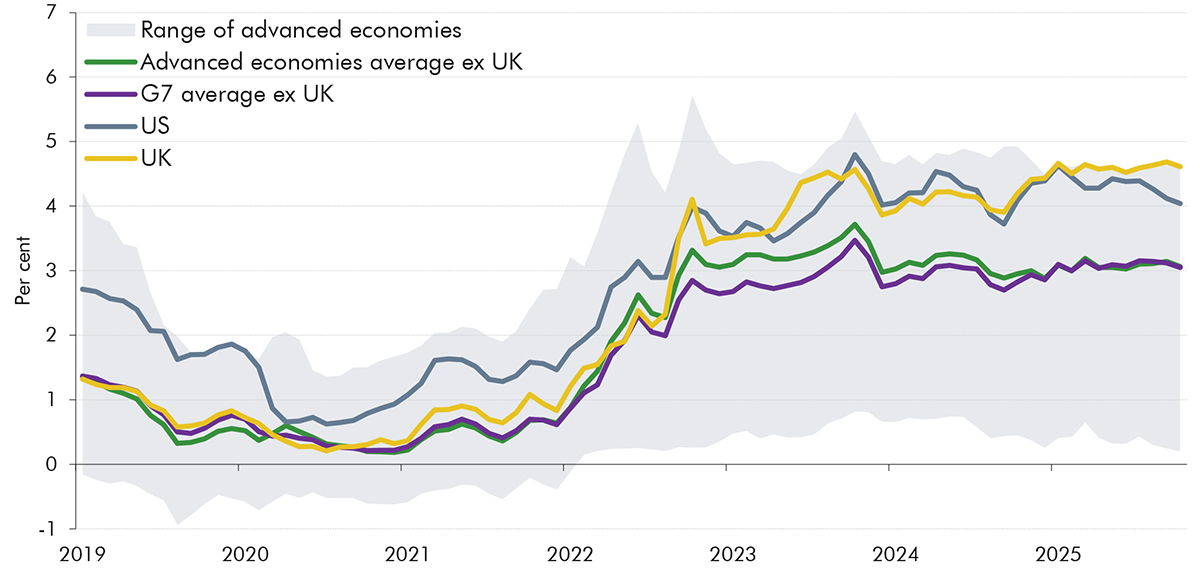

2.6 UK government bond yields are now the highest in the G7, and second highest among the advanced economies, after Iceland. [4] A rise in interest rates has been a common feature across advanced economies over the past three years, however the increase in UK rates since 2021 has outstripped that of its peers (Chart 2.2). Between the start of 2021 and this October, the average 10-year government bond yield for advanced economies (excluding the UK) has risen 2.8 percentage points (from 0.2 to 3.1 per cent) and the 10-year US Treasury yield has also increased by 3.0 percentage points (from 1.1 to 4.0 per cent). Over the same period, the 10-year UK gilt yield has increased by 4.2 percentage points (from 0.4 to 4.6 per cent). This means, since 2021, the differential between UK and other advanced economies has increased by 1.4 percentage points, while the differential relative to the US has risen by 1.3 percentage points.

2.7 The much higher increase in UK government financing costs than in other advanced economies likely reflects several factors:

First, the UK has experienced higher and more persistent inflation since the Russian invasion of Ukraine sparked a Europe-wide energy crisis. Annual inflation peaked across advanced economies in 2022, with UK CPI reaching 9.1 per cent, slightly above the 8.8 per cent average for advanced economies. UK inflation has remained elevated since then and is expected to average 3.5 per cent in 2025, 0.9 percentage points higher than the average of advanced economies at 2.6 per cent.

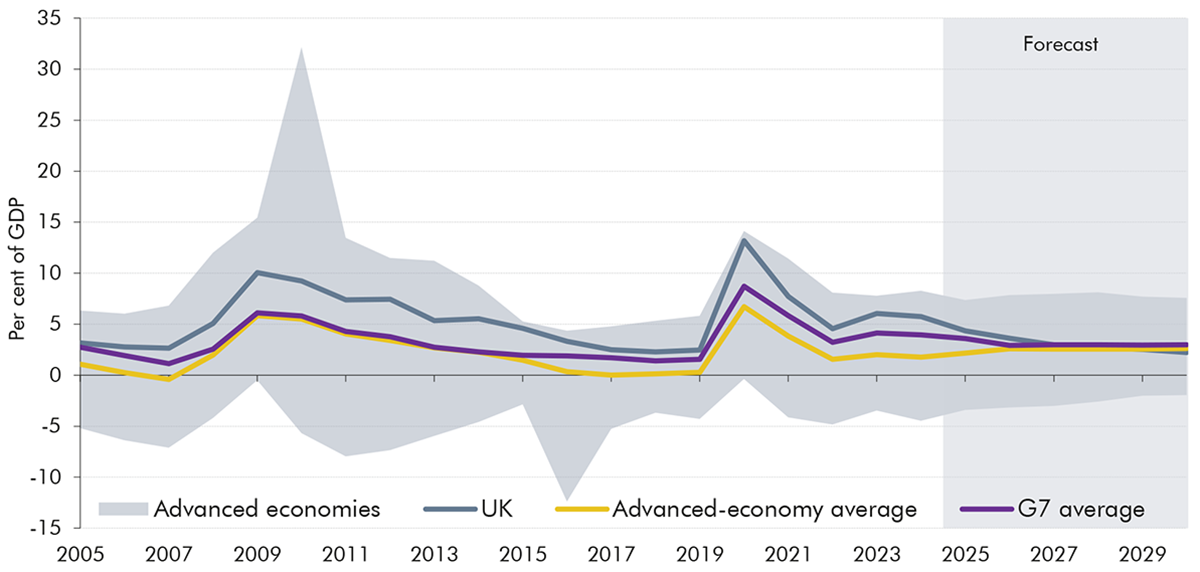

Second, the UK has seen a much larger increase in total government debt and has run more persistent fiscal deficits than other advanced economies. A series of global economic shocks including Covid and the energy crisis have hit the UK particularly hard among advanced economies. Between 2019 and 2024, government debt as a share of GDP rose 18 percentage points in the UK but only 3 percentage points on average among advanced economies. In 2024, the UK government deficit was 5.7 per cent of GDP – the fourth highest among advanced economies, and three times higher than the advanced economy average of 1.8 per cent (see Chapter 6).

