On 1 January 2021 some, but not all, of the provisions of the Trade and Cooperation Agreement came into effect following the UK's departure from the EU. In this box we looked at the initial impact of the new regime on UK trade patterns. We also considered whether the data was consistent with our assumption that Brexit will eventually reduce UK imports and exports by 15 per cent.

This box is based on ONS and OBR data from October 2021 .

Since our first post-EU referendum EFO in November 2016, our forecasts have assumed that total UK imports and exports will eventually both be 15 per cent lower than had we stayed in the EU. This reduction in trade intensity drives the 4 per cent reduction in long-run potential productivity we assume will eventually result from our departure from the EU.

While the UK left the EU on 31 January 2020, the transition period meant that trading terms between the UK and EU were unchanged until 1 January 2021 when some, but not all, of the provisions of the Trade and Cooperation Agreement (TCA) came into effect. We expect the full impact of Brexit on trade to be manifest only after all the terms of the TCA have been fully implemented and businesses have had time to adjust fully to the change in trading conditions, including reorganising their supply chains. Initial data under the new regime may nevertheless provide early insights about the impact of Brexit and the TCA on UK trade patterns.

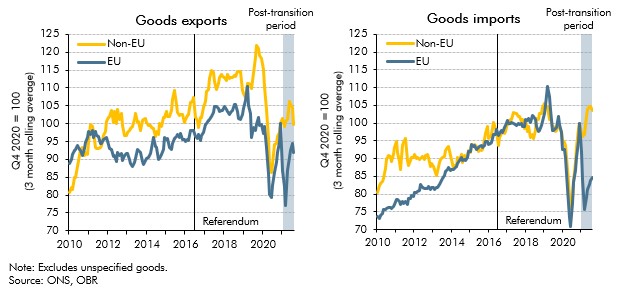

UK-EU goods trade volumes fell sharply after the TCA came into effect, and remain below their pre-Brexit (and pre-pandemic) levels in 2019. Chart E shows that UK goods exports to the EU fell by 45 per cent in January of this year (greater than their fall early in the pandemic) and in August were still down around 15 per cent on the level before the transition period ended. UK goods imports from the EU also fell by over 30 per cent at the start of the year and were still down around 20 per cent in August compared to December 2020. While goods trade with the rest of the world experienced similarly sharp falls at the start of the pandemic, in August it had recovered to 7 per cent below average 2019 levels whereas total goods trade with the EU remained down 15 per cent.a

Chart E: EU and non-EU goods trade

Of course, some of the recent disruption to trade was associated with the onset of the pandemic in early 2020, the more stringent testing of lorry drivers initiated in response to the spread of the Alpha variant at the turn of the year, and the emergence of supply bottlenecks as the global recovery gathered pace. The Centre for European Reform has attempted to isolate the impact of Brexit using a ‘doppelganger UK’ (constructed as a weighted average of other countries’ gross goods trade flows) as a counterfactual for what would have happened had the UK remained in the EU. That analysis concluded that, since the transition period ended, leaving the single market and customs union had reduced UK goods trade by 15.8 per cent as of August 2021.b

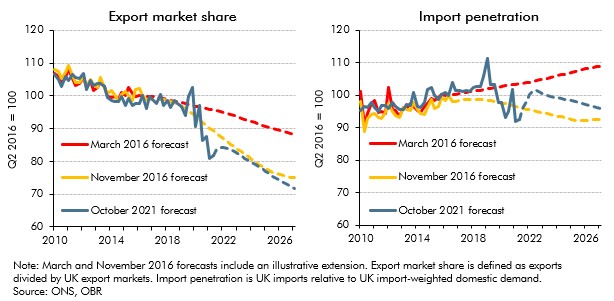

Chart F shows that the UK’s export market share (UK exports relative to total imports in the countries the UK exports to) and import penetration (the degree to which UK domestic demand is

satisfied by imports) are still broadly tracking our post-referendum forecast from November 2016 despite the disruption of the pandemic and the fact Brexit was delayed compared to our initial assumption. This suggests that UK trade was lowered even before trading conditions with the EU changed, potentially due to anticipatory effects and the uncertainty created by the EU referendum.c

Chart F: Export market share and import penetration

In summary, the evidence so far suggests that both import and export intensity have been reduced by Brexit, with developments still consistent with our initial assumption of a 15 per cent

reduction in each. It is, however, too early to reach definitive conclusions because:

- The terms of the TCA are yet to be implemented in full, meaning trade barriers will rise further as more of the deal comes into force. For example, the introduction of full checks on UK imports has recently been delayed until 2022.

- The full effect of the referendum outcome and higher trade barriers will probably take several years to come through, with businesses needing considerable time to adjust.

- The pandemic has delivered a large shock to UK and global trade volumes over the past 18 months, making it difficult to disentangle the separate effect of leaving the EU.

- Finally, trade data tend to be relatively volatile and are revised frequently, rendering any initial conclusions subject to change as the data are revised.

We will keep our assumptions under review as more information becomes available.

This box was originally published in Economic and fiscal outlook – October 2021