"It is the duty of the Office to examine and report on the sustainability of the public finances"

Forecast evaluation report – January 2023

Our annual Forecast evaluation report (FER), examines how our forecasts compare to subsequent outturn data and identifies lessons for future forecasts.

This year we assess how our forecasts have performed against outturn for 2021-22 – the year the UK economy started to recover from the pandemic-induced shock of 2020-21.

The Office for Budget Responsibility was created in 2010 to provide independent and authoritative analysis of the UK public finances. Twice a year – at the time of each Budget and Autumn or Spring Statement – we publish a set of forecasts for the economy and public finances over the coming five years in our Economic and fiscal outlook (EFO). We use these forecasts to assess the Government’s progress against its fiscal targets.

In each EFO, we stress the uncertainty that lies around all such forecasts. We compare our central forecasts to those of other forecasters. We highlight the limited confidence that should be placed in our central forecast given the scale of shocks that inevitably drive a wedge between any central predictions and subsequent outcomes. We use sensitivity and scenario analysis to show how the public finances could be affected by alternative economic outcomes. And we highlight the residual uncertainties in the public finances, even if one were confident about the path for the economy – for example, because of uncertain estimates of the cost of policy measures.

Notwithstanding these uncertainties, we believe that it is important to set out our forecast in detail. We also believe that it is important to examine regularly how our forecasts compare to outturn data and to explain any discrepancies so that we can learn from our experience.

Throughout this report, we describe the arithmetic divergence between our central forecasts and the subsequent outturns. To a significant extent these differences between outturns and previous forecasts are inevitable given unforecastable shocks that hit the economy. But some differences are due to genuine errors, which would have been corrected before the forecast was finalised if we had spotted them. When we identify them, we describe them as such. Errors of this sort are inevitable from time to time in a highly disaggregated forecasting exercise like ours.

This year our report analyses our forecasts for 2021-22, focusing mainly on the March 2021 forecast for the year ahead, as the economy and public finances started to recover from the huge pandemic-induced shock that began a year earlier.

We provided a final copy of this report to the Treasury two working days in advance of publication. This timing has been extended to reflect forthcoming changes to our Memorandum of Understanding with HM Treasury and our main forecasting departments.

The Budget Responsibility Committee

Richard Hughes, Professor David Miles CBE and Andy King

Chapter 1: Executive summary

1.1 The focus of this year’s Forecast evaluation report (FER) is the performance of our forecasts for the financial year 2021-22. This was the year in which the economy and public finances began recovering from the historic, pandemic-induced shock that saw output tumble and the deficit soar in 2020-21. The pandemic resulted in record year-ahead differences between our forecast and outturn for GDP growth and borrowing, which we explored in our December 2021 FER. This report therefore focuses on the accuracy of our forecast for the economic recovery from the pandemic and its impact on the public finances in 2021-22.

1.2 Overall, 2021-22 was characterised by a sharp recovery in demand, in the UK and across advanced economies, as vaccines were rolled out and consumers and businesses adapted to the lifting of public health restrictions. But this stronger-than-expected recovery in demand bumped up against domestic and international supply bottlenecks through the autumn and winter, which were compounded by the Russian invasion of Ukraine and associated sharp rise in European gas prices toward the end of the financial year.

1.3 The unexpected strength and speed of the recovery in demand, underestimation of the constraints on supply, and spike in European energy prices meant that we significantly underestimated inflation. Subsequent downward revisions to the level of GDP in 2020-21 mean that we also underestimated real GDP growth in 2021-22 as the economy bounced back from a deeper downturn than previously estimated. The resulting faster-than-expected growth in nominal GDP, coupled with its concentration in tax-rich parts of the income distribution and the economy, explain much of our £108.6 billion overestimate of borrowing in 2021-22 – a difference second only in absolute terms to the £258.0 billion underestimate of borrowing in our March 2020 pre-pandemic forecast for 2020-21.

1.4 The extent of the CPI inflation overshoot in 2021-22 is the largest difference between forecast and outturn since the OBR began forecasting in 2010 – though this record will be beaten again when we come to evaluate our forecasts for 2022-23. CPI inflation was 4.0 per cent in 2021-22, more than double the 1.7 per cent we expected in our March 2021 forecast. This 2.3 percentage point difference can be explained by several factors – some that were unanticipated, and others that proved more acute or long-lasting than expected. It is largely driven by unexpectedly strong rises in the prices of tradable goods due to:

An unexpectedly strong recovery in demand in advanced economies, meaning global GDP growth in 2021 was 0.5 percentage points stronger than forecast.

Persistent supply and logistics bottlenecks, especially in emerging economies in Asia, that struggled to respond to that strong growth in demand. As a result, the prices of tradable goods rose by 3.1 percentage points more than expected in 2021-22, explaining around half of the overall forecast difference for CPI inflation (1.1 out of 2.3 percentage points).

Rising energy costs brought on by surging demand for energy-intensive manufactured goods and later by the Russian invasion of Ukraine. This pushed up energy and fuel price inflation, together explaining around one-third of the overall difference (0.2 and 0.5 percentage points respectively).

A tighter-than-expected domestic labour market in the wake of the pandemic.This led to non-tradables inflation coming in 1.1 percentage points above forecast (explaining 0.2 percentage points of the overall difference).

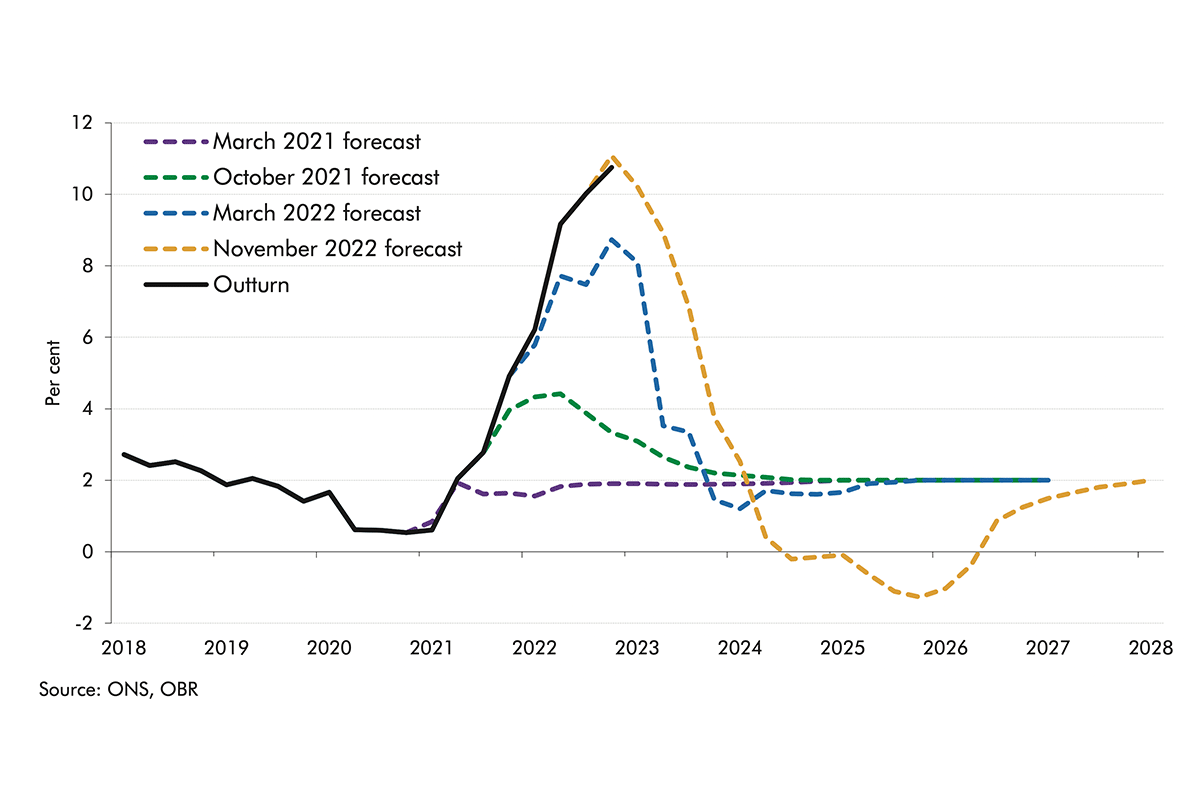

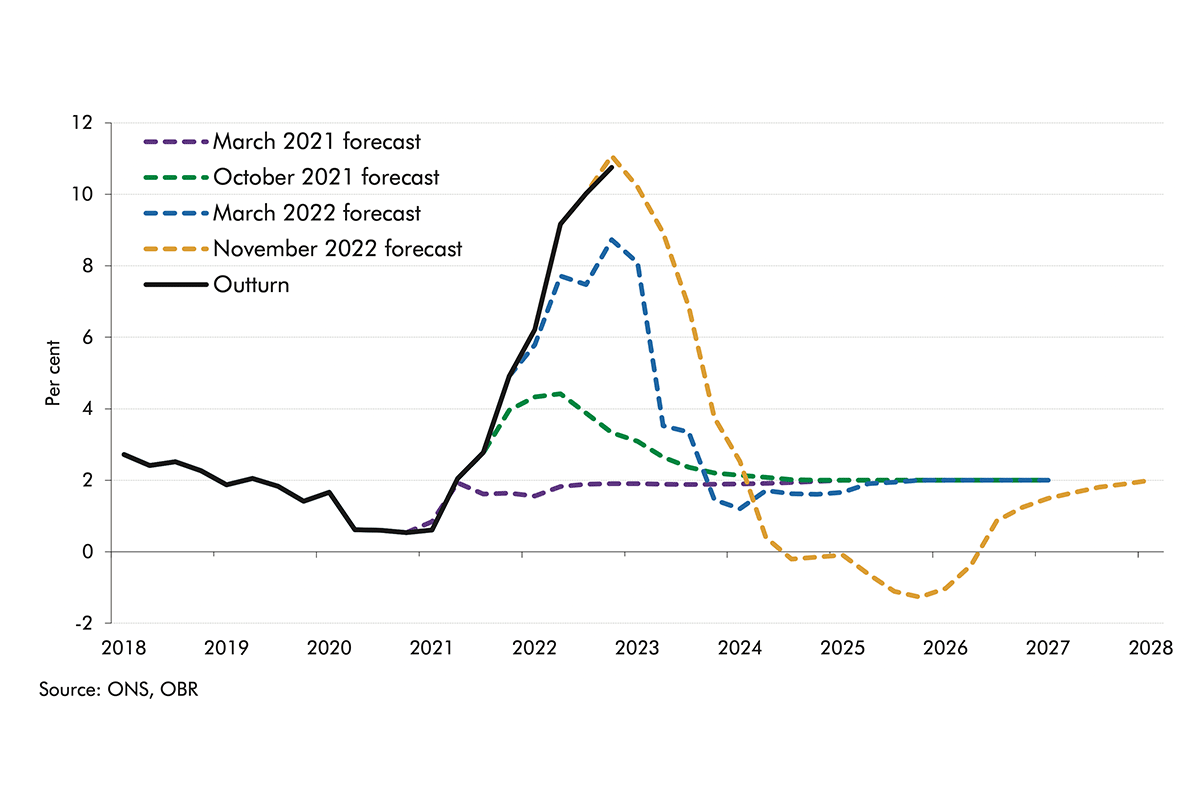

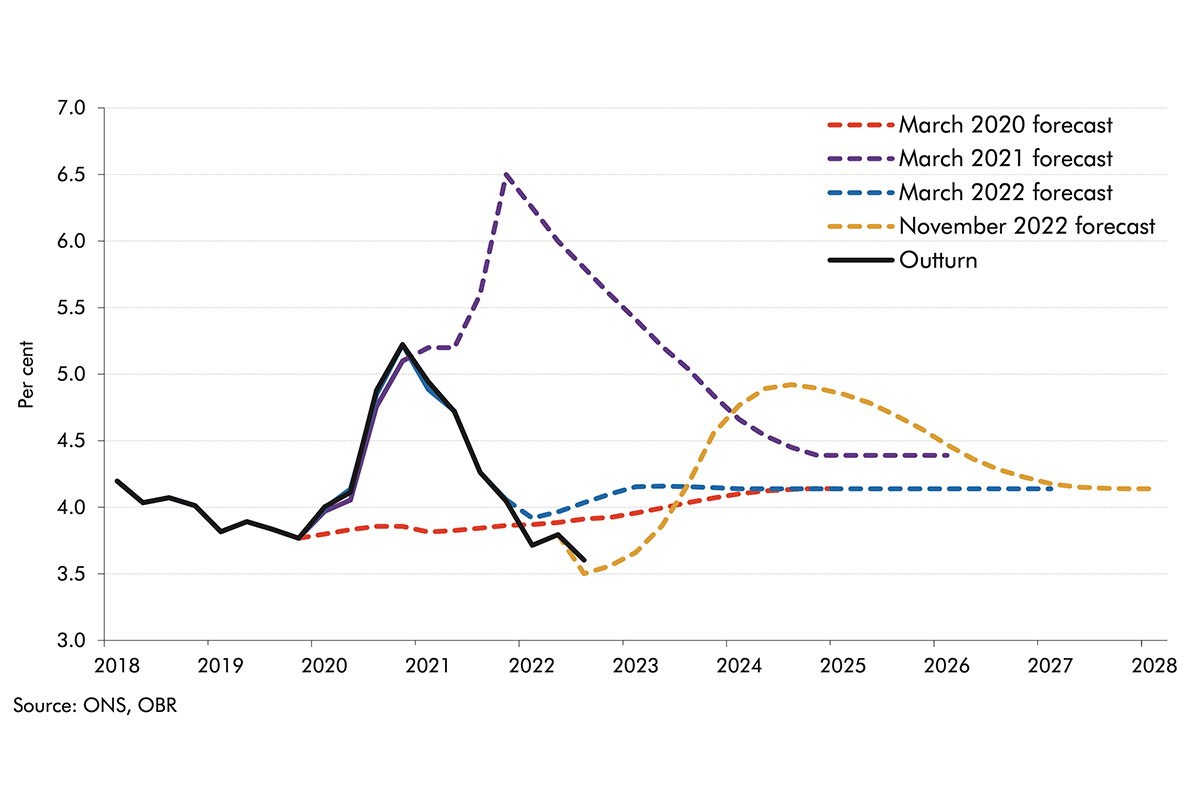

1.5 Since our March 2021 forecast we, and other forecasters, continued to underestimate the strength of CPI inflation in 2022, up until our November 2022 forecast. Inflation was 10.7 per cent in the fourth quarter of 2022, which is 8.8 percentage points higher than our March 2021 forecast. And even our March 2022 forecast, which was completed in the early days of the Russian invasion of Ukraine, underestimated inflation by 2.0 percentage points at the end of last year (Chart 1.1). Our November 2022 forecast was a modest overestimate of 0.3 percentage points. The proximate causes of our repeated underestimate of inflationary pressures were an intensification of the shock to global energy prices, combined with ongoing nominal wage pressures as the domestic labour force contracted by more than we expected while vacancies remained historically high.

Chart 1.1: Successive inflation forecasts

GDP

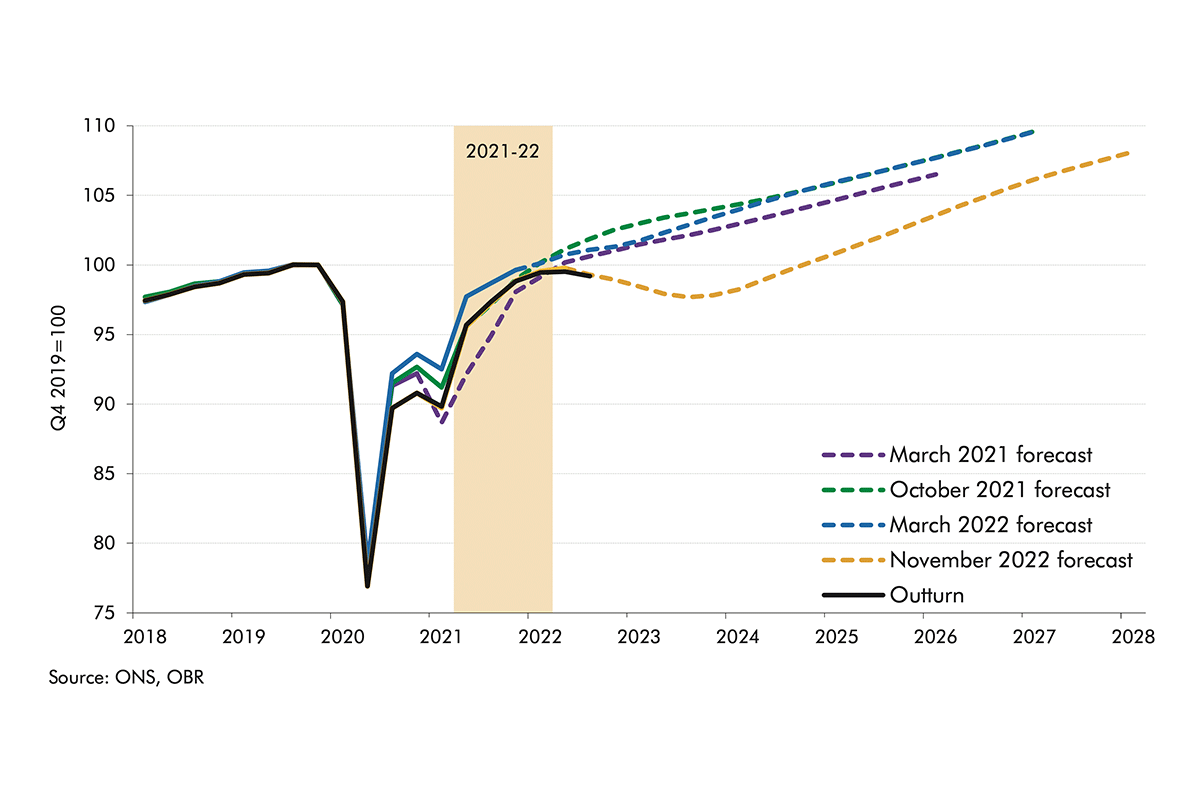

1.6 Despite the hit to real incomes from higher-than-expected inflation, the level of real GDP is broadly in line with our March 2021 forecast by the first quarter of 2022. That forecast anticipated the economy recovering to its pre-pandemic level of output by the middle of 2022, but the latest data suggest that output was still 0.5 per cent below its pre-pandemic peak at that point. The profile of growth was also steeper across the early part of 2021-22 than we expected in March 2021, suggesting an economy that rebounded more quickly following the lifting of the remaining public health restrictions, before slowing as supply bottlenecks and rising energy prices took hold later in the year. Combined with significant subsequent downward revisions to the level of outturn GDP in 2020-21, our March 2021 forecast underestimated real GDP growth in 2021-22 by 3.2 percentage points.