Third, the UK has experienced a significant fall in domestic demand for government debt. The decline of defined benefit pension schemes and the Bank of England’s shift from quantitative easing to quantitative tightening have reduced the gilt holdings of pension funds and of the central bank respectively. This has shifted the composition of demand for gilts towards more price-sensitive overseas buyers, as highlighted in our 2025 Fiscal risks and sustainability report (FRS). The FRS analysis found that expected shifts in gilt demand away from domestic pension funds towards overseas and other investors over the next fifty years could push up the overall interest rate on UK government debt by 0.8 percentage points.

Chart 2.2: International comparison of 10-year government bond yields

Note: Andorra, Iceland, Estonia, and Latvia are excluded from this chart due to lack of available time series data. As noted in the text, Iceland has higher borrowing costs than the UK, with its 10-year government bond yield at 6.5 per cent as of 19 November.

Source: Haver Analytics, OBR

Equity prices

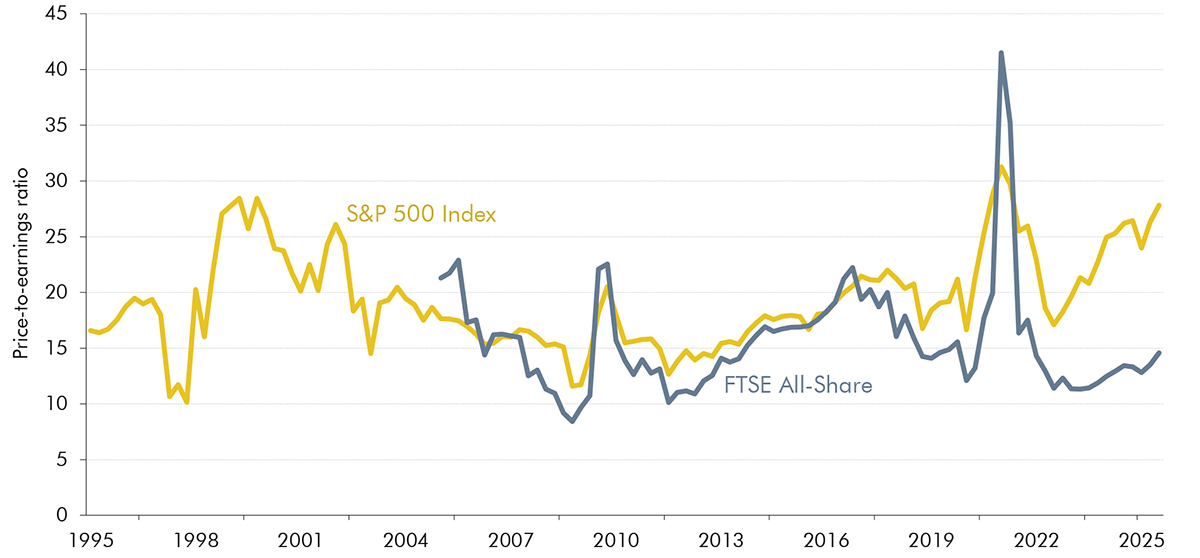

2.8 Equity prices, measured by the FTSE All-Share index, rose 10 per cent in the first three quarters of 2025. We assume equity prices grow in line with nominal GDP over the forecast period, leaving them 4 per cent higher on average than in our March forecast.

2.9 Growth in global equity prices, driven by US equities, has outpaced growth in corporate earnings so far this year, with the S&P 500 price-to-earnings (P/E) ratio reaching 28 in the third quarter. This level has only been reached twice this century: during the dotcom bubble in the early 2000s and the post-pandemic rally in 2021, both of which were followed by a fall in equity prices (of around 46 per cent and 25 per cent, respectively). UK P/E ratios appear to be closer to historic averages, with the P/E ratio of the FTSE All-Share index at 15 in the third quarter, just under its post-2010 average of 16. However, global equity markets are highly correlated, particularly during periods of stress, and the IMF’s October 2025 World Economic Outlook (WEO) highlights the risk of a price correction to US equities, which could have a negative impact on UK equities. While market turbulence is hard to anticipate, a large global equity price correction poses a downside risk to both our economy and fiscal forecast. We explore the potential impact of a fall in global equity prices in Chapter 7.

Chart 2.3: S&P 500 and FTSE All-Share price-to-earnings ratio

Note: Bloomberg calculations. The FTSE All-Share P/E ratio is calculated as last price divided by the trailing 12-month earnings per share before ‘nonrecurring items’. The S&P 500 P/E ratio is calculated as last price divided by the trailing 12-month diluted earnings per share. The two series are not directly comparable and are used to make within-series comparisons over time.

