The Government announced substantial reforms to the residential stamp duty land tax (SDLT) system at Autumn Statement 2014. This box explored how the tax system changed and how these reforms were costed.

This box is based on HMRC stamp duty data from November 2014 .

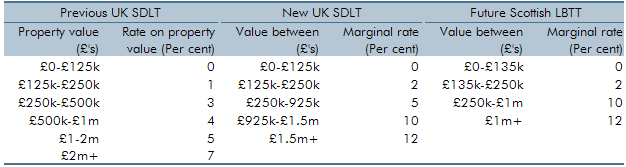

The Government has announced substantial reforms to the residential stamp duty land tax (SDLT) system, which take effect from 4 December across the UK. The measure moves SDLT from a ‘slab’ system (where a single tax rate is paid on the entire purchase price) to a ‘slice’ system (where successive bands of the purchase price are taxed at increasing rates). The Scottish Government had already announced in October that it would move to a slice system for residential and non-residential properties with the introduction of its land and buildings transactions tax (LBTT) next April. This has a different rate schedule to that announced for the UK, with those rates still subject to approval by the Scottish Parliament (see Table C).

Table C: Tax rates under each system

Our pre-measures forecast for this Economic and fiscal outlook is based on the slab SDLT system. Our post-measures forecast for 2014-15 is based on the new slice SDLT system being applied throughout the UK and from 2015-16 it is based on the LBTT system being applied in Scotland and the slice SDLT system in the rest of the UK. This box describes how the effects of these measures on our forecast were costed.a

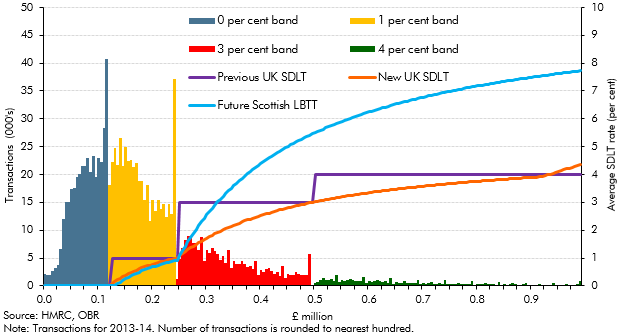

The first step is to establish the tax base – in this case the number and distribution of property transactions in the pre-measures forecast. The next step is to estimate the static or pre-behavioural costing. This simply involves applying the new tax system to the pre-measures tax base. Chart B shows the effective tax rate paid on property transactions at different prices up to £1 million under each system, and the distribution of housing transactions in 2013-14. It underlines the fact that most transactions take place below the £250,000 threshold. If the new regime had been in place in 2013-14 then roughly 2 per cent of transactions would have paid more stamp duty than under the old regime and around 98 per cent the same or less.

Chart B: Average SDLT rates under different transaction tax schedules

The most complex step in most costings is to estimate the behavioural response of taxpayers. The shift from the old slab to the new slice system is expected to prompt a number of responses:

- the slice system removes the cliff edges between tax bands that caused ‘dead zones’ in the price distribution of transactions, whereby very few transactions take place immediately above the thresholds at which the tax liability jumps. That should smooth the distribution of prices, particularly around the £250,000 threshold where many transactions take place, but also at the £500,000, £1 million and £2 million thresholds where fewer transactions take place;

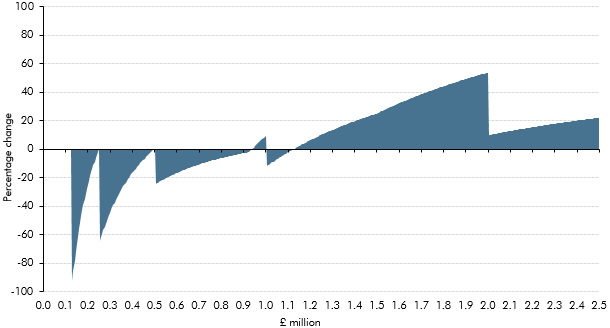

- the future transaction costs associated with selling a house are reflected in the price of the house, so changes in those costs due to the policy will affect house prices. As shown in Chart C, the new system reduces or leaves unchanged SDLT for all residential properties from £125,000 to £935,000 and raises it for most properties above £935,000. So the distribution of house prices will change. (The uneven profile of these changes reflects the cliff edges in the old slab system that the new system is being compared against); and

- SDLT costs affect the frequency of property transactions. For the vast majority of house values where SDLT costs will fall, sales would be expected to be more frequent.

