"It is the duty of the Office to examine and report on the sustainability of the public finances"

Economic and fiscal outlook – October 2024

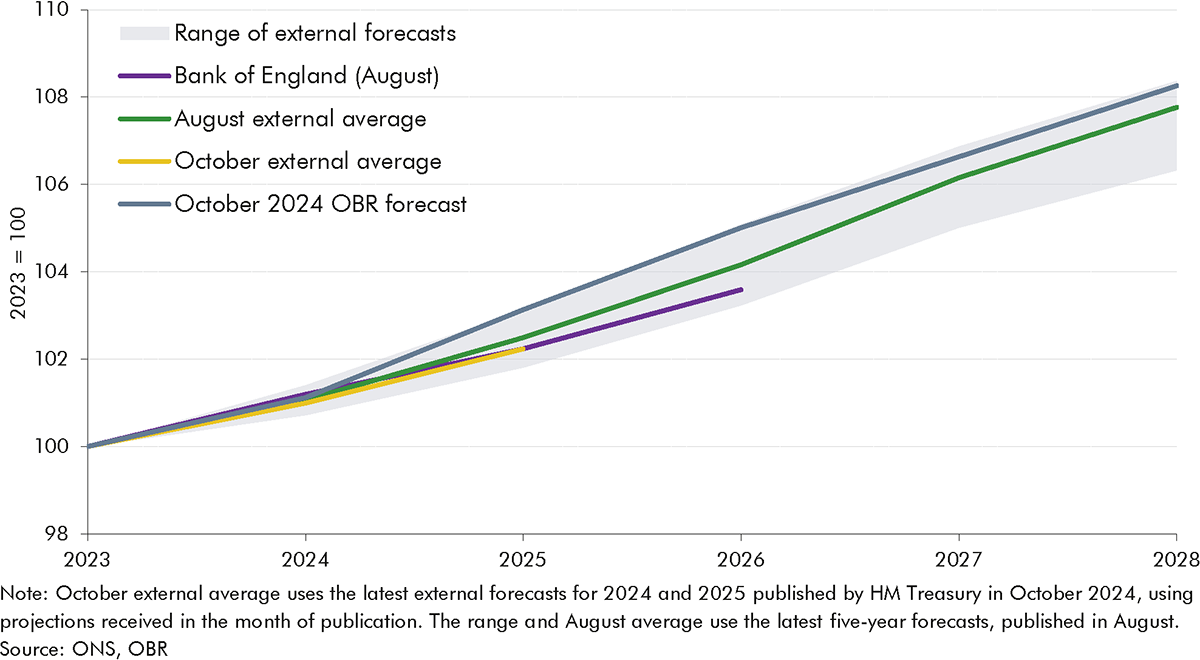

The latest update of our forecasts was published on 30 October 2024 in the October 2024 Economic and fiscal outlook. Read the Executive summary for the key messages of our forecast or the full report on our website.

Chapter 2 sets out our forecasts for the economy over a five-year horizon. We cover our latest forecast changes in light of recent developments and the effect of policies in the Autumn Budget.

In Chapter 3, details the policy measures announced since March 2024, provides an update on selected previous measures, and discusses policy risks and uncertainties.

Chapters 4-6 sets out our forecasts for receipts and public spending over a five-year horizon. We also explain our loans and other financial transactions forecasts. All this, together with new policy decisions, builds the outlook for borrowing and debt.

In Chapter 7, we assess the Government against its fiscal targets and assesses their likelihood of being met on current policy under our central forecast. We consider the uncertainty around our economic and fiscal forecasts and the risks to the Government meeting its targets. We also test the sensitivity of our fiscal forecasts in an alternative economic scenario.

Annex A contains detailed summary tables setting out our economic and fiscal forecasts.

Annex B explains public sector net liabilities (PSFNL) that the Government has announced as its new supplementary target.

This Economic and fiscal outlook (EFO) sets out our central forecast and the uncertainties that surround it for the five years to 2029-30, taking account of recent data and government policies announced up to and including the October 2024 Budget. The forecasts presented in this document represent our collective view as the three independent members of the OBR’s Budget Responsibility Committee (BRC). We take full responsibility for the judgements that underpin them and for the conclusions we have reached.

As always, we have been greatly supported in our work by the staff of the OBR. We are very grateful for their hard work and expertise. We have also drawn on the work and expertise of numerous officials across government in preparing these forecasts. We are grateful for their engagement and insight.

The date for this forecast was announced on 29 July, giving four weeks more than the ten weeks’ notice required by the Memorandum of understanding between the Office for Budget Responsibility, HM Treasury, the Department for Work and Pensions and HM Revenue and Customs (MoU).

We published the timetable of the key stages of the forecast on 21 August, once it had been agreed by signatories of the MoU. On this occasion, the timetable was adjusted to permit 24 working days instead of the MoU-prescribed 21 days between our final pre-measures economy forecast and the Budget date to allow sufficient time to finalise the pre-measures fiscal forecast and to incorporate major Budget policy decisions after the completion of this pre-measures forecast. Overall, the forecast process for this EFO proceeded very smoothly given the size of the Budget package. The timetable was adhered to at each of the following stages:

OBR staff prepared an initial economy forecast, drawing on data released since our previous forecast in March 2024 and incorporating our preliminary judgements on the outlook for the economy. This first economy forecast was sent to the Chancellor on 3 September.

Using the economic determinants from this forecast (such as the components of nominal income and spending, unemployment, inflation, and interest rates), we commissioned updated forecasts from the relevant government departments for the various tax and spending items that in aggregate determine the position of the public finances. We discussed these in detail with the officials producing them, which allowed us to investigate proposed changes in forecasting methodology and to assess the significance of recent tax and spending outturn data. In many cases the BRC requested changes to methodology and/or the interpretation of recent data. This first fiscal forecast was finalised on 18 September, and we sent a note that described the main elements of it to the Chancellor the following day.

As the process continued, we identified further key judgements that we would need to make for our economy forecast. Where we thought it would be helpful, we commissioned analysis from the relevant teams in the Treasury. We then produced a second and final pre-measures economy forecast, which incorporated the latest data, and the economic implications of our first fiscal forecast. This final pre-measures economy forecast was based on energy and financial market data averaged over the 10 working days to 12 September. It was sent to the Treasury on 26 September.

This second economy forecast provided the basis for the next round of fiscal forecasts. Discussions with HMRC, DWP and other departments gave us the opportunity to follow up our requests for further analysis, methodological changes, and alternative judgements from the previous round. We finalised our second and final pre-measuresfiscal forecast on 7 October and sent a summary of the forecast to the Chancellor the following day.

In parallel, we undertook a process of engagement and analysis to assess the set of policy measures to be announced in the Budget that we deemed could have specific effects on our economy forecast, to inform our forecast judgements. This involved several rounds of engagement with the Treasury and other departments as both the specification of policy packages and our assessment of their impact were refined.

We also scrutinised the costing of individual tax and spending measures announced since our March 2024 forecast. As usual, OBR staff and the BRC requested further information and/or changes to almost all the draft costings prepared by HMRC and other departments. We have certified all policy measures in the forecast as reasonable and central.

Alongside the development of the final economy forecast we made an initial assessment of the economic and fiscal effects of the emerging policy package. This built on earlier analysis that allowed us to factor in an initial package of measures that was provided by the Treasury on 9 October. We incorporated this package into a preliminary post-measures forecast, in order to provide an early view on the effect of Budget measures on the economy and public finances, which we sent to the Chancellor on 14 October. This forecast round was produced using our internal ready-reckoner models (rather than being sent to departmental forecasters).

In line with the agreed timetable, on 16 October the Treasury provided the final package of measures that would cause movements in our economy forecast. We sent the resulting final economy forecast to the Treasury on 21 October and a near-final fiscal forecast on 22 October. Final policy decisions were provided by the Treasury on 23 October and our forecast was then finalised on 25 October and sent to the Treasury on the same day.

The Treasury made a written request, as provided for in the MoU between us, that we provide the Chancellor and an agreed list of her special advisers and officials with a near-final draft of the EFO on 25 October. This allowed the Treasury to prepare the Chancellor’s statement and accompanying documents. We also provided pre-release access to the full and final EFO on 28 October.

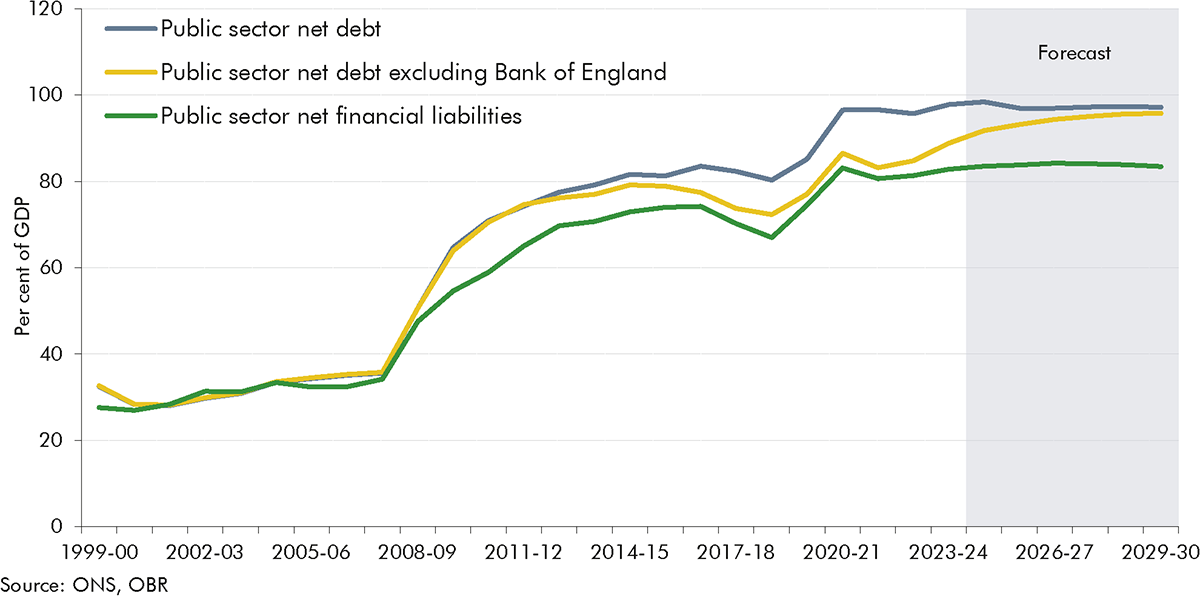

During the forecasting period, the BRC held dozens of scrutiny and challenge meetings with officials from other departments, in addition to numerous further meetings at staff level and with external stakeholders. We have been provided with all the information and analysis that we requested and have come under no pressure from Ministers, advisers or officials to change any of our conclusions as the forecast has progressed. The BRC met with the Chancellor on three occasions to discuss the forecast over the course of its production (on 11 September, 3 October and 23 October). A full log of our substantive contact with Ministers, their offices and special advisers can be found on our website. This includes the list of special advisers and officials who received the near-final draft of the EFO on 25 October.

Alongside this EFO, we have published the findings and recommendations of our review into the preparation of the March 2024 forecast for departmental expenditure limits (DEL). This forecast incorporates the recommendations of that review.

Our non-executive members, Dame Susan Rice and Baroness Hogg, provide additional assurance over how we engage with the Treasury and other departments. This includes reviewing any correspondence that OBR staff feel either breaches the MoU requirement that it be confined to factual comments only or could be construed as doing so. That review takes place as soon as practicable after each EFO has been published. Any concerns our non-executive members have will be raised with the Treasury’s Permanent Secretary or the Treasury Select Committee if they deem that appropriate.

We would be pleased to receive feedback on any aspect of the content or presentation of our analysis. This can be sent to [email protected].

The Budget Responsibility Committee

Richard Hughes, Professor David Miles CBE and Tom Josephs

Chapter 1: Executive summary

Overview

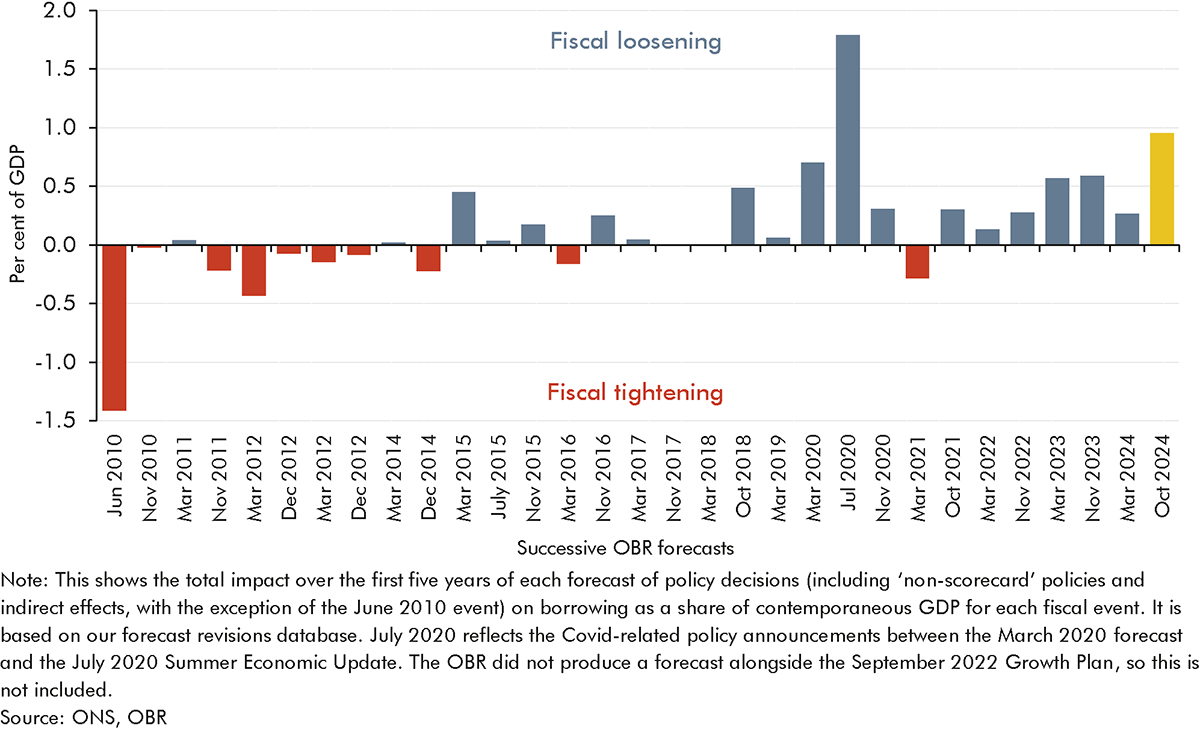

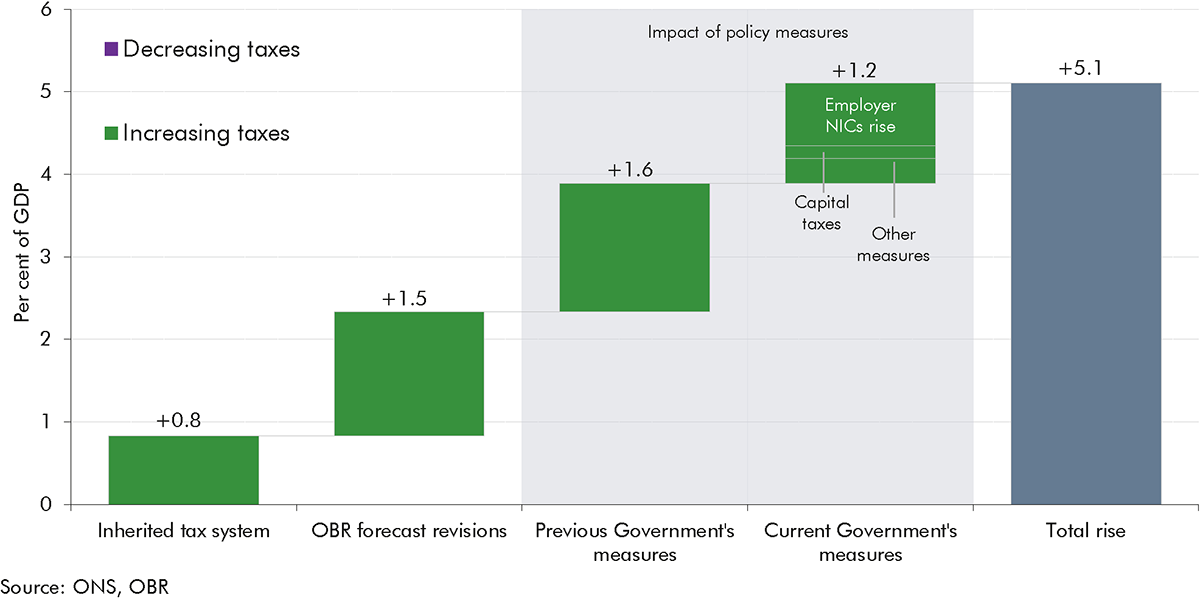

1.1 Against a broadly unchanged economic and fiscal backdrop since March, this Budget delivers a large, sustained increase in spending, taxation, and borrowing. Budget policies increase spending by almost £70 billion (a little over 2 per cent of GDP) a year over the next five years, of which two-thirds goes on current and one-third on capital spending. As a result, the size of the state is forecast to settle at 44 per cent of GDP by the end of the decade, almost 5 percentage points higher than before the pandemic. Half of the increase in spending is funded through an increase in taxes, mainly on employer payrolls, on assets, and through greater tax compliance. These raise £36 billion (just over 1 per cent of GDP) a year in additional revenue and push the tax take to a historic high of 38 per cent of GDP by 2029-30. The other half of the increase in spending is funded by a £32 billion (1 per cent of GDP) a year increase in borrowing, one of the largest fiscal loosenings of any fiscal event in recent decades.

1.2 Having stagnated last year, the economy is expected to grow by just over 1 per cent this year, rising to 2 per cent in 2025, before falling to around 1½ per cent, slightly below its estimated potential growth rate of 1⅔ per cent, over the remainder of the forecast. Budget policies temporarily boost output in the near term, but leave GDP largely unchanged in five years. If the increased level of public investment were sustained, it would permanently raise supply in the long term and by significantly more than it does in the forecast period. Budget policies push up CPI inflation by around ½ a percentage point at their peak, meaning it is projected to rise to 2.6 per cent in 2025, and then gradually fall back to target.

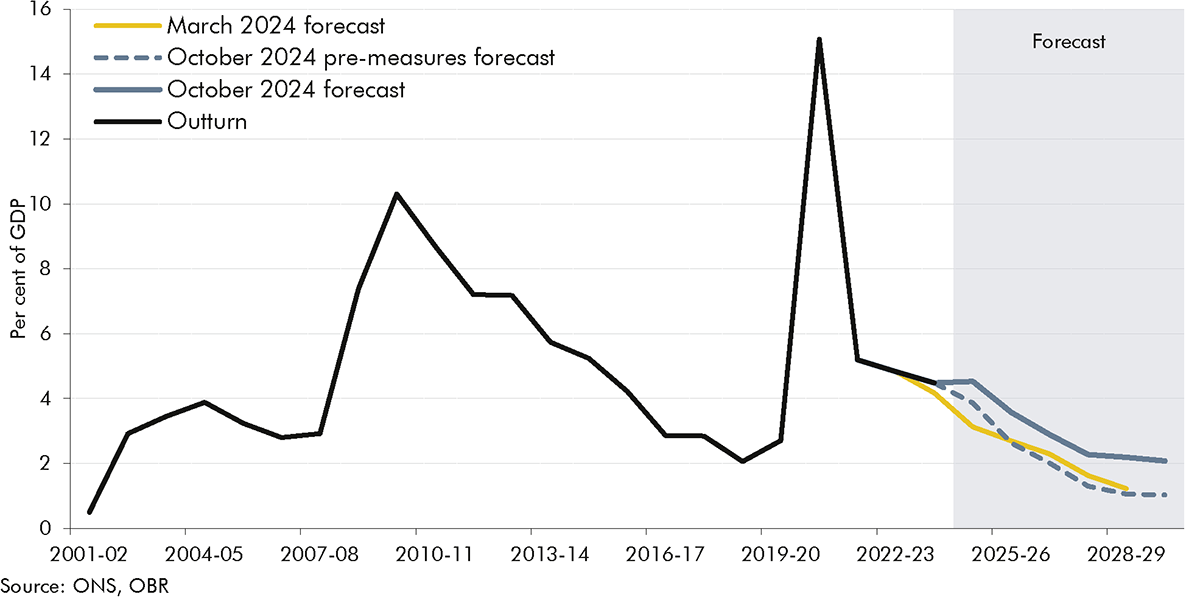

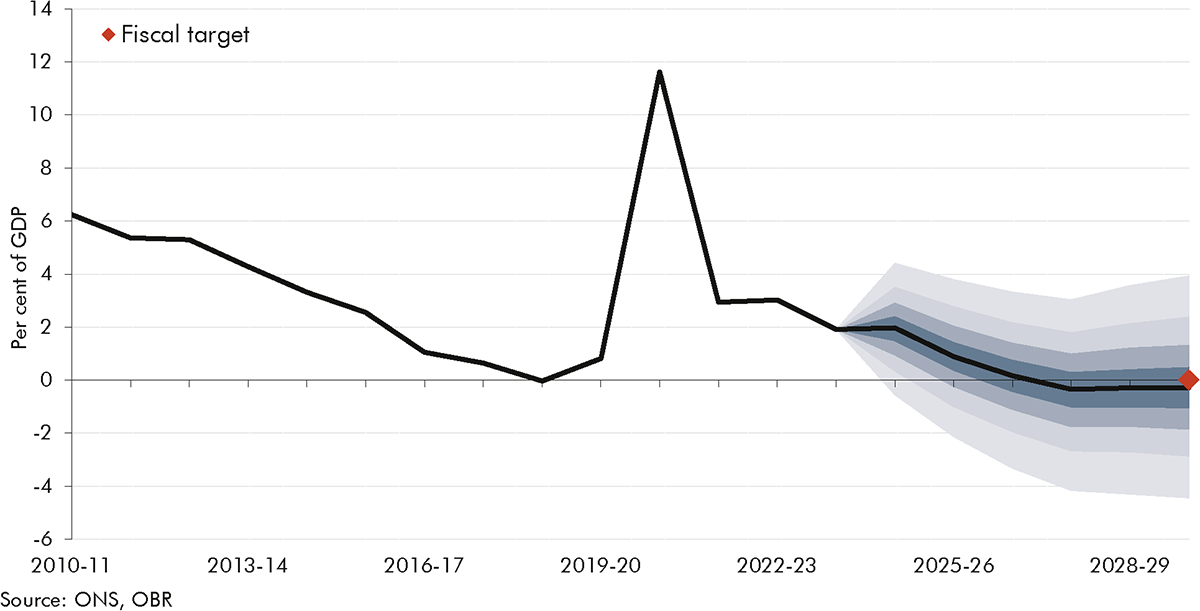

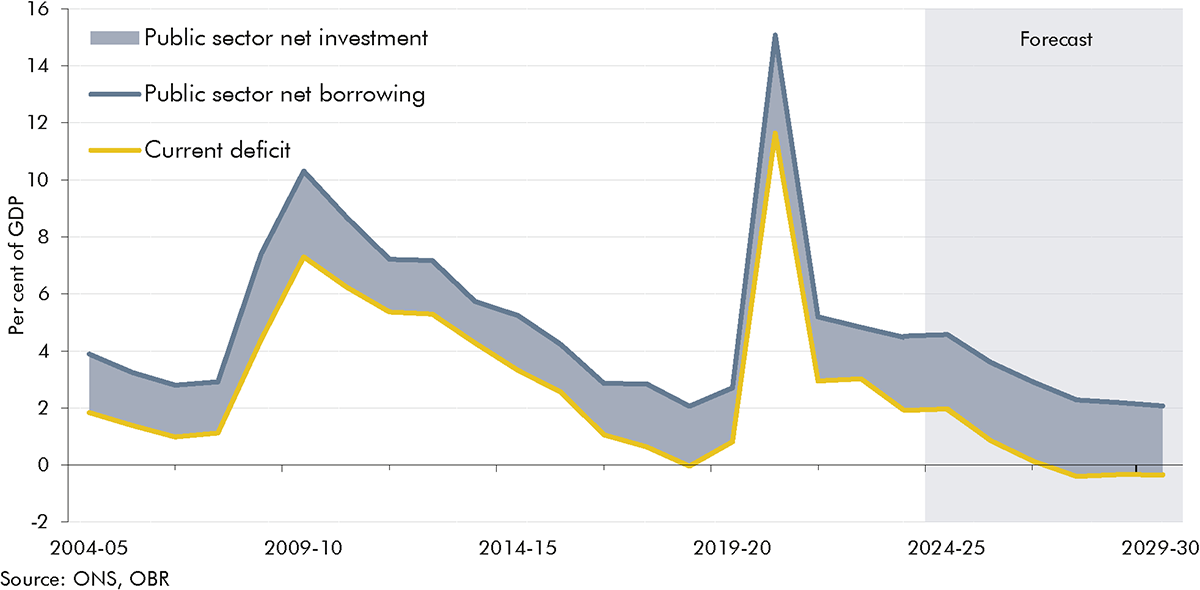

1.3 This Budget slows the pace of deficit reduction relative to the previous Government’s plans. Borrowing is projected to rise marginally from £122 billion (4.5 per cent of GDP) last year to £127 billion this year, before falling back to £71 billion (2.1 per cent of GDP) in 2029-30. Net debt falls as a share of GDP from 98.4 per cent this year to 97.1 per cent by the end of the decade. But underlying debt, excluding the Bank of England, rises as a share of GDP in every year of the forecast. The Budget sets two new fiscal rules: to deliver a current balance and for net financial liabilities to be falling, both initially in five years. On the central forecast they are on course to be met by margins of £9.9 billion and £15.7 billion.