Source: Bloomberg

Energy prices

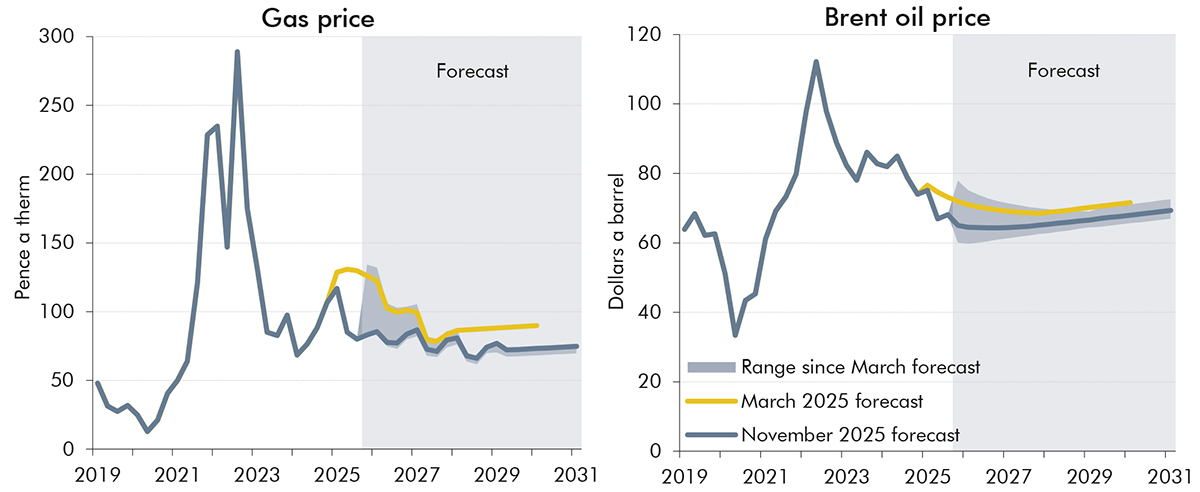

2.10 Market expectations for energy prices have fallen since March, particularly in the near term. Wholesale gas prices average 78 pence a therm across the forecast, almost 20 per cent lower than in March (Chart 2.4, left panel). Brent oil prices average 67 dollars a barrel, 6 per cent below March values (Chart 2.4, right panel). Electricity prices average 76 pence per megawatt hour, 7 per cent below March values.

Chart 2.4: Gas and oil prices

Source: LSEG Workspace, OBR

World economy, trade, and the exchange rate

2.11 Our forecast for the world economy is based on the IMF’s October 2025 WEO. Global GDP is forecast to grow 3.2 and 3.1 per cent in 2025 and 2026, respectively. This is 0.1 and 0.2 percentage points lower than our March forecast, which did not fully incorporate early developments in US and global trade policy. The IMF’s latest WEO includes trade policy up to the start of September, at which point the US’s weighted average statutory tariff rate levied on all trading partners stood at around 19 per cent, 16 percentage points higher than at the end of 2024. The IMF expects these higher barriers to trade to weigh on global growth, though it notes the world economy has proven more resilient than expected to date.

2.12 We expect global trade growth to slow from 3.7 per cent in 2024 to 2.3 per cent in 2026, broadly in line with the IMF’s forecast. Growth in 2026 is 1.0 percentage point lower than in March, and an average of 0.2 percentage points lower over the rest of the forecast. Global trade intensity declines over the medium term from 57.2 per cent in 2023 to 53.6 per cent in 2030. Compared to our March forecast, growth in UK export markets is 0.7 percentage points higher in 2025, as foreign importers brought activity forward to avoid higher tariffs, but averages 0.2 percentage points lower over the rest of the forecast.

2.13 The trade-weighted sterling effective exchange rate has strengthened by around 1 per cent since our March forecast. While the pound has appreciated against the dollar by around 8 per cent, it has depreciated against the euro by around 4 per cent.

Fiscal policy

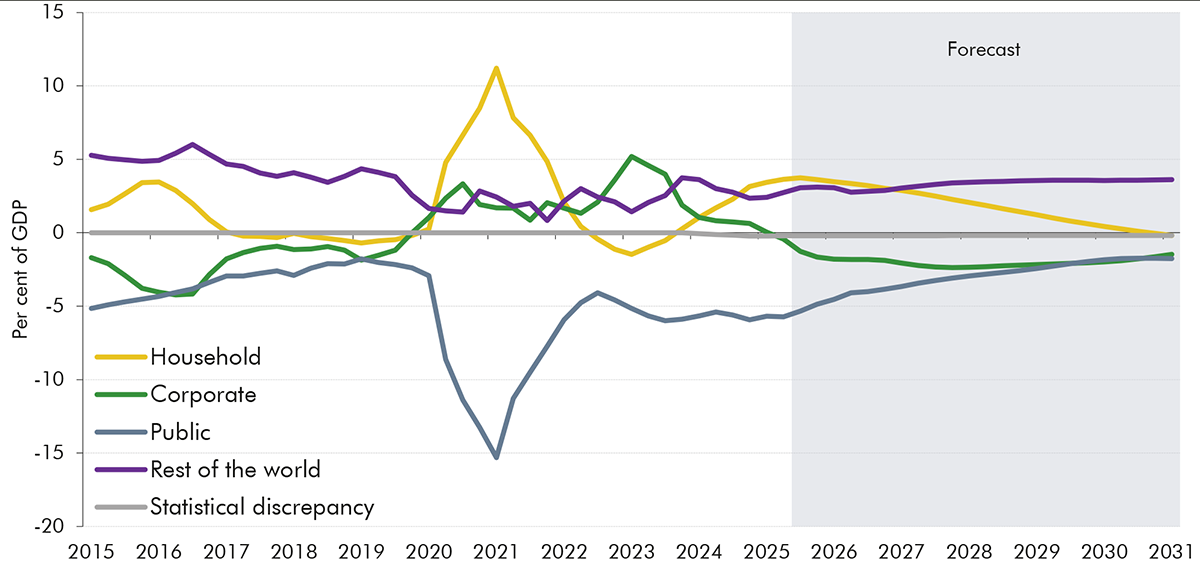

2.14 Compared to our March forecast, public sector net borrowing is higher as share of GDP in most years of the forecast. It is projected to fall from around 5 per cent of GDP in 2024-25 to a little under 2 per cent of GDP by 2030-31. The primary balance (public sector non-interest revenue minus non-interest expenditure) moves from a deficit of around 2¼ per cent of GDP to a surplus of around 1¼ per cent of GDP over the same period. As set out in Chapter 6, the borrowing reduction over the forecast is driven mainly by an increase in tax as a share of GDP, while public spending also declines slightly as a share of GDP.

2.15 Policy measures in this Budget increase borrowing in the near term, mainly through increases to spending, and then reduce borrowing in the medium term primarily through increases to taxation. This means that, relative to March, the fiscal consolidation starts from a higher borrowing level and is more backloaded, with measures pushing a greater share of the consolidation later in the forecast, to 2028-29 and 2029-30. The measures temporarily raise aggregate demand and our central estimate of the real GDP level by 0.1 percentage point in 2026-27 but have no lasting impact on the level of GDP by 2030-31. This is discussed in more detail in Chapter 3.