Chart 1.2: Successive forecasts for the level of real GDP

Labour market

1.7 The unexpected strength of the post-pandemic recovery in output can also be partly explained by our assumption that the closure of the furlough scheme would lead to a rise in unemployment to 5.9 per cent in 2021-22. This was not borne out, as the Government’s support schemes proved more successful than we had assumed in preserving viable businesses and protecting employment, and instead unemployment dipped to 4.2 per cent.

1.8 However, the pandemic appears to have had a more adverse effect on levels of inactivity, which has risen by 575,000 since the start of the pandemic, over 100,000 more than expected. The rise in inactivity appears to be driven by a range of factors, including increases in long-term sickness and early retirement. We intend to explore further the latest trends in inactivity in both our next Economic and fiscal outlook and Fiscal risks and sustainability reports. But this adverse news on inactivity has been partly offset by higher levels of net migration than expected (over 500,000 people in the year to June 2022, versus our ONS-based assumption of 150,000 in our March 2021 forecast). The net outcome is that the overall growth of the labour force was 161,000 smaller than we expected.

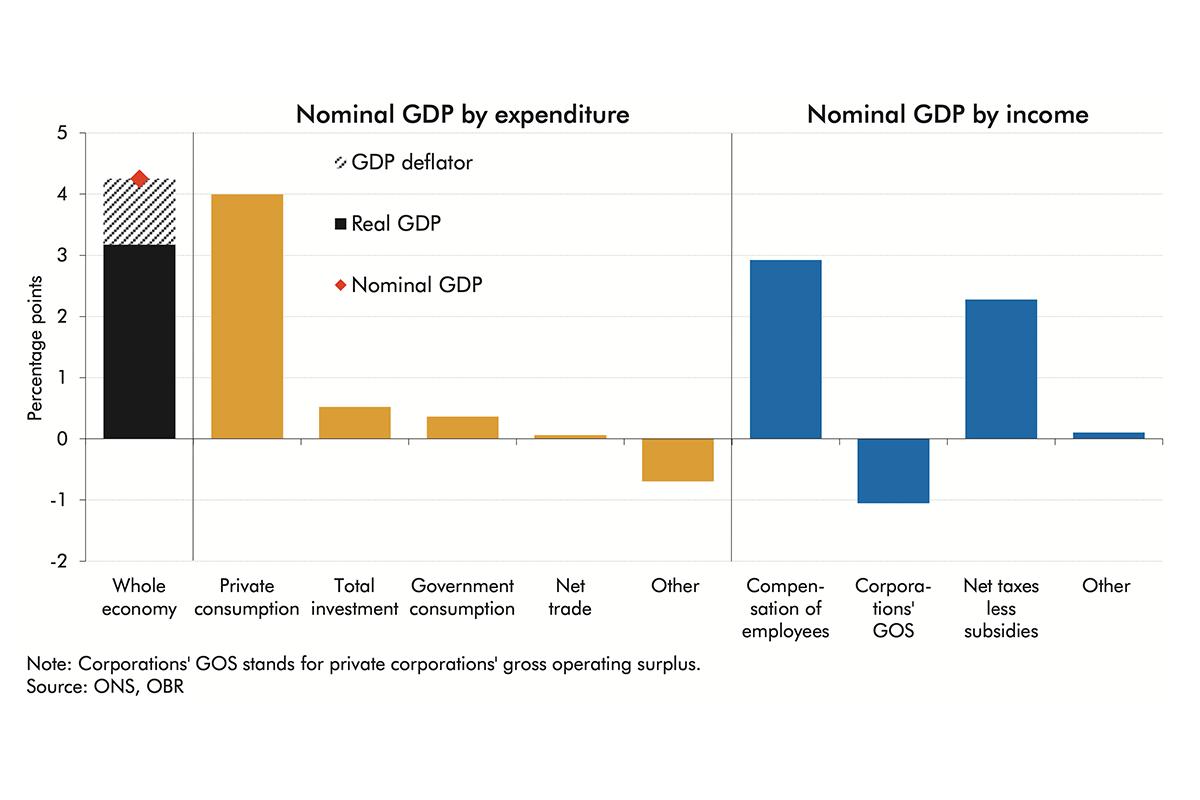

1.9 Our underestimates of both real GDP growth and inflation in 2021-22 combined to drive a 4 percentage point upside surprise (relative to our March 2021 forecast) in nominal GDP growth – more important than real GDP growth for the public finances. Surprises in the composition of nominal GDP, as well as its overall size, also had important fiscal consequences. Chart 1.3 shows that by expenditure component, private consumption explains almost all of the nominal GDP growth underestimate, while on the income side, a tighter-than-expected labour market contributed to a large upside surprise in labour income growth – the largest tax base of all and the most tax-rich component of nominal GDP. Higher tax bases (such as increased VAT receipts from higher consumption growth) supported net taxes and subsidies, offset by lower-than-expected profits.

Chart 1.3: March 2021 forecast differences in contributions to nominal GDP growth in 2021-22

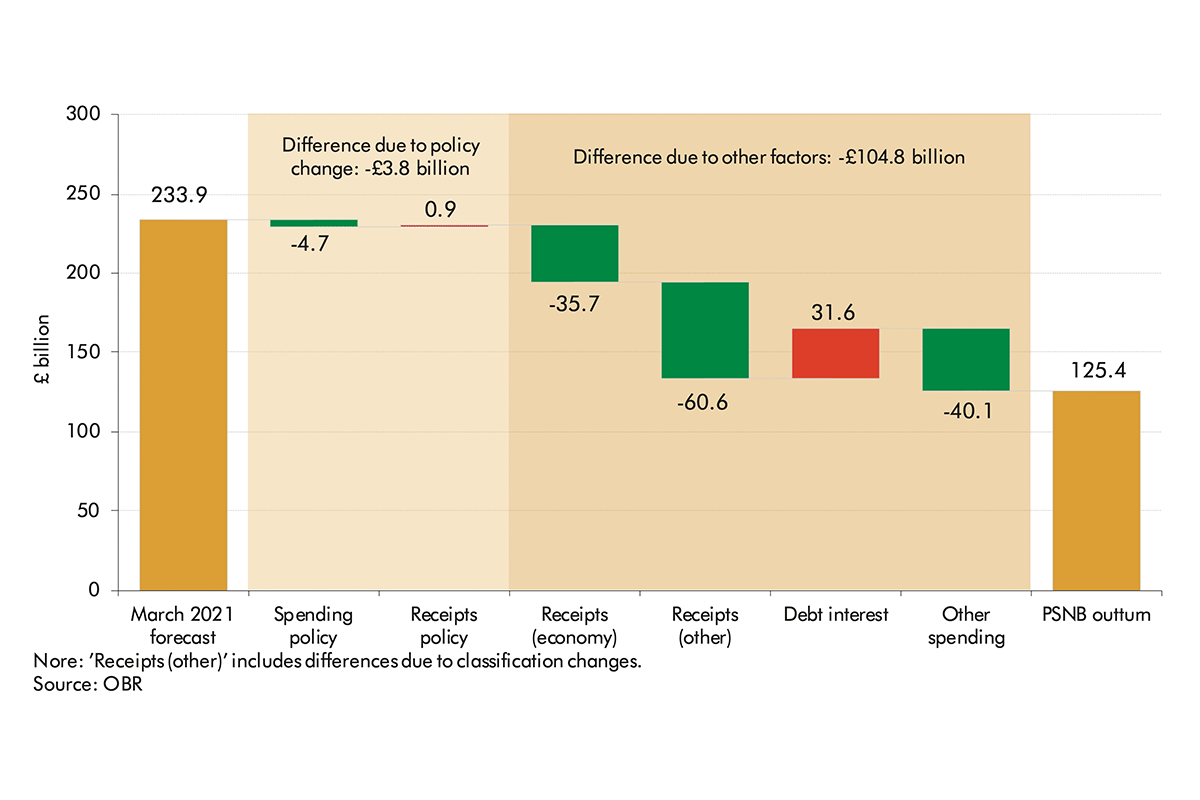

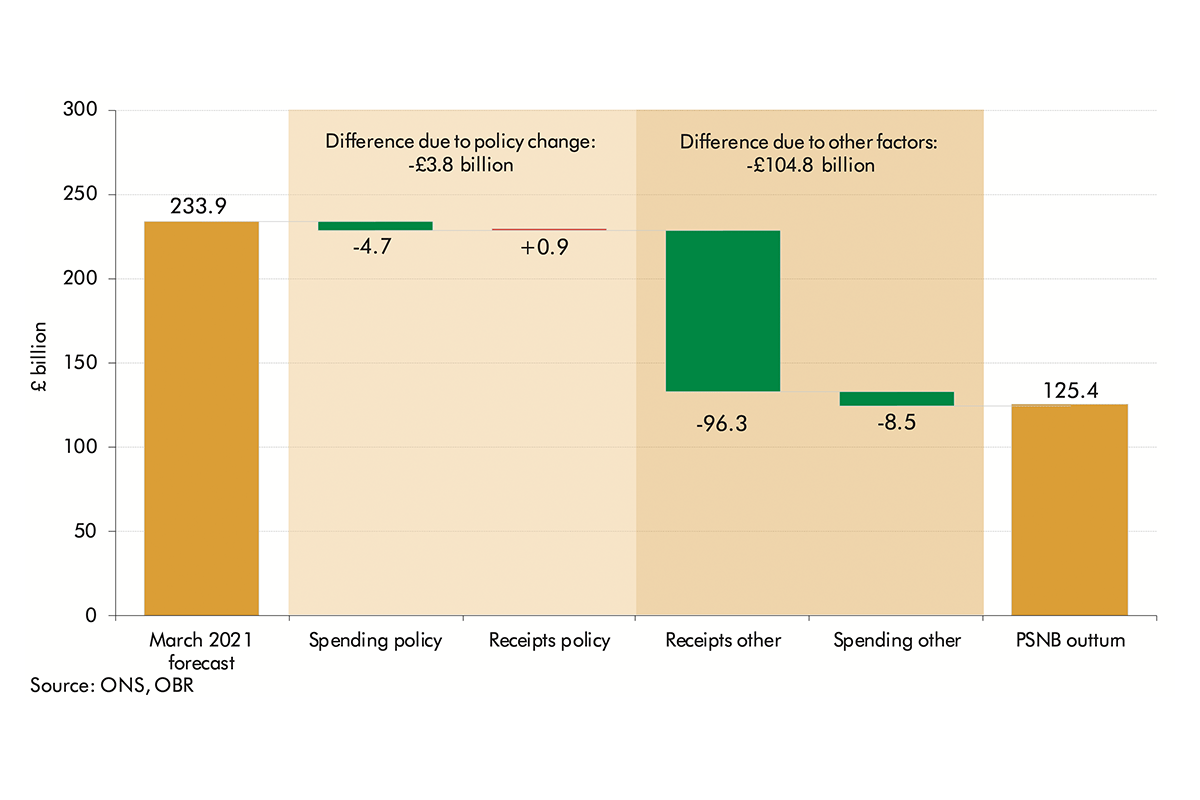

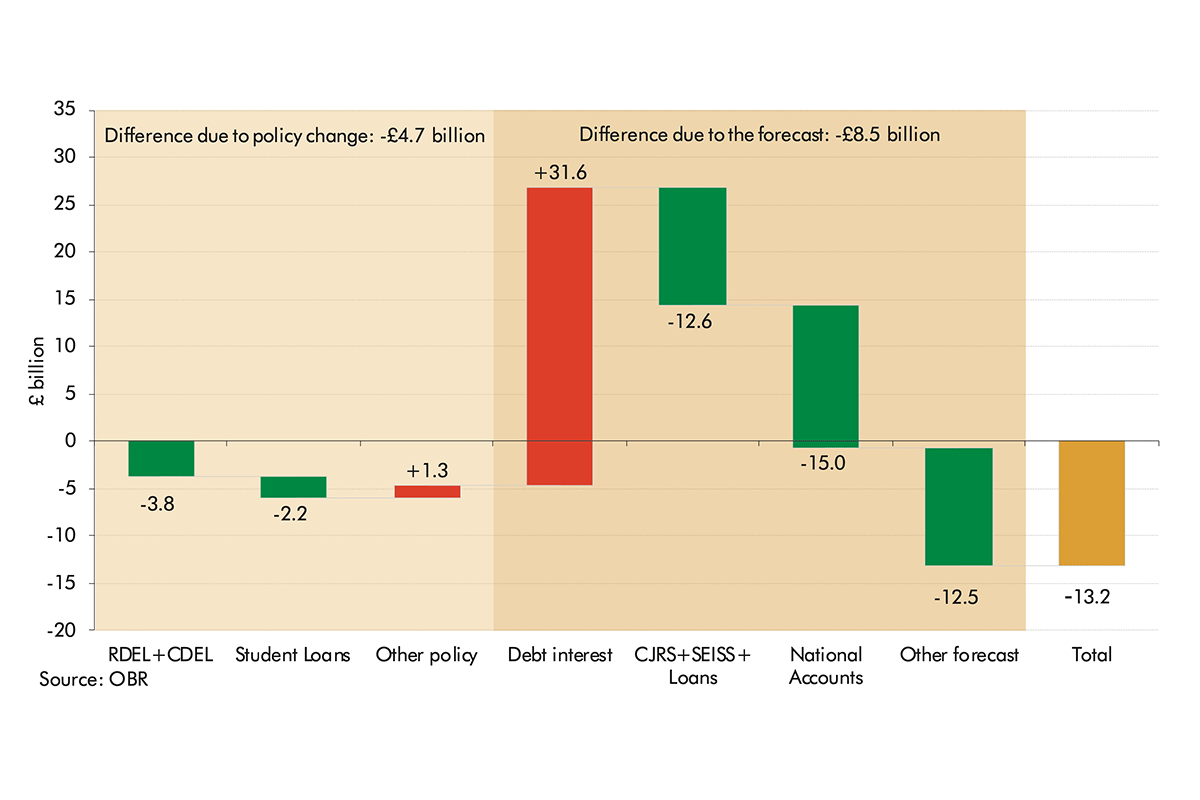

1.10 These nominal GDP surprises provide a partial explanation for government borrowing in 2021-22 coming in £108.6 billion (46.4 per cent) below our March 2021 forecast. Chart 1.4 shows that this overestimate of borrowing was driven by:

A £3.8 billion overestimate of borrowing due to policy changes announced after our March 2021 forecast. This small contribution is more than explained by spending reductions: lower departmental capital spending limits and lower spending on student loans as a result of reforms to terms for new and existing borrowers.

A £35.7 billion upside surprise in receipts due to economic factors, in particular our underestimates of labour income and private consumption, set out above. These are the main tax bases for income tax, NICs and VAT, which together account for £29.8 billion (84 per cent) of the overall surprise in receipts due to economic factors.

A £60.6 billion upside surprise in receipts due to other forecasting differences.[1] Much of this relates to stronger-than-expected fiscal drag bringing more people into more heavily taxed parts of the income distribution, alongside growth being concentrated in tax-rich sectors of the economy, raising effective tax rates for income tax, NICs and corporation tax. Together these taxes account for £37.4 billion (62 per cent) of the overall upside surprise in receipts due to other forecasting differences.

An £8.5 billion overestimate of spending due to forecasting differences. This includes a large £31.6 billion underestimate of debt interest spending, due in particular to much higher-than-forecast RPI inflation, offset by spending in a range of other areas coming in lower than forecast, in particular in respect of pandemic-related income support schemes and loan guarantees, and National Accounts adjustments.

Chart 1.4: Sources of March 2021 borrowing forecast differences for 2021-22

Refining our forecasts

1.11 Previous FERs have identified specific issues with elements of our normal forecasting approach that have caused us to refine and develop particular economic and fiscal forecasting models and techniques. But the challenges for forecasting created by the pandemic – which endured into 2021-22 – have been more fundamental in nature and prompted us to reassess elements of our whole approach. The dramatic rise in energy prices due to the Russian invasion of Ukraine late in 2021-22 underscored and added to many of these challenges, and re-emphasised the core lessons of our December 2021 FER:

The need to be analytically agile, and capable of developing new analytical tools quickly in response to novel shocks. For example, in our July 2022 Fiscal risks and sustainability report we set out a new production function to quantify the effect of energy price rises on the supply potential of the UK economy.