1.4 These margins are a small fraction of the risks around that central forecast. The economic outlook depends on uncertain judgements on the paths for productivity, inactivity, and net migration. The fiscal forecast also remains highly sensitive to movements in interest rates and inflation given the level of debt. The Budget crystallises much of the significant upside risk to spending highlighted in previous forecasts, but only sets detailed departmental plans for one more year and is still based on seldom-implemented fuel duty rises.

Budget policies

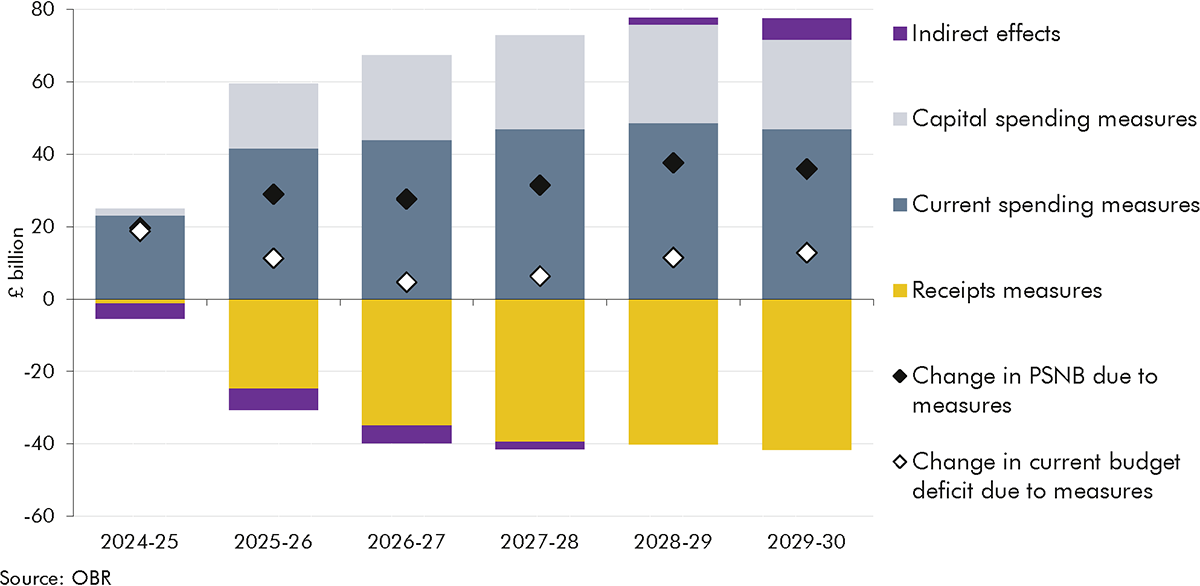

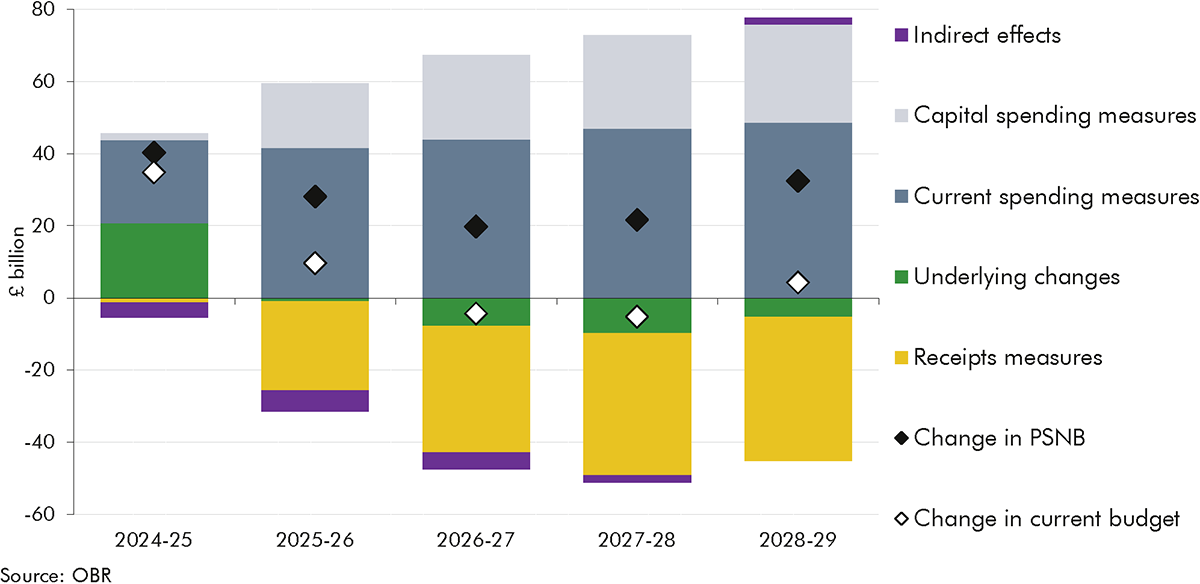

1.5The net effect of Budget policies is to increase borrowing by £19.6 billion this year and by an average of £32.3 billion over the next five years. Policy decisions increase current and capital spending in total by an average of £69.5 billion a year from 2025-26. Around half of this is offset by tax policies, which increase revenue by £36.2 billion a year on average. The fiscal impacts of the indirect effects of these policies on the economy are largely offsetting. Overall, policy decisions raise the current budget deficit by an average of £9.3 billion a year over the next five years, as the policy-driven increase in current spending is not fully offset by the increase in receipts.

Chart 1.1: Impact of measures on public sector net borrowing and current deficit

1.6Budget spending policies add £69.5 billion (2.2 per cent of GDP) a year over the next five years, and £71.6 billion by the end of the decade, to the level of public expenditure. On average £45.6 billion goes on current spending and £23.8 billion goes on capital spending. The main components are:

an increase in departmental current expenditure (resource DEL) of £22.9 billion this year rising to £48.8 billion by 2029-30;

an increase in departmental capital expenditure (capital DEL) of £21.6 billion by 2029-30;

additional payments for the infected blood and Post Office Horizon compensationschemes of £1.4 billion in 2029-30, and £13.6 billion in total over the forecast; and

cost savings of £3.5 billion from DWP fraud and error measures and £1.7 billion from the means-testing of winter fuel payments by 2029-30.

1.7Budget tax measures increase total revenues by £36.2 billion (1.1 per cent of GDP) a year on average and £41.5 billion by the end of the decade. The main components of the increase are:

an increase in employer NICs, via a higher rate and lower threshold, raising £25.7 billion by 2029-30 before allowing for its indirect effects on the economy;

several tax compliance measures raising £3.5 billion by 2029-30, and debt collection measures raising a further £2.7 billion;

changes to the regimes for capital taxes and for non-domiciled taxpayers, which together raise £5.2 billion by 2029-30;

levying of VAT on private school fees, raising £1.7 billion by 2029-30;

other net tax changes, including increasing the rate of the energy profits levy and extending it to 2029-30 and increasing air passenger duty rates, raising a total of £3.6 billion by 2029-30; and

these are slightly offset by an extension of the freeze and 5p cut to fuel duty rates to 2025-26, costing £3.0 billion in 2025-26 and £0.9 billion by 2029-30.

Economic outlook

1.8Budget policies deliver a temporary boost to GDP in the near term and some crowding out of private activity in the medium term. We estimate that the policy package boosts real GDP by 0.6 per cent at its peak in 2025-26 as the fiscal loosening temporarily raises output above its potential level. This temporary stimulus fades to zero over the remainder of the forecast as we assume monetary policy acts to rein in any excess demand. Budget policies also have lasting impacts on the supply potential of the economy. The employer NICs rise is estimated to reduce labour supply by 50,000 average-hours equivalents, while the net fiscal loosening would crowd out some private investment in an economy with little spare capacity. At the same time, the increase in public investment boosts potential output by raising the public capital stock and incentivising some private investment. Taken together, Budget policies leave the level of output broadly unchanged at the forecast horizon. In the longer term, the net effect of Budget policies would be positive for the economy-wide capital stock and potential output if the increase in public investment were to be sustained.

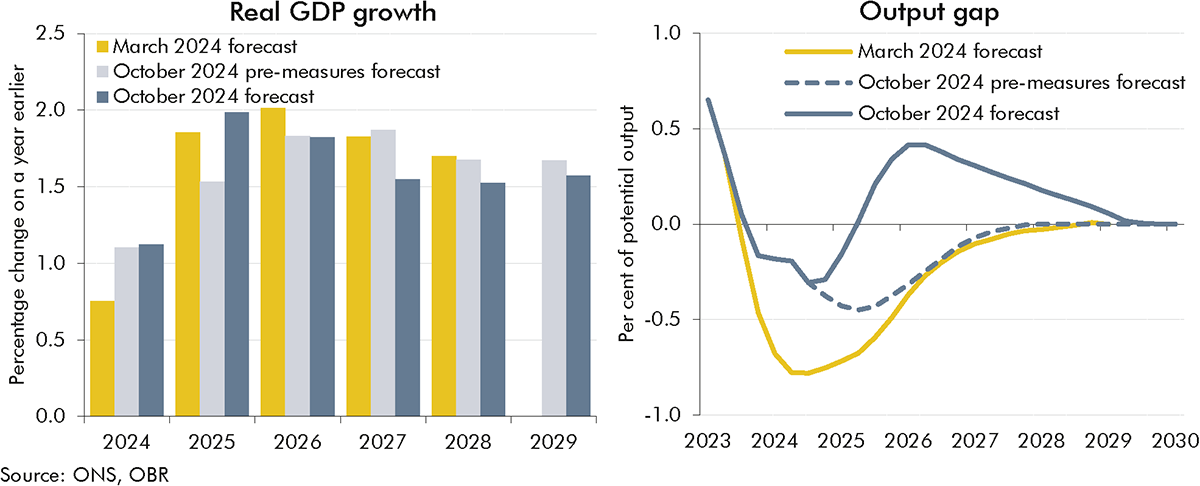

1.9Real GDP growth is therefore forecast to pick up from close to zero last year, to 1.1 per cent this year, 2.0 per cent in 2025, and 1.8 per cent in 2026, before falling back to around 1½ per cent thereafter. Stronger growth in the near term, supported by the easing in monetary policy, pushes GDP above our estimate of potential output. The economy moves from having a small negative output gap in 2024 to a positive output gap, which peaks at just under ½ a per cent in 2026. As the effects of monetary policy loosening and the temporary boost to demand in this Budget fade, the output gap is expected to close over the rest of the forecast. This lowers GDP growth to around 1½ per cent in the final three years of the forecast, slightly below our estimate of medium-term potential output growth of 1⅔ per cent. Compared to our March forecast, growth is forecast to be an average of a ¼ percentage point higher this year and next. This reflects stronger GDP and real wage growth in recent quarters, and the net fiscal loosening in this Budget. Growth is then weaker between 2026 and 2028 as these temporary effects fade.

Chart 1.2: Real GDP growth and the output gap

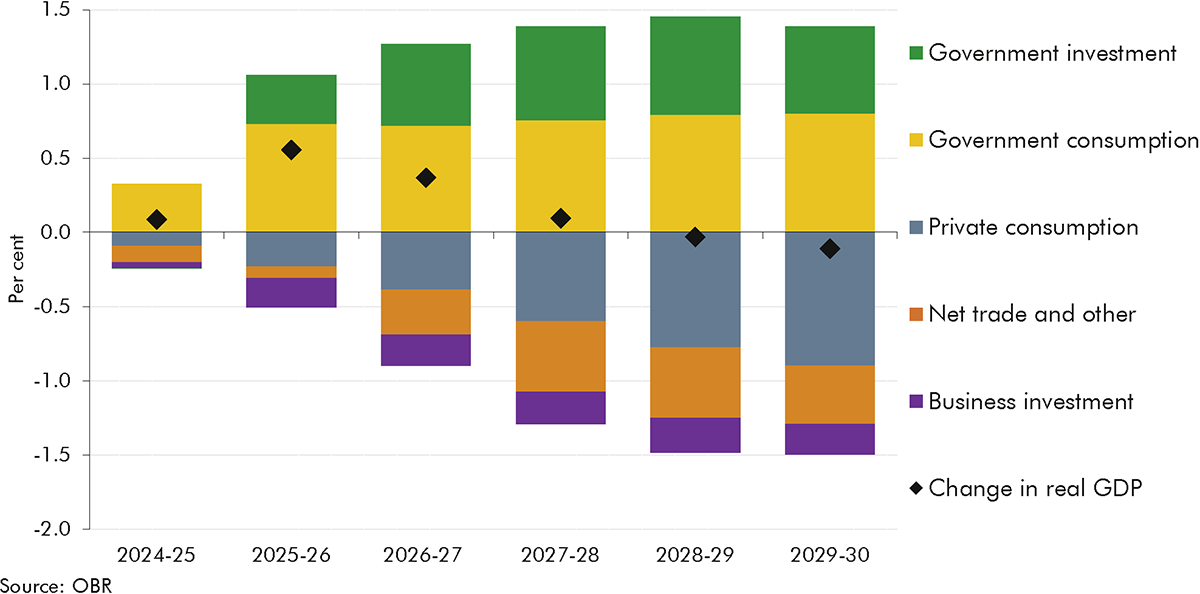

1.10Policies announced in this Budget lead to a sustained increase in real government spending as a share of GDP. Government consumption rises by around 0.8 percentage points of GDP between 2023 and 2029. Government investment remains broadly flat, rather than falling by around ¾ of a percentage point as in our pre-measures forecast. The increase in government activity, alongside a net fiscal loosening, crowds out some private consumption, business investment and net trade in a capacity-constrained economy. Tax rises in this Budget weigh on real incomes, so private consumption falls as a share of GDP. Corporate profits are expected to continue falling as a share of GDP in the near term, before rising gradually from 2026 as firms rebuild margins and pass on more of the cost of the employer NICs rise. Over the forecast, business investment falls as a share of GDP as profit margins are squeezed, and the net impact of Budget policies lowers business investment. Higher government investment increases incentives for businesses to invest but that is more than offset by the crowding out effect of the fiscal loosening.

Chart 1.3: Policy impacts on real GDP and its components

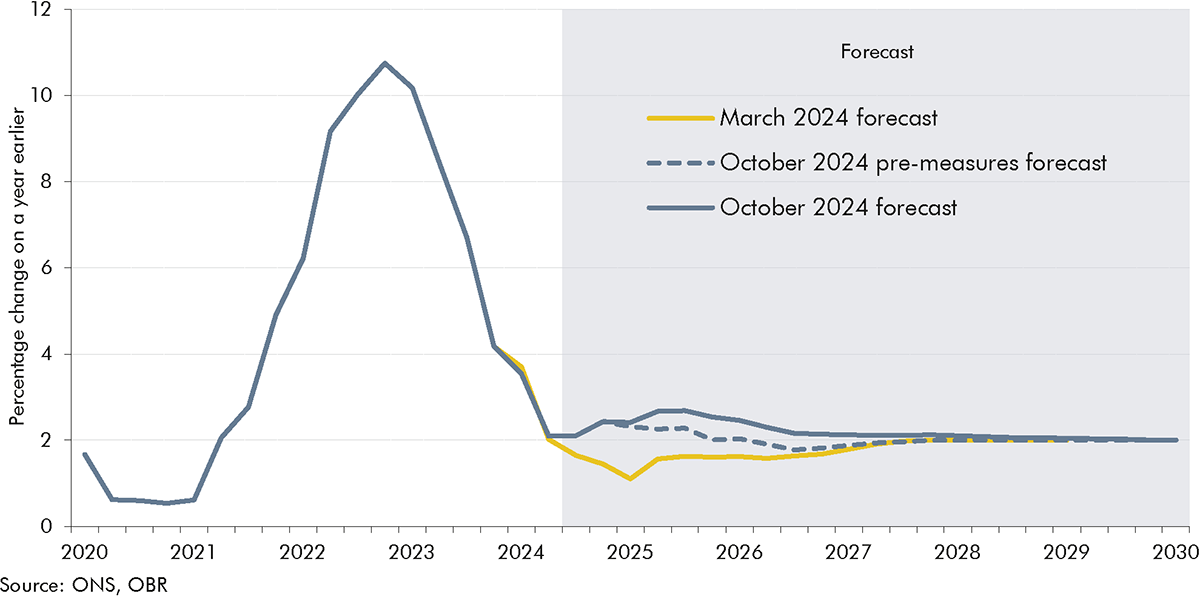

1.11Having fallen back to around the 2 per cent target in mid-2024, we expect CPI inflation to pick up to 2.6 per cent in 2025 partly due to the direct and indirect impact of Budget measures. Inflation then slowly returns to the 2 per cent target by the forecast horizon as the effect of these measures fades and the positive output gap closes. Compared to our March forecast, inflation is 1.1 percentage points higher in 2025 and 0.6 percentage points higher in 2026, driven mainly by greater-than-expected persistence in wage growth and the impact of the near-term fiscal loosening in this Budget. We estimate that Budget policy measures increase inflation by 0.4 percentage points at their peak effect in 2026, mainly reflecting the impact of the excess demand generated by the fiscal loosening and some pass-through of employer NICs to consumer prices. A further escalation of the conflicts in the Middle East poses a risk to our inflation forecast, initially via its impact on energy prices. Market expectations for 2025 oil prices have ranged between 68 and 84 dollars a barrel since the March forecast, compared to 71 dollars a barrel in our central forecast.

Chart 1.4: CPI inflation

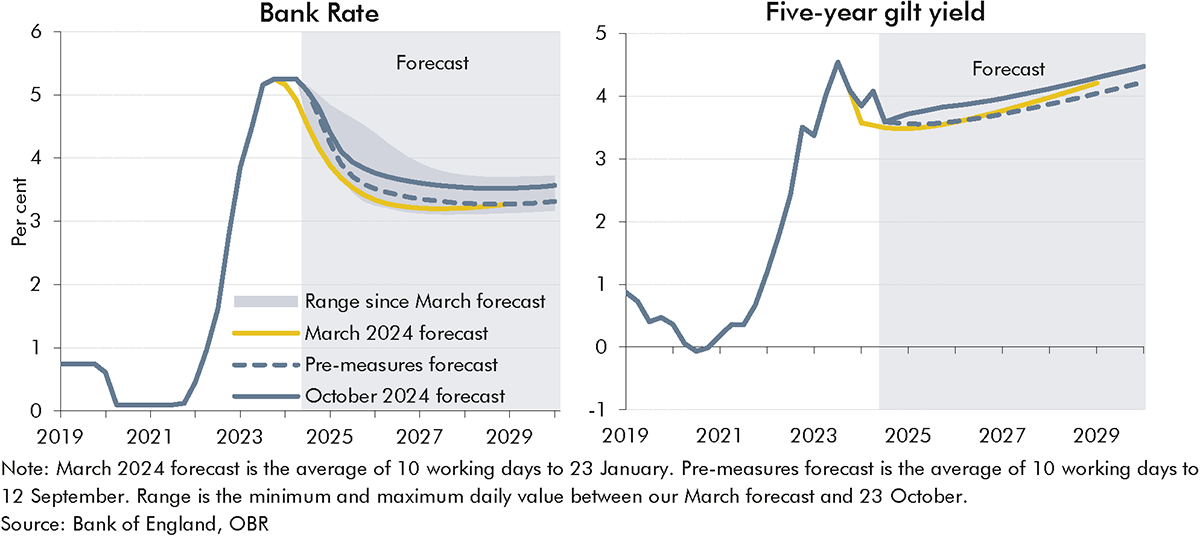

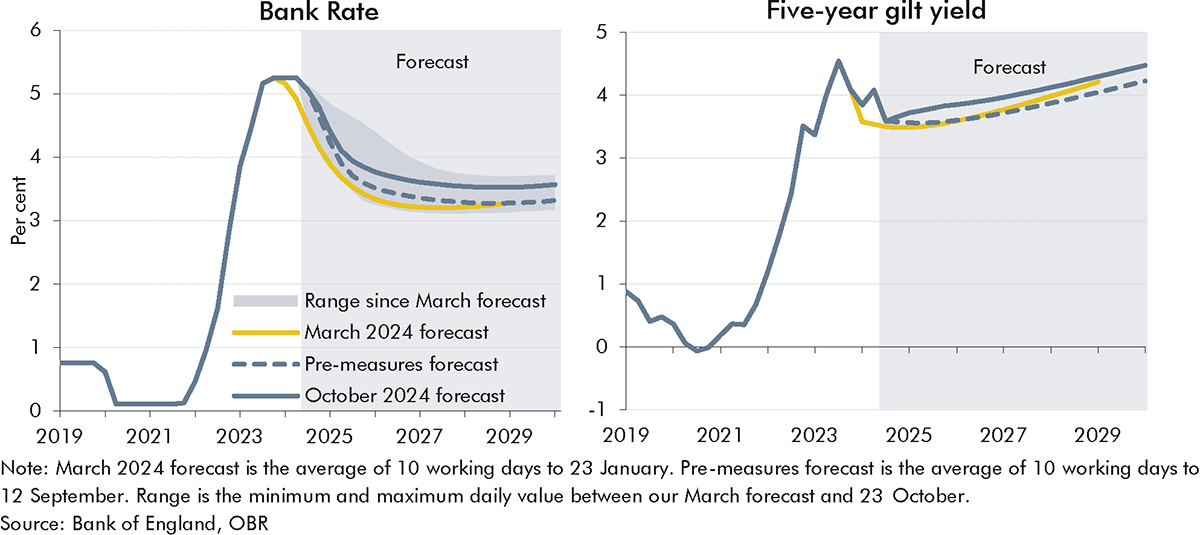

1.12From its current level of 5 per cent, Bank Rate is expected to fall to 3.5 per cent in the final year of the forecast. Over 2025 and 2026, this is around ½ a percentage point higher than the level of Bank Rate in our March forecast, partly reflecting market expectations at the time we closed our pre-measures interest rate forecast on 12 September. However, the full extent of discretionary fiscal easing in this Budget is unlikely to have been anticipated by market participants at this time, so we have raised Bank Rate and gilt yields by a ¼ percentage point across the forecast. This is broadly consistent with where market expectations for interest rates were when we finalised our post-measures forecast.