Potential output, productivity, and labour supply

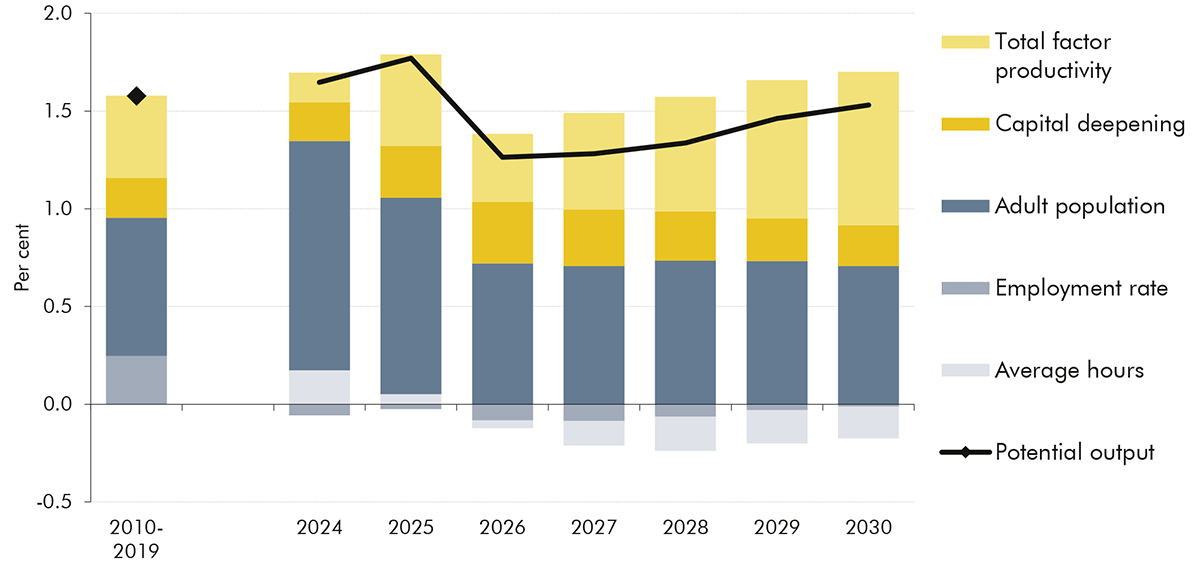

2.16 In our central forecast, potential output growth in 2029 is 0.3 percentage points lower than in March, at 1.5 per cent. This reflects a reduction in our forecast of underlying medium-term total factor productivity (TFP) growth from 1.1 per cent in March to 0.8 per cent in this forecast. Our forecasts for capital deepening and labour supply growth in 2029 are broadly unchanged at 0.2 and 0.5 per cent respectively. We set out the reasoning for, and analysis behind, our new productivity assumption in Briefing paper No. 9: Forecasting productivity, published alongside this EFO and summarised in Box 2.1.

2.17 Our central forecast sees potential output growth slow from 1.8 per cent in 2025 to 1.3 per cent in 2026, before picking up to 1.5 per cent by 2030 (Chart 2.5). The slowdown next year partly reflects a further fall in levels of net migration, which affects labour supply and aggregate output but has a much smaller impact on output per person. Potential output growth picks up over the rest of the forecast thanks to a recovery in TFP growth, which rises from 0.3 per cent in 2026 to 0.8 per cent in 2030.

