Our March 2023 fiscal forecast had a difference across other current spending of £14.9 billion, accounting for around 40 per cent of the £39.8 billion overall difference between the March 2023 spending forecast and outturn. This box explored explanations and set out which forecast methodologies we would review as priorities.

This box is based on HMT, ONS, and OBR data from June 2025 .

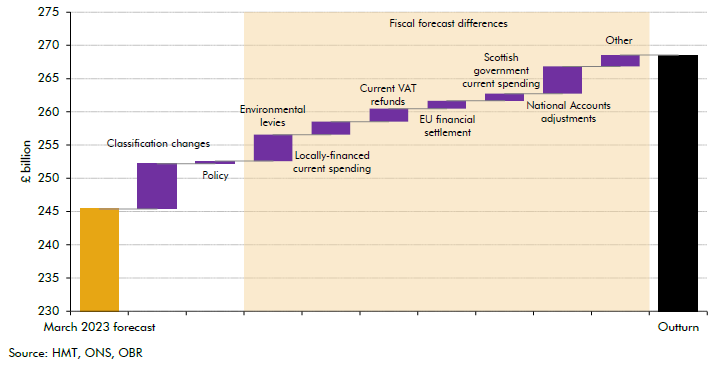

The March 2023 forecast underestimated other current spending in 2023-24 by £23.1 billion. Of this, £7.9 billion reflects classification changes which are neutral for overall spending (see Table 3.10), while £0.4 billion is explained by policy changes to Scottish government spending. However, this leaves a substantial remaining fiscal forecast difference of £14.9 billion, comprising:

- a £2.9 billion underestimate of environmental levies, primarily reflecting lower-than-forecast electricity prices, and a £1.9 billion underestimate of current VAT refunds. Both of these are largely fiscally neutral as they are offset by an equal receipts forecast difference.

- a £1.2 billion underestimate of the EU financial settlement, mostly explained by a change in the timing of payments, and so is partially offset in later years of the forecast.

- a £2.0 billion underestimate of locally financed current spending, most of which (£1.4 billion) is due to higher-than-expected use of reserves by local authorities, and a £1.1 billion underestimate of Scottish government current spending.

- a £4.1 billion underestimate of National Accounts adjustments. These adjustments align the forecasts of spending items as defined in the Treasury’s spending control framework, to the definitions of current and capital expenditure used in the public sector finances.

Initial ONS outturn data also suggests a significant underestimate of £13.3 billion in the March 2024 forecast of other current spending for 2024-25. Revisions to some areas of this outturn data are likely later in the year when additional data on spending and local authority borrowing becomes available. Nonetheless, provisional analysis at this point suggests that the forecast underestimate for this year is concentrated in some similar areas to the 2023-24 forecast underestimate. In particular, against the initial outturn data for 2024-25 there is a £6.1 billion fiscal forecast difference in the National Accounts adjustments forecast, and a £1.2 billion difference in the locally financed current spending forecast. It is also the case that there are initial forecast differences in these areas between the in-year forecast for 2024-25 made in March 2025, and the initial ONS outturn estimates. As a result, we are, as a priority, reviewing the forecast methodologies and data sources used in these areas:

- National Accounts adjustments: we are, with the Treasury, reviewing the methodologies used to produce this forecast including assessing the sources of the residuals between ONS outturn and the Treasury’s estimates of accounting adjustments. The aim is to minimise these residuals so that we have a fuller understanding of each element of the forecast.

- Locally financed spending and local authority net borrowing: we are reviewing these forecasts to further decompose the recent series of underestimates. We have started work with the Treasury and ONS to better understand how the ONS produces estimates of local authority outturn with the aim of better aligning methodologies. We will also consider the scope for improving the supply to the OBR, ONS and the Treasury of in-year data on local authorities.

Chart A: Sources of difference in the March 2023 forecast for other current spending in 2023-24

Chart B: Preliminary analysis of sources of difference in the March 2024 forecast for other current spending in 2024-25

This box was originally published in Forecast evaluation report – July 2025