Chart 1.5: Bank Rate and five-year gilt yield

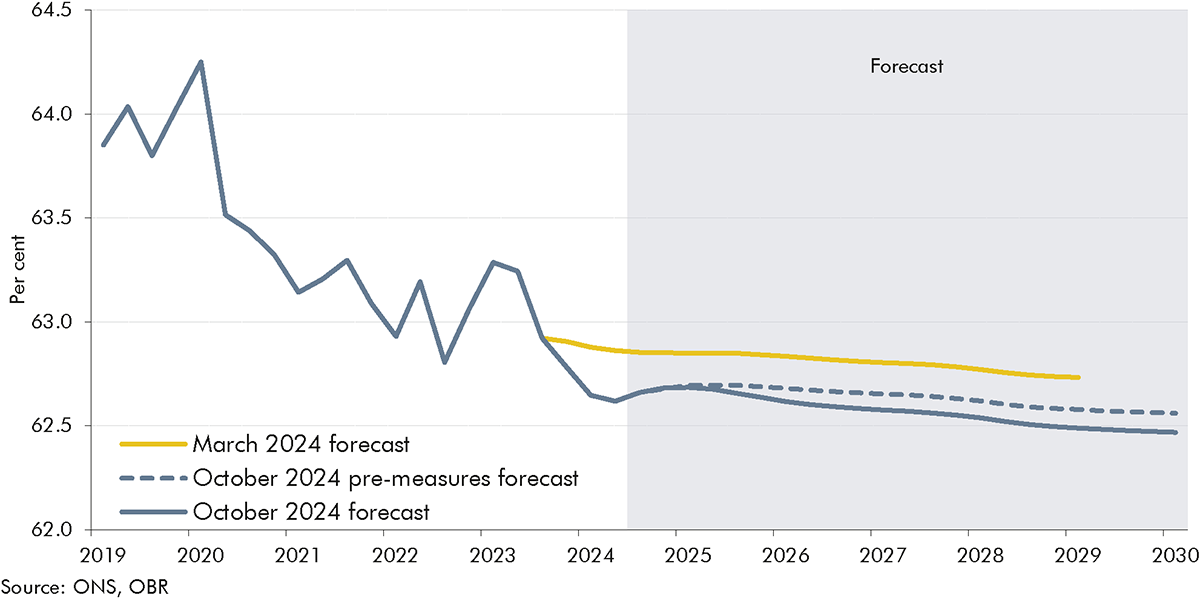

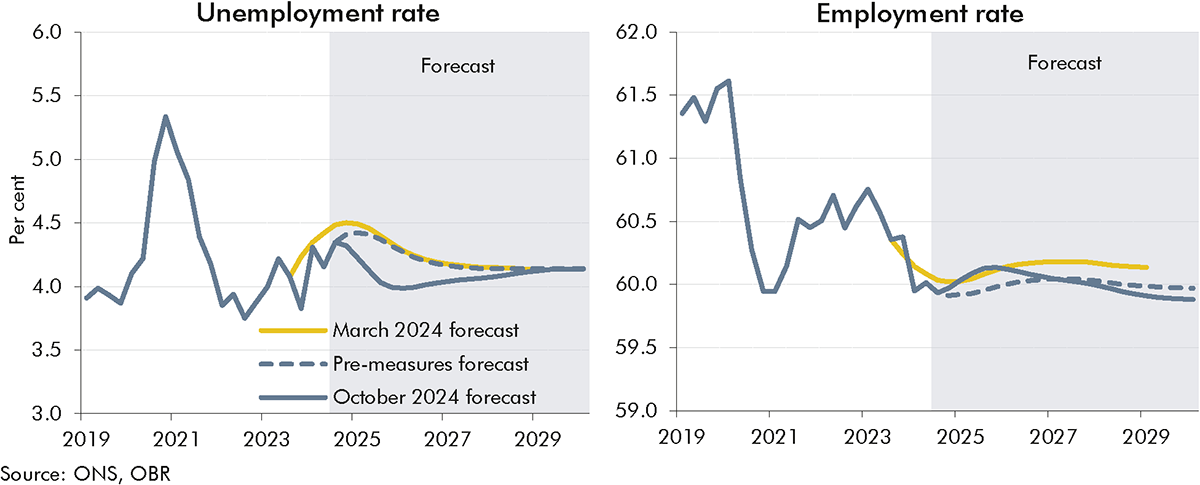

1.13Supported by the temporary boost to demand from this Budget, the unemployment rate falls from 4.3 per cent this year to 4.0 per cent in 2026 before returning to its estimated structural rate of 4.1 per cent in 2028. The impact of Budget policy measures accounts for nearly all the reduction in the unemployment rate relative to the March forecast, with a peak impact of 0.3 percentage points (100,000 people) in 2025. The participation rate declines slightly over our forecast to reach 62½ per cent in 2029 – well down from the peak of 64¼ per cent in the first quarter of 2020. The biggest drag comes from the ageing of the population, with the rise in employer NICs in this Budget also having a small negative effect. The overall effect of tax rises in this Budget is to lower the participation rate by 0.1 percentage points, leaving it 0.2 percentage points below our March forecast in 2028. The employment rate rises a little in the near term and then declines to just under 60 per cent by the forecast horizon, but population growth means that total employment increases by 1.2 million people from 2024 to 2029.

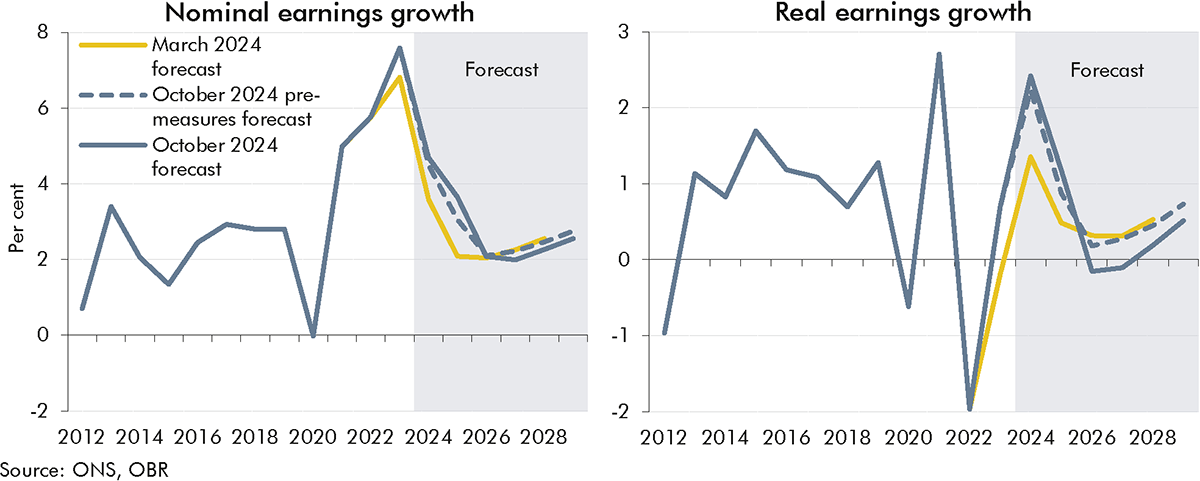

1.14We expect nominal earnings growth to fall from 4.7 per cent this year to around 3½ per cent in 2025 and then average 2¼ per cent over the remainder of the forecast. Compared to our March forecast, this is over 1 percentage point higher this year due to higher private and public sector wage settlements. Next year, it is around 1½ percentage points higher, partly due to the fiscal loosening in this Budget. But forecast and policy changes leave nominal and real earnings growth lower over the remainder of the forecast as employers pass on the NICs rise, rebuild profit margins, and the temporary boost to demand fades. Real earnings growth is around 2½ per cent in 2024, but then falls to around zero in 2026 and 2027. Real wages are around 1½ per cent higher than our March forecast in 2028, despite being lowered by around ½ a per cent due to Budget policies, due to a higher starting point.

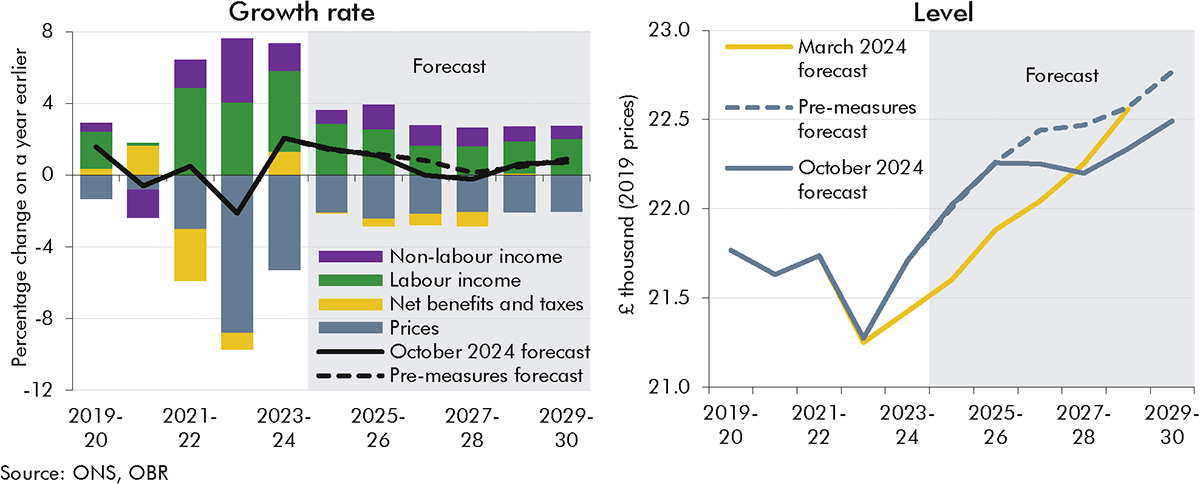

1.15Real household disposable income (RHDI) per person, a measure of living standards, grows by an average of just over ½ a per cent a year over the forecast. But the profile is uneven, with strong real wage increases resulting in growth of 1¼ per cent this fiscal year and next before RHDI per person stalls for two years in the middle of the forecast as real wage growth slows and taxes increase. Compared to our March forecast, the level of RHDI per person is just over 2 per cent higher at the start of the forecast due to data revisions, but 1¼ per cent lower by the start of 2029. The bulk of this difference (around 85 per cent) is explained by policies announced in this Budget.

1.16Nominal GDP growth is expected to average 3.8 per cent from 2024-25, around ½ a percentage point higher than in our March forecast. More persistent domestically generated inflation and the impact of this Budget mean higher GDP deflator growth more than offsets slightly lower real GDP growth. However, the upward revision to nominal GDP growth is not fully reflected in stronger growth in the key tax bases. Growth in wages and salaries and profits are constrained by the increase in employer NICs. And consumption growth is lowered by the effect of policy measures on household incomes.

Fiscal outlook

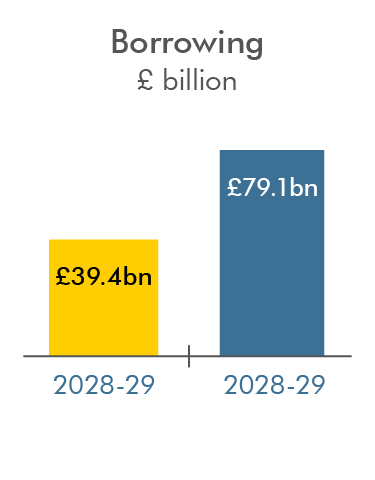

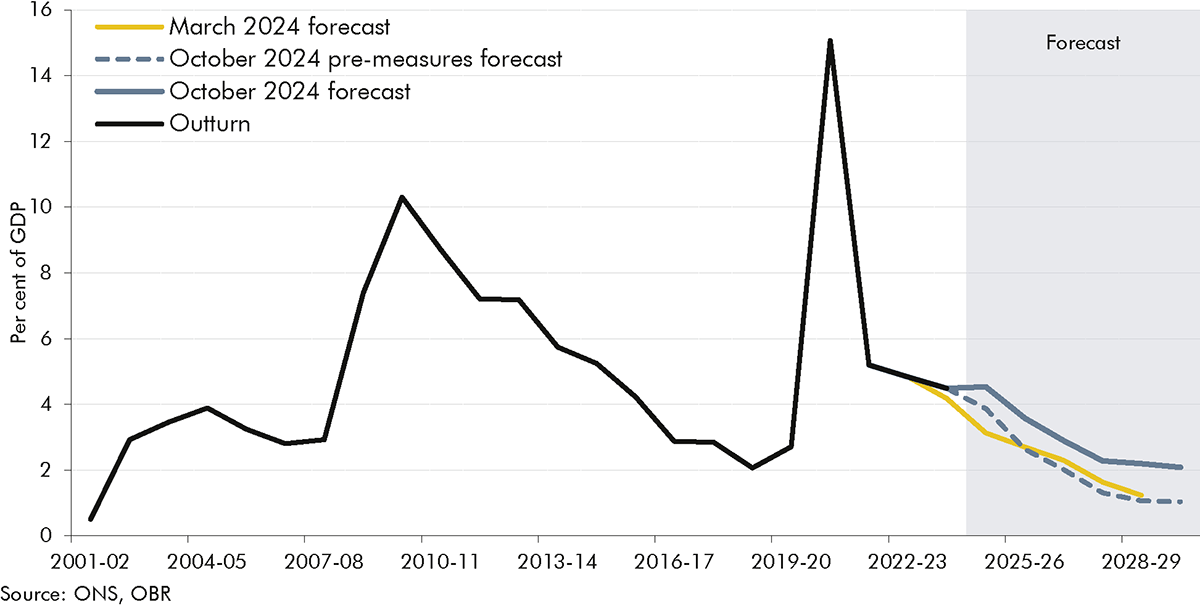

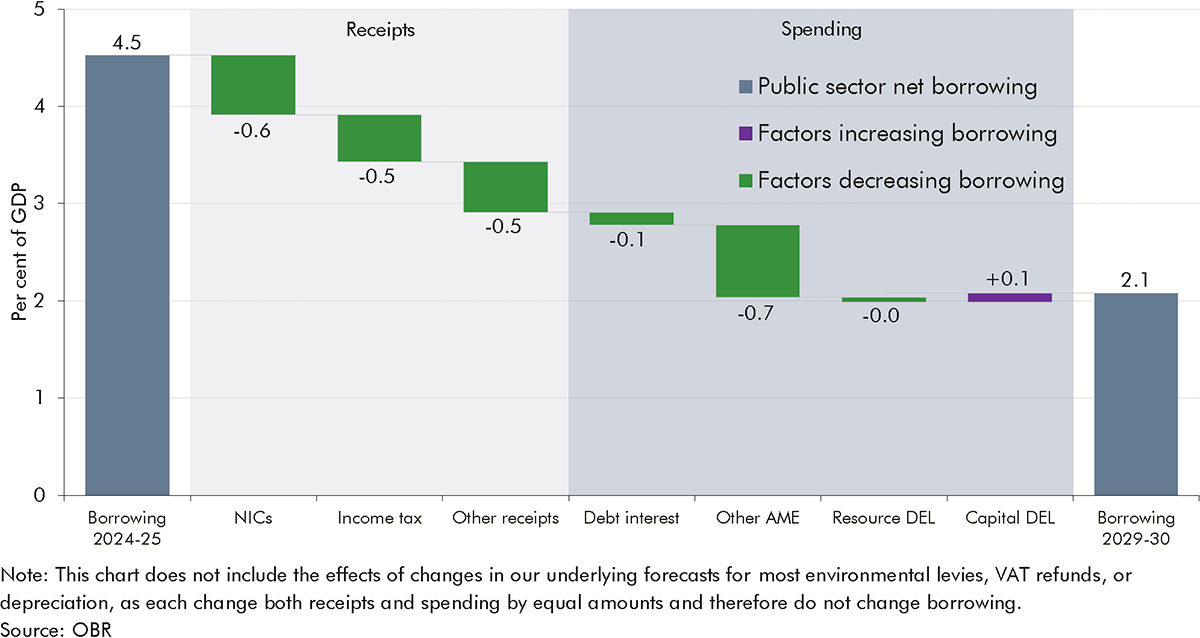

1.17Public sector net borrowing is forecast to rise from £121.9 billion (4.5 per cent of GDP) last year to £127.5 billion this year, before falling steadily back to £70.6 billion (2.1 per cent) by 2029-30. Overall, borrowing is £28.4 billion (0.9 per cent of GDP) a year higher on average over the forecast compared to March. By far the largest driver of the increase in the medium term is the Budget policy changes, which increase borrowing by £32.3 billion a year on average from 2025-26 to 2029-30. Pre-measures changes to the forecast increase borrowing by £20.7 billion this year, due mainly to higher inflation pushing up debt interest spending. In the medium term, pre-measures borrowing is £5.2 billion lower in 2028-29 relative to March, due to higher nominal earnings and equity prices increasing receipts by more than spending.

Chart 1.6: Public sector net borrowing

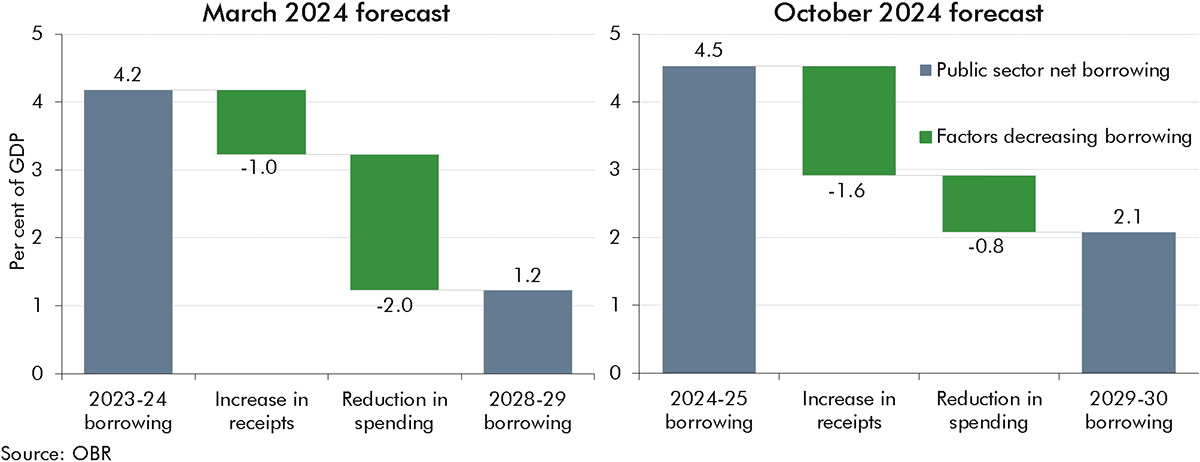

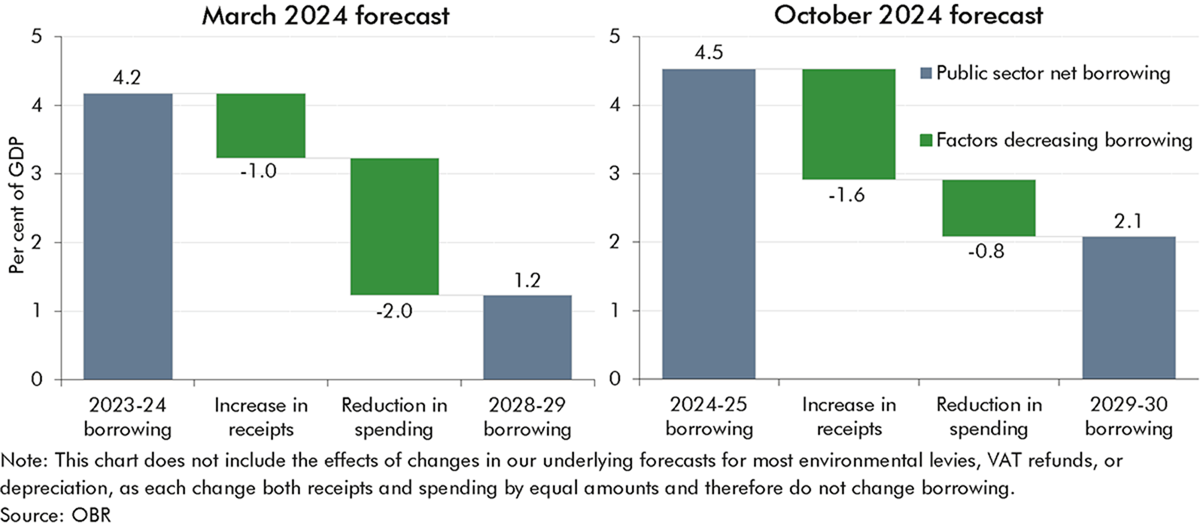

1.18Overall these changes mean that, compared to March, borrowing is now projected to decline less sharply from its peak to the end of the forecast. And while in March most of the decline was driven by spending falling as a share of GDP over the forecast, now it is mainly driven by taxes rising as a share of GDP. In March, borrowing was projected to fall by 2.9 per cent of GDP between 2023-24 and 2028-29, with one-third due to increases in receipts and two-thirds due to a reduction in spending. At this Budget, borrowing is forecast to fall by 2.5 per cent of GDP between 2024-25 and 2029-30, with around two-thirds driven by higher revenues and the rest by a reduction in spending as a share of GDP.

Chart 1.7: Change in borrowing over forecast periods: March and October

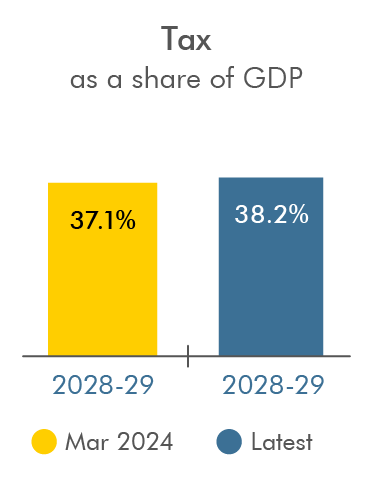

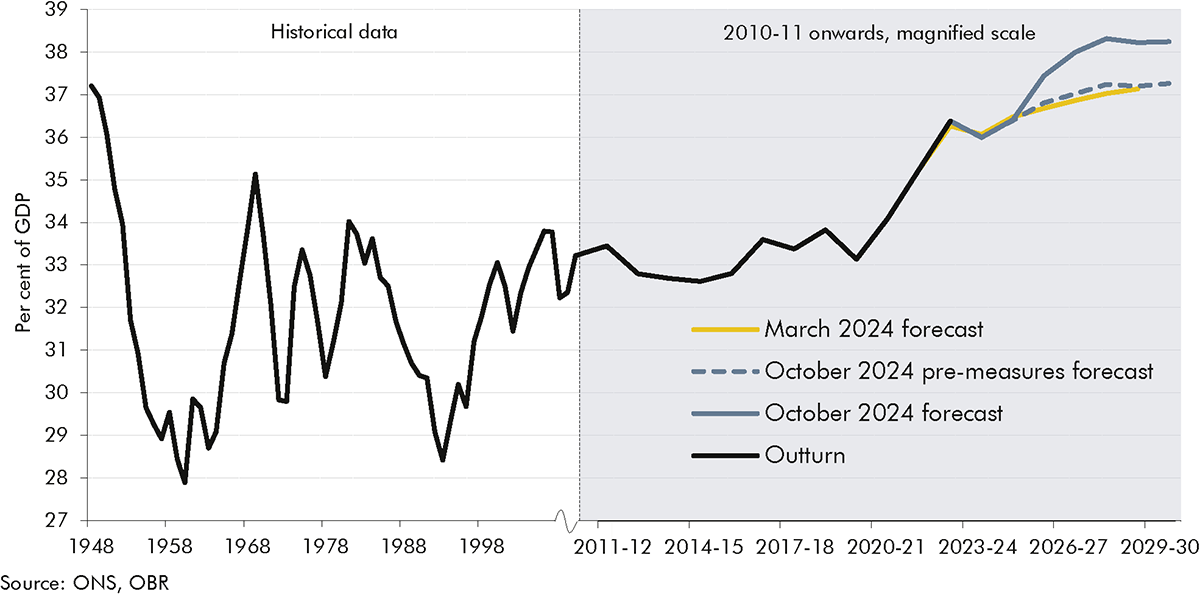

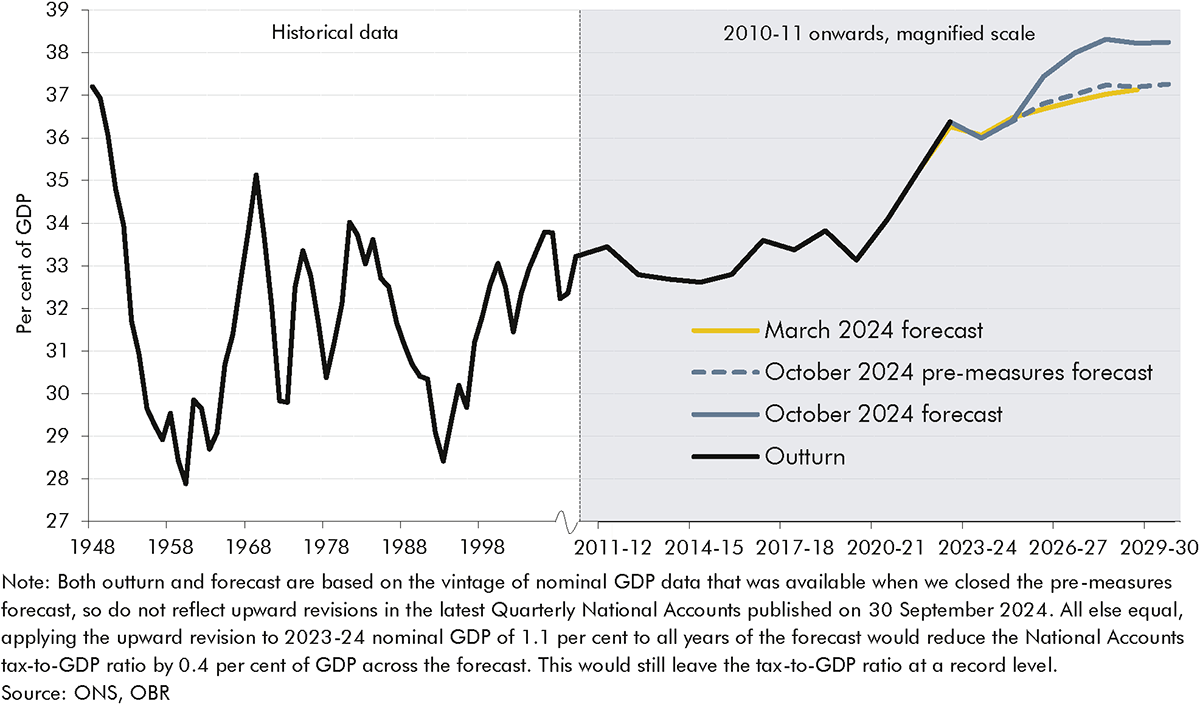

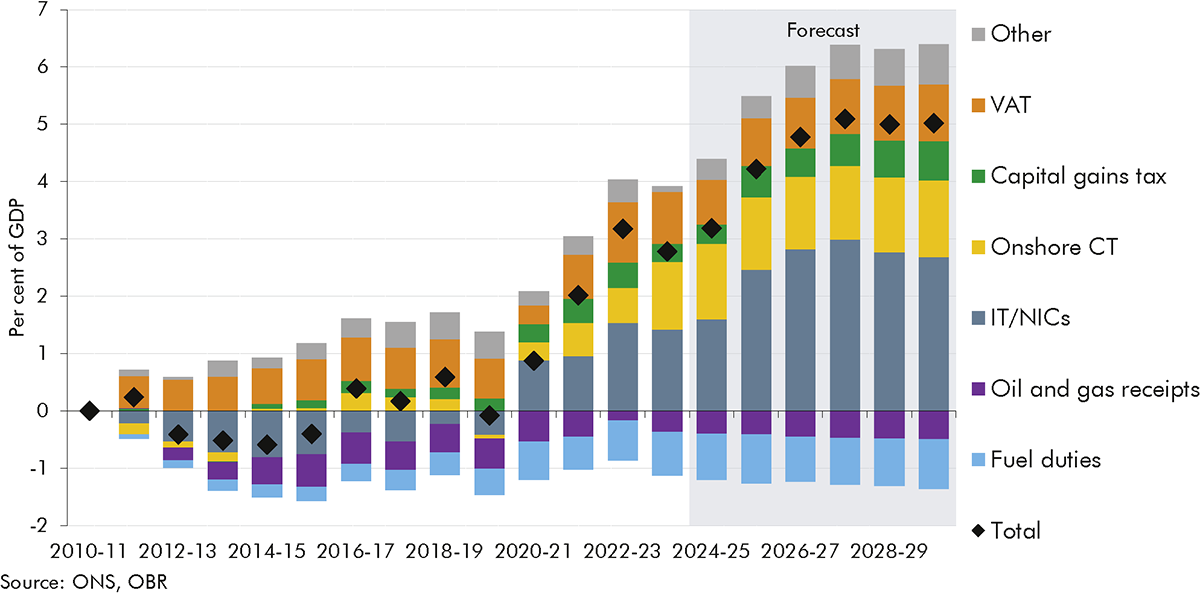

1.19Tax as a share of GDP is forecast to rise from 36.4 per cent this year to a historic high of 38.2 per cent in 2029-30, 5.1 per cent of GDP higher than before the pandemic. The increase is driven mainly by personal taxes (including the impact of the employer NICs measures in this Budget, earnings growth and frozen thresholds) and by capital taxes, (reflecting the path of equity prices, property prices and measures in this Budget). The tax take in 2028-29 is 1.1 per cent of GDP higher than in the March forecast.