Chart 2.5: Potential output growth

Source: ONS, OBR

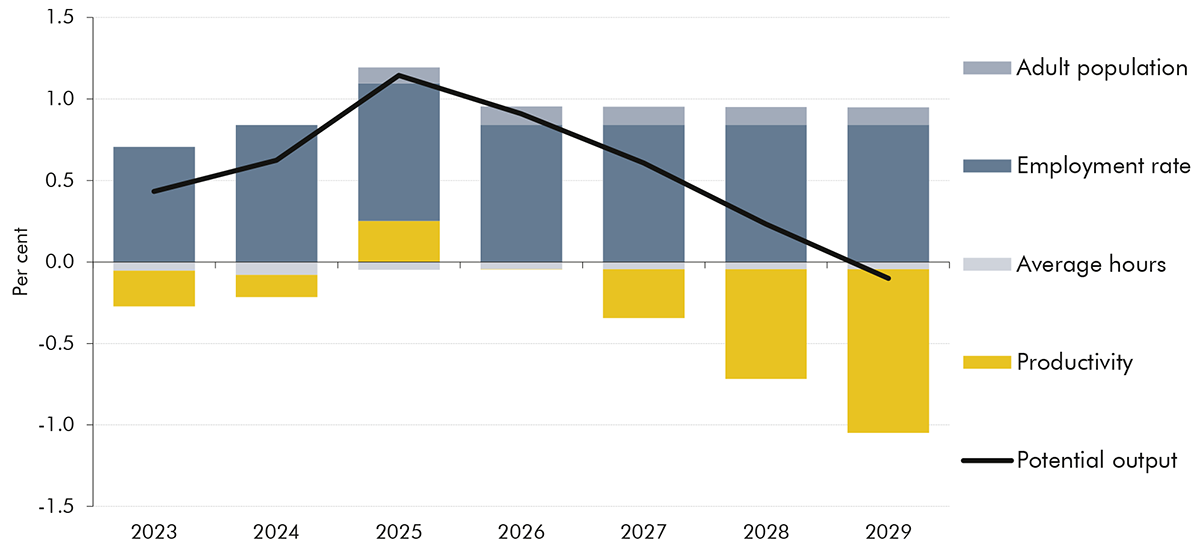

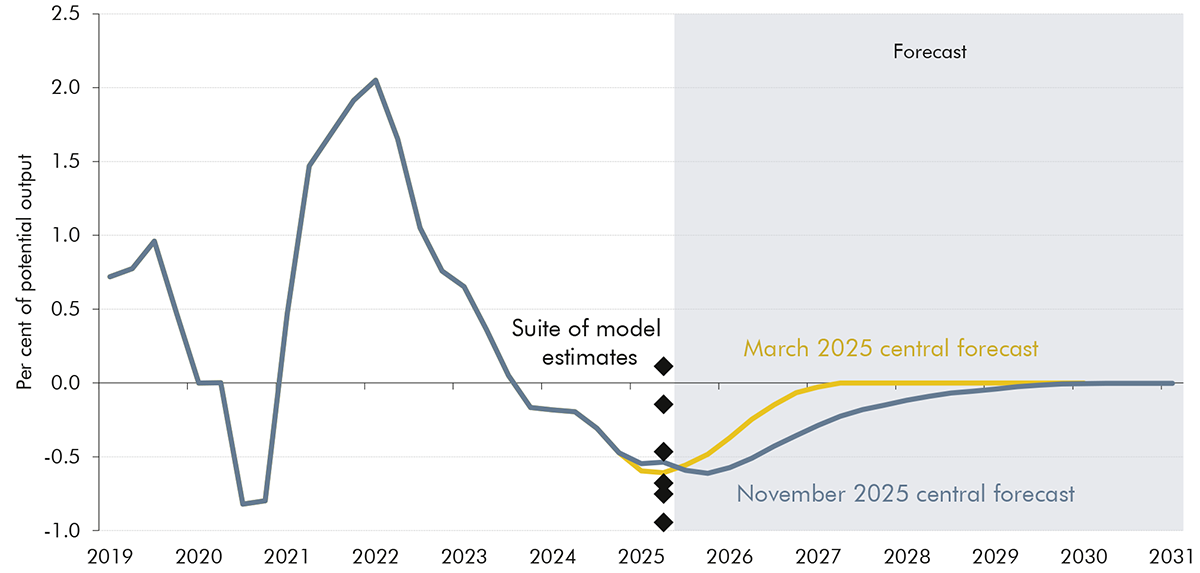

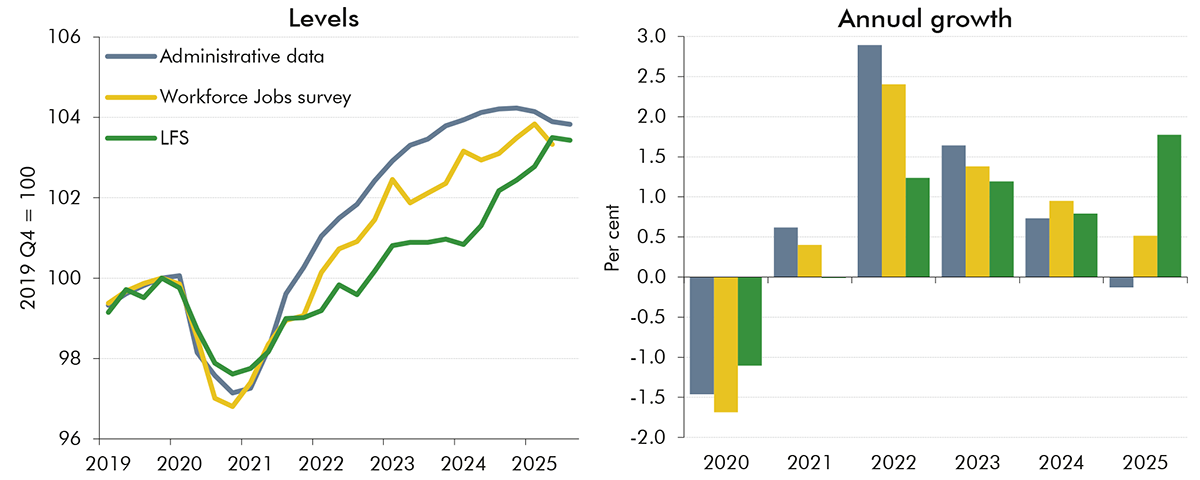

2.18 The central estimate of the level of potential output in 2029 is broadly unchanged from March, as weaker growth over the forecast is offset by a higher starting point. Historical revisions to ONS data left our estimate of potential output in 2024 0.6 per cent higher than in March. Alongside stronger-than-expected real GDP outturns in the first half of 2025 and a little-changed output gap, this means we expect the level of potential output to be 1.1 per cent higher in 2025 than we projected in March. Much of the upward revision to the starting level of potential output is due to our higher estimate for the historical trend employment rate, as the ONS measure of actual employment was 60.9 per cent in the middle of 2025, 0.4 percentage points higher than we projected in March. Slower growth in productivity over the forecast period then brings the level of potential output back into line with our March forecast by 2029 (Chart 2.6).