The need to understand and make use of multiple sources of high-frequency, real-time data,such as HMRC’s real-time information from the PAYE system and Google mobility data, to understand the impact of the pandemic, lockdowns, and re-opening on employment, incomes, and consumption.

The need to draw on international experiences and expertise outside of government, for example by asking security and energy experts to help us understand the implications of the Russian invasion of Ukraine for European and UK energy prices.

1.12 On the fiscal side, less than half of our large overestimate of the 2021-22 deficit can be explained by the more rapid economic recovery than we had assumed, with the remaining difference highlighting several fiscal forecasting issues that we have already reflected and acted upon, particularly in our March 2022 Economic and fiscal outlook. In particular:

the unexpectedly strong rise in effective tax rates led us to bolster our analysis of sectoral receipts data and the rich data on the distribution of employee earnings from the PAYE system to inform our in-year receipts estimates; while

the large changes in departmental spending allocations during the pandemic have prompted us to expand the range of data sources we use when making judgements about the extent to which spending limits set by the Treasury will be underspent.

Comparison with past official forecasts

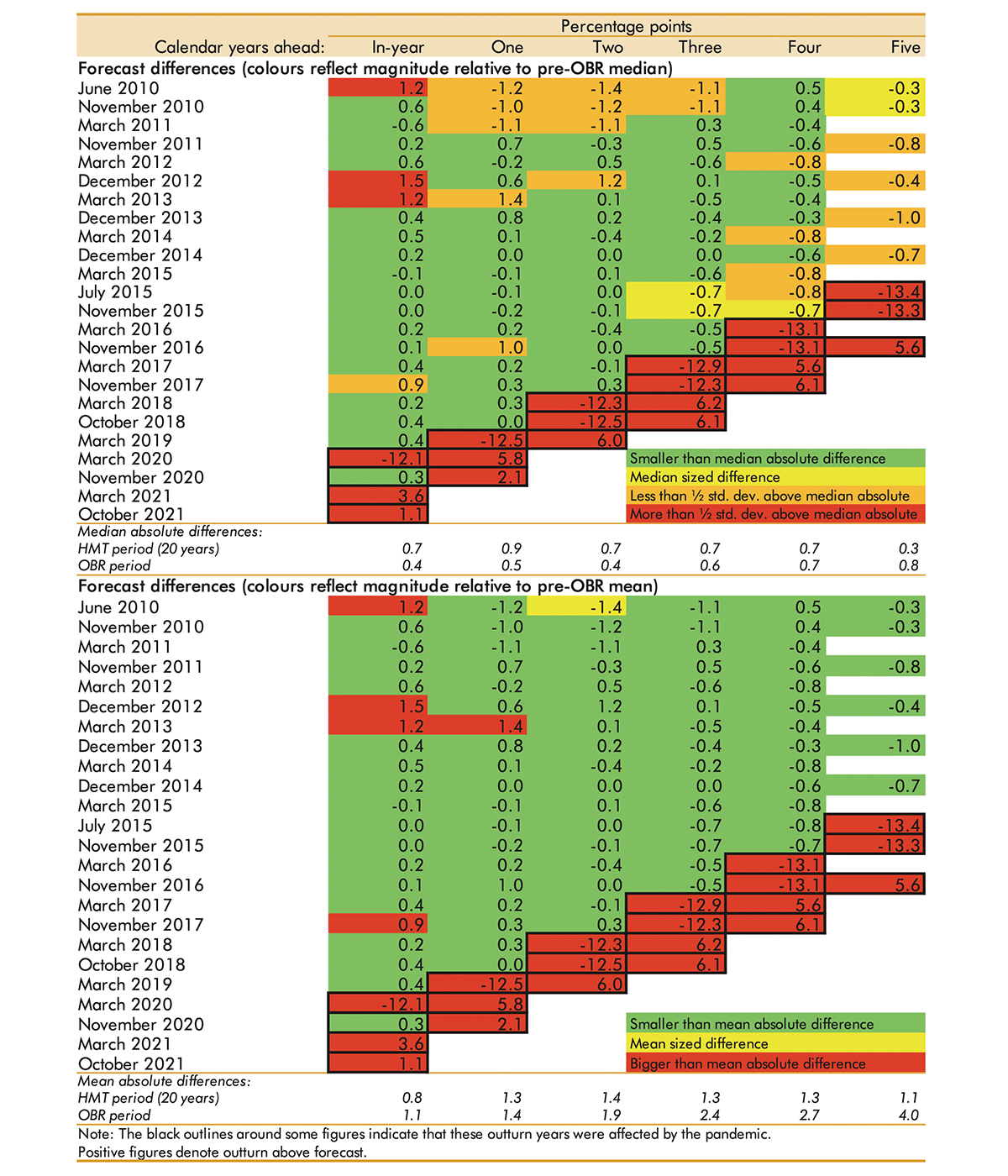

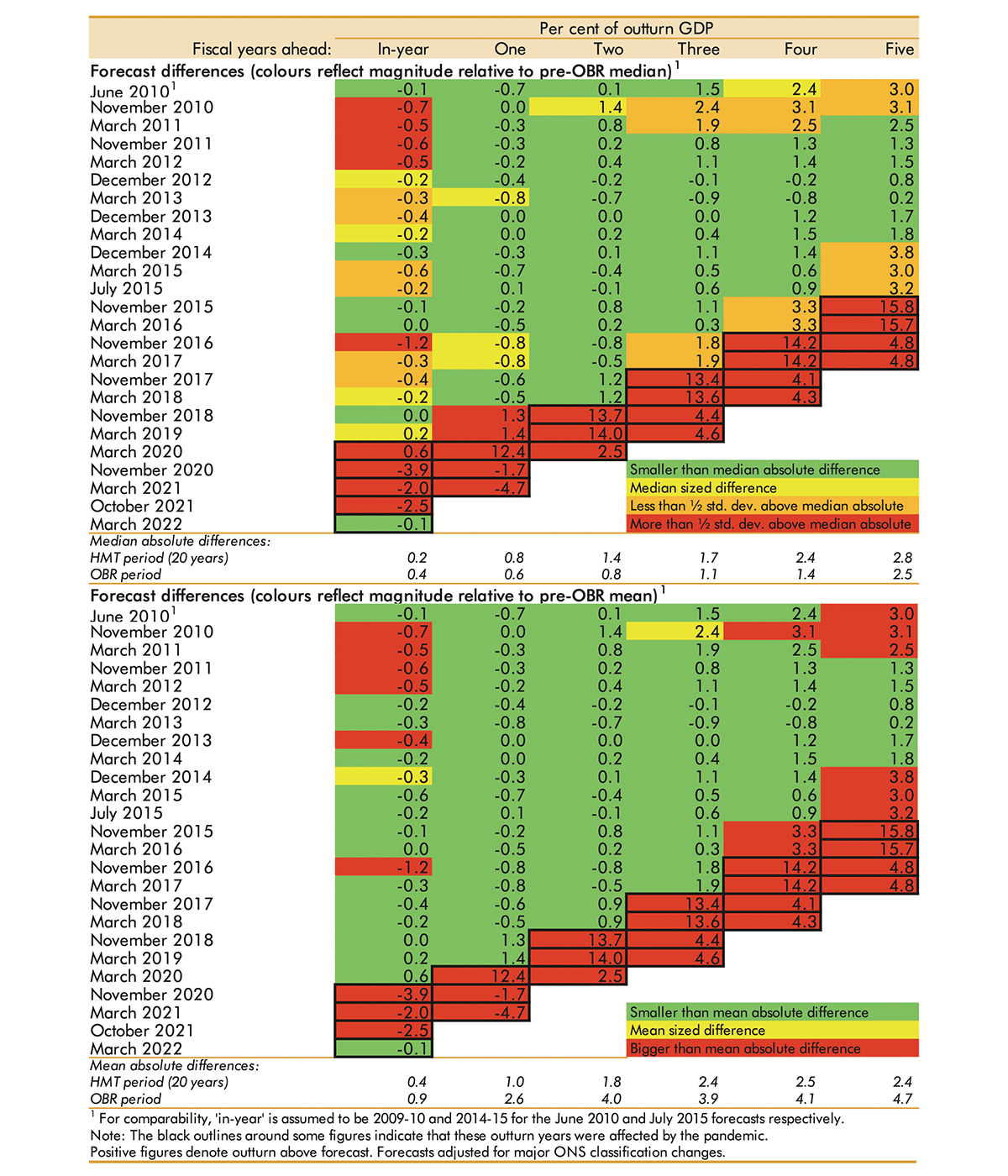

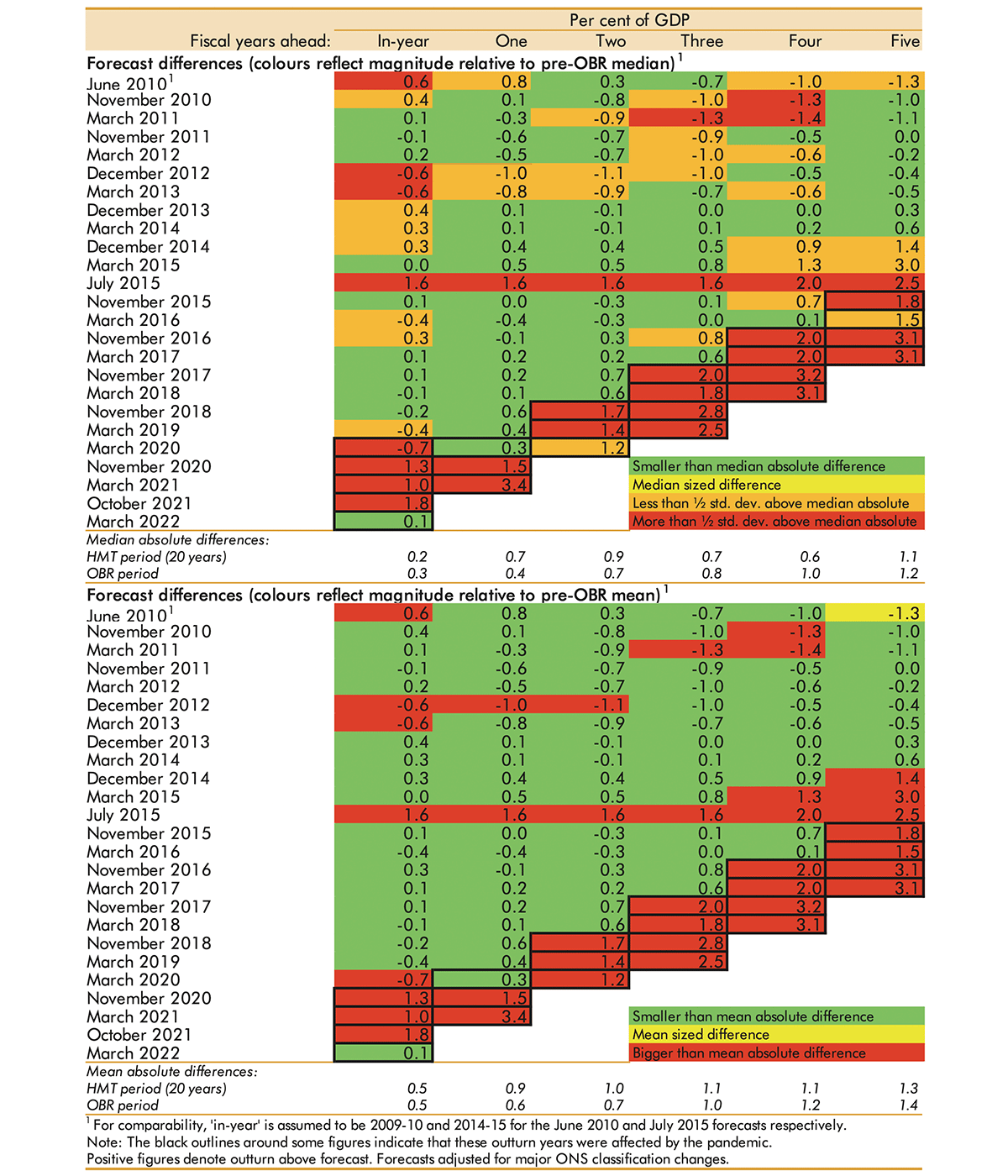

1.13 In Annex A we compare the performance of our forecasts since 2010 to the average across official Treasury forecasts made in the 20 years before the OBR was created. We assess our forecasts for their accuracy (the absolute average difference, capturing the overall size of differences regardless of their direction), and for the first time in our FERs, any degree of ‘bias’ (the average difference, which captures the direction, or skew, of differences).

1.14 In terms of accuracy, it remains the case that our forecasts for real GDP and net borrowing are more accurate than the Treasury’s when measured on a ‘median’ basis (which puts less emphasis on rare but very large shocks such as the financial crisis or the pandemic). Our median absolute difference for real GDP growth in the third year of the forecast is 0.6 percentage points, 0.2 percentage points lower than the Treasury’s. Our median absolute three-year-ahead borrowing difference, at 1.1 per cent of GDP, is 0.3 per cent of GDP lower than the equivalent figure for the Treasury era. But since the pandemic struck, the margins of outperformance relative to the Treasury have been narrowing, and OBR forecasts are no longer more accurate than Treasury ones when measured on a ‘mean’ basis (due to the historic size of the pandemic shock, which saw outturns differ from forecasts by margins nearly twice as large as seen in the financial crisis).

1.15 In relation to bias, both OBR and Treasury forecasts have tended to overestimate real GDP growth and underestimate borrowing, although our forecasts have done this to a slightly lesser extent in each case. The OBR has typically overestimated three-year-ahead GDP growth by 0.5 percentage points, compared to a 0.6 percentage point median Treasury overestimate; and the OBR has underestimated three-year-ahead borrowing by 1.1 per cent of GDP, 0.3 per cent of GDP below the Treasury’s median borrowing bias.

1.16 This optimism bias in OBR economic and fiscal forecasts largely reflects the combination of our overoptimism about the recovery in productivity growth following the financial crisis; increases in departmental spending announced between the Brexit referendum and the 2019 election that our borrowing forecasts could not anticipate; and the impact of the adverse economic shock associated with the pandemic. While in previous FERs we have highlighted the time it took for us to adapt to the disappointing post-financial crisis productivity performance, the departmental spending policy changes and the consequences of the pandemic are not outcomes that we could reasonably anticipate in central forecasts (and are proscribed by legislation from doing so in the case of changes to government policy). But they underscore the importance of our assessment of risks and uncertainties – including the sensitivities around our forecasts, alternative scenarios, and discussion of policy-related risks – both in our Economic and fiscal outlooks and our annual Fiscal risks and sustainability reports.

Chapter 2: The economy

Introduction

2.1 This chapter assesses the performance of our March 2021 economic forecast for the 2021-22 financial year, a 12-month period that saw the UK economy begin to recover from the Covid pandemic but also suffer the initial consequences of the February 2022 Russian invasion of Ukraine and associated rise in energy prices. In particular, the chapter explores the differences between our forecast and latest outturn data for the:

rate of inflation and its components, including the prices of energy, tradable goods, and non-tradeable services;

other market-derived assumptions including interest rates, equity prices, and the exchange rate;

rate and composition of real GDP growth;

labour market and productivity; and

rate and composition of nominal GDP growth, a key determinant of our fiscal forecast.

2.2 We look principally at our March 2021 economy forecast rather than also re-evaluating our March 2020 pre-pandemic forecast (as has been the practice in past Forecast evaluation reports (FERs)). This allows us to focus on how our forecast for the UK economy’s recovery from the Covid pandemic compared with outturn. More detailed analysis of our March 2020 forecasts, which were affected by the arrival and evolution of the Covid pandemic in 2020-21, can be found in our July 2021 Fiscal risks report and December 2021 FER. As Chapter 3 reviews our March 2020 fiscal forecast to help explain our forecast performance for 2021-22, later in this chapter we also briefly summarise the differences between our March 2020 forecast and outturn for cumulative growth from 2019-20 to 2021-22 for nominal GDP and its income and expenditure components.

Inflation

Inflation in 2021-22

2.3 Averaging 4 per cent across the financial year as a whole, the overall rate of CPI inflation was 2.3 percentage points higher in 2021-22 than our March 2021 forecast, one of the largest differences from outturn to forecast in our history to date.[2] As Table 2.1 shows, rather than falling from 1.9 to 1.6 per cent over the course of the financial year as we forecast, inflationary pressures gathered pace from an annual rate of 2.1 per cent in the second quarter of 2021 to 6.2 per cent by the first quarter of 2022. A similar pattern can be seen in RPI inflation, which instead of easing picked up from 3.4 to 8.3 per cent on a quarterly basis between the start and end of the financial year.

Table 2.1: Inflation forecast

Percentage change on a year earlier

2021

2022

2021-22 annual average

Q2

Q3

Q4

Q1

CPI inflation

March 2021 forecast

1.9

1.6

1.6

1.6

1.7

Latest data

2.1

2.8

4.9

6.2

4.0

Difference(1)

0.1

1.2

3.3

4.7

2.3

RPI inflation

March 2021 forecast

3.1

2.7

2.4

2.0

2.6

Latest data

3.4

4.5

6.9

8.3

5.8

Difference(1)

0.2

1.8

4.5

6.3

3.2

(1)Difference in percentage points.

