In this box, we discussed the impact that policy changes and announcements since October have on our economy forecast. Specifically, we looked at how the policy package and planning reforms affect real GDP and inflation, before also considering the impact of welfare reforms and its potential future impact.

This box is based on OBR data from March 2025 .

Our economy forecast accounts for the economic impacts of announced government policies. The demand-side effects of fiscal policy are calculated using a set of fiscal ‘multipliers’ which are drawn from empirical literature and reviewed periodically.a These capture the impacts of measures on demand, through changes to private incomes and consumption. We typically assume these effects taper to zero as the Bank of England uses monetary policy to bring the economy back to the trend path of potential supply. The impact of policies on the supply side of the economy is also accounted for if credible evidence suggested that measures will have a significant, additional, and durable impact on potential output.

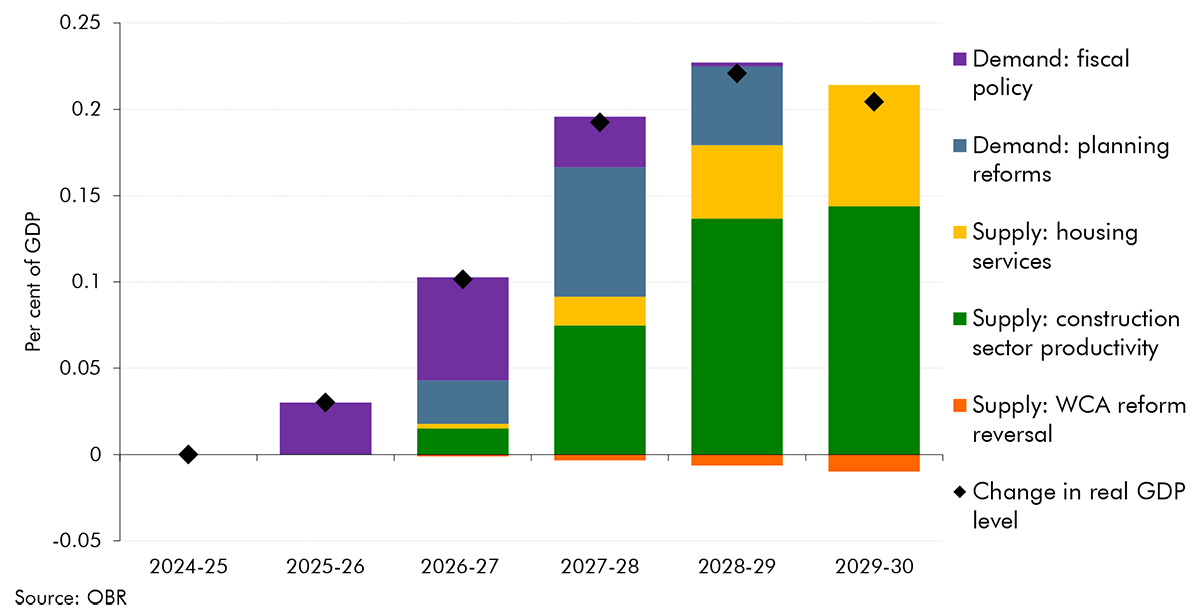

As set out in Table 3.1, the direct effects of the fiscal policies incorporated in this forecast increase borrowing very slightly in 2025-26 before reducing borrowing from 2028-29 onwards. As a result of the reallocation of spending from mainly overseas Official Development Assistance (ODA) to mainly domestic spending on defence, the small near-term demand-side boost to the economy is larger than might otherwise be expected, increasing real GDP by a peak of 0.06 per cent in 2026-27 (Chart A, purple bars).b

As described from paragraph 3.36 of this chapter, we have also incorporated an estimate of the impact of the Government’s residential planning reforms on both supply and demand. We estimate these reforms will increase housebuilding, which leads to a modest temporary boost to demand by raising near-term residential investment (blue bars). In the medium term, these reforms provide a permanent boost to the supply capacity of the economy, via increases in construction sector productivity and the flow of housing services, which reaches 0.2 per cent of GDP in 2029-30 (green and yellow bars).

In this forecast, we have only made one adjustment to the forecast on the supply side of the economy in relation to the welfare reform package announced in the March Pathways to Work Green Paper.c This is the reversal of work capability assessment (WCA) reforms announced by the previous Government in Autumn 2023. As we had previously adjusted the forecast to account for the original policy, we are now reducing labour supply by 8,000 in average-hours equivalent terms to remove its effect. This reduces potential output by 0.01 per cent in 2029-30 (Chart A, orange bars). We have not incorporated the labour supply effects of any other new welfare and employment support measures in our forecast, due to insufficient information on both the specification of policies and their effects in time for us to do so. As discussed in Box 3.2, we will fully assess the employment implications of the wider welfare reform package ahead of our next forecast.

Chart 3A: Real GDP impact of Government decisions

We also expect the policies in this forecast to provide a very small boost to CPI inflation, increasing the price level by less than 0.1 per cent by the end of the forecast.

This box was originally published in Economic and fiscal outlook – March 2025