Chart 2.6: Level of potential output: changes since March

Source: ONS, OBR

Productivity

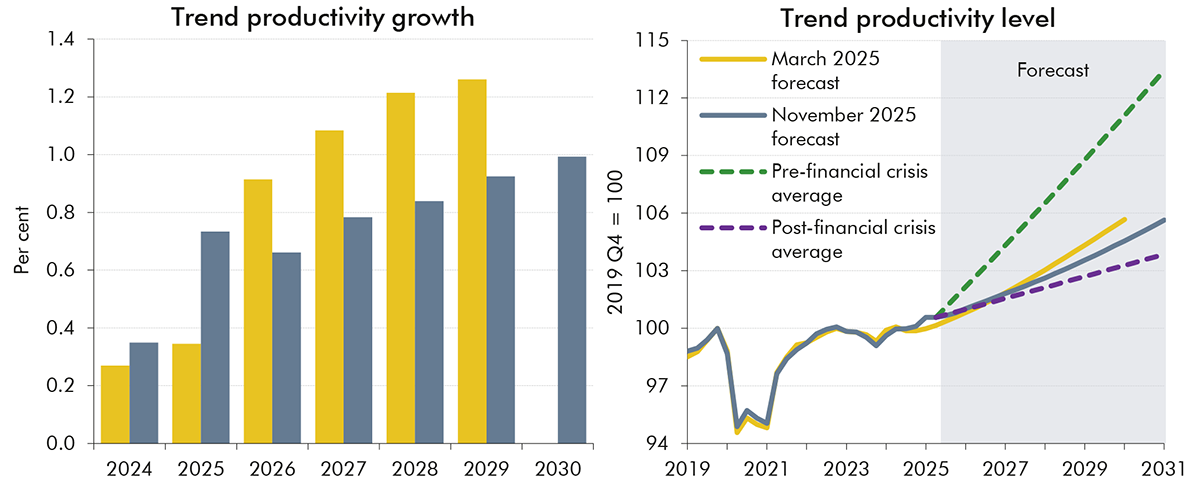

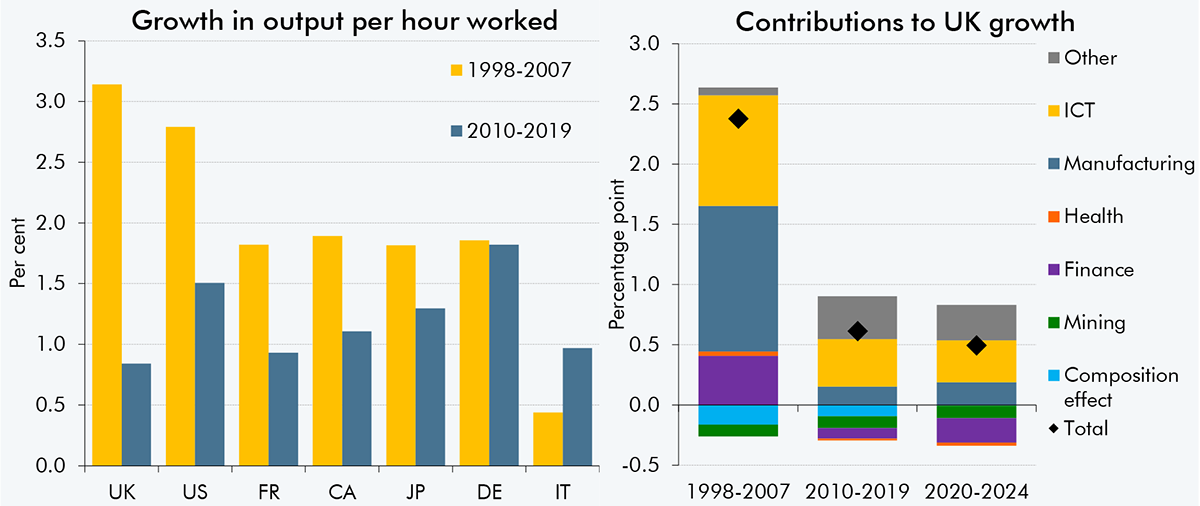

2.19 Our central forecast for trend productivity growth now rises from 0.3 per cent in 2024 and 0.7 per cent in 2025 to reach our revised medium-term assumption of 1.0 per cent in 2030 (Chart 2.7, left panel). The pick-up in productivity growth over the forecast period is based on judgements about the effect that the fading of some past negative shocks, the impact of artificial intelligence technology, and a boost from planning reforms announced in March 2025 have on TFP growth. The contribution of capital deepening is expected to be broadly flat. Our medium-term assumption for trend productivity growth of 1.0 per cent is significantly lower than the pre-financial crisis decade (1998-2007) average of 2.1 per cent but higher than the post-financial crisis decade (2010-2019) average of 0.6 per cent.

Chart 2.7: Trend productivity

Note: Pre-financial crisis average uses mean growth between 1998 and 2007. Post-financial crisis average uses mean growth between 2010 and 2019.

Source: ONS, OBR

2.20 Productivity growth is inherently difficult to forecast, and the outlook is subject to significant uncertainty. Differences across data sets remain a key challenge, with sizeable ONS revisions to both the numerator (real GDP) and the denominator (total hours worked) in recent years. Box 2.1 sets out our revised central judgement for medium-term trend productivity growth, alongside plausible upside and downside scenarios. The fiscal implications of these alternative productivity scenarios are discussed in Chapter 7.

Box 2.1: Forecasting productivity

The likely rate of productivity growth is one of the most important judgements in our economic and fiscal forecasts. Alongside this EFO, we have published Briefing paper No.9: Forecasting productivity, which sets out our latest view of trend productivity growth. This box sets out key findings from the paper and scenarios for future productivity growth.

We have revised down our central estimate of underlying medium-term productivity growth from 1.3 per cent to 1.0 per cent in this forecast. This judgement is based on assessments of:

the UK’s productivity performance over long periods, alongside comparisons with other major advanced economies;

what successive vintages of official output and labour force data imply about underlying productivity and the impact of economic shocks in recent years; and

structural changes affecting the UK’s past and future productive potential, including developments in global trade policy, shifts in the composition of output, and underlying trends including the rise of artificial intelligence (AI).

Historically, there have been points when the trajectory of productivity growth changes across eras, while sudden rises or falls are typically followed by some reversion to that era’s trajectory. It is easier to identify these eras looking backward than to characterise current or future growth.

UK productivity growth has clearly been much lower since 2008. Annual productivity growth, defined as real GDP growth per hour worked for the whole economy, averaged 2.1 per cent between 1998 and 2007, 0.6 per cent from 2010 to 2019, and 0.4 per cent from 2020 to 2024. The productivity slowdown has been global, but the UK has seen the largest fall in the G7 (Chart A, left panel). We have previously made downward revisions to our trend productivity forecast in response to shocks and the period of persistently weak productivity growth since 2008. The 0.3 percentage point revision we have made to medium-term productivity growth is significant, though not as large as the 0.5 percentage point revision we made in November 2017. Looking at previous forecast changes in five-year cumulative trend productivity growth, there are five other forecasts where we have made downward revisions of a similar or larger magnitude to the one in this forecast.

Chart A: Productivity growth averages before and after the financial crisis

Note: The left chart uses data from EUKLEMS & INTANProd for comparability across countries. This covers market sectors excluding agriculture, except in Canada and Japan, which use the whole market sector. In the right chart, productivity is gross value added per hour worked for sectoral analysis. We chose 1998-2007 and 2010-2019 to cover a decade before and after the financial crisis.