2.4 This difference is largely explained by unexpectedly strong rises in the prices of tradable goods in the wake of the pandemic and in energy associated with the Russian invasion of Ukraine. An unexpectedly rapid recovery in post-lockdown demand in advanced economies, particularly in the US, coupled with persistent supply and logistics bottlenecks, especially in Asia, meant that prices of other tradables in 2021-22 rose by 3.1 percentage points more than we forecast, explaining 1.1 percentage points (just under half) of the overall difference in CPI inflation 2021-22. Rebounding demand for energy-intensive manufactured goods and later the Russian invasion of Ukraine also pushed up the contribution of energy and fuel price inflation, explaining 0.2 and 0.5 percentage points respectively (around one-third combined) of the overall difference in CPI inflation in 2021-22. A tighter-than-expected domestic labour market in the wake of the pandemic also contributed to the inflation overshoot, with the contribution from other non-tradables inflation coming in 1.2 percentage points above forecast and explaining 0.2 percentage points of the overall difference in CPI inflation (around one-tenth). These unexpectedly strong price pressures continued to build through 2022, and Box 2.1 explores in more detail why we also significantly underestimated the strength of inflation over the past year.

Table 2.2: Contributions to differences from our March 2021 inflation forecast

Percentage point contribution to annual CPI inflation

Food, beverages and tobacco

Utilities

Fuels

Other tradables

Other non-tradables

Total

March 2021 forecast

0.2

0.2

0.1

0.3

0.9

1.7

2021-22 outturn

0.3

0.4

0.7

1.4

1.2

4.0

Difference

0.2

0.2

0.5

1.1

0.2

2.3

Box 2.1: Why inflation has been so much stronger than our forecasts in 2022?

Inflation in 2022 has significantly outpaced most of our forecasts since March 2021, with the exception of our most recent EFO in November 2022, generating the largest differences from our forecasts for inflation since the OBR was established. As Chart A shows, against an outturn annual average figure of 9.1 per cent across 2022 as a whole:

Our March 2021 forecast, published just as the UK was emerging from the final lockdown, assumed no post-pandemic surge in inflation and forecast that CPI inflation would remain close to its 2 per cent target.

The forecast in our October 2021 EFO was published as a post-lockdown surge in global demand and bottlenecks in supply chains was becoming apparent (as discussed in Box 2.1), and it predicted the resulting rises in goods prices would push UK CPI inflation up to a peak of 4.4 per cent.

Our March 2022 forecast, which was closed 19 days after the Russian invasion of Ukraine, assumed that the spike in European gas and oil prices would push CPI inflation to a peak of 8.7 per cent in the fourth quarter of 2022.

Our November 2022 forecast, which was produced after Russia had effectively cut off most pipeline gas exports to Europe and the UK Government had announced its Energy Price Guarantee (EPG), forecast that CPI inflation would peak even higher at 11.1 per cent in the fourth quarter of 2022 (albeit 2½ percentage points lower than it would have been without the EPG).

Chart A: Successive OBR inflation forecasts

As Table A shows, all components of the CPI basket contributed positively to the surprise in inflation in 2022 relative to our March 2021 forecast. However, many of these inflationary pressures emerged at different stages and compounded each other over time. So, while subsequent forecasts for 2022 inflation were more accurate than our March 2021 forecast, the cumulative effect of these prices pressures was not fully captured until our November 2022 forecast. The remainder of this box discusses the factors that explain our underestimation.

Table A: Contributions to the difference from our forecasts for 2022 inflation

Percentage point contribution to annual CPI inflation

Food, beverages and tobacco

Utilities

Fuels

Other tradables

Other non-tradables

Total

March 2021

0.3

0.2

0.0

0.3

1.1

1.8

October 2021

0.3

0.7

0.0

0.9

2.0

4.0

March 2022

0.7

2.5

0.6

1.8

1.8

7.4

November 2022

1.5

2.2

1.0

2.5

1.9

9.1

2022 CPI outturn

1.5

2.2

1.0

2.4

2.0

9.1

Difference to forecast

March 2021

1.2

2.0

1.0

2.1

0.9

7.3

October 2021

1.1

1.5

1.0

1.5

0.0

5.1

March 2022

0.7

-0.3

0.3

0.6

0.2

1.6

November 2022

0.0

0.0

0.0

-0.1

0.1

-0.1

Larger-than-expected increases in the prices of ‘other tradables’ (mainly manufactured goods) explain around a quarter of the overshoot in CPI inflation relative our March 2021 forecast. For instance, prices of clothing and footwear rose by 8 per cent in 2022, compared to a rise of only 0.3 per cent in the previous year. This unexpected spike in tradable goods prices was due in large part to our failure to anticipate the combination of: (i) the strength of the post-lockdown surge in demand for tradable goods among advanced economies, especially in the US;a (ii) the persistence of pandemic-driven constraints on the capacity of emerging market countries, especially China, to produce those goods; and (iii) the severity of the logistical challenges in transporting those goods between producers and consumers. The resulting ‘bottlenecks’ pushed up global prices for tradable goods which, as a net importer of manufactured goods, added 2.4 percentage points to UK consumer price inflation in 2022. Our October 2021 and March 2022 forecasts anticipated some of these pressures on tradable good prices, which were subsequently exacerbated by rising energy prices that further pushed up the cost of energy-intensive products.

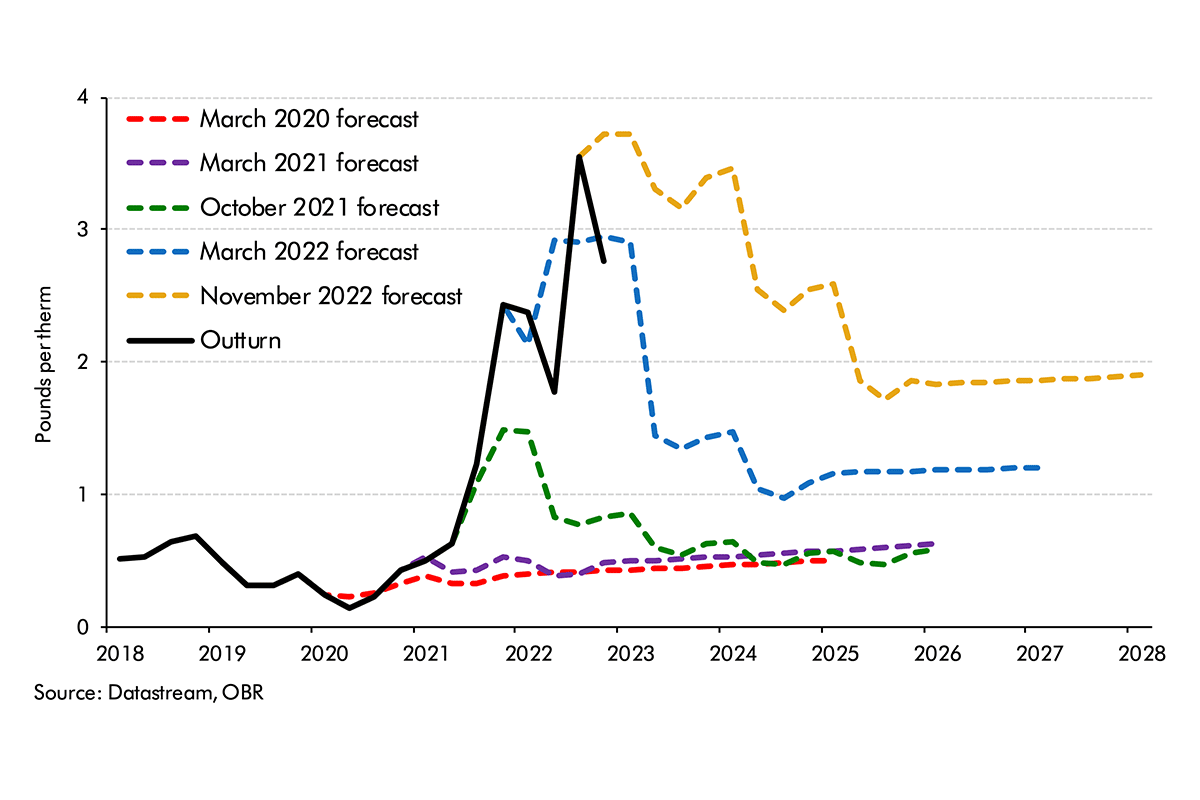

Larger-than-expected increases in the prices of utilities and fuels explain a further two-fifths of the surprise in inflation relative to our March 2021 forecast. This was driven almost entirely by developments in gas (and to a lesser extent oil) prices leading up to and following the Russian invasion of Ukraine. We base our forecasts for oil and gas prices on market expectations, which have been more volatile as a result of the Russian invasion. As shown in Chart B, pressures on European energy prices started to emerge in mid-2021 when Russia began reducing gas deliveries to Europe, sending futures prices up to a peak of £1.50 per therm in the fourth quarter of 2021 in the vintage of the forward curve reflected in our October 2021 forecast. Following the Russian invasion in February 2022, gas prices futures spiked even higher to £3.00 per therm in fourth quarter of 2022 in the curve used in our March 2022 forecast. The cessation of Russian pipeline gas deliveries and concerns about the sufficiency of European storage capacity in the Autumn of 2022 drove gas futures prices higher still, peaking at £3.70 per therm for delivery in the first quarter 2023 in our most recent forecast in November 2022. The impact of this latest surge on retail gas and electivity prices was partly offset by the Government’s Energy Price Guarantee, announced in September, which reduced consumer price inflation by about 2 percentage points in the final quarter of 2022. By the end of 2022, gas prices were nearly five times higher and oil prices twice as high as we had anticipated 22 months earlier.b

Chart B: Successive market forecasts for gas prices

In addition, food, beverages and tobacco contributed a further 1.2 percentage points to the surprise in inflation and one-sixth of the overshoot in CPI relative to our March 2021 forecast. At 16.8 per cent, the December 2022 figure for food and non-alcoholic beverage inflation was the highest since 1977. In part, this reflects the further consequences of higher energy prices (both because energy is used in the production and transportation of agricultural products and because natural gas is an important input to nitrogen-based fertilisers) and the war in Ukraine more generally (such as disruption to Ukrainian wheat production and the Russian blockade of exports). But other factors have also played a role, such as la Niña weather phenomena returning for a third year in 2022, causing droughts in Europe and the Americas.

Inflation in other non-tradables (mainly services) of 6.1 per cent in 2022 also surprised to the upside and accounted for another one-eighth of the overshoot in CPI inflation relative to our March 2021 forecast. This unexpectedly large rise in the prices of domestically-produced services reflected a combination of: (i) higher energy and other input costs; (ii) pressures for higher wage increases to offset at least some of the increased cost of living; and (iii) a larger than anticipated reduction in the size of the labour force in the aftermath of the pandemic, which put further upward pressure on wages. Some of this increase in the cost of non-tradables was anticipated in our October 2021 forecast, and our March and November 2022 forecasts predicted the 2022 outturn more or less exactly.

a Tauber, K., Van Zandweghe, W., Tauber, K., Van Zandweghe, W., 2021, Why has durable goods spending been so strong since the Covid-19 Pandemic, Federal Reserve Bank of Cleveland Economic Commentary.

b To better capture the transition between past and expected prices, we have switched to using spot prices to represent outturn gas prices rather than front-month futures prices.

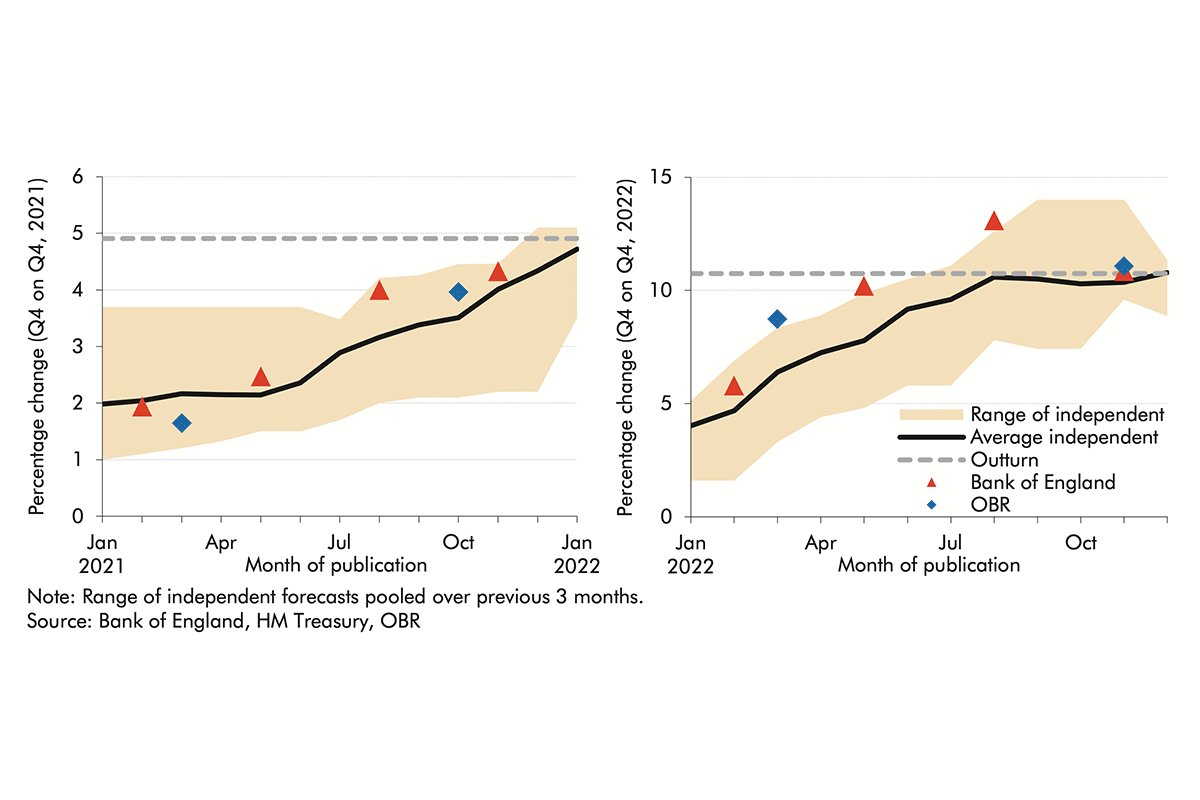

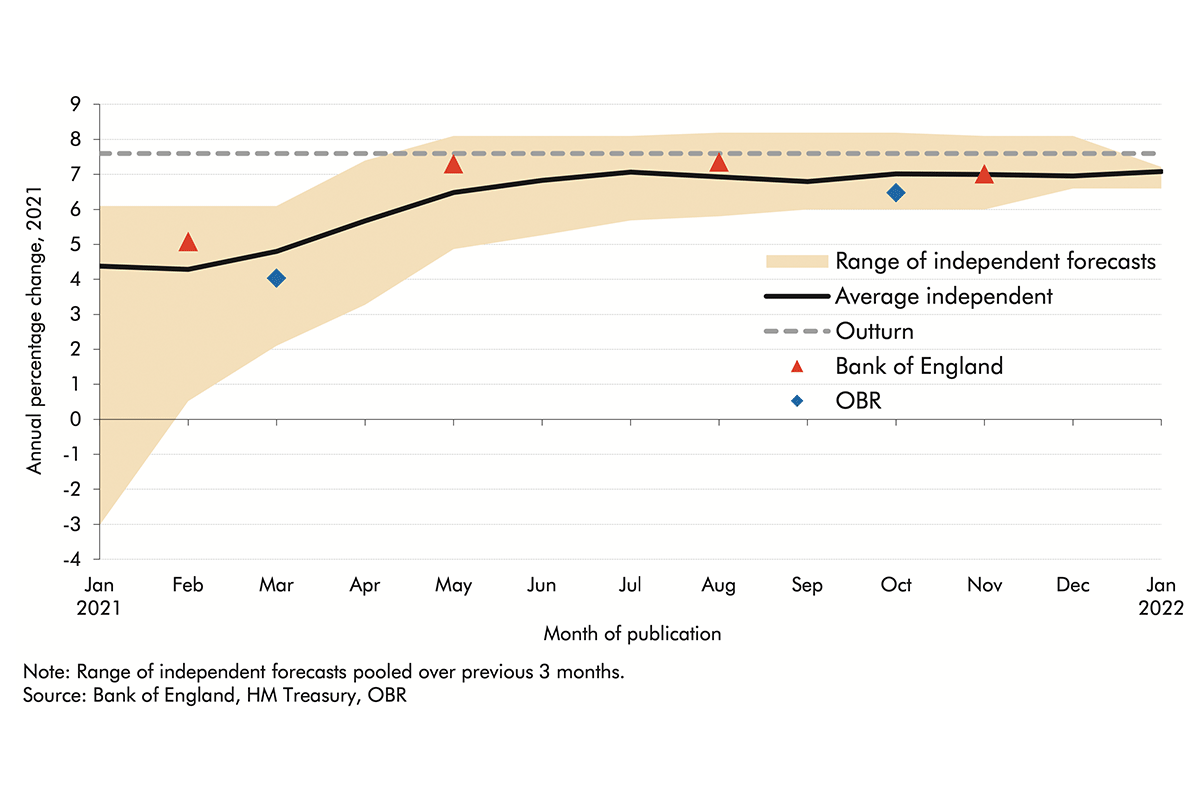

2.5 We were not alone in underestimating the build-up in inflationary pressures mounted across 2021 and 2022. As Chart 2.1 shows, both the average and range of independent forecasts for CPI inflation increased sharply across 2021 and 2022, as forecasters realised the extent of inflationary pressures in those years. On average, independent forecasts produced in the first quarter of 2021 underestimated annual inflation by the fourth quarter of that year by around 3 percentage points. And independent forecasts produced in the first quarter of 2022 underestimated inflation by the fourth quarter of that year by 6 percentage points on average. All independent forecasts produced in the first quarter of both years underestimated the ultimate rate of inflation by at least 1 percentage point in 2021 and by at least 2 percentage points in 2022.