Chart 1.8: National Accounts taxes as a share of GDP

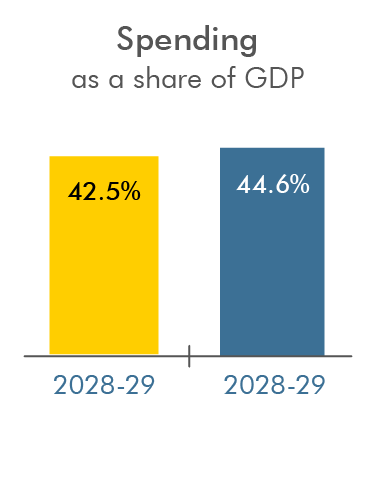

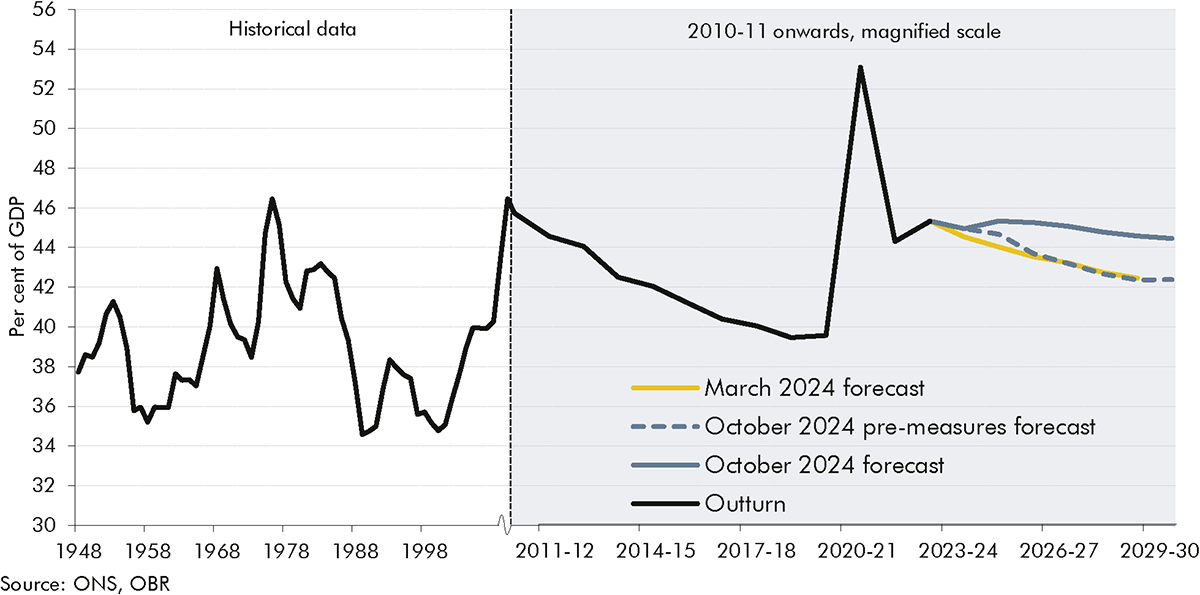

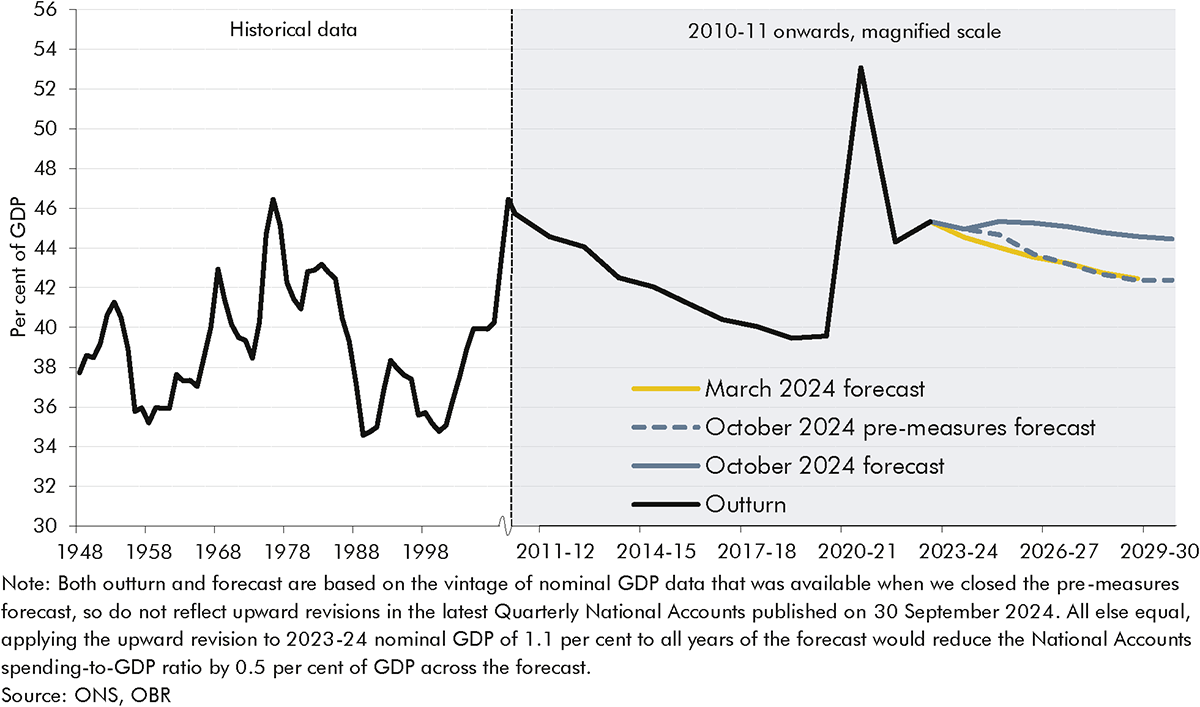

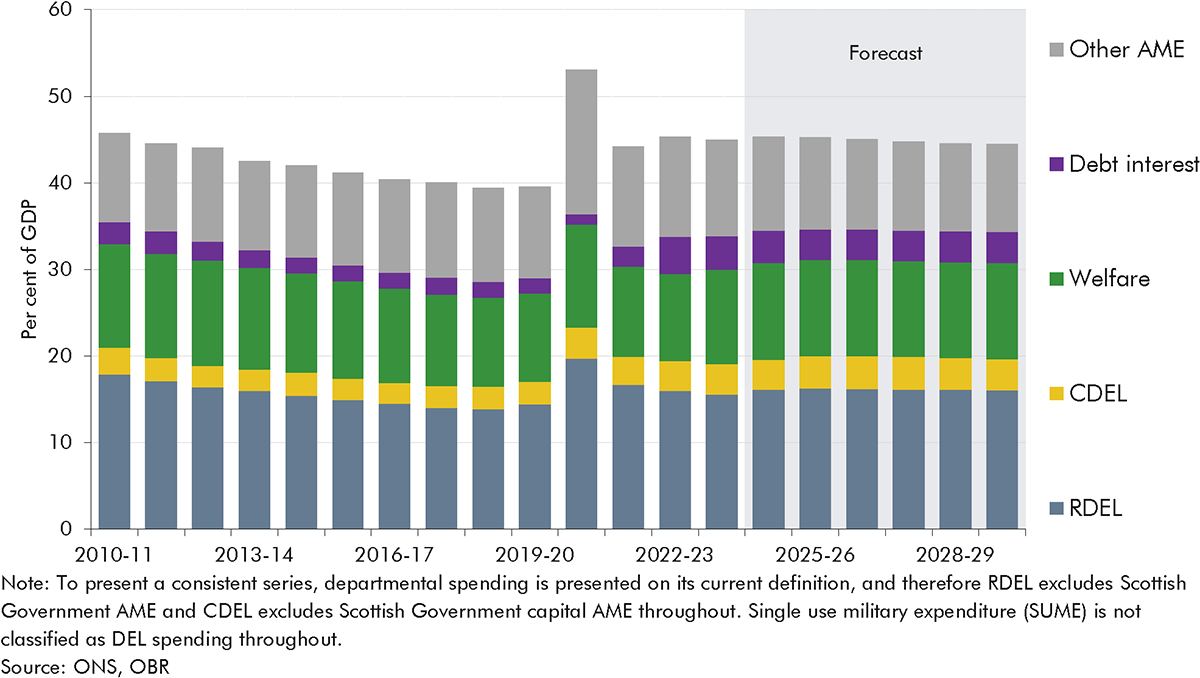

1.20Spending as a share of GDP is forecast to rise from 44.9 per cent last year to 45.3 per cent this year, before falling back slightly to 44.5 per cent in 2029-30, 4.9 percentage points higher than pre-pandemic. Additions to departmental spending, additional payments for the infected blood and Post Office Horizon compensation schemes, and higher debt interest costs all push up the spending-to-GDP ratio this year and next. The decline in spending as a share of GDP over the remainder of the forecast reflects departmental spending growing more slowly than the economy and declines in spending on unfunded pensions and student loans. Debt interest and welfare spending remain broadly flat as a share of GDP.

Chart 1.9: Public spending as a share of GDP

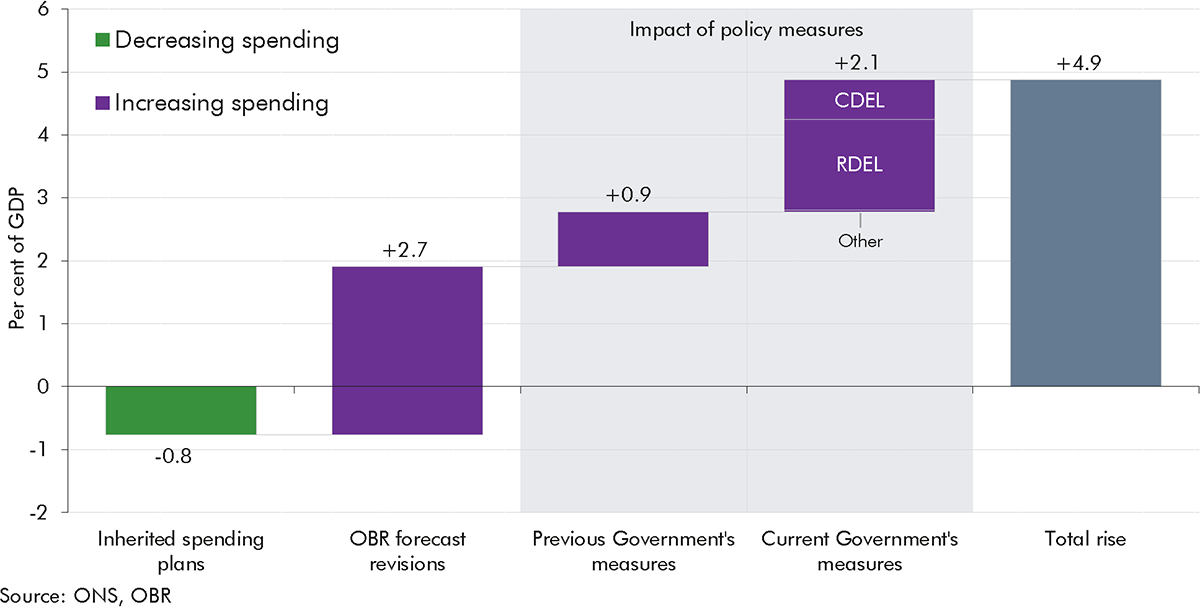

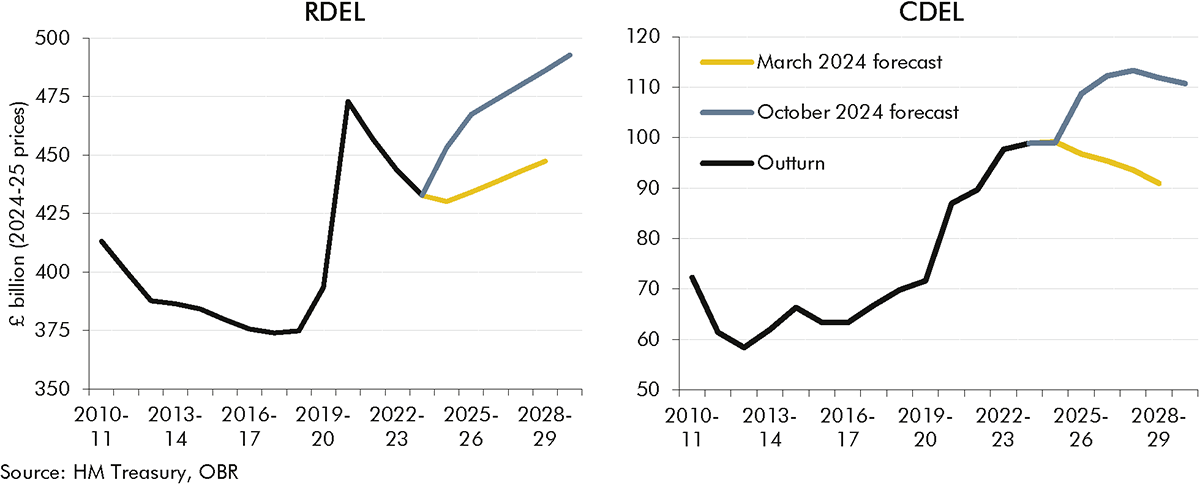

1.21Overall departmental spending is an average of £55.3 billion a year higher than in our March forecast, in which the previous Government’s plans entailed spending falling by 1 per cent of GDP between 2023-24 and 2028-29.

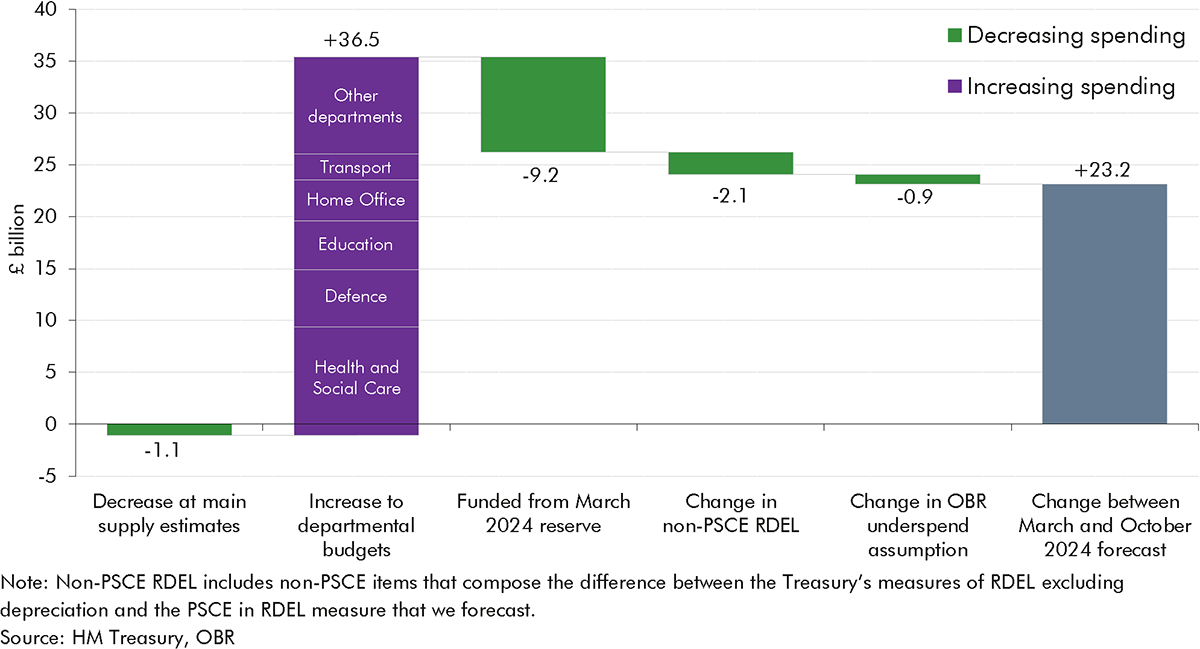

Current spending now grows in real terms by 4.8 per cent this year, 3.1 per cent next year, and by an average of 1.3 per cent between 2025-26 and 2029-30. The £23.2 billion increase in current spending in 2024-25 relative to the March forecast reflects a combination of the funding of undisclosed spending pressures that existed at the time of the March Budget and have since come to light, and the cost of new policies announced by this Government.

Capital spending grows in real terms by 9.8 per cent in 2025-26 and then flattens off, before falling slightly in the final two years of the forecast. Taking account of expected under-execution, estimated average annual real growth in capital spending between 2023-24 and 2028-29 is 2.6 per cent, compared to real annual falls averaging 1.1 per cent in our March forecast.

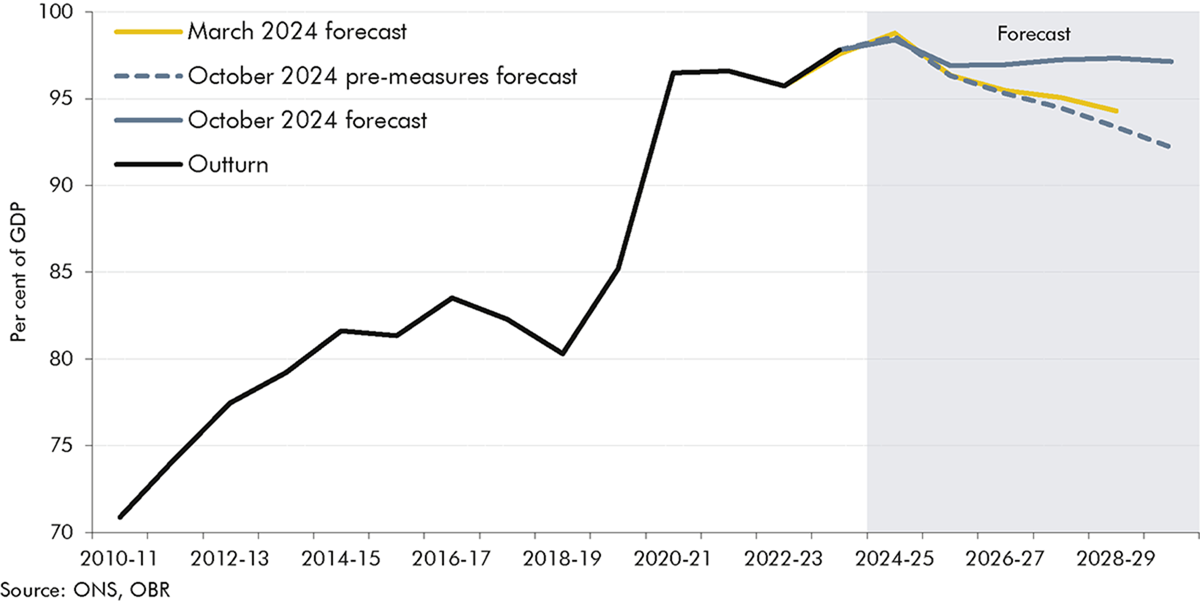

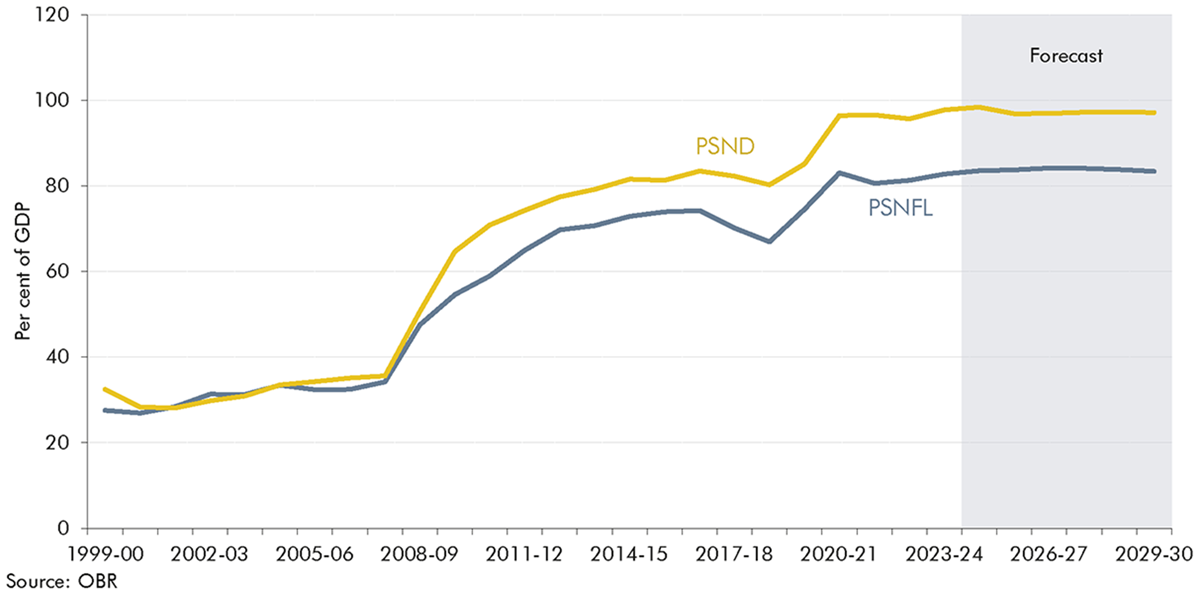

1.22Public sector net debt (PSND) falls from a peak of 98.4 per cent of GDP this year to 97.1 per cent of GDP in 2029-30. The fall is mainly driven by Term Funding Scheme repayments in 2025-26, after which debt is stable as a share of GDP as borrowing declines over the rest of the forecast. But due to the additional borrowing in this Budget, debt is 3.0 per cent of GDP (£169.8 billion) higher in 2028-29 than we projected in March. And the measure of debt excluding the Bank of England now rises as a share of GDP in every year, from 91.8 per cent this year to 95.8 per cent in 2029-30. The elevated level of debt means the public finances are highly sensitive to changes in interest rates. Market expectations for interest rates remain volatile, with expectations for Bank Rate in 2025 varying between 3.6 and 4.7 per cent and daily five-year gilt spot yields varying between 3.5 and 4.2 per cent since the March forecast.