Source: EUKLEMS & INTANProd, ONS, OBR

The latest downward revision to our central productivity growth forecast partly reflects updated ONS estimates for the path of output and hours worked. Based on earlier vintages of data, measured productivity growth after the pandemic appeared to be rising toward our previous medium-term trend assumption that TFP growth would return to halfway between its pre- and post-financial crisis averages. But the productivity picture has become somewhat clearer, though not stronger, more recently. According to Labour Force Survey (LFS)-based ONS data, average annual growth in GDP per hour worked between the second quarter of 2023 and the second quarter of 2025 averaged -0.5 per cent. Alternative productivity estimates, which account for the sample bias in the LFS by using wider labour market evidence, suggest average productivity growth over this period was positive though no stronger than in the 2010-2019 period.a

Therefore, on a range of measures productivity growth has remained tepid, several years on from the shocks of Covid and the energy crisis, and a decade-and-a-half from the financial crisis. This ongoing weakness makes it less likely that a substantial and rapid productivity growth rebound, as seen after previous shocks, will now materialise as the Covid and energy price shocks retreat into history. Rather, it suggests persistent weakness in productivity growth relative to the pre-financial crisis period is more likely to reflect underlying structural trends. In particular:

UK and global productivity growth between the early 1990s and mid-2000s was likely boosted by rapid increases in trade as a share of GDP. UK trade intensity has stagnated since 2008, and we expect it to fall in the coming years due to the recent resurgence in global protectionism on top of the enduring effects of Brexit. This is set to weigh on productivity growth for the reasons set in in Annex C of the briefing paper.

Sectoral factors in the UK economy are also likely to continue to drag on productivity growth (Chart A, right panel). Falling contributions from the previously more productive finance, manufacturing, and information and communications technologies (ICT) sectors since the mid-2000s are unlikely to reverse in the coming years or be offset by a rebound in productivity in other sectors. Our analysis suggests AI will likely provide a smaller boost to productivity growth over the next five years than the ICT revolution did before 2008.

Other underlying trends should also weigh on productivity growth, including increased employment in the relatively less productive health and social work sectors as the population ages, slowing growth in the number of people entering higher education, and the negative impacts of climate change and the near-term costs of the net zero transition.

We nonetheless still expect productivity growth to rise from its recently depressed rate over the forecast. This acceleration over the medium term reflects our judgement that:

Part of the recent weakness is from temporary factors arising from the major shocks the UK economy has experienced over the past 15 years. As the lingering effects of these fade, we continue to expect productivity growth to pick up, but less sharply than before.

We also expect AI to begin having a positive effect on productivity growth within the forecast period. There is significant uncertainty around both the size and timing of this effect. Our central estimate is that it will build over time as adoption grows to reach an estimated 0.2 percentage points by our five-year forecast horizon. The productivity impact of AI beyond that point could be larger, as explored in Annex B of the briefing paper.

The downward revision to our medium-term productivity growth estimate takes it closer to those of other forecasters, both for the UK and peer countries. Our November 2025 forecast of 1.0 per cent medium-term productivity growth is at the top end of the range of external forecasts for the UK, where several other forecasts cluster including the Bank of England, IMF, and NIESR. It also is in the middle of the range of official forecasts for comparable countries.

While productivity growth is one of our most impactful forecast variables for the public finances, it is also one of the most uncertain. To illustrate uncertainty around this central forecast, we present two scenarios. We explore their fiscal implications in Chapter 7.

In our upside scenario, more of the recent weakness in productivity growth was due to temporary shocks, and there is a larger boost from AI, pushing potential productivity growth up to 1.5 per cent in the medium term.

In the downside scenario, productivity growth stays around its post-financial crisis average of 0.5 per cent over the forecast.

Chart B: Trend productivity scenarios

Source: ONS, OBR

a) This measure uses an estimate for employment based the average of three sources: Resolution Foundation estimates which draw on real-time information (RTI) payroll employee and self-employment tax data, the Bank of England’s underlying employment measure, and the Workforce Jobs survey. This is then multiplied by the LFS estimate of average hours worked, adjusted slightly to account for some known LFS-related biases, to derive total hours worked.

Labour supply

2.21 Labour supply growth is expected to slow over the forecast from 1 per cent this year to around ½ a per cent over the medium term. This is broadly unchanged from March, and the slowdown reflects further falls in net migration from historically high levels and the effect of the ageing population on average hours and participation. We have revised up the starting point for labour supply (trend total hours worked), mainly based on a reassessment of historical trend participation following improvements to ONS data which has seen the level recently converge with alternative measures. This leaves the level of labour supply 0.9 per cent higher at the end of the forecast than in March. Personal tax measures announced in this Budget are likely to reduce labour supply, but the estimated effect is below our new significance threshold of a 0.1 per cent change to the level of potential output by the fifth year of the forecast, so we have not explicitly adjusted our forecast for them (see Chapter 3).

Adult population

2.22 The size of the adult population is forecast to rise from 56.2 million in 2025 to 58.3 million in 2030. The Labour Force Survey (LFS) outturn for the adult population in the second quarter of 2025 was 63,000 higher than we expected in March. This difference is largely maintained across our forecast, with the adult population growing at a similar pace to our March forecast, averaging 410,000 more people a year.