Chart 2.1: Range of forecasts for CPI inflation in 2021 and 2022

Other market-derived assumptions

2.6 Other market-derived assumptions evolved broadly in line with our March 2021 forecast in 2021-22. The initial pace of monetary tightening was only slightly faster than assumed, reflecting the upside news on inflation, though Bank Rate has risen much further since. At only £30 billion less than we had assumed, the stock of assets held in the APF in 2021-22 was broadly in line with our March 2021 expectations of £900 billion. The successful rollout of vaccines, a tight labour market, and surging inflation supported nominal equity prices, which came in 3.4 per cent higher than our forecast. And the effective exchange rate came in 3.0 per cent higher than expected.

Table 2.3: Other market-derived assumptions for 2021-22, financial year average

Bank rate (per cent)

Market gilt rates (per cent)

Quantitative easing(1) (£ billion)

Equity prices (FTSE All-share)

Exchange rate (index)

March 2021 forecast

0.03

0.6

900.3

3958

79.5

Latest data

0.19

1.0

866.8

4092

81.9

Difference(2)

0.16

0.4

-33.5

3.4

3.0

(1) Total asset purchases, including corporate bonds, at the end of the 2021-22 financial year. (2) Per cent difference except Bank Rate (percentage points) and quantitative easing (£ billion).

Real GDP: level, growth and composition

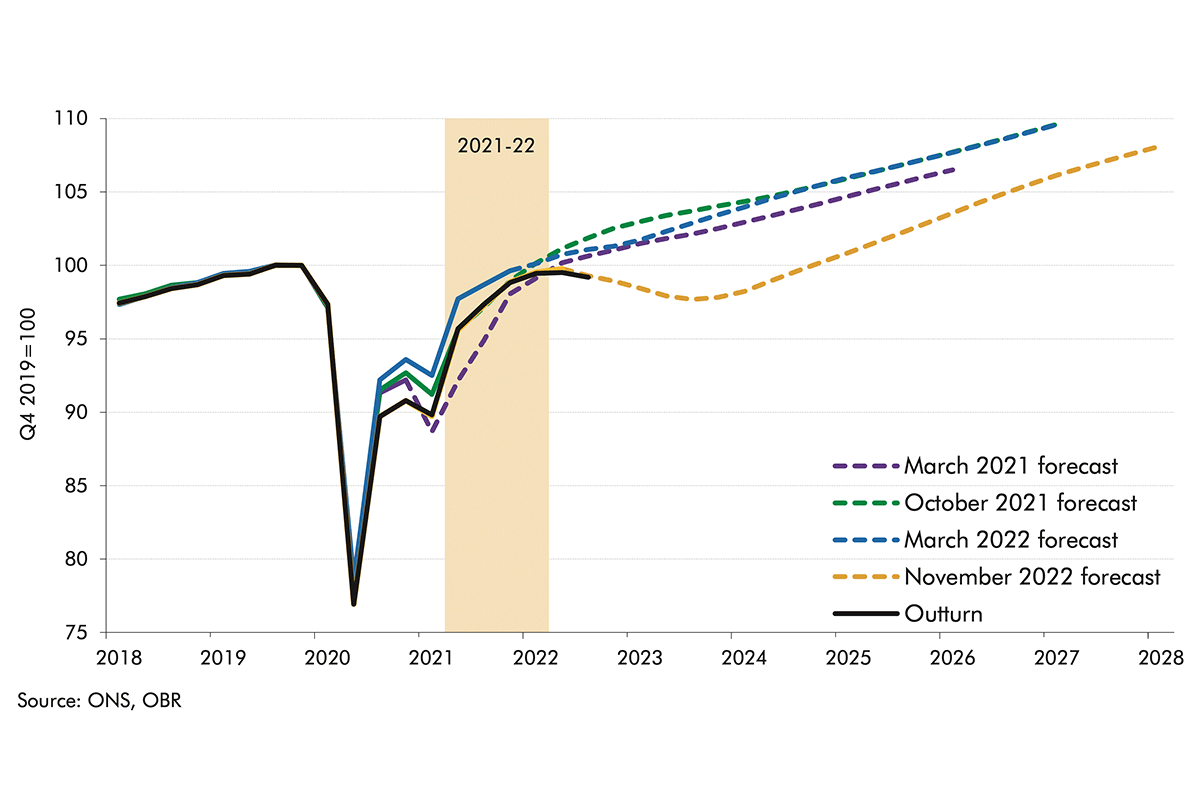

2.7 Despite the hit to real incomes from higher-than-expected inflation, the level of real GDP is broadly in line with our March 2021 forecast by the first quarter of 2022. That forecast anticipated the economy recovering to its pre-pandemic level of output by the middle of 2022, but the latest data suggest that output was still 0.5 per cent below its pre-pandemic peak at that point. In our latest forecast from November 2022, the pre-pandemic level of output is now not expected to be recovered until the last quarter of 2024 due to the recession triggered by the subsequent rise in energy prices.

Chart 2.2: Successive forecasts for the level of real GDP

2.8 Significant downward revisions to the level of outturn GDP in 2020-21, mean that the profile of growth was steeper across the early part of 2021-22 than we expected in March 2021, and we underestimated real GDP growth in 2021-22 by 3.2 percentage points. The latest vintage of data therefore suggest that the economy initially rebounded less strongly from the first wave of the pandemic than we had thought at the time of our March 2021 forecast, but then rebounded more quickly than expected to the few public health restrictions that remained in place.[3] The economic recovery slowed in the latter part of the year as the rebound in demand bumped up against supply bottlenecks and rising energy prices associated with the Russian invasion of Ukraine. Table 2.4 breaks this 3.2 percentage point forecast difference down into the different expenditure components of GDP:

Stronger consumption growth explains 2.7 percentage points, or more than four-fifths of the difference. A faster-than-expected recovery in demand due to the effective rollout of vaccines and supported by consumers and businesses surprising adaptability to public health restrictions, boosted consumption and GDP.

Business investment growth was broadly in line with our forecast, although the housing market recovered from the pandemic faster than we had expected in March 2021 with the ‘race-for-space’ and stamp duty holiday fuelling private residential investment, the contribution of which was 0.5 percentage points stronger than our forecast.

Government spending contributed 0.5 percentage points less to real GDP growth than forecast. This in part reflects lower measured covid- and non-covid-related health activity than we expected.

Net trade proved to be less of a drag on growth than expected, contributing 1.3 percentage points more to GDP growth than we forecast in March 2021 As discussed above, even prior to the Russian invasion of Ukraine, the unexpected growth in the costs of tradable goods weighed on the volume of UK imports while demand for UK exports grew more quickly as the economies of our trading partners also bounced back more quickly than anticipated from the pandemic. But changes in data collection mean that these data are even more prone to revision than normal.[4]

Other components contributed 0.8 percentage points less to growth than we anticipated in March 2021. Over three-quarters of this is driven by changes in inventories, as firms built up less stocks than anticipated recovering from the pandemic likely owing to supply bottlenecks and global shortages. Inventories is also a highly volatile series subject to large revisions.

Table 2.4: Expenditure contributions to real GDP growth in 2021-22

Percentage points

Private consumption

Business investment

Private residential investment

Total government

Net trade

Other

GDP

March 2021 forecast

5.9

0.7

0.4

3.7

-3.1

1.9

9.5

Latest data

8.6

0.7

0.9

3.2

-1.8

1.2

12.7

Difference(1)

2.7

-0.1

0.5

-0.5

1.3

-0.8

3.2

(1)Difference in unrounded numbers.

2.9 Our forecasts for real GDP growth over calendar year 2021 were broadly in line with, if slightly below, those of other contemporaneous independent forecasters. As Chart 2.3 shows, we and other forecasters revised up our projections for real GDP growth between March 2021 and October 2021, as we got more information over the course of the year about both downward revisions to 2020 and the upside surprise to demand in the wake of the pandemic. However, even our forecast of 6.5 per cent growth in our October 2021 forecast turned out to be lower than the 7.6 per cent growth rate in outturn for 2021.

Chart 2.3: Range of forecasts for real GDP growth

Labour market and productivity

2.10 One of the factors behind our underestimating the strength of the post-pandemic recovery in output was an assumption that the closure of the coronavirus job retention scheme (the CJRS or ‘furlough scheme’) would lead to a rise in the unemployment rate from 4.8 per cent in 2020-21 to 5.9 per cent in 2021-22 (and a peak of 6.5 per cent on a quarterly basis). As shown in Chart 2.4, this post-pandemic rise in unemployment did not materialise and, instead, the rate fell slightly to 4.2 per cent in 2021-22 as a whole (and has fallen to a multi-decade low of 3.6 per cent on a quarterly basis in the third quarter of 2022). The CJRS, and other pandemic-related business support, thus proved more successful than we had assumed in preserving viable businesses and protecting employment through one of the largest peacetime economic shocks.

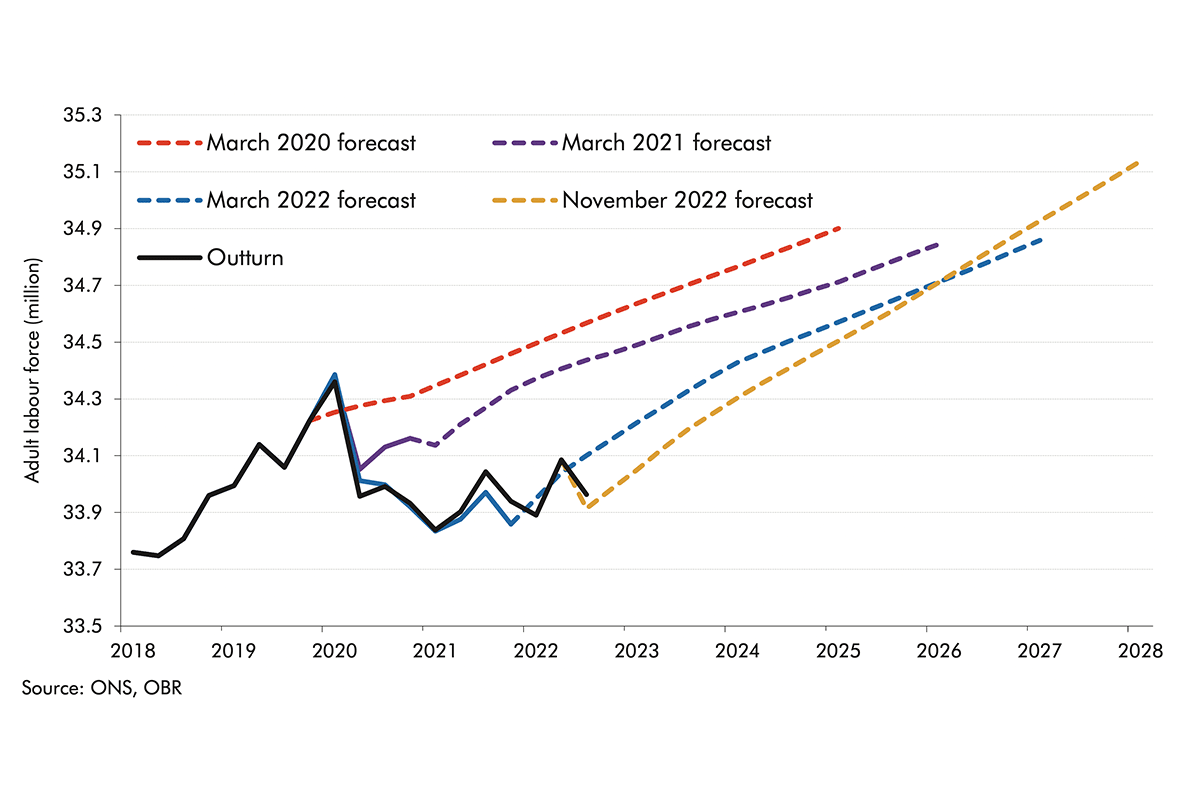

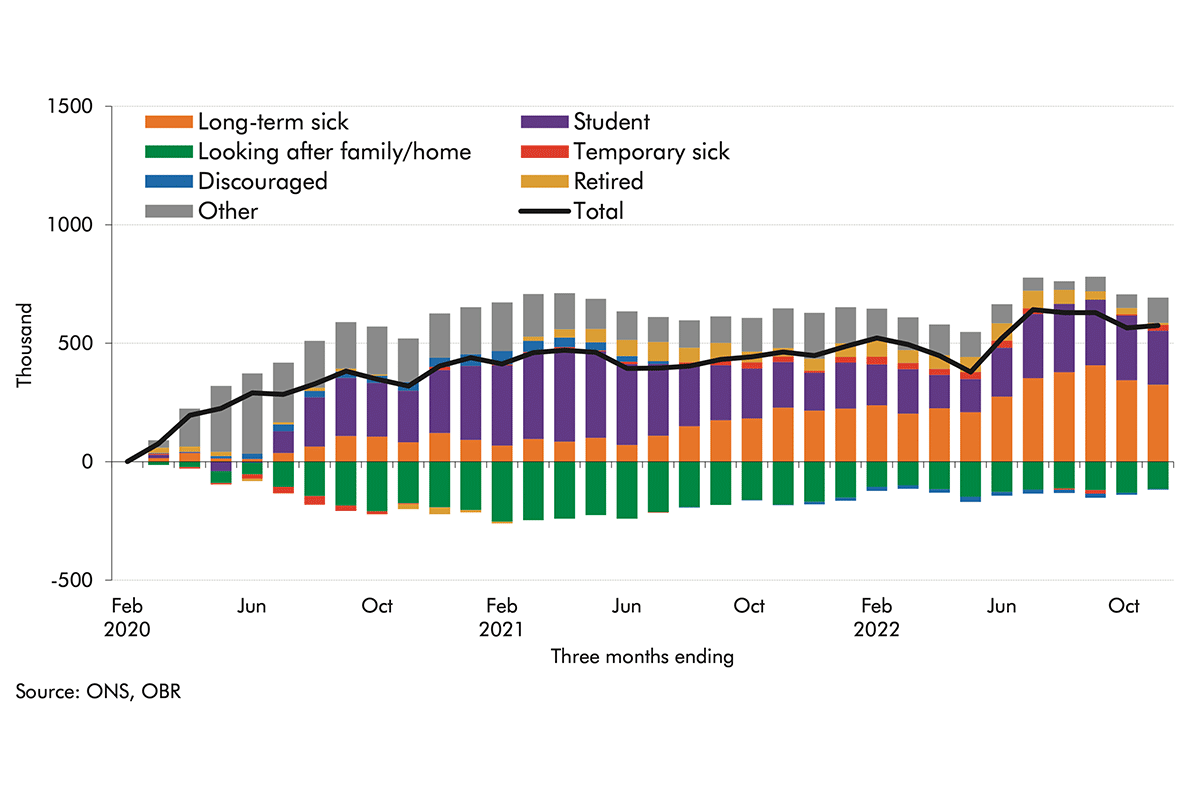

2.11 However, the pandemic seems to have had a more adverse effect on the overall size of the labour force than we forecast in March 2021, where we assumed that the labour force would recover from its pandemic level of 34.1 million in the second quarter of 2020 and average 34.3 million people in 2021-22.[5] In fact, in the first quarter of 2022 the labour force remained at 33.9 million, close to where it was at the height of the pandemic in the second quarter of 2020. The flipside of this shortfall in the size of the labour force has been the rise in inactivity post-pandemic of 575,000, discussed in paragraph 2.13. The Labour Force Survey shows that this rise has been driven by increases in the numbers of students (227,000) and those reporting long-term ill health (325,000). And, as Chart 2.5 shows, later forecasts have taken account of lower post-pandemic rates of economic activity, but still assumed some recovery in the overall size of the labour force.