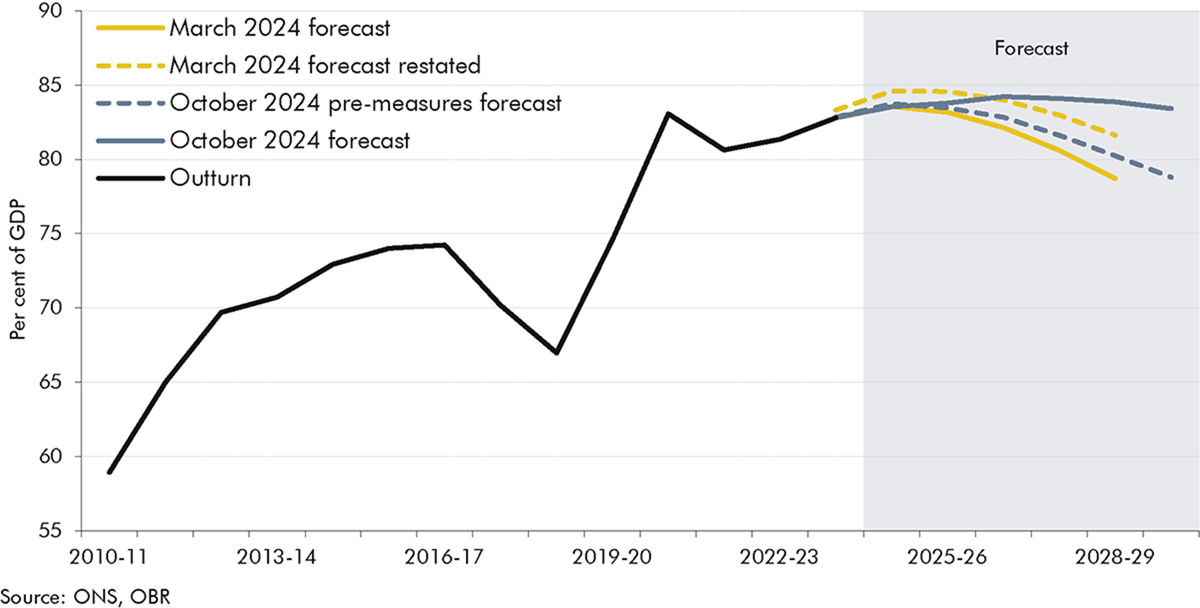

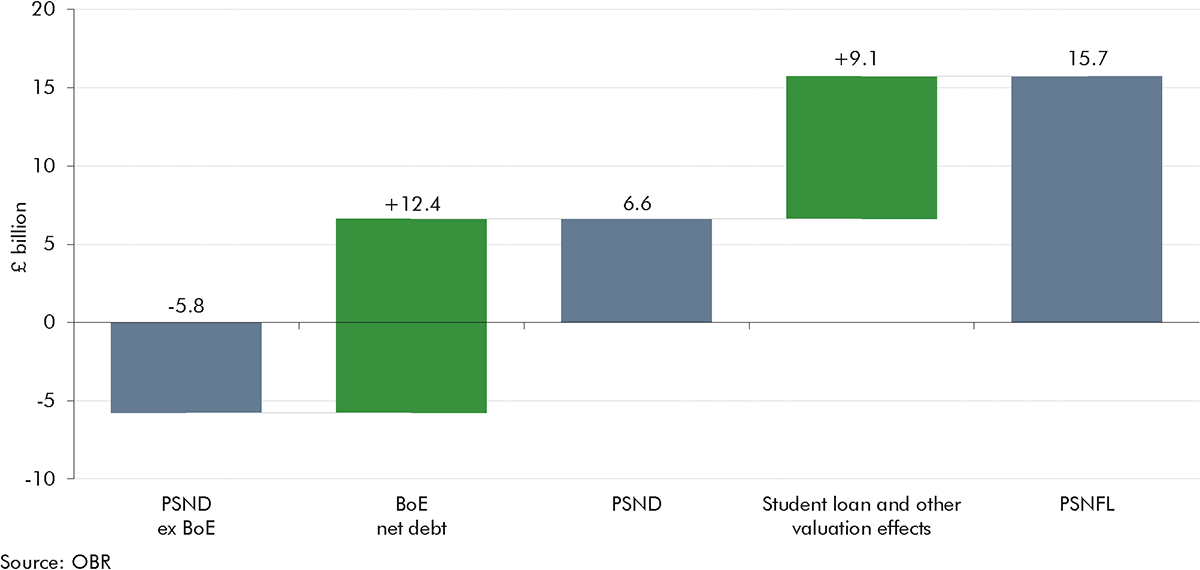

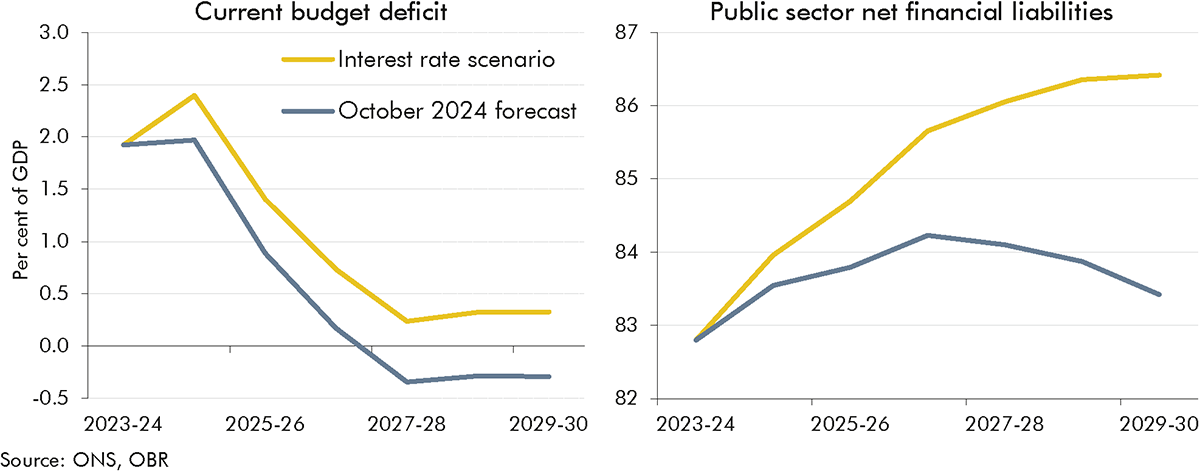

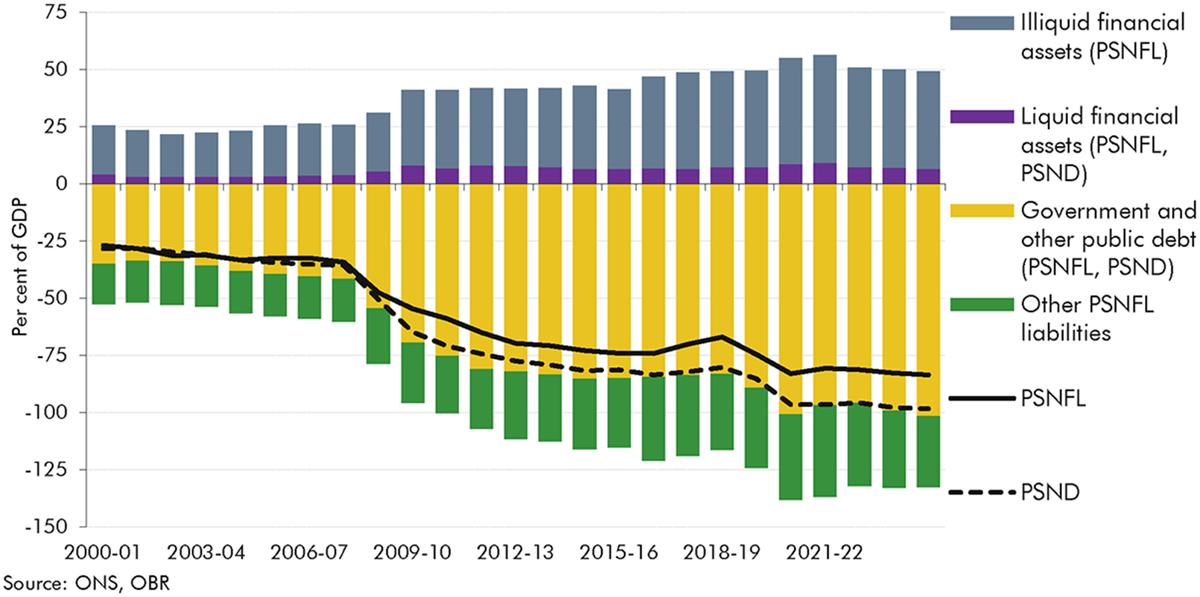

1.23Public sector net financial liabilities (PSNFL) – a wider measure of the balance sheet that includes all financial assets, but not physical assets such as hospitals, schools, and infrastructure – are forecast to increase from 83.5 per cent of GDP this year to 84.2 per cent in 2026-27, then fall to 83.4 per cent in 2029-30. While PSND rises very slightly (by 0.2 per cent of GDP) between 2026-27 and 2029-30, PSNFL falls gently (by a total of 0.8 per cent of GDP). The difference is more than explained by the accumulation of student loan assets, which increase by 1.7 per cent of GDP over this period. Financing the loans increases PSND but is neutral for PSNFL where both the asset and liability are counted.

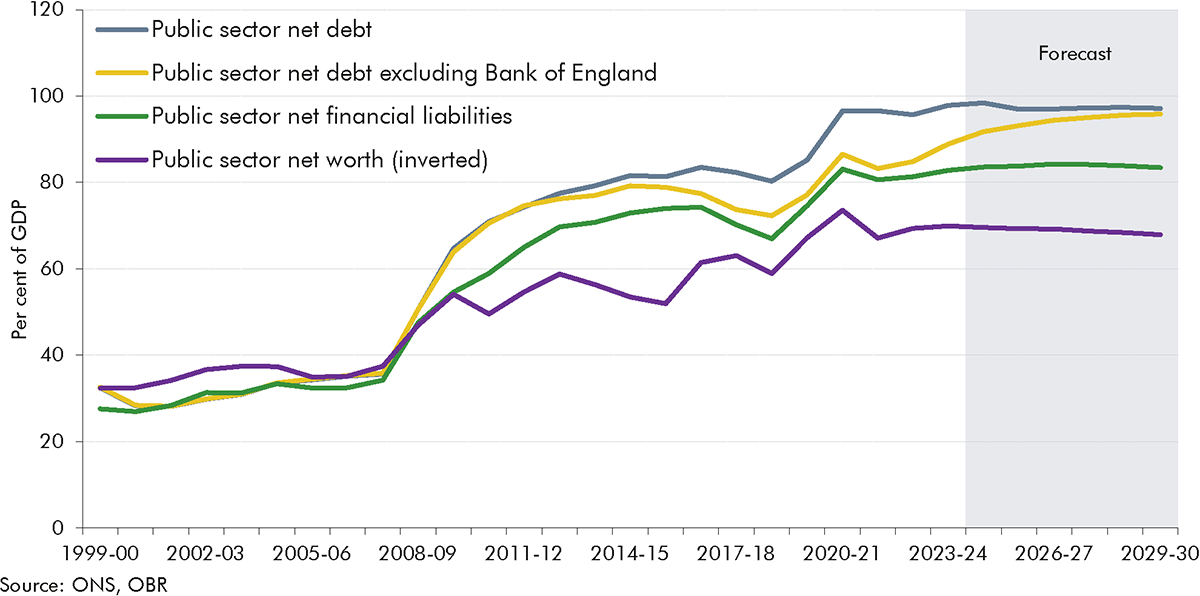

Chart 1.10: Public sector balance sheet measures

Performance against the Government’s fiscal targets

1.24In this Budget, the Government has announced three new fiscal targets:

a fiscal mandate for the current budget – revenues minus day-to-day spending – to be in surplus by 2029-30 (until 2029-30 becomes the third year of the forecast period, from which point the mandate applies to the third year);

a supplementary target for public sector net financial liabilities to fall as a share of GDP by 2029-30 (again until 2029-30 becomes the third year of the forecast, from which point this target applies to the third year); and

a revised welfare cap, with the target year updated to 2029-30.

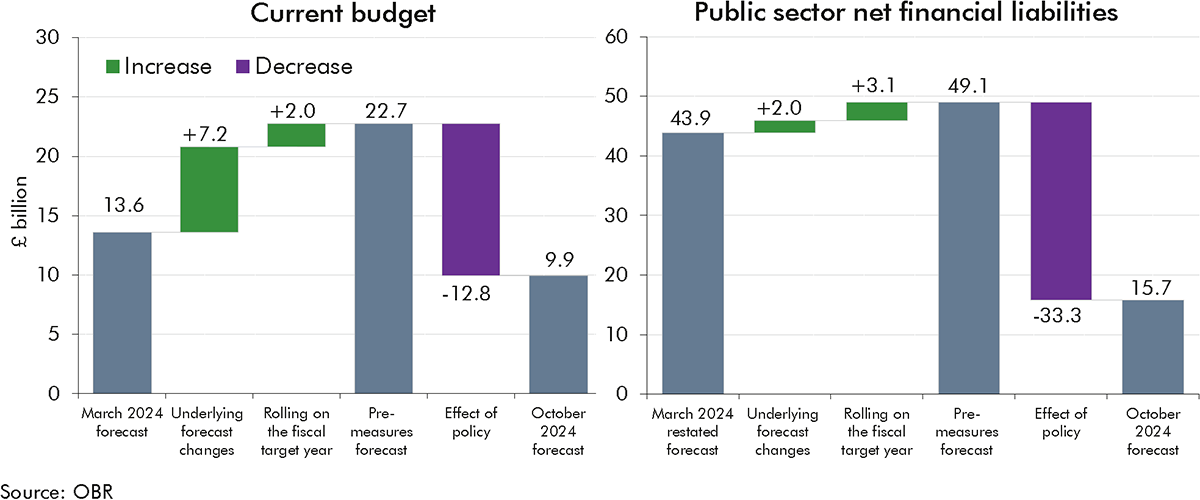

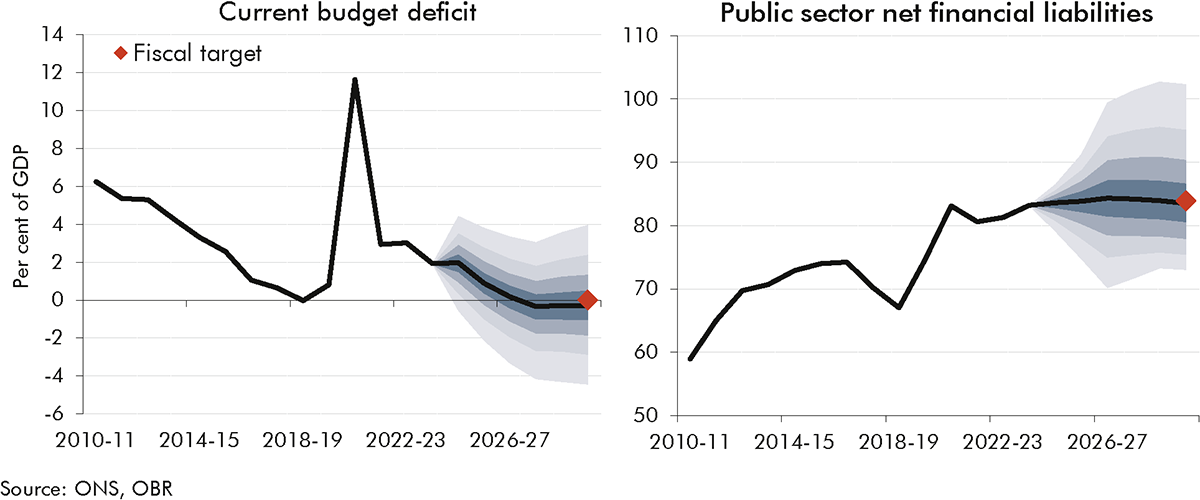

1.25In the central forecast, the current budget target is met two years early and by a margin of £9.9 billion (0.3 per cent of GDP) in the target year. The current budget improves from a deficit of 2.0 per cent of GDP this year to reach surplus in 2027-28, and then holds stable as a share of GDP. In the pre-measures forecast, the rule is met by a margin of £22.7 billion (0.7 per cent of GDP), but the direct and indirect effects of Budget policies reduce this headroom as the increase in current spending exceeds the yield from tax policy measures.

Chart 1.11: Current budget deficit

1.26The central forecast is that public sector net financial liabilities decrease in each of the final three years of the forecast, and fall by 0.5 per cent of GDP (£15.7 billion) in 2029-30. The composition and behaviour of PSNFL are explored in more depth in Chapter 6 and Annex B.

Risks and uncertainties

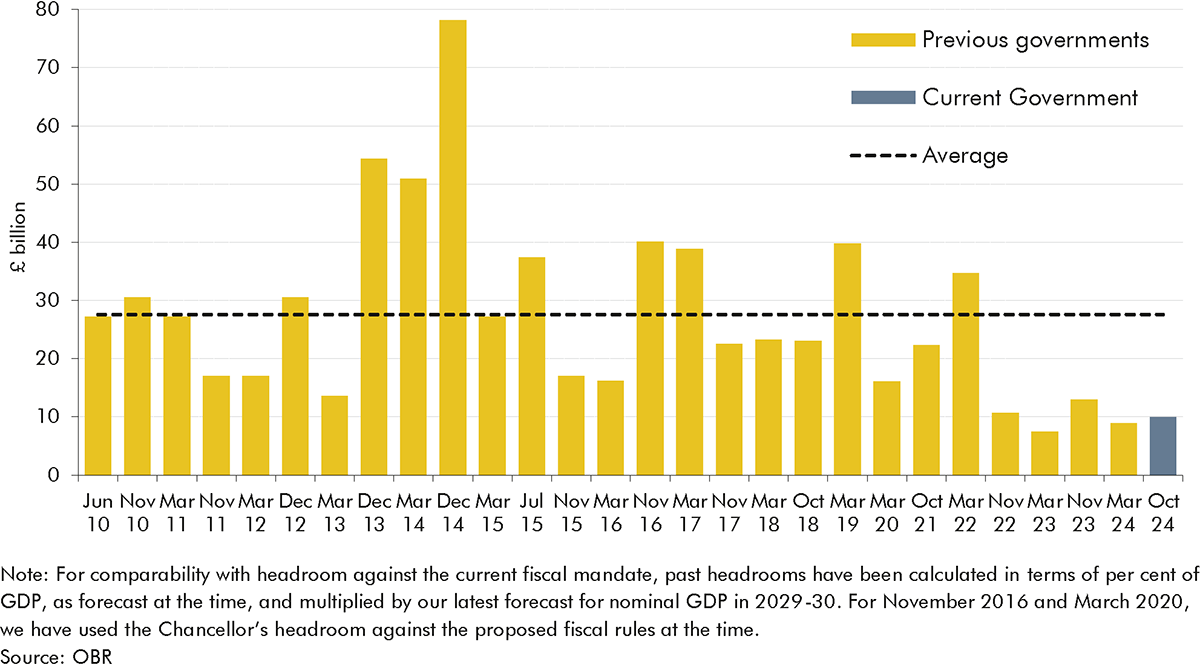

1.27These margins are both very small in the context of the significant uncertainties and risks around our central forecast. The underlying economic and fiscal context for this forecast was not significantly different from March. But previous forecasts have seen significant change due to volatility in energy prices, inflation, interest rates, and wage growth. Key risks for our economy forecast include:

Market expectations for Bank Rate and gilt yields remain volatile. If these were 1.3 percentage points higher across the forecast, it would be enough to wipe out the headroom to the supplementary fiscal target.

The inflation outlook remains uncertain. Our March 2024 Economic and fiscal outlook (EFO) scenario showed how escalating conflict in the Middle East could raise energy prices, push inflation to 7½ per cent, and increase borrowing by £23 billion on average over the five-year forecast.

Productivity growth is one of our most important and uncertain judgements. In our November 2023 EFO we estimated that ½ a per cent higher or lower annual growth in productivity would reduce or raise borrowing by around £40 billion in 2028-29.

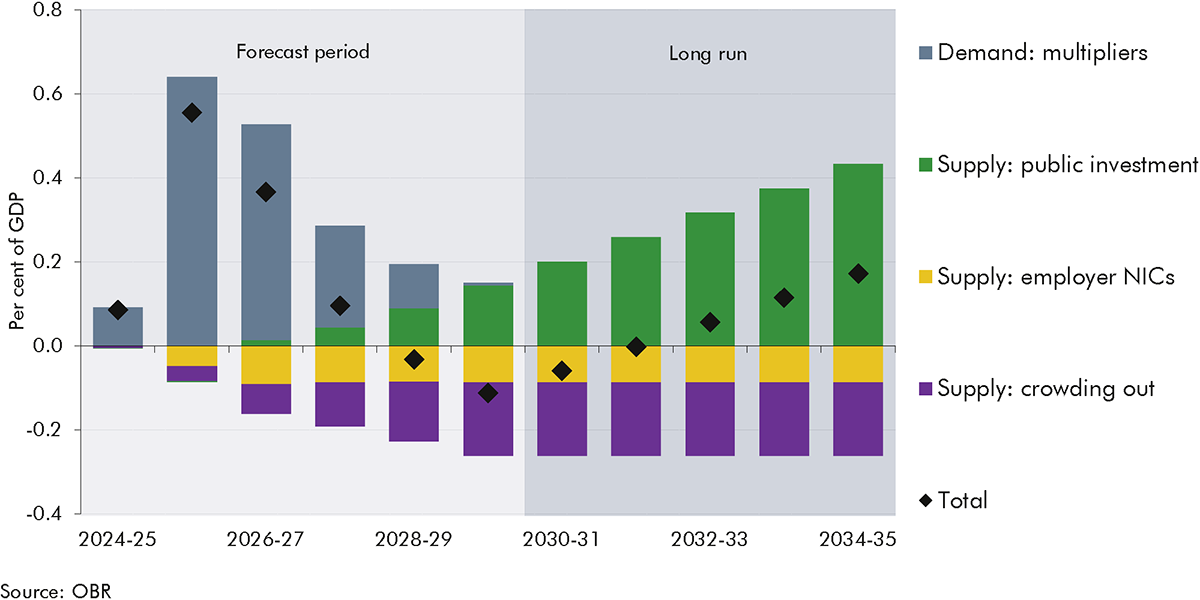

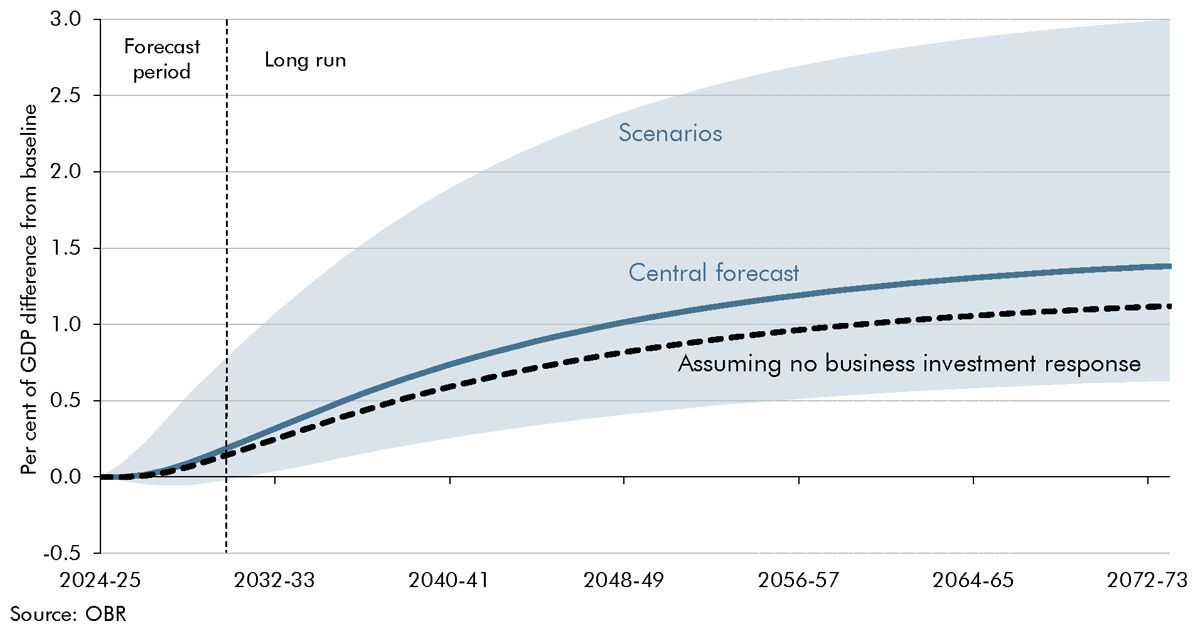

Our scenarios show that, if sustained, the impact of the increase in public investment announced in this Budget on potential output in 2073-74 could range between twice and half our central estimate of 1.4 per cent, depending on the degree to which public and private investments are substitutes or complements.