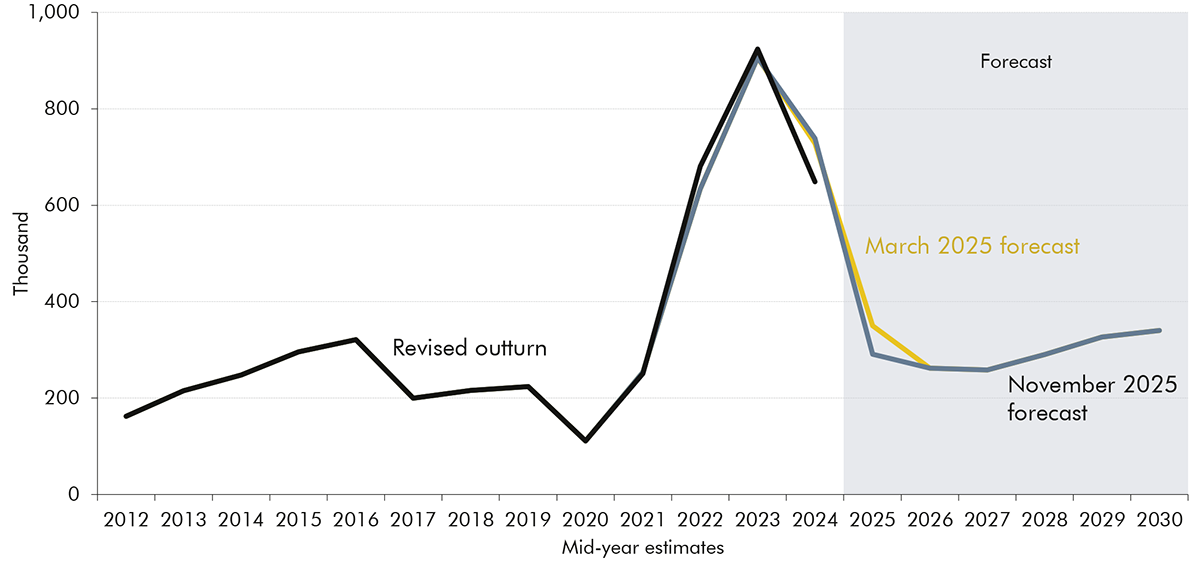

2.23 Net migration has been the main driver of adult population growth in recent years and contributes to around three-quarters of the increase in population across the forecast period. From an estimated record high of 873,000 in 2022, net migration fell back to an estimated 431,000 in 2024, around 25,000 lower than we expected in March. [5] Net migration is expected to fall further to around 262,000 in the year to mid-2026. This is driven by the tightening of visa rules in recent years and a rise in emigration, especially among students, following several years of elevated immigration. Net migration is then projected to rise to reach 340,000 by the end of the forecast, consistent with the ONS ‘migration category variant’ that also underpinned our March forecast. [6]

2.24 Our net migration forecast is unchanged from March, as we judge developments since then are largely offsetting. Our immigration forecast incorporates further reductions due to the Immigration White Paper measures enacted to date, including tighter eligibility requirements for skilled worker visas and the end of the care visa route. But lower emigration over the medium term offsets these effects, as the latest evidence suggests immigrant stay rates in the UK under the new migration system have risen more than we assumed in March. [7], [8]

Chart 2.8: Net migration

Source: ONS, OBR

Participation rate

2.25 The trend labour force participation rate is forecast to gradually fall from 63.5 per cent in 2024 to 63.4 per cent in 2029, similar to our March forecast. Declining participation is driven by an ageing population and rising inactivity due to long-term sickness – the latter is also reflected in our forecast for a rise in incapacity benefits caseloads (see Chapter 5 for more details). [9] These factors are partly offset by three upward pressures on participation: a rise in the state pension age from 66 to 67 between 2026 and 2028; falling birth rates and childcare policy measures lowering inactivity due to childcare; and the continuing inflow of new migrants, who are more likely to be of working age than the domestic population.

2.26 We have revised up our estimate of the starting trend participation and employment rates by 0.5 percentage points in 2024 and 2025, based on the latest ONS data. LFS sample sizes have recovered recently, so we judge the survey is now producing more reliable estimates of employment levels. The latest figures are more consistent with other sources, such as payroll data, as discussed in paragraph 2.37. This means total employment now rises from 33.9 million in 2025 to 35.2 million in 2029, a similar increase to our March projection. We expect trend average hours worked to fall slightly over the forecast, from 32.0 hours in 2025 to 31.8 hours in 2029, broadly unchanged from our March forecast. This steady reduction in average hours worked reflects population ageing, as older people work fewer hours on average.

Real GDP and the output gap

Real GDP

2.27 Real GDP growth in the second half of 2024 was revised up and growth in the first quarter of 2025 surprised on the upside relative to our March forecast, so we have raised our 2025 growth estimate by 0.5 percentage points, to 1.5 per cent. Temporary frontloading of exports and property transactions, ahead of US tariff increases and stamp duty threshold changes respectively, helped boost first-quarter growth to 0.7 per cent. Growth in the second quarter of 2025 slowed to 0.3 per cent as those temporary factors unwound. GDP growth fell further in the third quarter of 2025 to 0.1 per cent, partly due to the shutdown of Jaguar Land Rover operations in September. [10] The second and third quarter figures were a combined 0.4 percentage points below our March forecast. We expect growth to only pick up slightly in the fourth quarter, as business and consumer confidence remain subdued, including in anticipation of further tax rises. The level of GDP in 2024 has been revised up 0.6 per cent since our March forecast, partly due to the Quarterly National Accounts consistent with the Blue Book 2025 (described in more detail in Box 2.2). These together leave the level of real GDP in 2025 1.1 per cent higher than expected in March.

2.28 Subdued growth in the second half of 2025 means we have lowered real GDP growth in 2026 by 0.5 percentage points to 1.4 per cent in our central forecast. It then stabilises at 1.5 per cent a year over the rest of the decade, supported in the near term by a closing negative output gap, aided by loosening monetary policy, and, in the medium term, supported by trend productivity growth rising to its medium-term rate. Compared to March, real GDP growth between 2026 and 2029 averages 0.3 percentage points a year lower. The combination of a higher starting level of GDP and lower growth across the forecast period leaves the level of real GDP in 2029 largely unchanged from our March forecast. The near-term fiscal loosening in this Budget temporarily raises our central estimate of real GDP growth from 1.4 to 1.5 per cent in 2026-27 but has no impact on the level of real GDP by 2030-31.

Chart 2.9: Real GDP

Source: ONS, OBR

2.29 There are significant risks on either side of our central forecast for real GDP growth. Based on the distribution of historical errors around our central forecast, there is a roughly one-in-five chance that 2026 growth will be negative and a similar chance it could exceed 2½ per cent (Chart 2.10). At the forecast horizon, there is a one-in-five chance that growth could be higher than 4¼ per cent or lower than -1¼ per cent. Productivity growth remains one of the largest potential drivers of variance around our central forecast, with the upside and downside scenarios in Box 2.1 corresponding to ½ a percentage point higher and lower real GDP growth in 2030. Significant risks also arise from our conditioning assumptions, notably interest rates, equity prices, and uncertainty around geopolitical tensions and global trade developments (as explored in our July 2022 FRS and March 2025 EFO).