Chart 2.4: Forecast and outturns for unemployment rate

Chart 2.5: Successive forecasts and outturn for the adult labour force

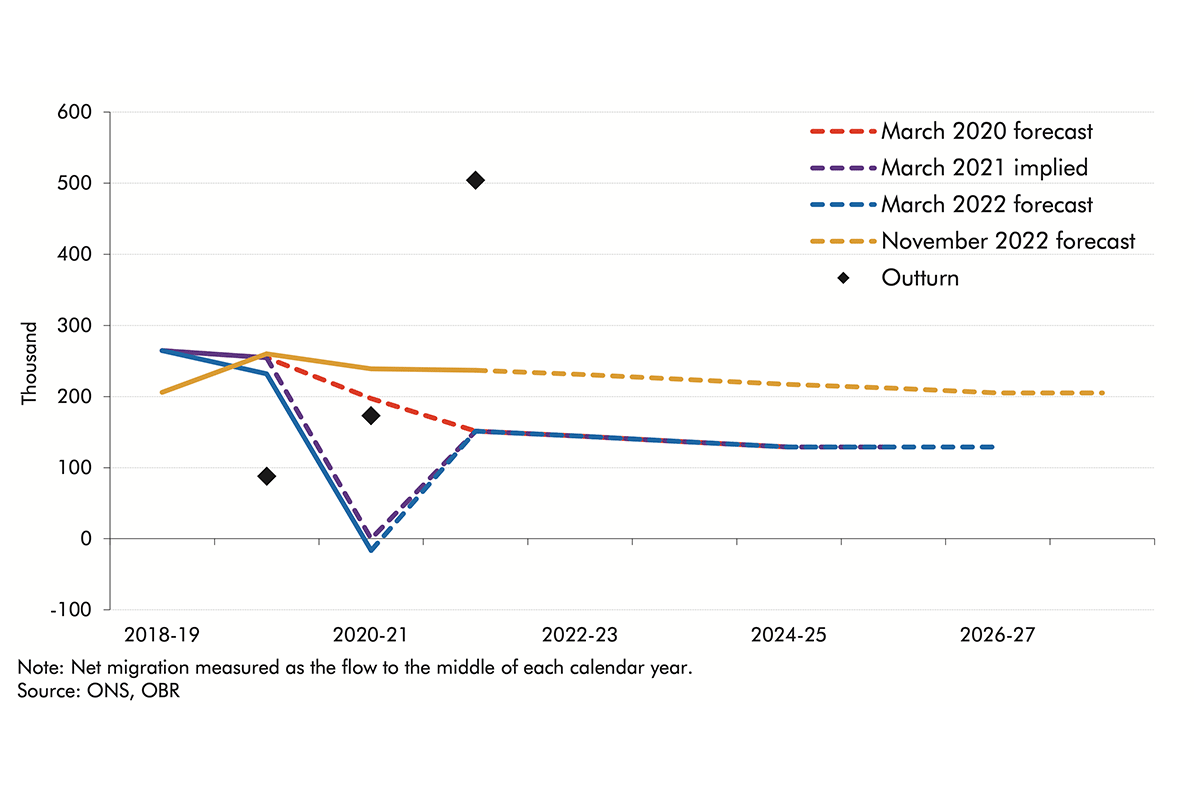

2.12 By contrast, net inward migration has surprised on the upside relative to our forecast. For the March 2021 forecast, we thought net migration would be around 150,000 in the year to mid-2022, consistent with the ONS net-zero-EU-migration variant of its population projections.[6] The latest data suggest that net inward migration was over half a million in the year to June 2022 – more than three times the amounts in our March 2021 forecast. A number of factors have coincided to lead to high immigration in the recent past, including the continued recovery in travel following the pandemic, the new immigration system following Brexit, the British National Overseas visas for Hong Kong nationals, and the ongoing support for Ukrainian nationals and others requiring protection.[7]

Chart 2.6: Net migration

2.13 The net result of our overestimation of the overall rate of labour force participation, but underestimation of the level of net migration,[8] was that our March 2021 forecast overestimated growth in the total adult labour force in 2021-22 by 161,000 people. And while migration may be an upside risk to our existing outlook, there is also downside risk from long-term sickness, with the latest data suggesting that those reporting long-term sickness as the reason for inactivity accounting for 57 per cent of the overall 575,000 rise in working-age inactivity since the start of the pandemic. The prevalence of ill health continues to be a risk to our forecast (Chart 2.7), and this risk is exacerbated by large numbers on NHS waiting lists, with the total for November 2022 standing at 7.2 million.

Chart 2.7: Changes in 16-64 inactivity

2.14 Total hours growth also surprised by 1.2 percentage points to the upside at 11.4 per cent in 2021-22, reflecting the combined influence of the factors set out above (as well as the more modest influence of average hours underperforming our March 2021 expectations). But with the upward revision to GDP growth greater still, growth in productivity per hour was 1.7 percentage points higher than our March 2021 forecast at 1.1 per cent in 2021-22. This was one of the factors that caused us to revise down our judgement regarding the long-run scarring effect of the pandemic on potential productivity levels from 2 to 1 per cent in October 2021, and lower again to 0.8 per cent in March 2022.[9]

2.15 The upside surprise on productivity growth and the combined influence of higher inflation and a tighter-than-expected labour market, with high churn in the labour market (job-to-job moves reached record highs of 997,000 in the first quarter of 2022), meant that average growth in nominal earnings was 4.4 percentage points above our March 2021 forecast of 2.4 per cent. Earnings data were distorted in mid-2021 by compositional and base effects from the height of the pandemic, but these should have unwound in late 2021.[10]

Table 2.5: Labour market indicators

Change, per cent, unless otherwise stated

Total hours

Average hours

Total employment

Labour force

Unemploy- ment rate

Average earnings

Productivity per hour

(million)

(hours)

(thousand)

(thousand)

ppts

March 2021 forecast

10.2

(94)

10.9

(3.1)

-0.7

(-213)

0.5

(176)

1.1

2.4

-0.6

Latest data

11.4

(105)

10.6

(3.0)

0.7

(219)

0.0

(15)

-0.6

6.9

1.1

Difference to forecast(1)

1.2

(12)

-0.3

(-0.1)

1.3

(432)

-0.5

(-161)

-1.7

4.4

1.7

(1)Difference in unrounded numbers.

Growth and composition of nominal GDP

2.16 Our economy forecast provides the basis for the fiscal forecasts that we use to estimate the costs of Government policies and assess the Government’s performance against its fiscal targets. The most fiscally important elements of the economy forecast are those that drive the major tax bases, namely the income and expenditure components of nominal rather than real GDP. These are influenced by both real GDP and whole economy inflation, as well as by changes in the share of whole economy nominal GDP accounted for by each component. The fiscal forecast differences discussed in Chapter 3 have been influenced heavily by surprises in the composition of nominal GDP as well as its overall size. In particular, fiscal support measures were sufficient to leave labour income – the largest tax base of all – little changed from our pre-pandemic March 2020 forecast despite nominal GDP falling well short of that forecast due to the pandemic. In this section we briefly review the key nominal forecasts that underpin the analysis of fiscal forecast differences in 2021-22 that is presented in Chapter 3.

Differences relative to our March 2020 nominal GDP forecast

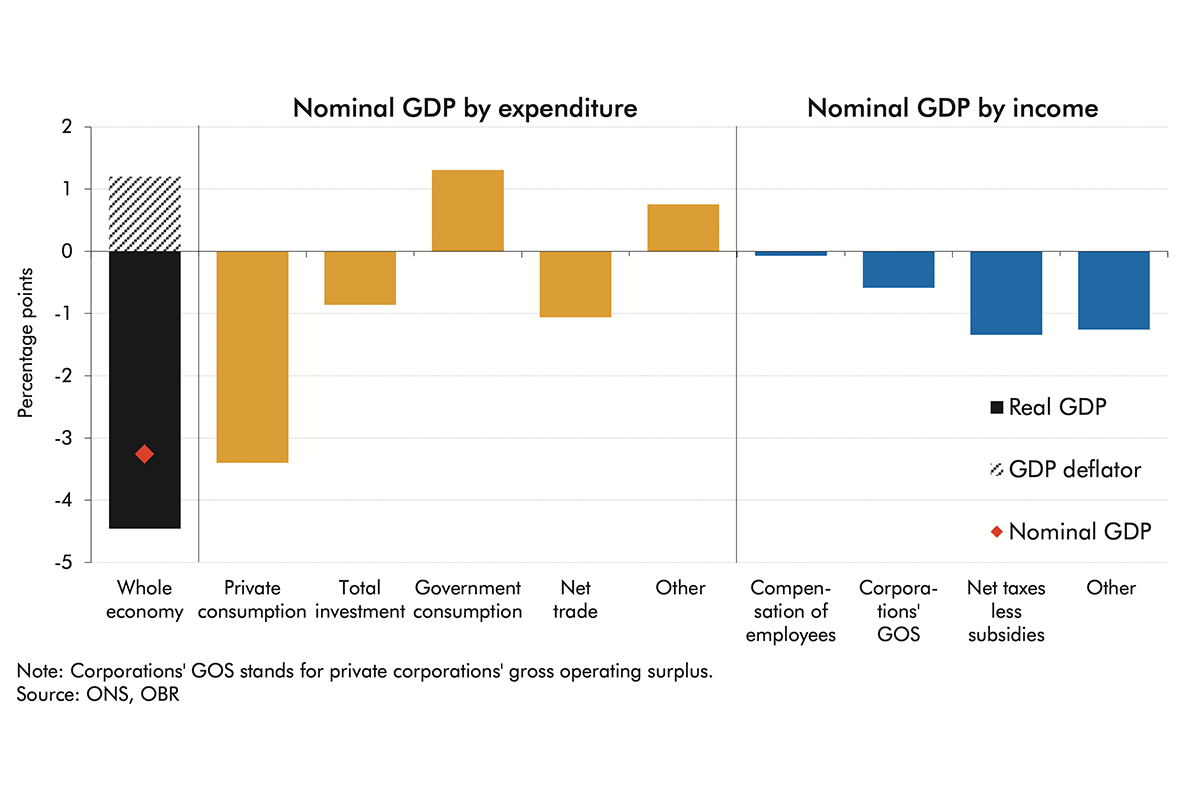

2.17 Nominal GDP in 2021-22 fell well short of our March 2020 forecast (cumulative growth between 2019-20 and 2021-22 was 3.3 percentage points weaker than forecast), as one would expect since we did not initially anticipate the full extent of the pandemic. But the composition of that forecast difference in terms of expenditure and income components varied considerably, which had material implications for the surprisingly modest difference between our forecast for the deficit in 2021-22 and the latest outturn. In particular:

By expenditure component, private sources of demand fell well short of our forecast, and particularly household consumption, the contribution of which grew by 0.3 per cent in nominal terms over the two years to 2021-22, 3.4 percentage points less than forecast and more than explained the overall shortfall in nominal GDP by expenditure.

By income component, labour income held up remarkably well, reflecting the still considerable fiscal support in place in 2021-22. Indeed, the contribution from compensation of employees grew by 4.0 per cent in the two years to 2021-22, only 0.1 percentage points less than we predicted ahead of the pandemic. Instead, it was net taxes and benefits and other incomes (of which over half is accounted for by the statistical discrepancy, but also includes mixed income and the operating surpluses of households and public sectors) that fell short of expectations.

Chart 2.8: March 2020 forecast differences in contributions to cumulative nominal GDP growth between 2019-20 and 2021-22

Differences relative to our March 2021 nominal GDP forecast

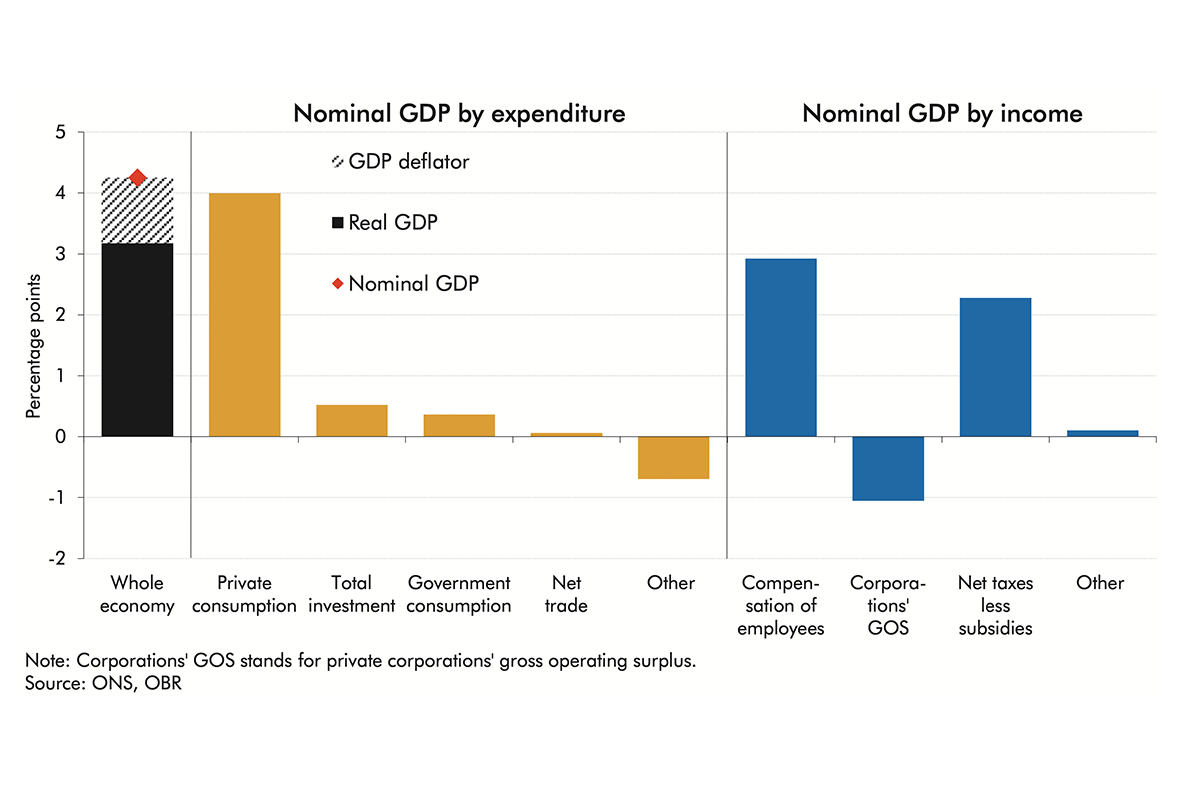

2.18 Turning to our first ‘post-pandemic’ forecast, nominal GDP growth was over 4 percentage points higher in 2021-22 than we expected in March 2021. Stronger-than-expected real GDP growth accounts for over 3 percentage points of this difference, while a higher-than-expected deflator accounts for around 1 percentage point.[11] This stronger-than-expected performance of nominal GDP reflected:

By expenditure component, it was almost entirely due to private consumption recovering more quickly than expected from a low base, and an upside surprise to the prices of consumption goods (as discussed earlier in the chapter).

By income component,compensation of employees contributed to over two-thirds of the upside surprise to growth as a tighter-than-expected labour market supported earnings growth, as discussed above. Higher tax bases (e.g. increased VAT receipts from higher consumption growth) supported net taxes and subsidies offset by lower-than-expected gross operating surplus (GOS, a measure of profits in the National Accounts). The contribution from growth in GOS was 1.2 percentage points, 1.1 percentage points lower than we expected in March 2021.

Chart 2.9: March 2021 forecast differences in contributions to nominal GDP growth in 2021-22

Chapter 3: The public finances

Introduction

3.1 This chapter assesses the performance of our pre-pandemic March 2020 fiscal forecast and – in more depth – our March 2021 fiscal forecast for the 2021-22 financial year. In each case we explore the differences between our forecast and the latest outturn data for:

public sector net borrowing (PSNB), beginning with a summary of how our estimates of PSNB in 2021-22 evolved over successive forecasts, and how these compared to estimates produced by other forecasters;

the receipts and spending forecasts that underpin our March 2020 and March 2021 PSNB forecasts for 2021-22; and

our March 2020 and March 2021 public sector net debt (PSND) forecasts for 2021-22.

3.2 Differences between outturn data and our forecasts have been broken down into policy changes – differences due to policies announced after the publication of the forecast being assessed – and other factors. For our receipts forecasts we further split this second category into: economic factors (due to the underlying economic forecasts); classification changes (due to items being reclassified into or out of the public sector following the forecast); and fiscal forecasting differences (any remaining differences that cannot be explained by the other categories, such as those related to how well the underlying forecast model matches reality or judgements that we impose on top of the effects of economic determinants).

