The capital tax measures announced in the October 2024 Budget affected an overlapping set of taxpayers and tax bases, mainly across capital gains tax, inheritance tax and income tax. In this box, we considered how individuals can respond to an increase in a capital tax liability, and what we assumed about these behaviours in our costings for capital tax measures.

This box is based on Tax Policy Associates and ONS data from October 2024 .

The capital tax measures announced in this Budget affect an overlapping set of taxpayers and tax bases. Together these measures are expected to raise £5.2 billion by the end of the decade, mainly across capital gains tax (CGT), inheritance tax (IHT) and income tax (IT). These costings are among the most uncertain in the policy package, reflecting the range of potential behavioural responses, the sensitivity of the yield to the decisions of a small number of high net-worth individuals, and interactions across measures.

Costings of tax measures produced by HMRC always account for material behavioural responses by individuals or businesses, and we also assess any indirect effects on the wider economy.a These responses are typically captured through the use of elasticities, which estimate the extent of the change in behaviour with respect to a change in either the tax rate or the share of gains an individual retains after a disposal or transaction, or parameters applying to specific behavioural channels. Broadly speaking, individuals can respond to an increase in a capital tax liability through:

- Changing the timing of asset disposals or transactions, either by forestalling (bringing activity forward) while conditions remain favourable, or ‘locking in’ (delaying) based on a belief that conditions will be more favourable in future, or even until death, to allow inheritors to benefit from capital gains rebasing.

- Shifting between different assets, or between gains and income, to take advantage of differences in effective tax rates. Individuals may also choose to run down their assets, in effect converting them to cash to be gifted or spent, in response to a higher IHT liability.

- Tax planning to reduce the effective tax rate faced, through use of reliefs, gifts, or specific vehicles with a more favourable tax treatment.

- Migration, either becoming non-UK resident for tax purposes, or diverting some or all activity to jurisdictions where the tax liability is lower.

- Non-compliance, by non-payment, misreporting or underreporting of chargeable assets, gains or income.

Forestalling typically takes place when individuals have time to respond to a known change in a tax rate. This is incentivised by the staggered increase to the BADR rate announced in this Budget, but not possible for the increase in main CGT rates as it takes effect on the day of the Budget.b Shifting between asset classes, or between gains and income, is generally motivated by changes in relative tax rates. For example, higher main CGT rates reduce the attractiveness of structuring earnings as gains rather than income, while aligning the main rates of CGT with residential property discourages transfers across asset classes.

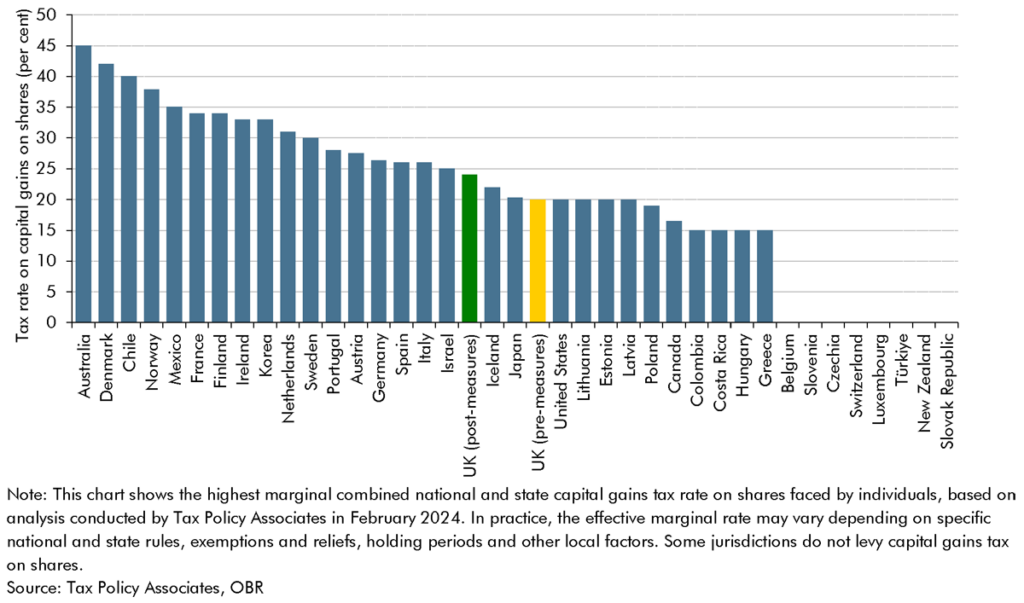

Migration in response to changes in capital taxes is more likely where the tax base is wealthy and internationally mobile, and where measures reduce the relative attractiveness of the UK as a jurisdiction. As such, we assume migration is not a significant factor in the response to the increase in the higher main rate of CGT at this Budget, as the headline rate in the UK remains among the middle of advanced economies (see Chart A).

Chart A: Highest marginal capital gains tax rates on shares by country

However, migration is assumed to be a significant behavioural response for non-domiciled taxpayers (as it was for the original reforms in March 2024) and for carried interest earners (where, as discussed in paragraph 3.18, the new effective tax rate is among the upper end of advanced economies). This is influenced both by these policy changes taken in isolation and the wider impacts of the capital tax package. The full package is assumed to increase migration by both these groups by a small amount in addition to the specific effects of the non-domicile and carried interest reforms, driven largely by the increase to the main CGT rates and increased IHT liabilities.

This box was originally published in Economic and fiscal outlook – October 2024