Chart C: Percentage change in tax paid between UK slab and slice SDLT systems

The smoothing of the price distribution was estimated simply by adjusting the distribution of transactions around the slab thresholds to match the distribution elsewhere. (That does not mean an entirely smooth distribution, as transactions tend to cluster at round numbers even when there is no SDLT threshold to induce that effect.)

The effects of changes in transactions costs on house prices and property transactions were factored into the costing using estimates of the relationship between such changes. HMRC produced these estimates, which we certified as reasonable and central:

- for prices, the costing is based on a 1 percentage point change in the average SDLT rate leading to a 1.4 per cent change in the house price. The same elasticity is applied across the price distribution;

- for transactions, the costing assumes that the effect will be different across the price distribution, because each percentage point change in SDLT reflects a different percentage of transaction costs at different prices. The estimates applied range from 3.5 at the bottom of the distribution to 1.5 at the top. Two further adjustments are made: first, to reflect the fact that lower SDLT would allow a purchaser to put more of their savings towards a deposit, enabling more would-be purchasers to meet lenders’ loan-to-value criteria; and second, that higher effective tax rates are likely to encourage efforts to avoid or evade the tax towards the top of the price distribution.

For Scotland, a similar methodology was applied to an estimate of the Scottish tax base and using the differences between the slab SDLT system and the forthcoming LBTT. Because the proposed LBTT rates have been pre-announced, a further adjustment is made to account for behavioural effects on the timing of transactions – some transactions at higher prices will be brought forward to pay the lower UK SDLT rates while some transactions at lower prices will be delayed to benefit from the lower LBTT rates.

The UK costing also includes adjustments to take account of:

- the transitional relief announced by the Government, which means that transactions that have reached exchange of contracts, but have not been completed by 4 December, will be subject to whichever SDLT system is cheapest for the purchaser; and

- a likely temporary increase in error in the initial months of operation, when transactions will be processed manually while IT systems are updated for the new structure.

Elsewhere in our forecast, we need to take into account the effect of the behavioural responses described above on other taxes. We have done so explicitly for inheritance tax and capital gains tax. The net effect on these receipts depends on the price distribution of those properties liable for the tax. These effects have been estimated using HMRC’s tax models.

The overall effect on our forecast of the reforms to SDLT in England, Wales and Northern Ireland is shown in Table D and the introduction of LBTT in Scotland is set out in Table E. As with any policy changes that are expected to generate behavioural responses, these estimates are subject to considerable uncertainty. But we consider these estimates to be reasonable and central, so we have certified the Government’s costing and included the effects in our forecast.

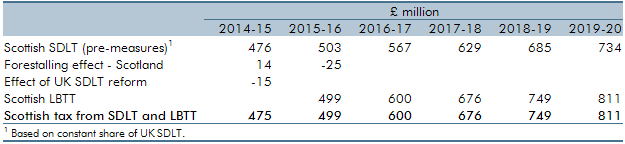

Our forecast for Scottish LBTT in 2015-16 of £499 million is higher than the Scottish Government’s estimate of £441 million. This is despite including forestalling and other behavioural effects, which would reduce expected receipts. A higher forecast would be consistent with the evidence of stronger receipts so far in 2014-15 from the Scottish element of UK SDLT than we expected in March, but such are the uncertainties around all costings of this type that the difference between the two estimates should not be regarded as significant.

Table D: UK SDLT costing

Table E: Scotland LBTT costing