The evolution of our borrowing forecast for 2021-22

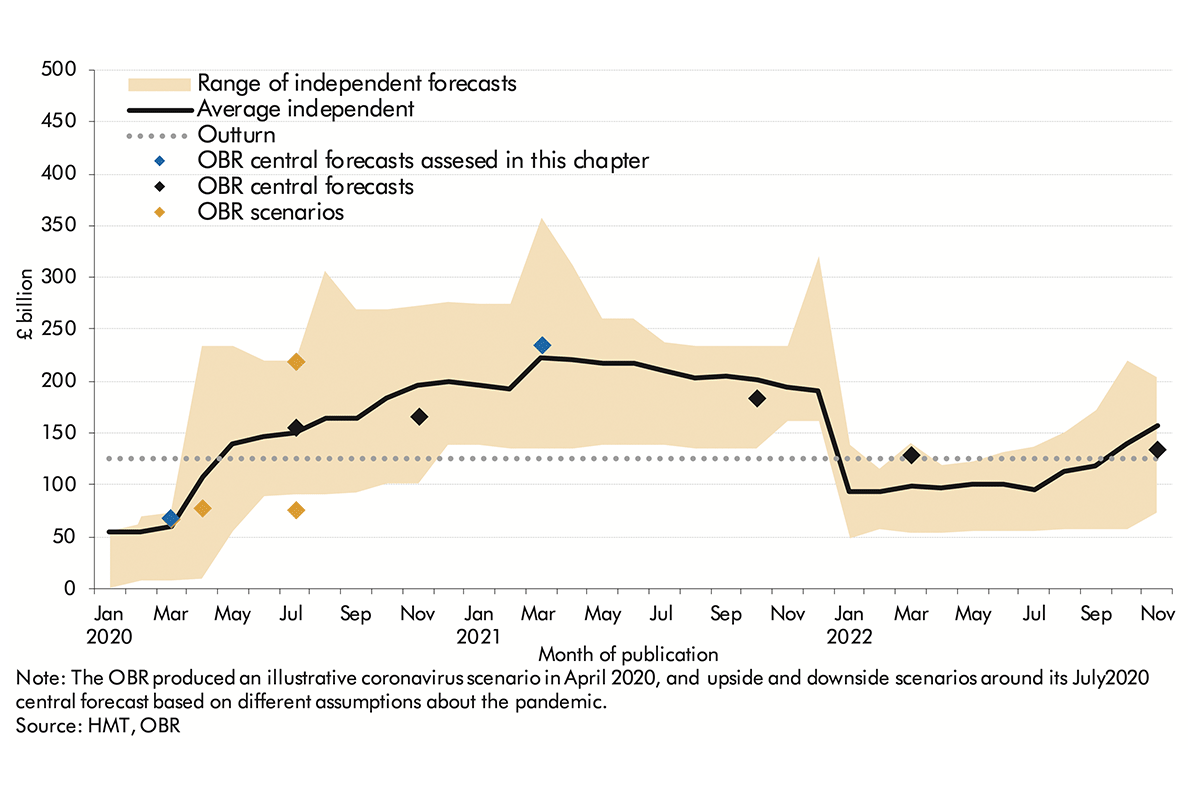

3.3 After the record peacetime deficit of 15.0 per cent of GDP (£312.8 billion) in 2020-21 when the public finances felt the full force of the Covid pandemic and the cost of associated fiscal support measures, the deficit fell back to 5.4 per cent of GDP (£125.4 billion) in 2021-22 on the latest ONS estimates. That was £58.7 billion higher than in our pre-pandemic March 2020 forecast – an unsurprising overshoot, though perhaps not as large as one might have expected. Thereafter, borrowing in 2021-22 came in below each of our subsequent four central forecasts – by as much as £108.6 billion in our March 2021 forecast. Understanding the drivers of this pre-pandemic borrowing overshoot, and in particular the larger March 2021 borrowing undershoot, is the core task of this chapter.

3.4 Given we have access to much more public finances data and information on policies being announced at fiscal events than other forecasters, our borrowing forecasts typically lead the consensus (as Chart 3.1 largely confirms for 2021-22). The main difference between our fiscal forecasts and those of many other outside forecasters is that ours must be conditioned on current stated government policy, so cannot, for example, anticipate temporary support measures being extended at a future fiscal event.

Chart 3.1: Evolution of the range of forecasts for PSNB in 2021-22

Our March 2020 fiscal forecast differences for 2021-22

Public sector net borrowing

3.5 In our March 2020 forecast, which was completed before the extent of the pandemic’s impact in the UK was known, we expected borrowing in 2021-22 to be £66.7 billion, an underestimate of £58.7 billion. Table 3.1 shows that this difference is more than explained by spending exceeding our forecast by £62.7 billion (6.4 per cent), thanks to the £65.8 billion cost of (largely pandemic-related) policies announced after this forecast was published. Remarkably, receipts exceeded our forecast by £4.0 billion (0.4 per cent) despite tax cuts announced after the March 2020 Budget and the lingering effects of the pandemic on the cash size of the economy in 2021-22.

Receipts

3.6 The £4.0 billion receipts surplus masks larger and offsetting effects from policy changes (which reduced receipts by £24.3 billion relative to the forecast) and a positive difference of £28.3 billion spread across classification changes (which added £0.7 billion)[12] and the combined effect of differences in underlying economic determinants and other fiscal forecasting differences (which contributed a surplus of £27.6 billion). Across individual taxes, these differences are attributable to:

Income tax and NICs outperforming the March 2020 forecast by £11.5 billion (3.1 per cent). This is not explained by policy changes, which accounted for only £0.2 billion of the difference, or by economic factors (with growth in wages and salaries falling slightly short of our forecast, explaining a £2.9 billion shortfall). Instead it is more than explained by a fiscal forecasting difference of £14.2 billion. Within PAYE income tax and NICs, the surplus reflects the effective tax rate on PAYE income exceeding our forecast as fiscal drag proved more powerful than expected. Within self-assessed income tax, the relatively modest £1.1 billion surplus reflects the combination of two largely offsetting differences. First, a shortfall of £6.7 billion due to economic determinants, reflecting in particular weaker-than-expected self-employment and dividend incomes as recorded in the National Accounts. But second, a surplus of £7.4 billion recorded as a fiscal forecasting difference, which reflects those taxable income streams and associated tax payments performing far better than the National Accounts measures would suggest.[13]

A VAT shortfall of £3.3 billion, more than explained by a £5.8 billion cost from policy measures, mainly a temporary reduced rate for the retail, hospitality and leisure sectors, offset by £2.5 billion of positive surprise from other factors.

Onshore corporation tax was £3.8 billion above forecast, despite a £9.3 billion policy-related reduction from the super-deduction measure. Profits in 2021-22 were helped by government grant, loan and furlough schemes as well as the fact that many large companies and high-paying sectors (such as financial services, professional services and parts of retail) were less affected by the pandemic. Both of these issues are discussed in more detail below in relation to the March 2021 forecast difference.

Other receipts fell £8.0 billion short of our forecast. This reflects policy changes that reduced receipts from a range of taxes, in particular business rates (£7.2 billion) and stamp duty land tax (SDLT, £2.3 billion). In terms of other forecasting differences, air passenger duty had the largest relative difference between forecast and outturn (a £3.0 billion or 72 per cent shortfall), reflecting the ongoing impact of travel restrictions on air passenger numbers in 2021-22.

Spending

3.7 The £62.7 billion underestimate of spending in 2021-22 is attributable to:

£47.3 billion of additional departmental spending (DEL), largely related to the ongoing effects of the pandemic. £51.8 billion of our DEL underestimate relates to decisions to increase departmental spending limits to fund vaccines, the test-and-trace programme, and pandemic-related support for businesses and households. This is partly offset by departments underspending against these limits by £4.5 billion more than expected (as discussed in relation to more recent forecasts in Box 3.2).

Welfare spending coming in £7.4 billion higher than forecast. Most of this difference (£6.0 billion) relates to subsequent policy decisions, in particular the £20 a week increase to universal credit that extended into the first half of 2021-22.

Debt interest spending being £18.5 billion higher than forecast, more than explained by accrued interest on index-linked gilts, which overshot by £22.3 billion thanks to higher-than-forecast RPI inflation. This was partially offset by the debt interest savings associated with the Bank of England’s Asset Purchase Facility (APF) coming in £6.4 billion higher than expected, largely thanks to the more than £400 billion increase in the size of the APF’s gilt holdings and Bank Rate being cut to 0.1 per cent.

£17.0 billion of spending on pandemic-related income support schemes – the coronavirus job retention scheme (CJRS, £8.6 billion) and self-employment income support scheme (SEISS, £8.4 billion) – in the first half 2021-22. These schemes were introduced shortly after our March 2020 forecast, and then extended several times.[14]

3.8 These underestimates relative to our March 2020 forecast were partially offset by a £27.6 billion overestimate of other spending, which included:

Local authority self-financed current expenditure coming in £9.5 billion lower than forecast (largely as a consequence of business rates measures that reduced local sources of financing and shifted spending from this category to DELs);

£4.4 billion of negative spending relating to downward revisions to the expected cost of pandemic loan guarantee schemes introduced after the March 2020 forecast (the initial estimated cost of which was recorded as spending in 2020-21); and

£14.3 billion in National Accounts adjustments that align our bottom-up spending-control-based forecasts to the definitions of current and capital expenditure used in the public sector finances data.

Table 3.1: Breakdown of March 2020 borrowing, receipts and spending forecast differences for 2021-22

£ billion

Forecast

Outturn

Difference, of which:

Total

Policy

Other

PSNB

66.7

125.4

58.7

90.2

-31.5

Receipts

910.8

914.7

4.0

-24.3

28.3

of which:

Income tax & NICs

374.4

385.9

11.5

0.2

11.3

VAT

145.9

142.6

-3.3

-5.8

2.5

Onshore corporation tax

58.9

62.6

3.8

-9.5

13.2

Other receipts

331.6

323.7

-8.0

-9.3

1.3

Spending

977.4

1,040

62.7

65.8

-3.2

of which:

Departmental spending

443.5

490.7

47.3

51.8

-4.5

Welfare

237.8

245.2

7.4

6.0

1.4

Debt interest

37.8

56.4

18.5

0.0

18.5

Pandemic-related income support

0.0

17.0

17.0

17.0

0.0

Other spending

258.3

230.7

-27.6

-9.0

-18.6

Note: this table uses the convention that a negative figure means a reduction in PSNB i.e. higher-than-forecast receipts or lower-than-forecast spending reduces PSNB in outturn relative to forecast.

Public sector net debt

3.9 Public sector net debt ended 2021-22 at £2.4 trillion, £545 billion higher than forecast in March 2020. Of this, £344 billion came from higher debt at the start of the year, largely thanks to the effects of the pandemic on borrowing in 2020-21; £59 billion from higher PSNB in 2021-22; and £143 billion from higher-than-expected financial transactions. This difference in financial transactions is more than explained by a £153 billion underestimate in relation to the Term Funding Scheme, the size of which we expected to decline by £63 billion, whereas it actually rose by £90 billion as a result of being extended by the Bank of England to provide additional support to the economy through the worst of the pandemic.

Our March 2021 fiscal forecast differences for 2021-22

Public sector net borrowing

3.10 Borrowing in 2021-22, at £125.4 billion, fell short of our March 2021 forecast by £108.6 billion (46.4 per cent), our second largest absolute year-ahead forecast difference in a Spring forecast after the pandemic-induced £258.0 billion underestimate for 2020-21 relative to our March 2020 forecast. As Chart 3.2 shows, this difference is very largely the result of receipts exceeding our forecast by £95.4 billion (11.6 per cent) – driven by economic factors and fiscal forecasting differences rather than subsequently announced policy. In addition, we overestimated spending by £13.2 billion as a result of both policy changes and other factors.

Chart 3.2: Sources of March 2021 borrowing forecast difference for 2021-22

Receipts

3.11 By re-running our March 2021 forecast models using outturn determinants in place of our March 2021 economy forecast, we can drill down into the sources of the £95.4 billion underestimate of receipts (detailed in Table 3.2). This exercise shows that this historically large forecast difference is explained by a combination of:

Economic factors (£35.7 billion) – in particular our underestimate of wages and salaries and private consumption (discussed in Chapter 2) which are the main tax bases for income taxes and VAT, the largest sources of tax revenue.

Fiscal forecasting differences (£61.8 billion) – particularly in relation to growth in tax-rich parts of the income distribution and the concentration of profits in certain sectors (and very large companies) that have typically been large payers of corporation tax. These differences are explored for the main taxes below.

Contributions from tax policy changes and classification changes only had a modest offsetting effect, lowering receipts by £0.9 billion and £1.2 billion respectively.[15]

Table 3.2: Breakdown of March 2021 receipts forecast differences for 2021-22

3.12 Our March 2021 forecast underestimated 2021-22 income tax and NICs receipts by £40.9 billion (11.9 per cent). This large upside surprise mostly reflects the unanticipated strength in economic factors, contributing £24.2 billion of the difference, while fiscal forecasting differences explain a further £16.8 billion. Taking the different elements of income tax and NICs in turn (detailed in Table 3.3):

The £35.9 billion underestimate of PAYE income tax and NICs receipts was largely driven by a £23.9 billion underestimate relating to economic factors, in the form of higher average earnings and higher employee numbers than anticipated. This partly reflects the fact that our PAYE income tax and NICs forecasts were framed by judgements around what would happen after CJRS closed:we anticipated a large rise in unemployment following the end of the scheme at the end of September 2021 that did not materialise, as explored in Box 3.5 of our March 2022 Economic and fiscal outlook (EFO). Fiscal forecasting differences of £12.0 billion account for the rest of our PAYE underestimate, largely due to stronger-than-expected aggregate pay growth within higher tax bands as fiscal drag brought more people than anticipated into higher tax brackets (explored in Box 3.2 of our March 2022 EFO). As a result, the effective tax rate on PAYE income in 2021-22, at 36.1 per cent, was 2.1 percentage points higher than that implied in our March 2021 forecast. A further £2.3 billion of the fiscal forecasting difference for PAYE income tax stems from the previous year’s estimate being too low, so the starting point for the forecast was higher.

We underestimated self-assessed (SA) income tax in 2021-22 by £6.3 billion. This is more than explained by a fiscal forecasting difference of £6.4 billion. With SA income tax receipts in 2021-22 largely relating to tax liabilities incurred during 2020-21, this reflects incomes recorded in SA returns performing much better than implied by the corresponding economic determinants in 2020-21. For example, SA returns data show growth in sole-trader and partners income of 6.0 per cent, relative to a forecast fall of 5.1 per cent. This discrepancy was driven by the fall in the number of sole traders and partnerships being smaller than implied by the Labour Force Survey data that underpinned the forecast,[16] alongside the SEISS cushioning incomes for those who were eligible to a greater extent than anticipated (both explored in detail in paragraph 3.34 of our March 2022 EFO). Similarly, SA returns show a 7.6 per cent fall in dividend income in 2020-21, smaller than the 13.7 per cent fall in our March 2021 forecast.

Table 3.3: Breakdown of March 2021 income tax and NICs forecast differences for 2021-22

£ billion

Forecast

Outturn

Difference, of which:

Total

Classification changes

Policy changes

Economic factors

Fiscal forecasting difference

Income tax (gross of tax credits)

198.2

225.0

26.8

0.0

0.0

15.5

11.3

of which:

Pay as you earn (PAYE)

170.8

192.6

21.8

0.0

0.0

15.2

6.6

Self assessment (SA)

30.7

37.0

6.3

0.0

0.0

0.0

6.4

Other income tax

-3.3

-4.6

-1.3

0.0

0.0

0.2

-1.6

National insurance contributions

146.8

160.9

14.1

0.0

0.0

8.7

5.4

VAT

3.13 VAT receipts in 2021-22 were £14.7 billion (11.5 per cent) higher than expected in our March 2021 forecast. Economic factors explain around a third of the difference (£5.7 billion), with nominal consumption outperforming our economy forecast due to faster-than-expected recovery of demand (discussed in Chapter 2). The remaining £9.0 billion difference between our March 2021 forecast and outturn is due to fiscal forecasting differences, including: a £5.1 billion difference related to allocating cash payments at the turn of the financial year between accruals years;[17] a £1.4 billion difference stemming from a smaller-than-expected VAT gap; higher-than-expected spending on standard-rated goods accounting for £1.4 billion; and a further £0.4 billion difference from policy measures announced before March 2021 having a more positive impact on VAT receipts than anticipated. The remaining £0.7 billion is an unexplained residual difference.

Onshore corporation tax

3.14 Onshore corporation tax (CT) receipts in 2021-22 were £23.1 billion (58.6 per cent) higher than expected in our March 2021 forecast, the largest forecast difference for this tax since the OBR’s inception. Receipts from non-oil, non-financial companies were £15.9 billion higher and receipts from the financial sector £6.0 billion higher. Our March 2021 forecast assumed a 12 per cent year-on-year fall in receipts in 2021-22, more than explained by the introduction of the two-year super-deduction capital allowance measure from April 2021 being expected to reduce receipts in 2021-22 by £12.3 billion.

3.15 Economic factors, mainly higher-than-expected 2021 profits for both the non-oil, non-financial sector and the financial sector, explain £2.3 billion of the overall difference. Non-oil, non-financial profits rose by 5 per cent in 2021, compared with a fall of 0.1 per cent in our March 2021 forecast. Financial company profits rose by 25 per cent in 2021, compared with a forecast of 8 per cent growth. These estimates remain subject to change given the likelihood of National Accounts revisions and the fact that that the CT returns available later in the year will provide a better estimate for financial company profits.

3.16 The much larger £21.2 billion fiscal forecasting difference reflects a range of factors:

The starting point for the CT forecast was stronger than we assumed in March 2021. Helped by government grants and loan schemes as well as the furlough scheme, profits in 2020 held up better than expected: profit growth in the non-oil, non-financial sector is now estimated at 2.2 per cent, whereas in March 2021 we assumed a 3.6 per cent fall. Likewise, cash receipts in 2021-22 relating to 2020 profits (and therefore accruing back to 2020-21) were stronger than expected, raising the latest accrued CT outturn for 2020-21 by £8.4 billion relative to our March 2021 forecast.

The estimated cost of the super-deduction in 2021-22 has been revised down from £12.3 billion to £9.3 billion, reflecting a lower estimate of the peak amount of business investment brought forward by the measure from 10 per cent to 5 per cent.[18] These figures are still subject to uncertainty given the difficulty of establishing the counterfactual of how business investment would have evolved absent the measure.