Several developing policy areas pose risks that we will consider as details are finalised. Reforms to the planning system could increase potential output, while the employment rights package could pose downside risks.

1.28There are also significant risks directly related to the fiscal forecast. Over the medium term, these include:

The tax-to-GDP ratio is forecast torise to a historic high in the late 2020s, with much of the increase driven by tax policy changes in the Budget. The estimated yield of several of these policies is highly uncertain and could undershoot or exceed our central forecast. This also assumes that the seldom-implemented indexation of fuel duty delivers around £4.8 billion in additional revenue by 2029-30.

Our March 2024 EFO highlighted the significant upside risk to departmental spending, as at the time spending allocations were only set for 2024-25. The Government has now allocated increased departmental spending for 2025-26 and set a significantly higher spending envelope for the three years beyond that, which will be allocated at next year’s Spending Review. Funding has now also been allocated for the infected blood and Post Office compensation schemes. Overall, the spending risks highlighted in our previous forecast are therefore reduced, though significant spending ambitions on defence and overseas aid remain unfunded. And governments have previously topped up the departmental spending envelope further when making final allocations.

Welfare spending on more costly incapacity and disability benefits is forecast to continue rising, from 2.4 per cent of GDP in 2023-24 to 3.0 per cent in 2029-30. This is an uncertain judgement as the increase to date has reflected a complex interaction of drivers across health, the economy, and the operation of the benefits system (as our 2024 Welfare trends report explored).

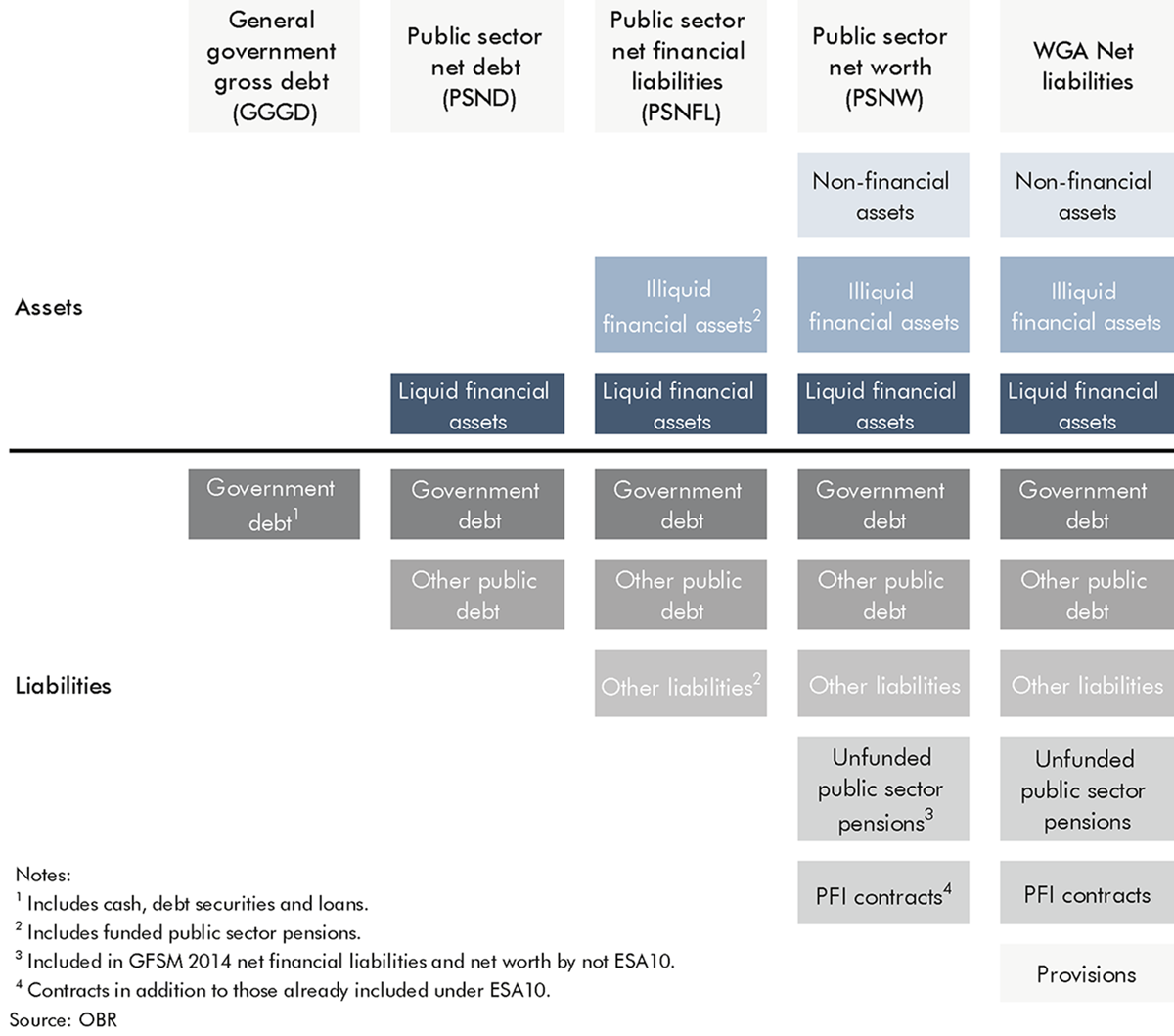

Unlike debt measures, public sector net financial liabilities incorporate the net position of public sector pension schemes, other equities held in the public sector, and loans made by public bodies. The recording of loans at nominal values is open to a risk of sharp changes in value when bad loans are written off, while changes in the composition and valuation of other assets and liabilities can also be substantial and uncorrelated with wider changes to fiscal policy.

The Government’s revised fiscal framework commits to spending reviews covering at least three years of the forecast window, and the fiscal mandate to ultimately take effect from the third year of the forecast. This will eventually reduce the risks around meeting the Government’s fiscal targets, as the targets will be earlier in the forecast period and will encompass years for which detailed departmental spending plans have been set.

Chapter 2: Economic outlook

Introduction

2.1 This chapter describes our latest economy forecast, summarised in Table 2.1, including:

our conditioning assumptions, including fiscal policy, interest rates and equity prices, commodity prices, the global economy and exchange rate (from paragraph 2.2);

how our forecasts for labour supply, business and government investment, and productivity influence the path of potential output (from paragraph 2.12);

real GDP and its components and the output gap (from paragraph 2.18);

inflation (from paragraph 2.29);

the labour market including participation, employment, unemployment, and earnings (from paragraph 2.33);

household incomes, housing, and the saving rate (from paragraph 2.40);

the current account and nominal GDP (from paragraph 2.46); and

how our forecast compares to recent external forecasts (from paragraph 2.50).

Table 2.1: Key economy forecast assumptions and judgements

Key metric (per cent unless otherwise stated)

March 2024

October 2024

Change

Gas prices

Average in 2025 (pence a therm)

84.0

97.3

↑

Oil prices

Average in 2025 ($ a barrel)

73.7

71.1

↓

Bank Rate

Average in 2025 and 2026

3.4

3.9

↑

Gilt yields

5-year gilt yields average from 2025 to 2028

3.8

4.0

↑

Inflation

Average in 2025 and 2026

1.6

2.4

↑

Output gap

Average in 2025 and 2026

-0.4

0.2

↑

Potential output

Growth average from 2025 to 2028

1⅔

1⅔

⚊

Net migration

Cumulative 5-year flow from 2024-25 (million)

1.5

1.5

⚊

Participation rate (16+)

Average in 2028

62.8

62.5

↓

Real GDP

Cumulative growth from 2024 to 2028

7.6

7.1

↓

Real GDP per person

Level in 2028 (Index, 2019=100)

104.7

104.3

↓

Unemployment rate

Average in 2025

4.4

4.1

↓

Nominal earnings

Average growth in 2025

2.1

3.6

↑

RHDI per person

Level in 2028 (Index, 2019=100)

103.4

102.5

↓

Nominal GDP

Level in 2028 (£ billion)

3,179

3,251

↑

Key: ↑ Higher, ↓ Lower, ⚊ Unchanged

Source: OBR

Conditioning assumptions

Fiscal policy

2.2 The measures announced at this Budget significantly loosen fiscal policy. Public sector net borrowing is around 1 per cent of GDP higher in every year from 2025-26 onwards. We assume this boosts the level of real GDP significantly in 2025-26 but leaves it broadly unchanged by 2029-30. This significant increase in borrowing, compared to the previous Government’s plans that were set out in the March Budget, is the net result of even larger changes in both spending and receipts. In 2028-29, current spending is 1¼ per cent of GDP higher than in our March forecast, departmental capital spending is ⅔ per cent of GDP higher, and taxes are 1 per cent of GDP higher. These changes also have significant effects on economic activity, prices, and interest rates, as we discuss in Box 2.1.

2.3 However, despite the fiscal loosening, after being broadly flat in 2024-25, borrowing is still forecast to fall in 2025-26 and over the rest of our forecast period. This means that, over the medium term, the boost to demand from fiscal policy is still expected to wane. Two-thirds of the 2½ per cent of GDP reduction in primary borrowing by our 2029-30 forecast horizon comes from rising receipts.

Box 2.1: The economic effect of policy measures

Our economy forecast accounts for the economic impacts of the latest announced government policies (described in detail in Chapter 3). This Budget delivers a significant and sustained loosening of fiscal policy which increases borrowing by £35 billion (1.2 per cent of GDP) in 2025-26 and by £30 billion (0.9 per cent of GDP) in 2029-30. This increase in borrowing relative to our pre-measures forecast is the net result of:

a £72 billion (2.1 per cent of GDP) increase in spending in 2029-30, around two-thirds of which is current spending and one-third capital spending; and

a £42 billion (1.2 per cent of GDP) increase in taxes in 2029-30, of which over half comes from an increase in employer National Insurance contributions (NICs).

The significant and sustained increase in public spending is only partially offset by tax rises, so the Budget delivers a temporary boost to demand and lifts it from below to above supply. This fiscal loosening is front-loaded, with the impact on demand peaking at 0.6 per cent in 2025-26. To inform the size of this demand boost we apply our standard ‘multipliers’ drawn from the empirical literature which taper to zero over the five-year forecast horizon.a, b

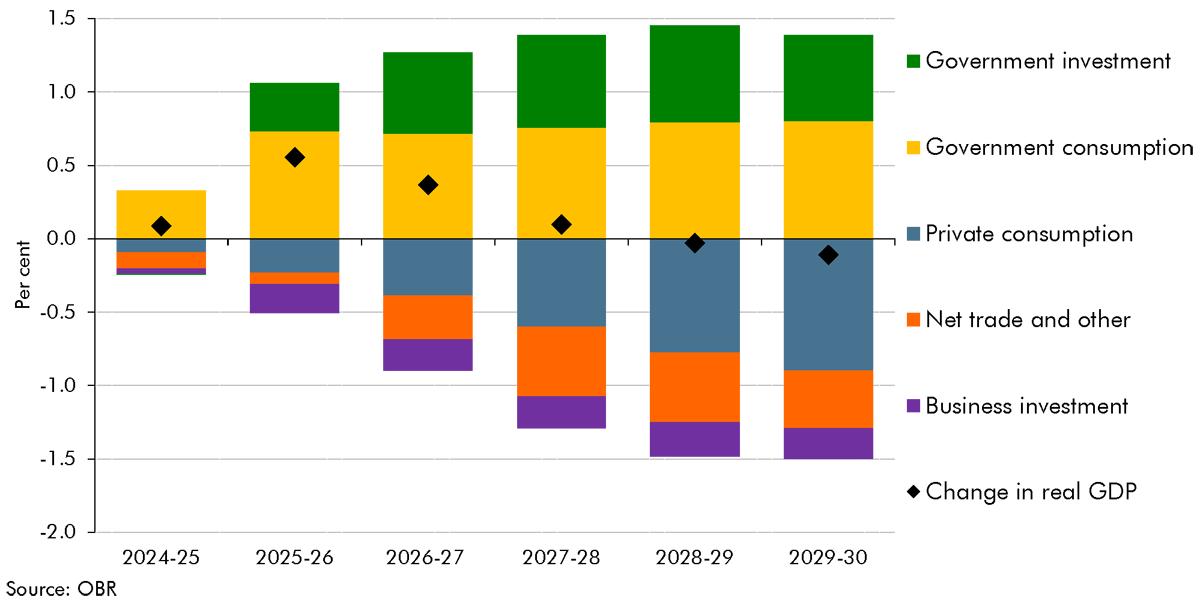

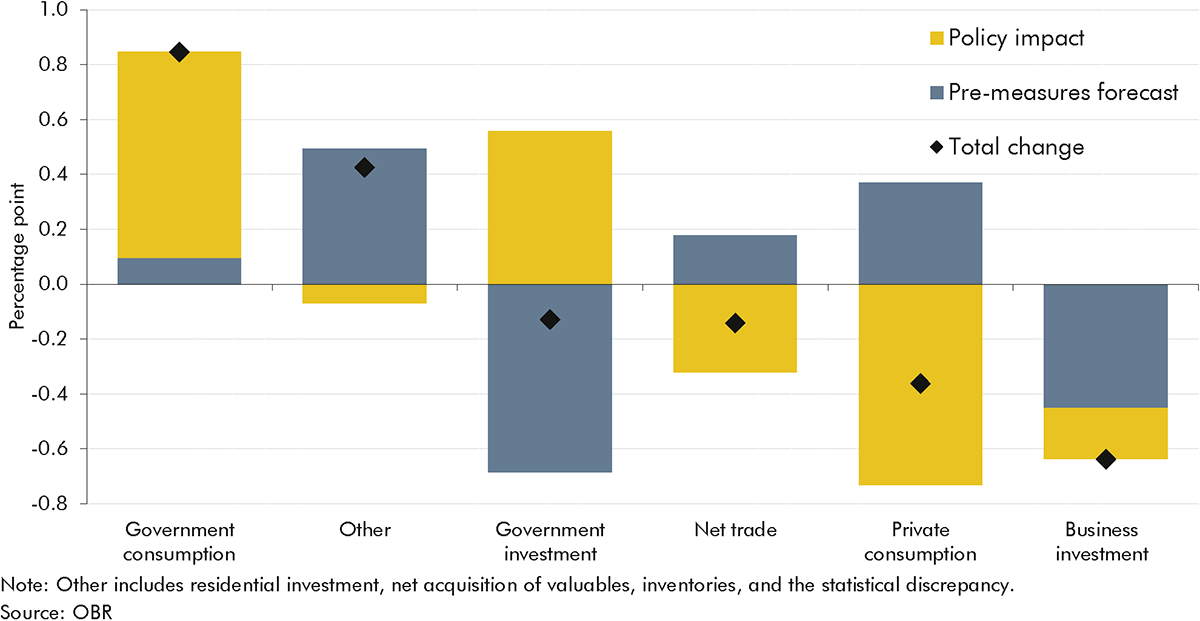

The gross and net changes in fiscal policy have significant effects on the expenditure composition of GDP (Chart A). There is a large increase in government spending over the five-year forecast. In an economy that is currently operating close to capacity and that is little changed in size at the forecast horizon, this has to be accommodated through a decrease in private sector spending and some rise in net imports. Part of this decrease comes through Budget policies, as higher taxes weigh on disposable income and, as a result, private consumption. But, as a consequence of higher interest rates, real wage adjustments, and capacity and skilled worker constraints, there is also some further crowding out of business investment, consumption, and net trade.

Chart A: Policy impacts on real GDP and its components

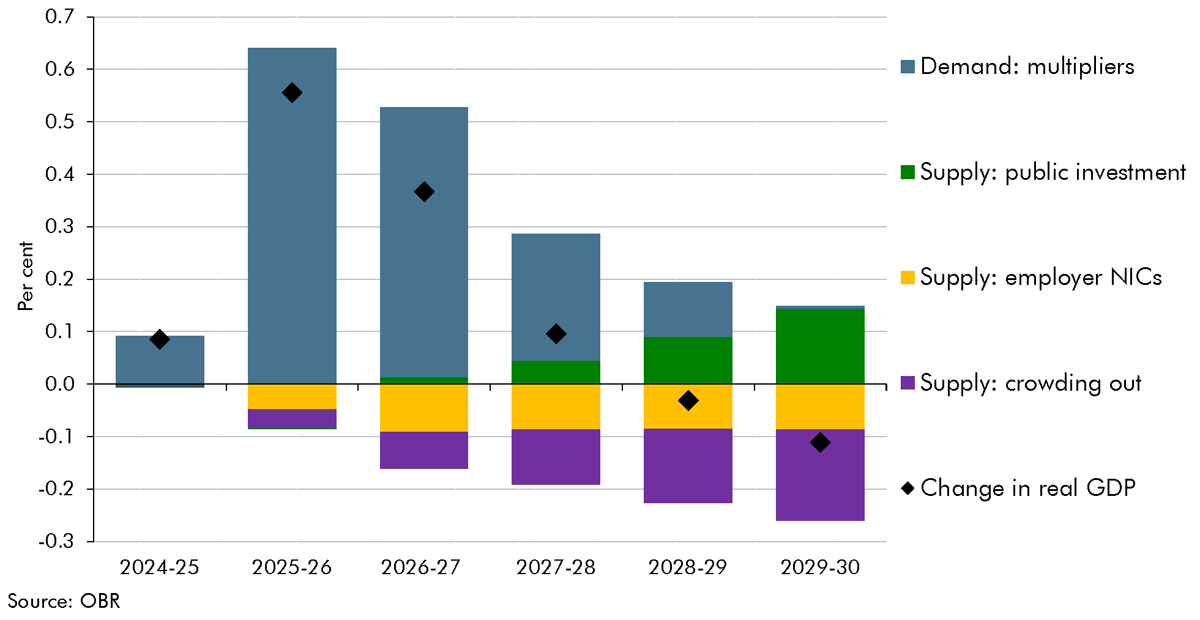

Some Budget policies also have lasting impacts, some positive and some negative, on the supply side of the economy. Their net effect on potential output is broadly neutral by the five-year forecast horizon, but becomes positive from the early 2030s. In this Budget, policies which we expect to have significant, material, and additional impact on potential output are:

The increase in employer NICs,which we estimate will reduce the level of potential output by 0.1 per cent at the forecast horizon (yellow bars, Chart B). As discussed further in Chapter 3, the NICs rise increases employer payroll costs by just under 2 per cent. We assume this lowers real wages and profits, and workers and firms reduce labour supply and demand in response, reducing labour supply by around 50,000 average-hours equivalents.

The 0.6 per cent of GDP average increase in departmental capital spending from 2025-26 raises potential output by 0.14 per cent in 2029-2030 (green bars, Chart B).c By 2029-30, the stock of completed and fully utilised capital projects only increases by 0.6 per cent of GDP due to time lags associated with the economic impact of investment spending (and because not all the increase in departmental spending raises the Government’s own stock of assets), raising GDP by 0.11 per cent. As these investments are assumed to be a complement to those made by the private sector, extra business investment provides a small further boost to potential output of 0.04 per cent of GDP in 2029-30. Chapter 3 describes these growing impacts in further detail, and Box 3.3 explains risks around these judgements and explores alternative scenarios.

As discussed above, with output close to potential in our pre-measures forecast, the net fiscal loosening crowds out some private sector spending, including on business investment, which reduces the private capital stock by 0.7 per cent and potential output by 0.2 per cent in 2029-30 (purple bars, Chart B).

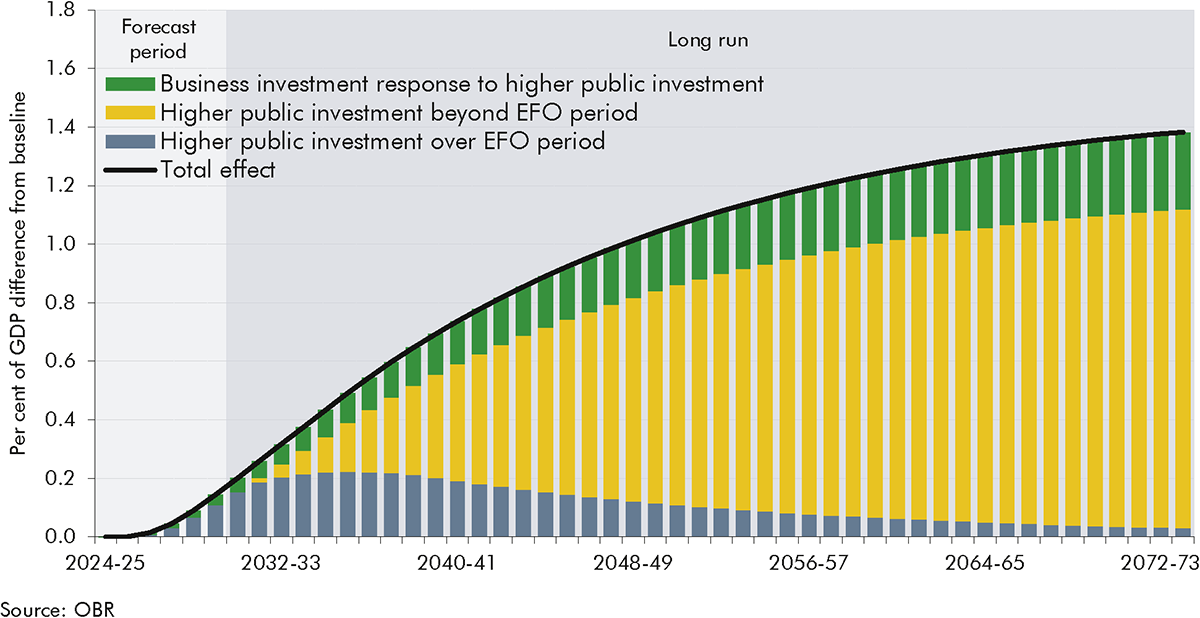

The combined effect of Budget policies on supply and demand over the forecast is shown in Chart B. Overall, the demand stimulus peaks in 2025-26 and fades over the remainder of the forecast. By contrast, there is a gradual build-up of the (positive) supply-side effects of the increase in public investment and of the (negative) supply-side effects of the employer NICs increases, and some crowding out of private investment. The supply-side impacts largely offset each other at the forecast horizon, leaving potential output little changed in 2029-30 (diamonds, Chart B). As discussed in Chapter 3, we expect the package as a whole would then have a net positive effect on potential output beyond the forecast horizon (starting in 2032-33). At the 50-year horizon, if the increase in public sector investment announced in this Budget were maintained as a share of GDP, this would increase GDP by around 1½ per cent.

Chart B: Policy impacts on real GDP, by measure

As discussed in paragraph 2.4, we judge that the loosening is consistent with a slightly higher path for interest rates than in our pre-measures forecast, raising both Bank and gilt rates by a ¼ percentage point across the forecast and at all maturities. Higher interest rates help to bring demand back into line with supply over the forecast period and account for some of the crowding out of business investment by raising the cost of capital.

Budget policies increase CPI inflation by 0.4 percentage points in 2025-26 and 0.3 percentage points in 2026-27, reflecting the combined effect of several measures, and leave the CPI level 1 per cent higher in 2029-30. The fiscal impulse raises the CPI level 0.6 per cent by the end of the forecast, with the effect of firms passing on part of the cost of the NICs measure to consumer prices adding a further 0.2 per cent. The introduction of VAT on private school fees and the reform to VED rates each add a further 0.1 per cent, while the fuel duty freeze lowers inflation in 2025-26 but increases it 2026-27, being neutral to the CPI level by 2029-30. Whole-economy inflation is also boosted by the increase in departmental spending, a proportion of which translates into higher prices. Together with the impact on consumer prices, this leaves the GDP deflator 1.3 per cent higher in 2029-30. Overall, the impact of policies in the Budget therefore leaves nominal GDP 1.2 per cent higher at the forecast horizon.

a) See Box 2.2 in our December 2019 Forecast evaluation report and Box 2.1 in our November 2020 Economic and fiscal outlook.

b) We have also made a small adjustment to lower the impact on demand in 2025-26 and raise it thereafter, to reflect the economy’s proximity to its supply capacity and the likelihood that imports therefore meet a larger proportion of the initial expansion than would otherwise be the case.

c) See Suresh, N., R. Ghaw, R. Obeng-Osei, and T. Wickstead, OBR Discussion paper 5: Public investment and potential output, August 2024, for a discussion of these transmission channels. We are grateful to the respondents to our discussion paper, including Venables, T., The impact of public investment on private investment: comment on ‘Public investment and potential output’, 2024, and National Institute of Economic and Social Research, Public Investment and Potential Output, 2024.

