There is growing literature on the economic costs of climate change, where there is near-consensus on the negative impact on economic output but with a wide range of estimated losses. This box explored the the scale of, and reasons for, such differences and examined relevant UK studies in this context.

This box is based on R. Tol's meta-analysis data from February 2024 .

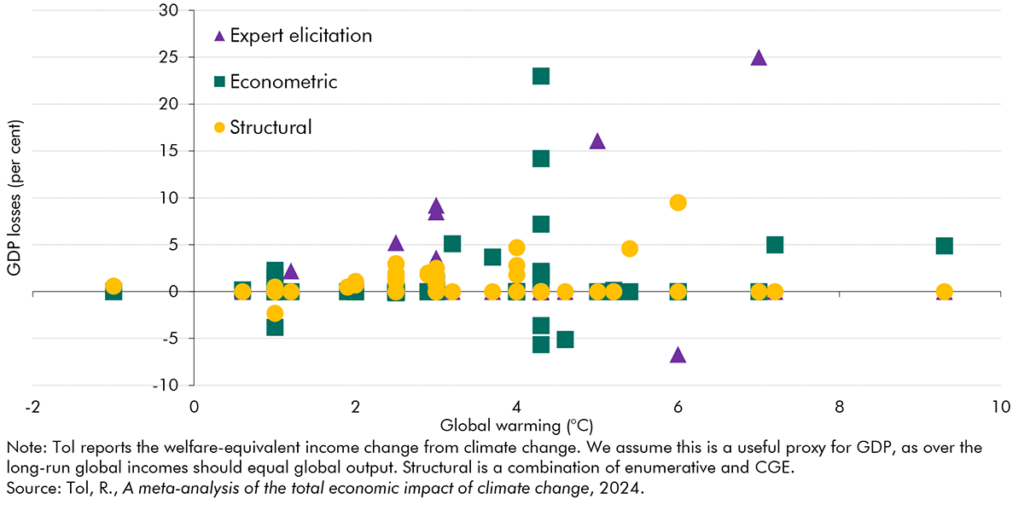

A near-consensus amongst economic studies is that the impact of global warming on economic output will be negative, with more warming leading to larger impacts.a However, there is a wide range of estimated GDP losses and making comparisons between them is not simple. For instance, as shown in Chart A, one comprehensive meta-study suggests that the estimates of long-run total loss of global GDP from global warming of 4°C are on average minus 4.2 per cent, but range between minus 23 and plus 6 per cent.b

The wide range of estimates partly arises from differences in both the physical impacts assumed and the corresponding economic transmission channels which the authors aim to capture. For example, studies vary in whether chronic or acute climate impacts, or both, are being captured and which aspects of the economy they impact. Some estimates are the result of examining such impacts in the context of the domestic economy only, while others also consider the international linkages through cross-country trade and investment. Another source of difference comes from the modelling approaches used. These include:

- Structural models, which employ existing relationships between economic variables and their interactions with the physical environment (such as General Equilibrium models).

- Econometric models, which empirically link past changes in temperature with changes in economic output.

- Expert elicitation, which uses expert judgment to calibrate the effects of climate change.

Chart A: Estimates of the long-run economic impact of climate change

As Chart A highlights, estimates of the economic impact of climate change obtained from econometric models are the most varied. In contrast, structural models, which are likely to explicitly model a finite subset of channels and allow for general equilibrium effects (i.e. reallocation of factors), tend to yield the smallest effects. Studies that only capture chronic effects and their domestic effects also tend to find less economic impact. The biggest effects are generally found in studies that capture: (i) both chronic and acute effects; (ii) both domestic and international transmission; and (iii) use econometric models. The largest effects for a given rise in temperature also often come from expert elicitation though some commentators have questioned these results.c

Impacts are also heterogenous across regions. For instance, Kalkuhl and Wenz (2020), an econometric study of chronic temperature impacts that underpins the NGFS scenarios, finds that there is a -0.8 per cent impact on GDP for every degree of additional heating in a relatively cool country.d Whereas in hotter regions, an additional degree of warming leads to 3.5 per cent of damage. This regional variance in economic impacts is confirmed by several other studies, which generally find that GDP impacts are higher for hotter countries, low-lying coastal countries, and places near the equator.

UK estimates

Given its geographic position, the UK’s projected temperature rise is less than most other regions in the world. As such, UK-specific estimates of the economic impact from climate change tend to

find less of an effect than the global average. The impacts are nonetheless significant compared to previous economic shocks the UK has faced.

Two of the most comprehensive studies of potential climate change-related damage to the UK economy generated estimates somewhat above our 5 per cent of GDP loss under a below 3°C scenario:

- The Bank of England’s 2021 Climate Biennial Exploratory Scenarios included a ‘no additional action’ scenario which estimated that 3.3 degrees of warming results in a -7.8 per cent impact on GDP in the UK in 2050.e This scenario, as with the unadjusted NGFS figures, was produced for the purposes of stress testing, and models both chronic and acute climate impacts through domestic and cross-country effects.

- The Grantham Research Institute estimated that 3.9 degrees of global warming produces a -3.3 per cent impact on UK GDP by 2050, and a -7.4 per cent impact by 2100.f These figures, in addition to capturing both chronic and acute climate impacts through domestic and cross-country effects, include a ‘catastrophic risk’ channel which makes up 4.1 percentage points of this impact. As such, it may be capturing channels we have not attempted to calibrate.

This box was originally published in Fiscal risks and sustainability – September 2024