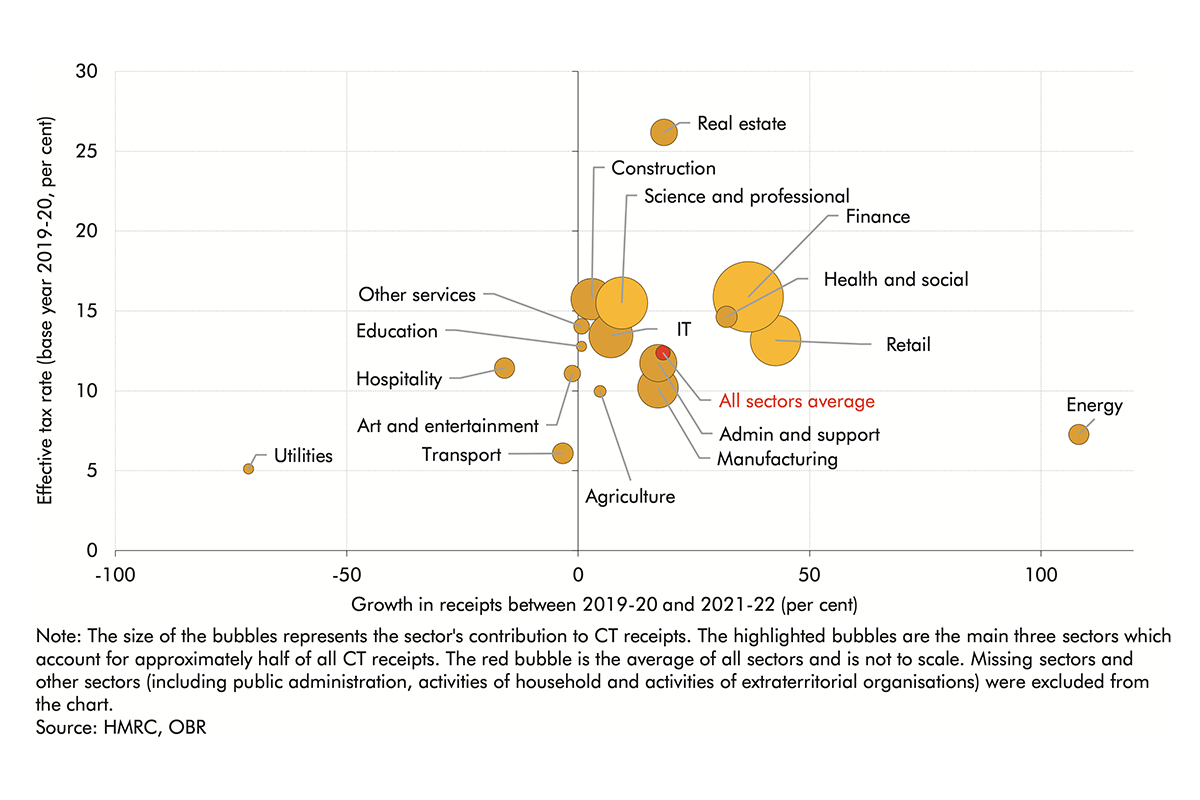

The strength of receipts in 2021-22 was concentrated in a few, relatively tax-rich sectors of the economy and among very large companies. HMRC administrative data indicate that over 60 per cent of the growth in receipts during 2021-22 comes from three sectors (the financial sector, professional services and retail) that have typically been large payers of corporation tax and performed better than the economy as a whole through the pandemic (Chart 3.3). Receipts from the financial sector benefited from strong profits in investment banking and the writing back of some of the loan-loss provisions made in 2020. Professional services benefited from stronger demand for consultancy services and the rise in government procurement, while supermarkets saw rises in profits as people switched to online deliveries. In contrast, some of the sectors most affected by the pandemic such as hospitality, arts and entertainment were not large payers of corporation tax prior to the pandemic. Our March 2021 forecast did not sufficiently anticipate these sectoral shifts. By size of company, very large companies (those with profits greater than £20 million) explain around £18 billion of the overshoot.

Our assumption that a pandemic-related spike in losses in 2020-21 would be, in part, carried forward and used against future profits was not borne out. While we do not have information on 2021-22 losses yet, CT returns data from 2020-21 do not point to a spike in losses, reducing the scope for losses to be used to offset 2021-22 profits.

Finally, it is possible that profits growth – an area that is particularly difficult to measure – was faster in 2021-22 than is currently recorded in the National Accounts. This would result in a greater share of our CT underestimate being accounted for by economic factors and a smaller share by fiscal forecasting differences (as explored in Box 3.1 in our March 2022 EFO).

Chart 3.3: Onshore corporation tax growth in 2021-22 versus pre-pandemic average effective tax rates by sector

Other receipts

3.17 Our March 2021 forecast underestimated 2021-22 receipts from other areas by £16.7 billion (5.4 per cent), largely explained by fiscal forecasting differences. This includes:

Capital gains tax (CGT) receipts in 2021-22, at £15.3 billion, exceeded our March 2021 forecast by £6.6 billion (76.1 per cent) – the largest surprise relative to our CGT forecasts since our inception. This is almost entirely explained by a fiscal forecasting difference of £6.4 billion, primarily driven by a small number of high-value financial asset disposals in 2020-21 (like SA income tax, CGT receipts largely relate to liabilities in the previous financial year). As discussed in our March 2022 EFO, this could reflect forestalling against feared tax rises (precipitated by an Office of Tax Simplification report in November 2020)[19] that did not come to pass.

We underestimated stamp duty land tax (SDLT) receipts by £3.0 billion (26 per cent), which can largely be attributed to economic factors (accounting for £2.1 billion of the difference), thanks to faster-than-expected growth in property prices and transaction volumes. The remaining difference (£0.9 billion) largely relates to our commercial SDLT forecast, reflecting above-average growth in high-value commercial property purchases. For example, the annual growth in liable commercial transactions with a value of over £2 million in 2021-22 was 50 per cent, compared to aggregate growth of 31 per cent. As the SDLT forecast is based on a model that uses aggregate expected growth rates to calculate receipts, this compositional shift towards higher-value properties will not have been fully captured in our March 2021 forecast.

We underestimated business rates receipts by £1.5 billion (6.5 per cent), despite subsequent policy changes in the Autumn Budget 2021 in the form of additional pandemic-related reliefs to sectors outside retail, hospitality and leisure, lowering receipts by £1.0 billion. This was offset by a classification change of £0.4 billion in relation to methodological changes that the ONS introduced in September 2022, and a £2.2 billion fiscal forecasting difference mainly related to the additional relief being paid out during 2022-23 rather than 2021-22 as originally assumed.

Box 3.1: Evaluating customs duties receipts in 2021-22, the first post-Brexit year

The UK’s post-Brexit trading regime with the EU was set out in the ‘UK-EU Trade and Cooperation Agreement’ (TCA), which was concluded on 24 December 2020 and came into effect from 1 January 2021. Following our departure from the EU, UK trade with non-EU countries that is not subject to other free-trade agreements is now subject to the new UK Global Tariff (UKGT), which typically imposes lower average tariffs than the EU’s Common External Tariff it has replaced. The UKGT rates are also levied on those imports from the EU that do not meet the terms of the TCA (for example, rules-of-origin requirements).a

Customs duties raised a total of £4.8 billion in 2021-22, £0.9 billion (23 per cent) higher than we forecast in March 2021, and £1.6 billion (49 per cent) higher than our March 2020 forecast (which did not factor in the TCA). The total value of imports in 2021-22 was not materially different from these previous forecasts, although the composition in terms of goods and services and EU versus non-EU trade did differ (with fewer EU imports and more non-EU imports). Rather, the main factors explaining the observed surpluses in revenues from customs duties have been higher-than-expected receipts from EU imports (due to a lower-than-expected share of EU imports arriving tariff-free) and a shift in the composition of imports (notably a rise in electric vehicle imports from China). We explore each factor in this box.

EU imports: lower-than-expected preference utilisation rates

The UKGT was first included in our forecast as a policy costing in our November 2020 EFO. We expected it to raise £1.4 billion in additional customs duties from EU imports in 2021-22. The two sources of this revenue are those imports now subject to tariffs that wereb previously exempt, and imports from traders that are unable or unwilling to take advantage of tariff-free trade under the terms of the TCA – captured via assumptions about the share of imports in different categories that are expected to utilise the preferential treatment on offer.

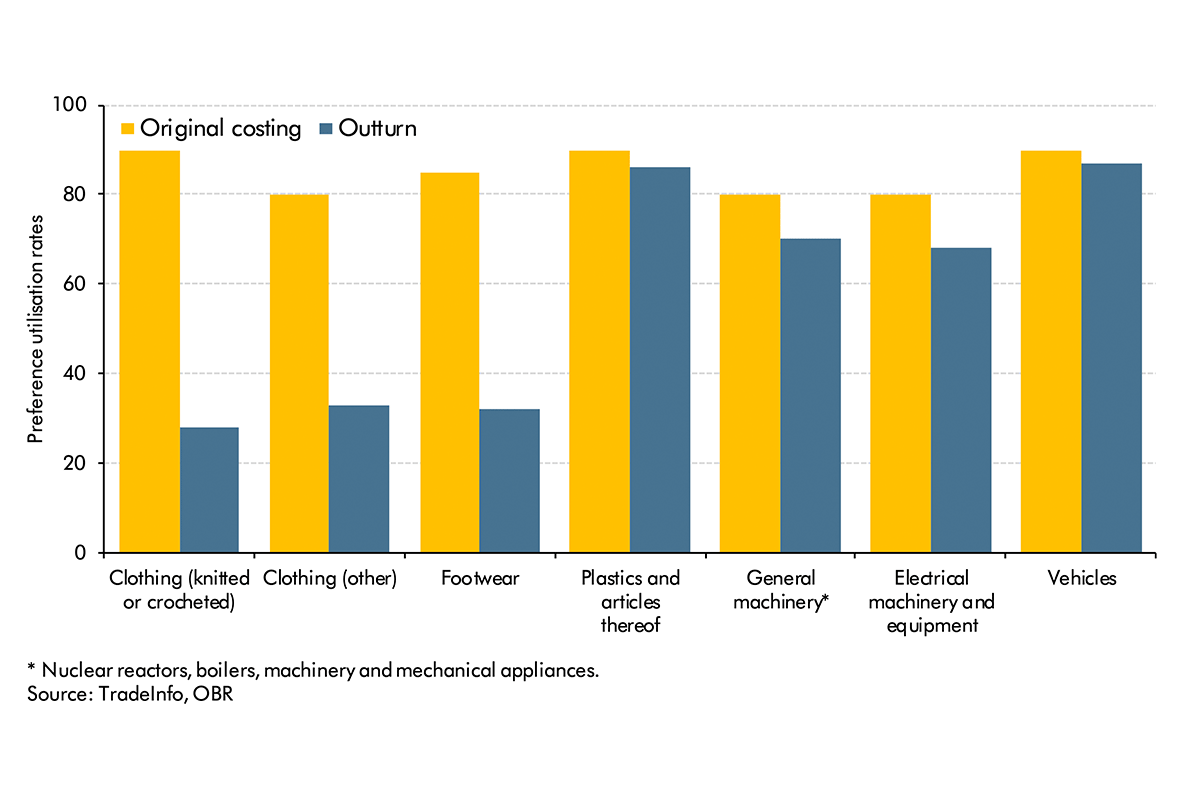

Preference utilisation rates (PURs) record the degree to which the favourable terms agreed in FTAs such as the TCA are used in practice, with 100 per cent signifying full usage. In every FTA there are some traders that cannot meet the rules-of-origin requirements and others for whom the administrative cost of doing so is greater than the tariff saving on offer. In the original costing, using evidence from previous FTAs, we assumed that PURs would typically fall in the 80 to 90 per cent range. Chart A shows several key sectors that have fallen well short of this.

Chart A: Preference utilisation in selected sectors in 2021-22: assumed vs outturn

The largest shortfalls are in the clothing and footwear sectors, where the average PUR during 2021-22 was only around 30 per cent, less than half the rate originally assumed. The shortfall in the other sectors is less pronounced in percentage terms but is material for revenue because they account for higher values of imports. We estimate that these sectors combined generated £1.3 billion of customs duties from EU imports in 2021-22 (with £0.6 billion of the total coming from clothing and footwear). That was £0.8 billion (170 per cent) more than assumed in the original costing. We now estimate that EU imports in total raised £2.1 billion of customs duties in 2021-22 – all of which is additional to our March 2020 forecast, which pre-dated the TCA, and £0.7 billion of which is additional to the March 2021 forecast (a 50 per cent overshoot).

Having initially thought that the low PURs might reflect teething problems that would pass, we now assume only a modest rise in PURs during our current forecast horizon since some of the contributory factors (such as more existing supply chains in European clothing and footwear retailing originating outside the EU) appear to be structural.

Changes in the composition of imports

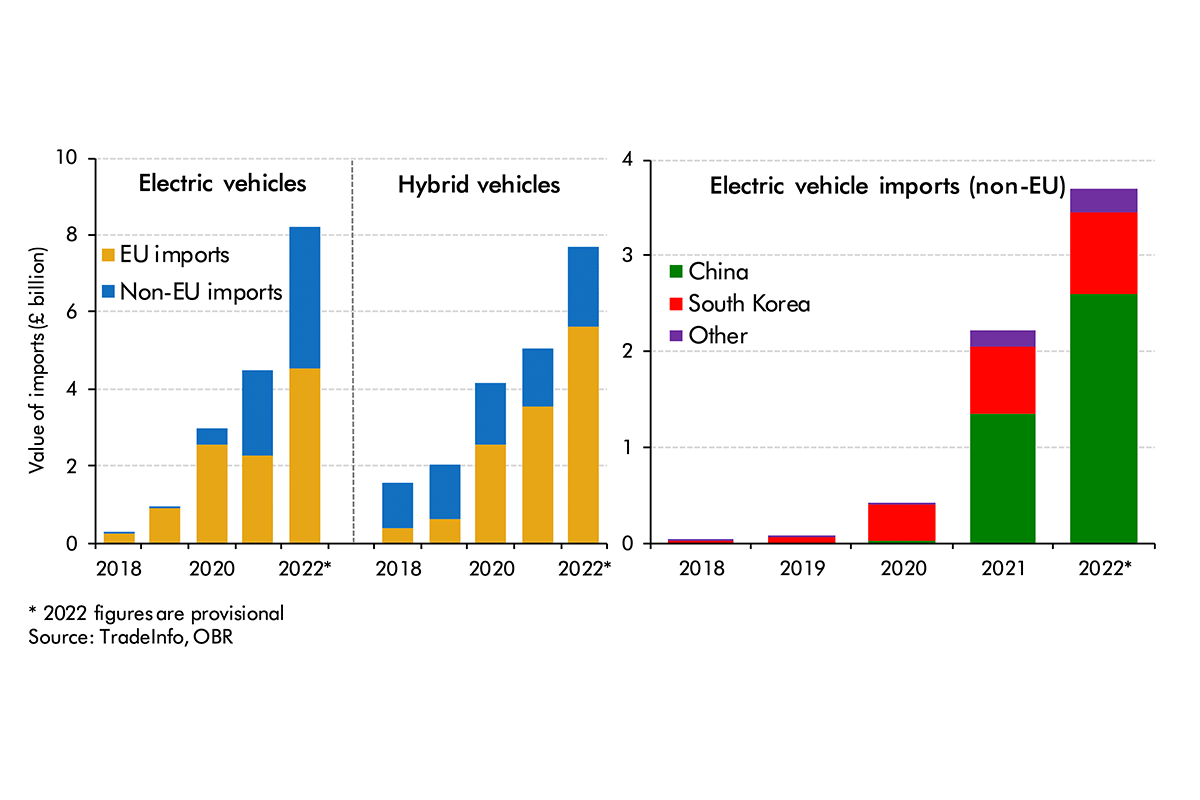

A second factor that explains higher-than-expected receipts in 2021-22 is the growth in the imports of electric and hybrid vehicles. Chart B (left panel) shows an eight-fold increase in imports over just four years, from £1.9 billion in 2018 to £15.9 billion in 2022. The impact from EU imports is captured in the discussion above, so we focus here on non-EU imports. The forecasts we are evaluating made no explicit assumptions about these imports, instead implicitly assuming that they would grow in line with total imports, so this rapid growth in relatively high-tariff imports represents news relative to our forecasts.c While non-EU imports of hybrid vehicles have increased relative to expectations, the growth in electric vehicles has been more surprising still, with negligible imports in 2019 rising to £3.7 billion in 2022.

The most notable growth (Chart B, right panel) is from China (and the UK’s FTA with South Korea makes the growth in imports from there less relevant when explaining the customs duty surplus). We estimate that the unanticipated growth in imports from China explains around £0.2 billion of the surplus relative to both our March 2020 and March 2021 forecasts.

Given the importance of this trend to our customs duty revenue forecast, we have since aligned our assumptions about future growth in dutiable imports of electric vehicles to the growth in electric vehicle sales assumed in our fuel duty and vehicle excise duty forecasts.

Chart B: Imports of electric and hybrid vehicles

A second compositional factor is the share of non-monetary gold in total imports. Non-monetary gold is traded tariff-free. Its share of total imports is large because London is the world’s major centre for such trade, and it can be volatile from year to year – it was 11 per cent in 2019-20, rose to 14 per cent in 2020-21 but then fell to 7 per cent in 2021-22. We estimate that the drop in the proportion of non-monetary gold imports increased receipts by an average of £0.3 billion relative to the flat shares assumed in our March 2020 and March 2021 forecasts.

a Rules-of-origin are the criteria used to determine the source country of an imported good and, among other things, whether it qualifies for most-favoured or preferential treatment. This is sometimes called the good’s ‘economic nationality’. Trade agreements between countries usually specify that, to qualify for preferential rates, a trader must demonstrate that a proportion of the value of the good, say 50 per cent, has originated in the exporting country. This threshold can be challenging to meet for those goods produced within a global supply chain spanning several countries, where multiple components add value. It also disqualifies goods that are offloaded in the EU before being ‘transhipped’ to the UK from benefiting from preferential TCA rates.