Monetary policy, gilts, and equity prices

2.4 Our pre-measures forecast was based on market expectations over the 10 working days to 12 September. The substantial fiscal easing in this Budget, boosting demand and borrowing, was not likely to have been fully anticipated by market participants at this time. We have therefore increased our Bank Rate and gilt rate forecasts by a ¼ percentage point over the five-year period in our post-measures forecast. Output is projected to be modestly above potential for much of the forecast period. The fiscal multipliers that we use to quantify the economic impact of the Budget assume that part of the crowding out of the fiscal impulse is a consequence of higher interest rates to keep inflation at target. This ¼ percentage point increase is broadly consistent with movements in market expectations between early September and mid-October, which could be consistent with market participants anticipating more of the Budget policies.

2.5 Bank Rate falls from its current level of 5 per cent to around 3½ per cent from 2027 onwards as the output gap closes and domestically generated inflation eases (Chart 2.1, left panel). Compared to our March forecast, Bank Rate is on average 0.4 percentage points higher in 2025 and 2026. Just over half of this reflects our post-measures adjustment. Since March, market expectations for Bank Rate in 2025 have ranged from 3.6 to 4.7 per cent, underscoring the continued uncertainty around the monetary policy outlook.

2.6 Five-year gilt yields are forecast to rise from 3.8 per cent on average this year to 4.4 per cent in 2029, on average 0.2 percentage points higher than our March forecast (Chart 2.1, right panel). Five-year gilt yields are more than 3 percentage points above their 2021 average and have remained volatile since our March forecast, with the daily spot yields ranging from 3.5 to 4.2 per cent. We explore the fiscal implications of higher interest rates in Chapter 7.

Chart 2.1: Bank Rate and five-year gilt yield

2.7 Equity prices, as measured by the FTSE All-shares index, have risen significantly since our March forecast. Equity prices are assumed to grow in line with nominal GDP in our forecast and are around 9 per cent higher over the forecast period than projected in March. Equity prices are an important determinant for our capital taxes forecast, and also drive the value of equity assets within public sector net financial liabilities (PSNFL) (see Annex B).

Commodity prices

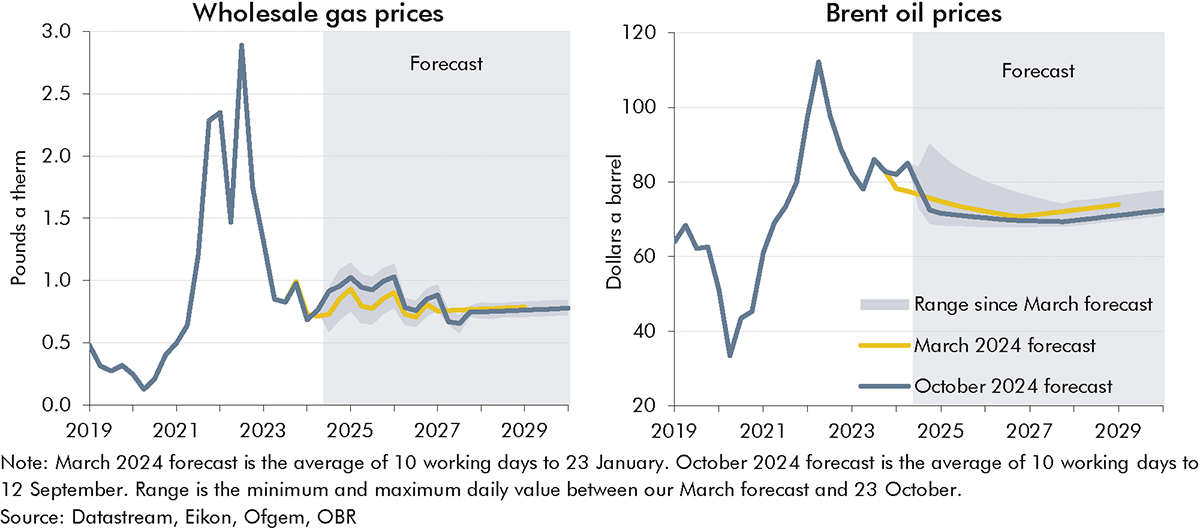

2.8 Gas prices are expected to average 97 pence a therm in 2025, 16 per cent higher than in our March forecast (Chart 2.2, left panel). Prices fell sharply from their quarterly peak of 289 pence a therm in the second half of 2022 to a low of 69 pence a therm at the beginning of this year. Prices have risen since, driven by expectations of a colder winter and the continued conflicts in Ukraine and the Middle East. The outlook for gas prices remains uncertain, underscored by price expectations for 2025 ranging between 70 and 108 pence a therm since our March forecast.

2.9 Oil prices are forecast to fall from 83 dollars a barrel in the first half of this year to around 70 dollars a barrel in 2025, and remain around that level over the forecast (Chart 2.2, right panel). The downward trend in oil prices reflects slowing growth in global oil demand led by weaker consumption in China and higher world supply from non-OPEC countries.[1] Compared to our March forecast, oil prices were 7 per cent higher in the first half of 2024 but are 3 per cent lower on average over the forecast.

2.10 Volatile energy prices continue to pose a risk to our forecast, as illustrated by the wide range of market expectations for prices since our March forecast (the swathes in Chart 2.2). Box 2.2 in our March 2024 Economic and fiscal outlook (EFO) included a scenario illustrating the economic risks posed by an escalation in the conflicts in the Middle East. In the scenario, we assumed a cut to energy supplies from the region comparable to the 1973 oil embargo and disruption to global supply chains similar to the height of the pandemic. This contributed to wholesale oil and gas prices rising 75 per cent above our central forecast at the time. CPI inflation peaked at 7.4 per cent in 2025, almost 6 percentage points above our then central forecast. The impact on inflation, interest rates and GDP pushed government borrowing £23 billion higher on average over the forecast.

Chart 2.2: Gas and oil prices

World economy and the exchange rate

2.11 Since our March forecast, the IMF has revised its projection for world GDP growth up slightly across the forecast period from 3.1 to 3.2 per cent on average.[2] This medium-term forecast is still significantly lower than the 2010-to-2019 average of 3.8 per cent, reflecting lower productivity growth and increasing global economic fragmentation. The trade-weighted sterling effective exchange rate has strengthened since our March forecast, driven by expectations of higher interest rates in the UK compared to the US and the eurozone. We hold the effective exchange rate constant in nominal terms, so it is 2.9 per cent higher than in March across the forecast.

Potential output

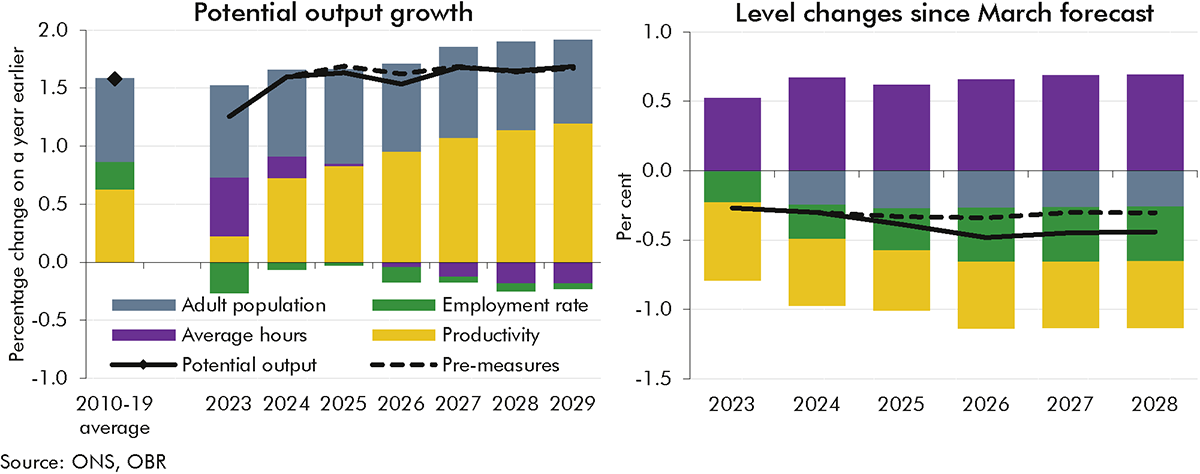

2.12 Our estimate of potential output growth averages around 1⅔ per cent over the forecast period. This is little changed from our March forecast, though the profile is slightly different reflecting the impact from measures in this Budget. Chart 2.3 summarises our central potential output forecast, with more detail on each component in the rest of this section:

The level of potential output in 2024 is 0.3 per cent lower than our March forecast because, while GDP outturn has surprised on the upside, we judge that this is more than explained by there being less spare supply capacity than in March.

Pre-measuresgrowth in potential output from 2025 to 2028 is unchanged from our March forecast at 1⅔ per cent a year on average (Chart 2.3, left panel). Labour supply growth slows over the forecast, mainly due to an ageing population dragging on trend participation and average hours worked. This is countered by a recovery in productivity growth towards our estimated long-term rate which is roughly halfway between its pre- and post-financial crisis averages.

Measures at this Budget are estimated to have a broadly neutral impact on potential output by the five-year forecast horizon but, if sustained, would deliver a net boost to the supply side of the economy in the 2030s. As described in Box 2.1 and Chapter 3, the net impact of Budget policies on potential output is the sum of: (i) the immediate negative impact of both the rise in employer NICs on the demand and supply of labour, and of crowding out of business investment from the overall loosening of fiscal policy; and (ii) the positive contribution from the increase in public investment spending, and its positive knock-on impact on business investment, which build over the forecast.

This leaves the level of potential output in 2028 0.4 per cent lower than in March, 0.3 percentage points reflecting our pre-measures outlook and 0.1 percentage points reflecting policies in this Budget (Chart 2.3, right panel).

Chart 2.3: Potential output growth and level changes since March

Labour supply

2.13 Labour supply growth falls from 0.9 per cent in 2024 to around 0.5 per cent in 2029, mainly driven by the drag on average hours worked from an ageing population. Labour supply is broadly unchanged from our March forecast. This is because higher average hours in outturn broadly offset a lower adult population in outturn and a lower employment rate (both from outturn data and the impact of the increase in employer NICs). The key drivers of the forecast are:

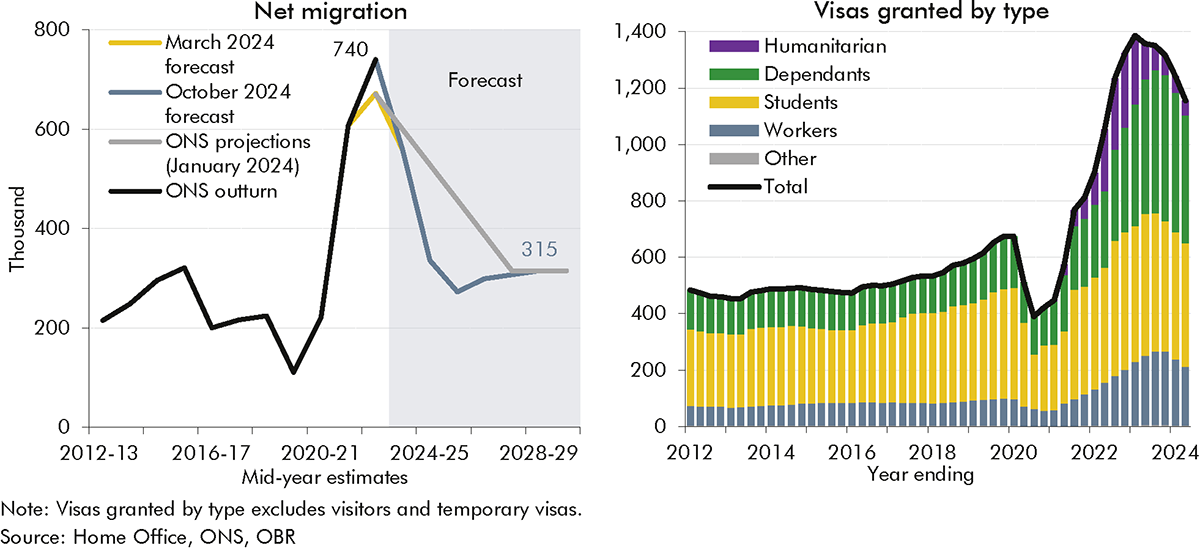

The adult population rises from 55.2 million in 2024 to 57.3 million in 2029. The Labour Force Survey (LFS) outturn for adult population in the second quarter of 2024 was 153,000 lower than we had expected in March, a difference that is largely carried through into the forecast. But this does not fully reflect the recent strength in net migration.[3] The adult population grows at a similar pace as in our March forecast, largely (around two-thirds) driven by net migration.

We forecast net migration to fall from 740,000 in the year to June 2023, 68,000 higher than estimated in March due to ONS revisions, to reach 315,000 in the medium term. The latter is in line with the ONS’s latest medium-term population projections and our March forecast (Chart 2.4, left panel). Net migration has already fallen to 685,000 in the year to December 2023. And more recent Home Office data, covering the period until the second quarter of 2024, show visas granted falling sharply (Chart 2.4, right panel). This largely reflects government restrictions coming into force in the first half of this year, which we now expect to have a slightly larger impact than we anticipated in March. We judge the stronger outturn and larger policy impact to be broadly offsetting, and therefore project net migration will continue to fall in line with our March forecast.

The trend participation rate is expected to slope gently downwards over the forecast from 62.7 per cent in 2024 to 62.5 per cent in 2029. The drag from an ageing population, rising health-related inactivity, and the rise in employer NICs is only partially offset by increases in childcare provision, a rise in the state pension age, and the boost from migrants (who are disproportionately of working age).[4] On a pre-measures basis, we have lowered the trend participation rate by an average of 0.2 percentage points relative to March, due to weaker outturn data and a reassessment of the effects of previously announced labour supply policies (see Box 3.2). The increase in employer NICs in this Budget lowers the trend participation rate by a further 0.1 percentage points from 2025-26.

Trend average hours worked fall gradually over our forecast from 31.9 in 2024 to 31.8 in 2029, reflecting the drag of an ageing population. Relative to our March forecast, trend average hours are 0.7 per cent higher in 2024 due to stronger-than-expected outturn data for the first half of 2024. But the cumulative percentage fall over the forecast (and, therefore, contribution to potential output growth) is similar to March, at around ½ per cent.

Chart 2.4: Net migration forecast and visas granted

Profits and investment

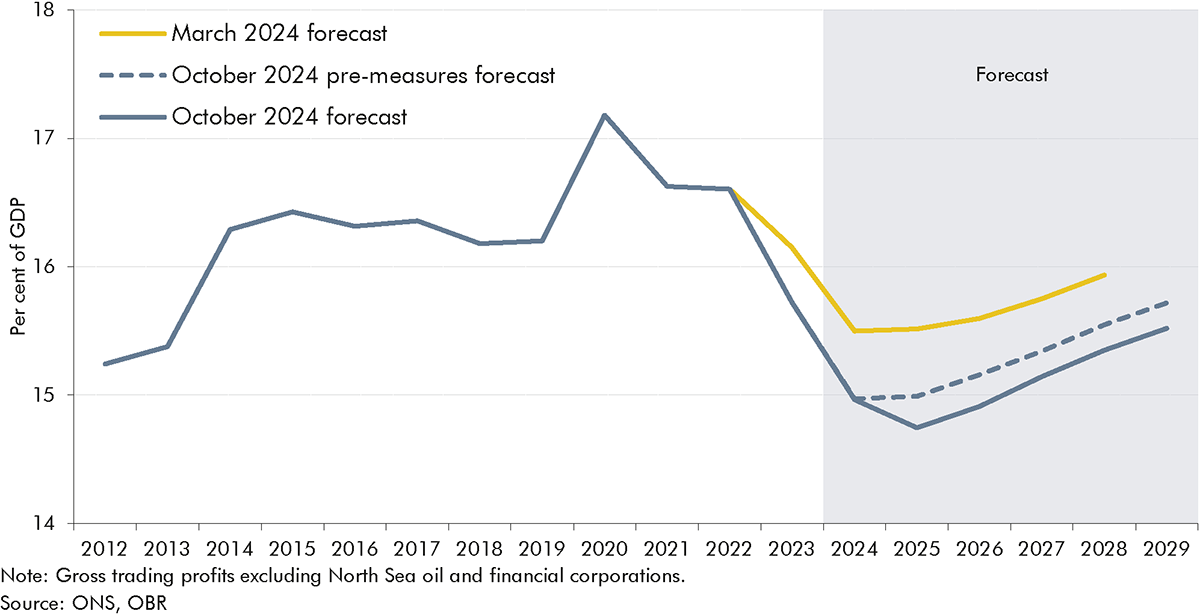

2.14 As a share of GDP, corporate profits (excluding financial and North Sea corporations) are expected to continue to fall from a peak of over 17 per cent in 2020 to around 14½ per cent in 2025. In the near term, wage settlement expectations have held up relative to recent falls in inflation expectations which, if realised, will continue to weigh on firms’ profit margins. The rise in employer NICs in this Budget will further erode profits and we assume firms are only able to pass on around 60 per cent of the cost to employees in the short term. We then expect the profit share to rise gradually from 2026 as firms rebuild margins and pass on more of the cost of the rise in employer NICs to higher consumer prices and lower nominal wages. By the end of the forecast, profits are expected to reach 15½ per cent of GDP. Compared to our March forecast, profits as a share of GDP are around ⅔ percentage point lower on average between 2024 and 2028. About one-third of this difference is explained by this Budget. Uncertainty around precisely how the Government’s Employment Rights Bill and Plan to Make Work Pay will eventually be implemented means that they represent a policy risk to our forecast (see Chapter 3 for more details).

Chart 2.5: Profits as a share of GDP

2.15 Business investment outturns were stronger than expected in the first half of 2024, with the level in the second quarter around 6 per cent higher than our March forecast. Our pre-measures business investment forecast assumed that some of this recent strength reflects temporary factors. Therefore, business investment returns to around its pre-Covid average share of GDP as these unwind and the squeeze on profit margins bites. Growth averages around 0.3 per cent over 2024 to 2028, 0.1 percentage points lower than our March forecast. In our central forecast, the net impact of policies at this Budget lowers business investment. Higher government investment increases incentives for businesses to invest, but in the near term this is more than offset by the crowding out effect of the fiscal loosening in this Budget (see Box 2.1 and Chapter 3). There was a large downward revision to business investment in the Blue Book 2024 which largely offsets the upside surprise in outturn since March, but was published too late to incorporate into our forecast.[5]

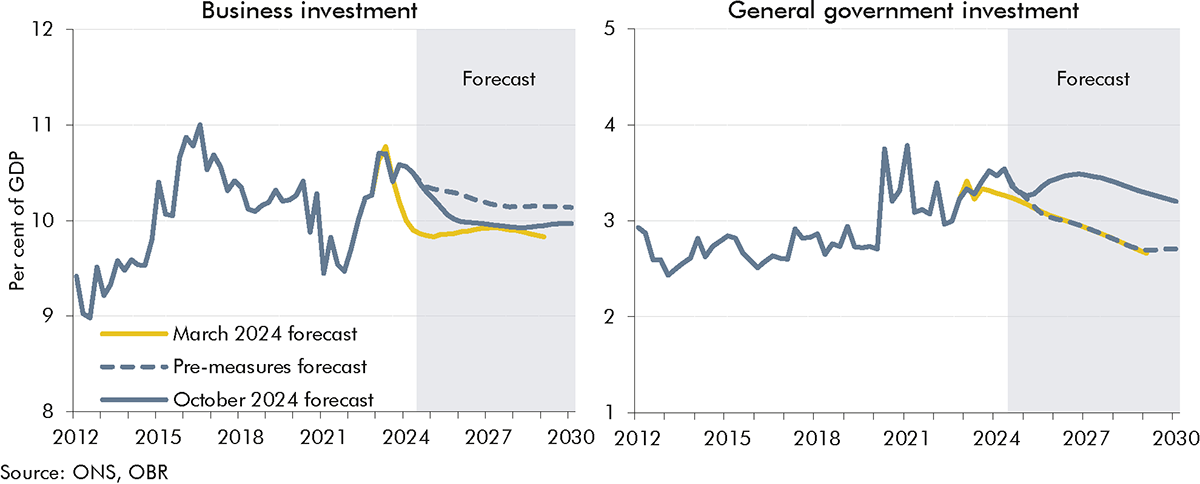

2.16 On a pre-measures basis, real government investment was forecast to fall as per cent of GDP from 3.4 this year to 2.7 in 2029, in line with spending plans in the March 2024 Budget. Higher departmental capital spending in this Budget raises real government investment by 15 per cent on average from 2025 to 2029, leaving it broadly stable at 3.4 per cent of GDP over the forecast period.

Chart 2.6: Business and government investment as a share of GDP

Productivity

2.17 Trend productivity growth (output per hour worked) picks up over the forecast from 0.2 per cent in 2023 to 1¼ per cent in 2029, little changed from March. This is a significant rise from an average rate of ⅔ per cent in the decade following the financial crisis. But it is still well below the average of around 2¼ per cent in the decade preceding the financial crisis. This forecast is comprised of:

Capital deepening (proxied by the change in the capital stock per hour worked) contributes ¼ percentage point to average annual productivity growth over the forecast period. It is broadly unchanged from March and reflects offsetting changes to our business and government investment forecasts as described above and shown in Chart 2.6. Budget policies raise whole-economy investment by 1.5 per cent on average from 2025 and by 1.7 per cent at the forecast horizon. Government investment takes longer to affect potential output than business investment. In turn, the measures in this Budget leave capital deepening broadly unchanged over the forecast, despite the increase in whole-economy investment. The impact of these measures on capital deepening is expected to become positive beyond our forecast horizon, as described in Chapter 3.

Total factor productivity (TFP, the economy’s efficiency at combining capital and labour to produce output) contributes ¾ percentage point to average productivity growth over the forecast period, unchanged from March. The outlook for TFP and overall productivity is one of our most important and uncertain forecast judgements. In our November 2023 EFO, we illustrated the sensitivity of the public finances to annual productivity growth being ½ percentage point higher or lower than in our central forecast. In the upside scenario, borrowing was £46 billion lower in 2028-29, and in the downside, borrowing was £42 billion higher.

Real GDP and the output gap

Historical GDP estimates

2.18 The level of GDP in the second quarter of 2024 was 0.3 per cent higher than we expected in our March forecast. This was due to the combination of a downward revision of 0.2 percentage points to GDP growth in 2023 and 0.7 percentage points upside surprise to growth in the first half of 2024. This forecast incorporates the first ONS estimate of quarterly GDP released on 15 August that provided outturn data up to the second quarter of 2024. The Blue Book 2024 data released on 30 September and the partial release by the ONS on 7 August were published too close to the Budget date for us to be able to include them in our pre-measures forecast that was finalised on 26 September. Box 2.2 sets out the potential implications of these data.

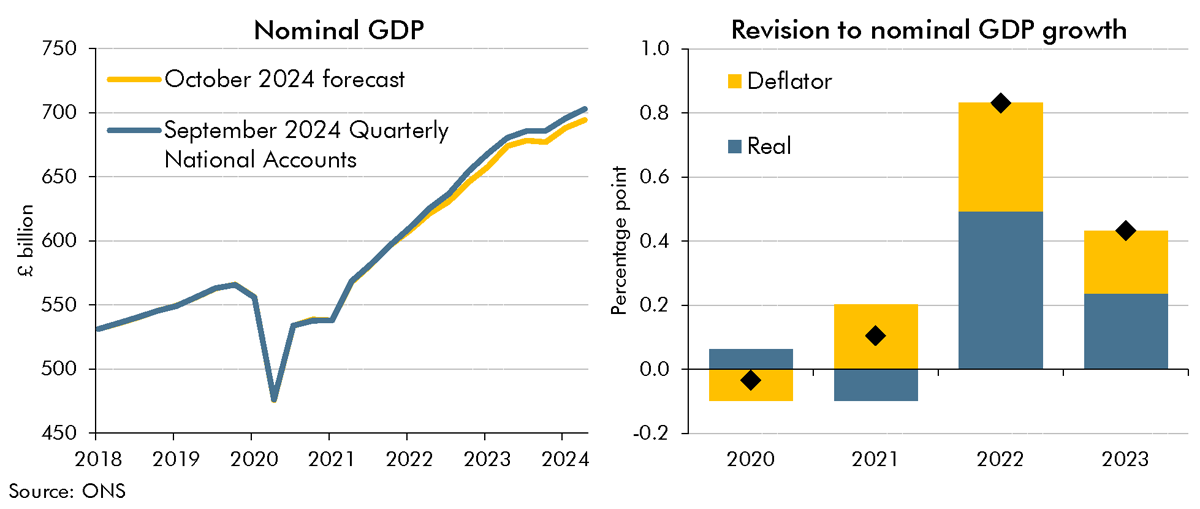

Box 2.2: Blue Book 2024 revisions

The Blue Book is an annual ONS publication which updates the sources and methods used for the UK National Accounts. The Blue Book 2024 will be published on 31 October. The implications for GDP up to and including 2022 were preannounced on 7 August.a The complete revisions to GDP from the Blue Book, including 2023 and the first half of 2024, were incorporated into the Quarterly National Accounts (QNA) published on 30 September. Since the full revisions were published after our pre-measures economy forecast was finalised, they were not incorporated into our forecast. The revisions indicate that the economy grew slightly faster in the years following the pandemic than previously estimated, in both real and nominal terms. As a result, the revisions would have raised the starting level of GDP in our forecast.

The Blue Book revisions raised the level of nominal GDP in the second quarter of 2024 – the starting point of our forecast – by 1.2 per cent. This reflects upwards revisions to growth in both real GDP and the GDP deflator. Cumulative real GDP growth since 2020 was revised up 0.5 percentage points, driven by higher growth in transport, professional, and business support services industries. Cumulative growth in the GDP deflator over the same period was revised up 0.7 percentage points, underpinned by upwards adjustments to the government consumption deflator and the terms of trade. The revisions were primarily concentrated in 2022, with nominal GDP growth revised up 0.8 percentage points. Nominal growth in 2023 was increased by 0.4 percentage points but this was mainly due to the base effects of the revisions to growth in 2022. And with little change to growth in 2024, the revisions provide limited new information on current economic momentum or inflationary pressures. Therefore, they would not have materially impacted our forecasts for GDP growth and inflation had we been able to include them.

Chart C: Nominal GDP

For the public finances, growth in nominal GDP can provide useful insight into developments in the size of the tax base. In outturn, the upward revision to the historical level of nominal GDP would not in and of itself affect our receipts forecast because it would offset in a correspondingly lower effective tax rate. The jumping off point for the receipts forecast also benefits from more timely receipts data that is less prone to revision. For all fiscal aggregates, the higher level of nominal GDP will only have a purely arithmetic effect by mechanically lowering metrics as a share of nominal GDP. In Chapters 4, 5 and 6 we note the implications of the upward revision in 2023-24 if this were applied throughout all years of the forecast.

a) ONS, Blue Book 2024: advanced aggregate estimates, August 2024.

Real GDP forecast

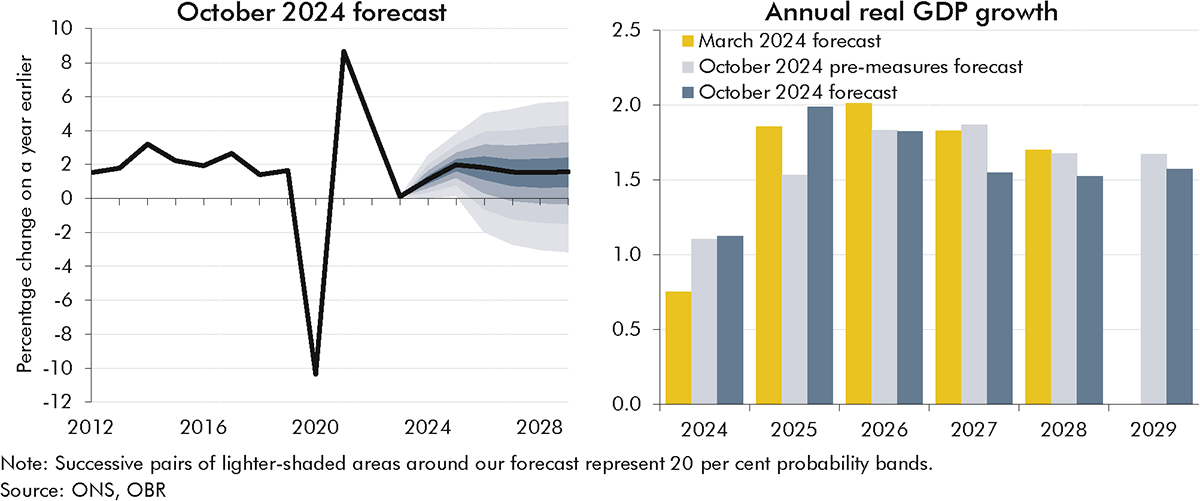

2.19 Our central forecast is for real GDP growth to accelerate from 1.1 per cent in 2024 to 2.0 per cent in 2025 and 1.8 per cent in 2026. This is driven by interest rates falling, the household saving rate passing its peak, and Budget measures temporarily boosting demand. After stagnating over 2023, real GDP growth picked up sharply in the first half of 2024. However, we judge that underlying momentum in the economy was weaker than headline growth. Notably, growth was led by volatile and non-fiscally relevant components of GDP, while growth in consumption and business investment was modest. Monthly GDP figures up to August also support this judgement and we expect quarterly growth to drop back in the third quarter. Timely indicators suggest underlying economic activity is picking up gradually. Measures of consumer and business confidence have generally trended higher over this year, albeit some have fallen back in recent months, and the S&P Global/CIPS UK composite PMI points to a modest expansion in activity. So we expect growth to pick back up in the fourth quarter of 2024 and the first half of 2025. In 2025, the demand impact of this Budget increases growth by 0.5 percentage points relative to our pre-measures forecast. Compared to our March forecast, growth is 0.4 and 0.1 percentage points higher, respectively, in 2024 and 2025.

2.20 As the effects of monetary policy easing fade and the support to demand from fiscal policy wanes, GDP growth slows to around 1½ per cent from 2027 onwards. This is slightly below our estimate of potential output growth as a small positive output gap that is expected to open up over 2025 and 2026 closes. The level of GDP in the first quarter of 2029 is around 0.4 per cent lower than our March forecast. Of this, 0.3 percentage points reflect the pre-measures upward revision to the starting output gap, which leaves less scope for above-trend GDP growth over the forecast. The remaining 0.1 percentage points is due to the net impact of measures announced in this Budget, as described in Box 2.1.

2.21 As always, our central real GDP forecast is uncertain, with pre-measures forecast judgements, the impact of policies, and unforeseen external shocks all potential sources of difference between outturn and forecast. The outlook for productivity growth remains our most important and uncertain forecast judgement. The effects of subdued investment, the energy price shock, and Brexit compound the ongoing weakness seen since the financial crisis. In this Budget, the temporary demand effects of the significant net fiscal loosening and the supply-side impacts of the tax and public investment increases are also uncertain. And the financial crisis, pandemic, and energy price shock showed that unforeseen external shocks can have a large impact on the UK. To give some sense of the potential range of uncertainty, based on historical forecast errors there is a roughly one-in-five chance that annual GDP growth in 2025 is either negative or above 4 per cent.

Chart 2.7: Real GDP growth

2.22 In per-person terms, real GDP growth picks up from 0.2 per cent in 2024 to average around 1.2 per cent over the rest of the forecast. Weak productivity growth and falls in the participation rate meant that real GDP per person fell for seven consecutive quarters over 2022 and 2023. In our central forecast, real GDP per person is expected to recover to its early 2022 level by the start of 2025 as productivity growth picks up, and the participation and saving rates start to stabilise. The temporary boost to demand in this Budget raises real GDP per person by ½ per cent in 2025 relative to our pre-measures forecast, and leaves it little changed at the forecast horizon.

Output gap

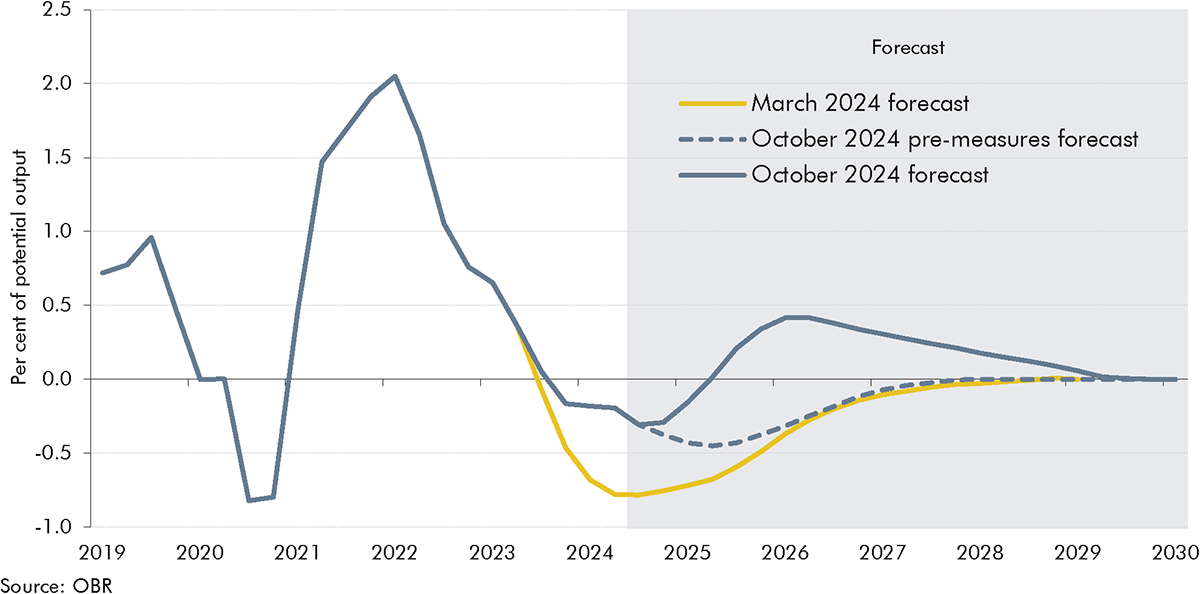

2.23 Latest indicators suggest that there is currently very little spare capacity in the economy. Our estimate of the output gap (real GDP relative to our estimate of potential output) in the second quarter of 2024 is therefore narrower (less negative) than we anticipated in March, at minus 0.2 per cent compared to minus 0.8 per cent. Capacity utilisation indicators have been falling since the middle of 2022 and are now at around their long-run average, suggesting little spare capacity within firms. Recruitment difficulties remain above normal levels, albeit falling, suggesting the labour market remains fairly tight despite a slight recent loosening and steady falls in vacancies. Given these movements, our models – within a wide range – suggest a current output gap of around zero. However, the directly unobservable nature of the output gap means there is significant uncertainty around these estimates.

2.24 As Budget measures boost real GDP growth at a time when monetary policy is loosening, we expect a small positive output gap to open up and peak at 0.4 per cent in 2026 (Chart 2.8). As the effects of monetary policy easing fade and the support to demand from fiscal policy wanes, the output gap closes in 2029. In our pre-measures forecast, we expected a small negative output gap to persist until mid-2027 but the impact of policy measures results in a small positive output gap for four years from mid-2025. Compared to our March forecast, the output gap is 0.6 percentage points higher on average in 2025 and 2026 due to our judgement of less spare capacity in 2024 and the impact of this Budget.

Chart 2.8: Output gap

Expenditure composition of GDP

2.25 The policies announced in this Budget lead to a significant and sustained increase in real government consumption and investment relative to March. As a share of GDP, real government consumption rises by around 0.8 percentage points from 2023 to 2029. Government investment is broadly flat as a share of GDP over the same period, rather than falling by around ¾ percentage points in our pre-measures forecast (Chart 2.9). Budget policies are also expected to weigh on real household disposable income (RHDI) and private consumption. But the former effect is larger than the latter effect. And given we think that there is currently little spare capacity in the economy, the expansion of public sector activity would be expected to compete for some of the same resources demanded by the private sector, pushing up prices. The Bank of England would be expected to act to bring inflation back to target over the medium term. This results in some crowding out of private consumption, business investment and net trade over our forecast period. So, by the forecast horizon, government spending comprises a larger part of little-changed real GDP.

2.26Real private consumption is forecast to fall 0.4 percentage points as a share of GDP from 2023 to 2029. In our pre-measures forecast, we expected this share to rise by 0.4 percentage point but this is more than offset by policy measures in the Budget. Policies are expected to weigh on consumer spending both due to the direct effect on RHDI and from crowding out. Private consumption was slightly weaker in the first half of 2024 than projected in March. In our central forecast, private consumption growth now picks up from 0.4 per cent in 2024 to 1.7 per cent in 2025. The saving rate levels out in 2025, after rising in 2023 and 2024, alongside falling interest rates and a drop in the unemployment rate. Consumption growth is steady over the rest of the forecast as a lower rate of saving smooths through falls in real income growth. The level of consumption is 1.6 per cent lower at the start of 2029 than in our March forecast.

2.27Real business investment is expected to fall 0.6 percentage points as a share of GDP from 2023 to 2029. This is driven by two factors. First, our pre-measures forecast anticipates a decline back to the recent historical average share of GDP as a recent temporary boost reverses. Second, we expect this Budget to result in some crowding out as a result of the increase in government spending and net fiscal loosening. After surprising on the upside in the first half of 2024, real business investment growth is expected to average 0.8 per cent between 2025 and 2029.

2.28Net trade is broadly stable as a share of GDP over the forecast. Exports declined slightly over the first half of 2024, but we expect growth to resume in 2025 and average 0.5 per cent over 2026 to 2029. There have been sharp changes in imports in 2024, but a considerable share of this was driven by volatile components of trade data, and so we expect it to unwind. We forecast import growth to average 1 per cent a year over 2026 to 2029. Weak growth in imports and exports over the medium term partly reflect the continuing impact of Brexit, which we expect to reduce the overall trade intensity of the UK economy by 15 per cent in the long term (see Box 2.4 of our March 2024 EFO).

Chart 2.9: Change in expenditure shares of real GDP from 2023 to 2029

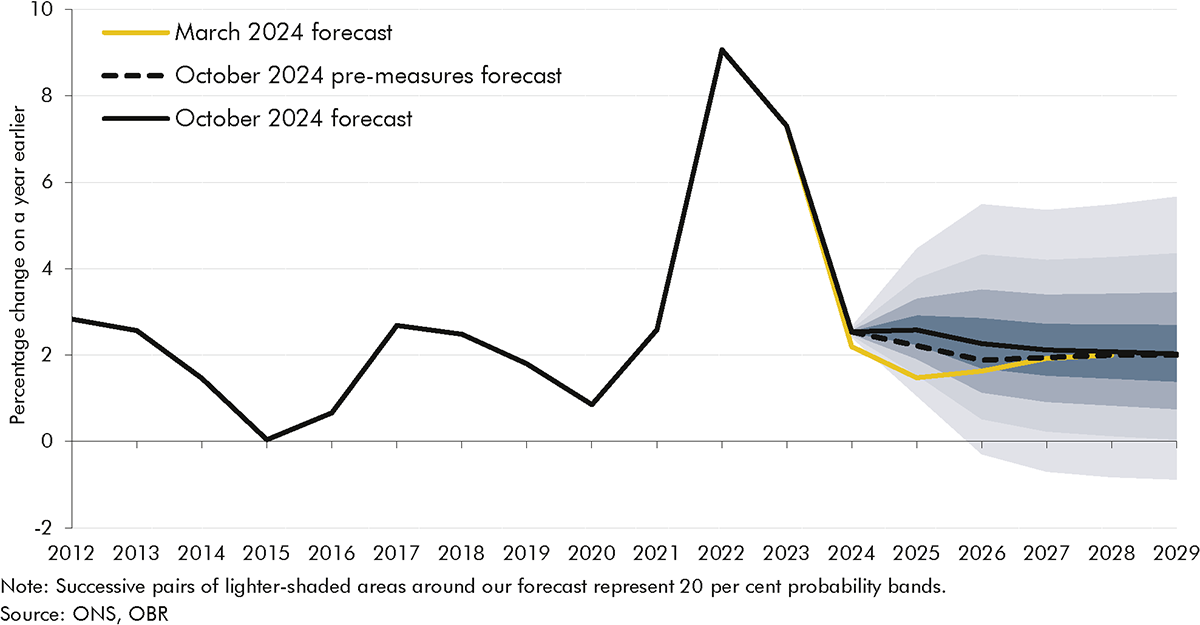

Inflation

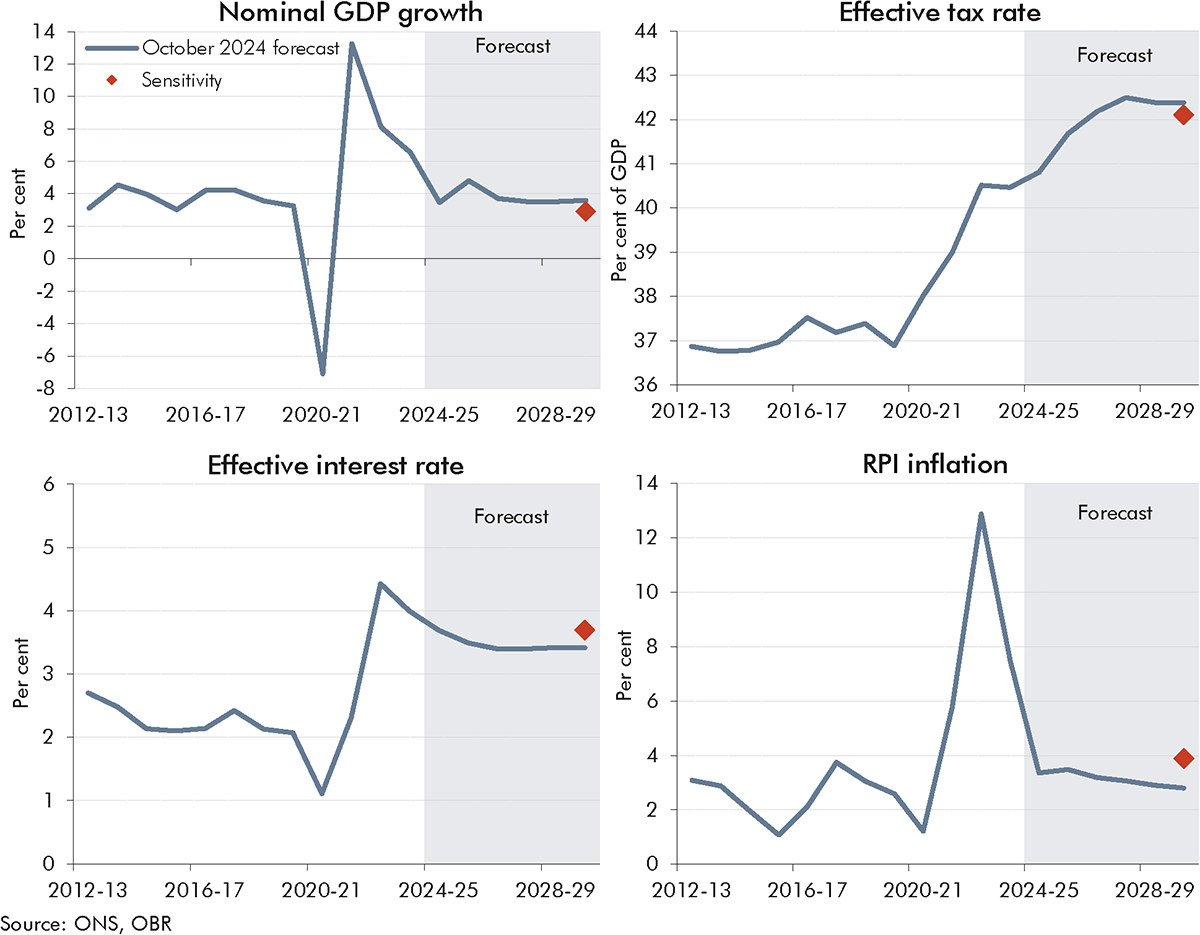

2.29 Having fallen from a 41-year high of 11.1 per cent in October 2022, annual CPI inflation is expected to remain close to the 2 per cent target throughout the forecast period. We expect a temporary rise, from around 2 per cent in the third quarter of this year, to an average of 2.6 per cent in 2025.[6] This is driven by higher gas and electricity prices, the direct effect of policies announced in this Budget, and the effect of a small positive output gap on domestically generated inflation. CPI inflation then gradually falls back to the 2 per cent target in 2029 as the positive output gap closes and energy price growth normalises. Compared to the March forecast, CPI inflation is higher in 2025 and 2026 by 1.1 and 0.6 percentage points respectively, and slightly higher until the end of the forecast. On average, just over half of the higher inflation in 2025 and 2026 is driven by our pre-measures judgements, with the rest due to the impact of policies in this Budget.

2.30 There is significant uncertainty around the forecast for CPI inflation. Domestically, if wage growth is less persistent than we assume this could drive lower inflation. There are also risks to the forecast from the external environment given the continuing war in Ukraine and the widening conflicts in the Middle East (see paragraph 2.10). Chart 2.10 illustrates that, based on historical forecast errors, there is roughly a one-in-five chance of CPI inflation being above 4.5 per cent or below 1.1 per cent in 2025.

Chart 2.10: CPI inflation

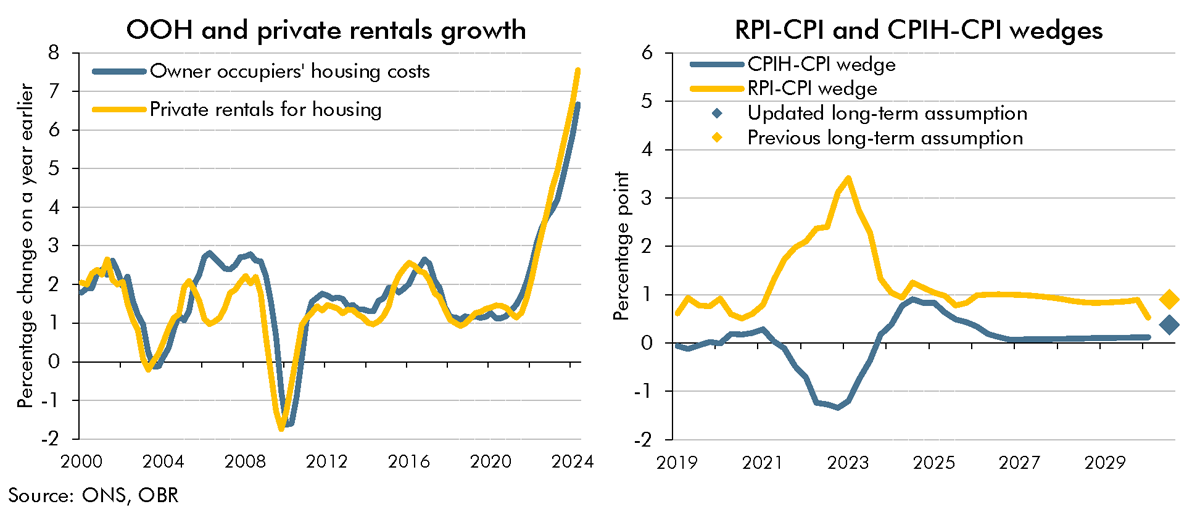

2.31 RPI inflation is forecast to average 3.5 per cent in 2025, before falling gradually to 2.9 per cent in 2028 and remaining broadly flat thereafter. Compared to March, the upward revision to RPI is slightly larger than our revision to the CPI forecast. This is due to our expectation of stronger growth in house prices and mortgage interest payments, which affect RPI but not CPI. We expect RPI inflation to fall sharply to 2.5 per cent in the first quarter of 2030, following the ONS’ current plans to align the methods of RPI with CPIH from February 2030 onwards (see Box 2.3).

2.32 The GDP deflator – which measures the price of all domestically-produced goods and services – is forecast to grow largely in line with CPI inflation throughout the forecast. We judge that the policy package will increase the level of the GDP deflator by around 1.3 per cent in 2029-30, of which around 60 per cent is due to higher departmental resource (RDEL) spending and around 40 per cent is due to the impact of the Budget on consumer prices.[7] Compared to our March forecast, the domestic price level is expected to be 2.6 per cent higher in 2028-29.

Box 2.3: The long-run difference between RPI and CPI inflation

RPI inflation is an important determinant in our fiscal forecast as it is used to uprate most excise duties and the principal value and coupon of index-linked gilts. RPI differs from CPI due to the way in which the indices are constructed, the goods and services included in the indices, and the representative population they cover. This creates a ‘wedge’ between RPI and CPI inflation, which we have previously estimated to be around 0.9 percentage points in the long run.a

In the future, movements in RPI will be aligned with the consumer price index including owner occupiers’ housing costs (CPIH),b which has been the ONS’s lead measure of consumer price inflation since March 2017. CPIH is identical to CPI, except that it also includes owner occupier housing costs (OOH) and council tax, which are significant expenses for many households. In practice, current ONS plans mean monthly growth rates in CPIH will be applied to RPI from February 2030, with the annual RPI and CPIH inflation rates fully aligning from February 2031 onwards. As our forecast horizon now extends to March 2030, we have started forecasting CPIH to produce our RPI forecast from the first quarter of 2030. To do so, we combine our CPI inflation forecast with our council tax and OOH forecasts:

Our council tax forecast is informed by known referendum principles, announcements by councils, and examining trends in recent behaviour. For the years in which policy is not currently set, our policy-neutral assumption is that levels will grow by 4.8 per cent.